Climate tech has undergone a visible evolution over the past few years, transitioning from a phase of abundant funding for innovation to capital more focused on large-scale deployments that approach being bankable and 'boring'.

Our annual report on climate tech investment trends examines this evolution, with a particular focus on venture and growth investment, which serve as crucial indicators. Venture and growth form the foundational layer of the climate capital stack, setting the stage for subsequent project finance and debt layers to finance the best solutions, and cross the valleys of death into broad deployment.

We've been meticulously tracking climate tech investment, deal by deal, since the term ‘climate tech’ emerged. But with the recent pullback in the overall venture market, we've expanded our scope to understand the dynamics and resilience in climate tech. Our report now includes extensive new analysis, going deeper into exits, graduation rates, investor activity, and trends across sectors and product types.

In 2023, a challenging macro environment marked by higher interest rates and a cautious private investment market raised the hurdles for deployment. Projects were canceled, investment declined, and companies who couldn’t weather the storm closed up shop. Investors and founders adopted a wait-and-see approach, anticipating a realignment of valuations with expectations and a stabilization of market uncertainty.

Now looking forward, interest rates are expected to come down, rules around policy incentives and regulation are emerging, and international competition has become a driving force for climate tech. 2024 is looking to be a critical year as climate tech continues its journey from the lab to large scale deployment.

Download this report with additional charts and commentary here.

💰 2023 investment: Funding in 2023 totaled $32bn, down 30% from 2022, although CAGR remains high since 2020 at 23%.

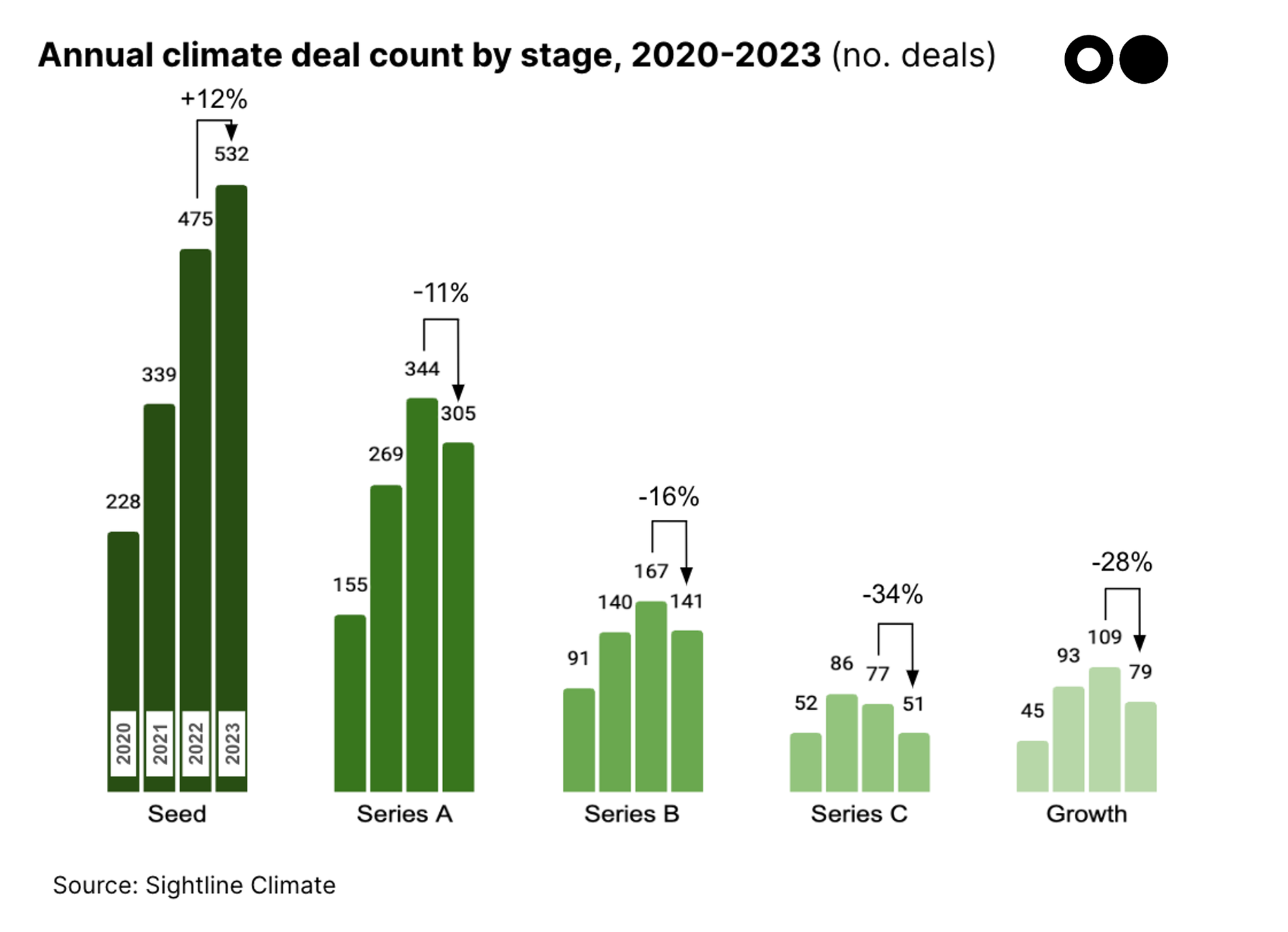

🤝 Deal count: Overall deal activity decreased for the first time since 2020, with deal count down 3% compared to last year.

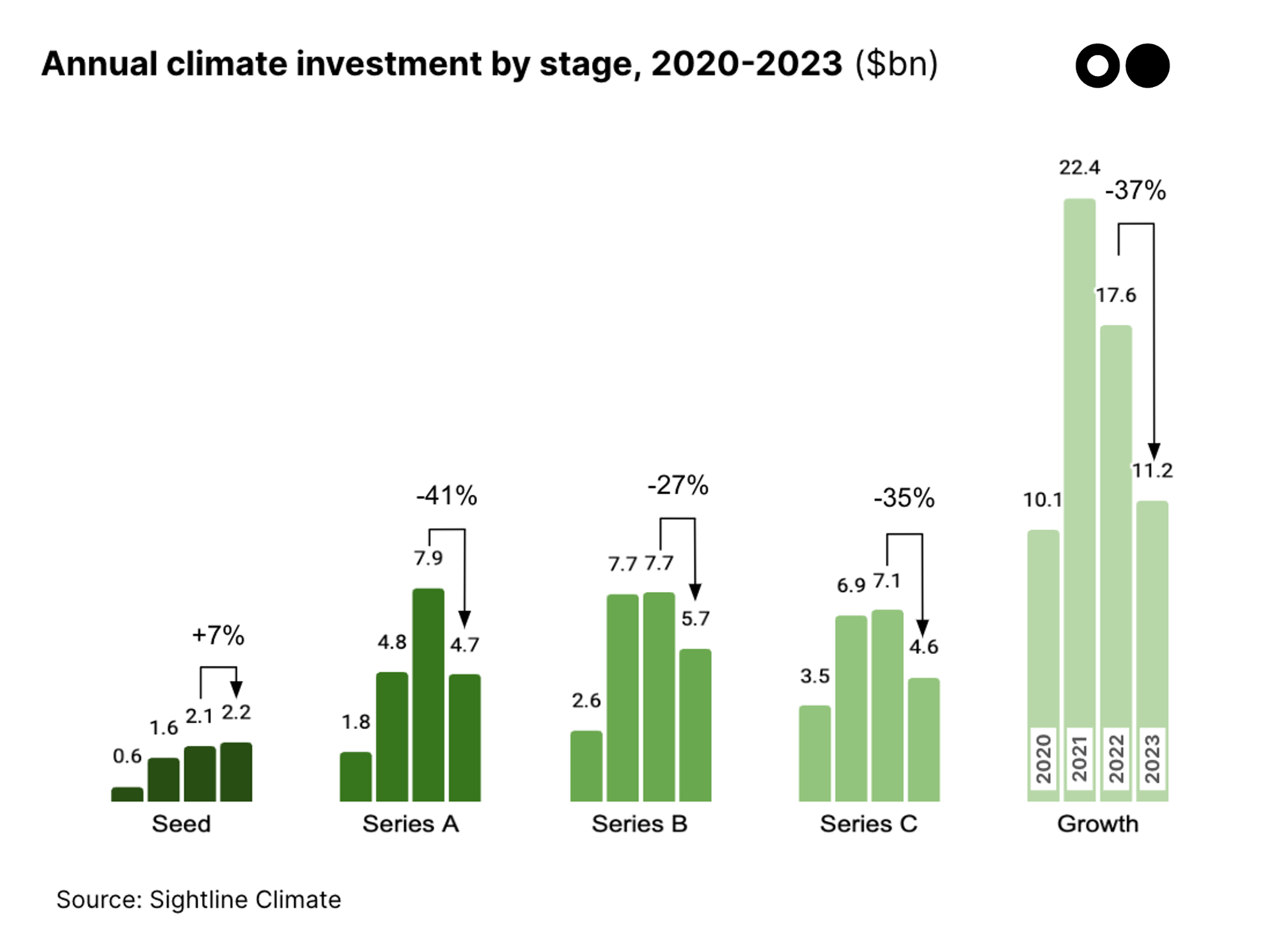

📉 Late: Growth investment fell 41% and Series C fell 35%, with deal counts for both down about 30%.

📈 Early: Seed and Series A deal activity tapered, marking the first decline in Series A deal count, down 11%, and a slower growth of Seed deals at 12%.

💸 Round size: Average deal size decreased 28%. As total deal count only fell 3%, smaller rounds were likely driving the overall market funding decline.

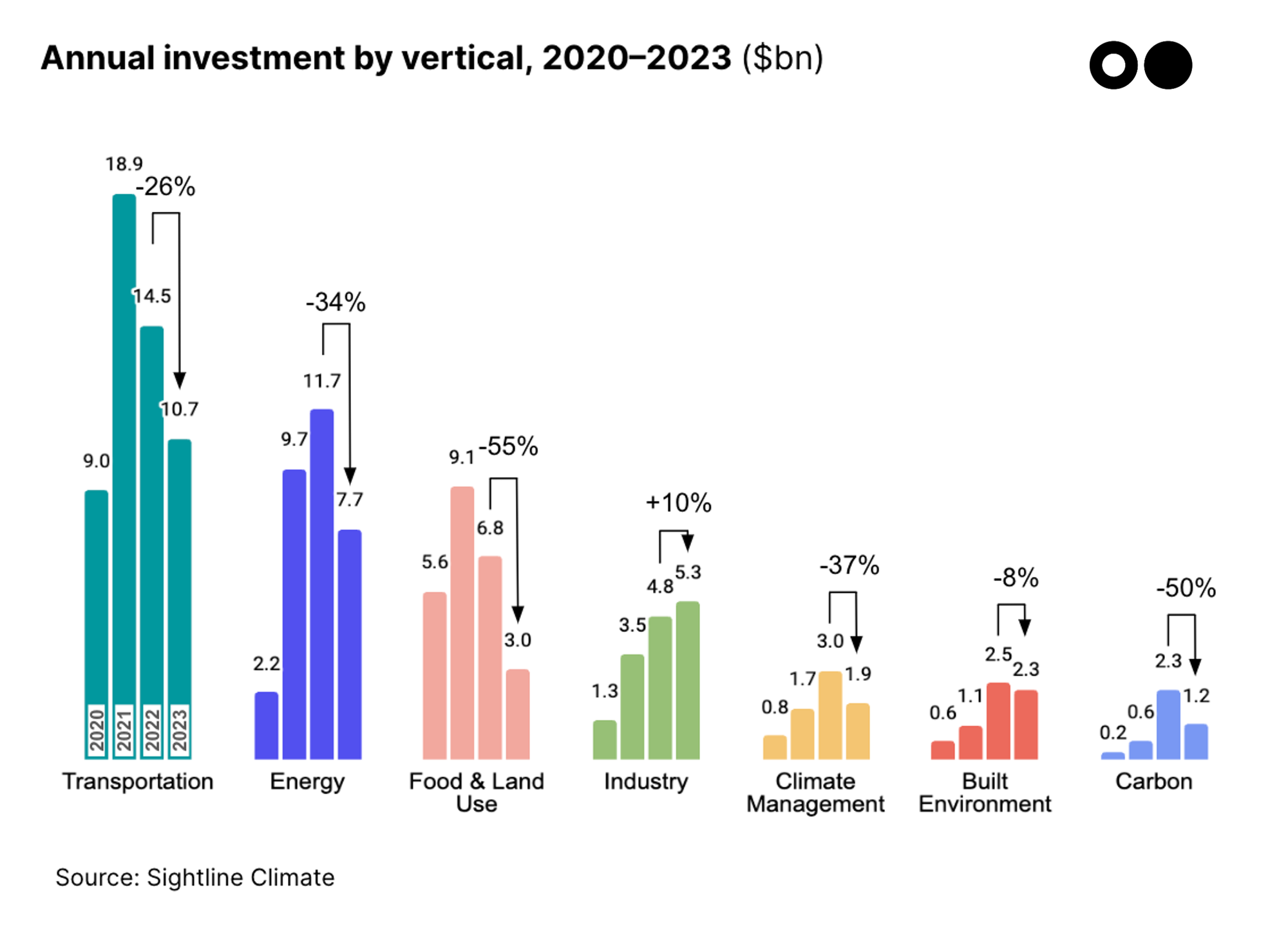

🚗 Vertical: Transportation and Energy investment declined, but remained on top. Food & Land Use fell dramatically, down -55%, and was replaced by Industry in the big three.

💤 Fewer repeat investors: The number of investors who have done 5+ climate deals in 2023 slumped 25% compared to last year.

🎉 Cumulative: Since the start of 2020, ~2,600 climate tech companies have raised $142bn+ of venture funding across 4,156 deals.

A note on methodology: This funding report captures only Venture Capital and Growth Equity deals that have been publicly announced through regulatory filings or press releases as of December 31, 2023. Please see the bottom of this post for full methodology and climate vertical definitions.

2023 Update

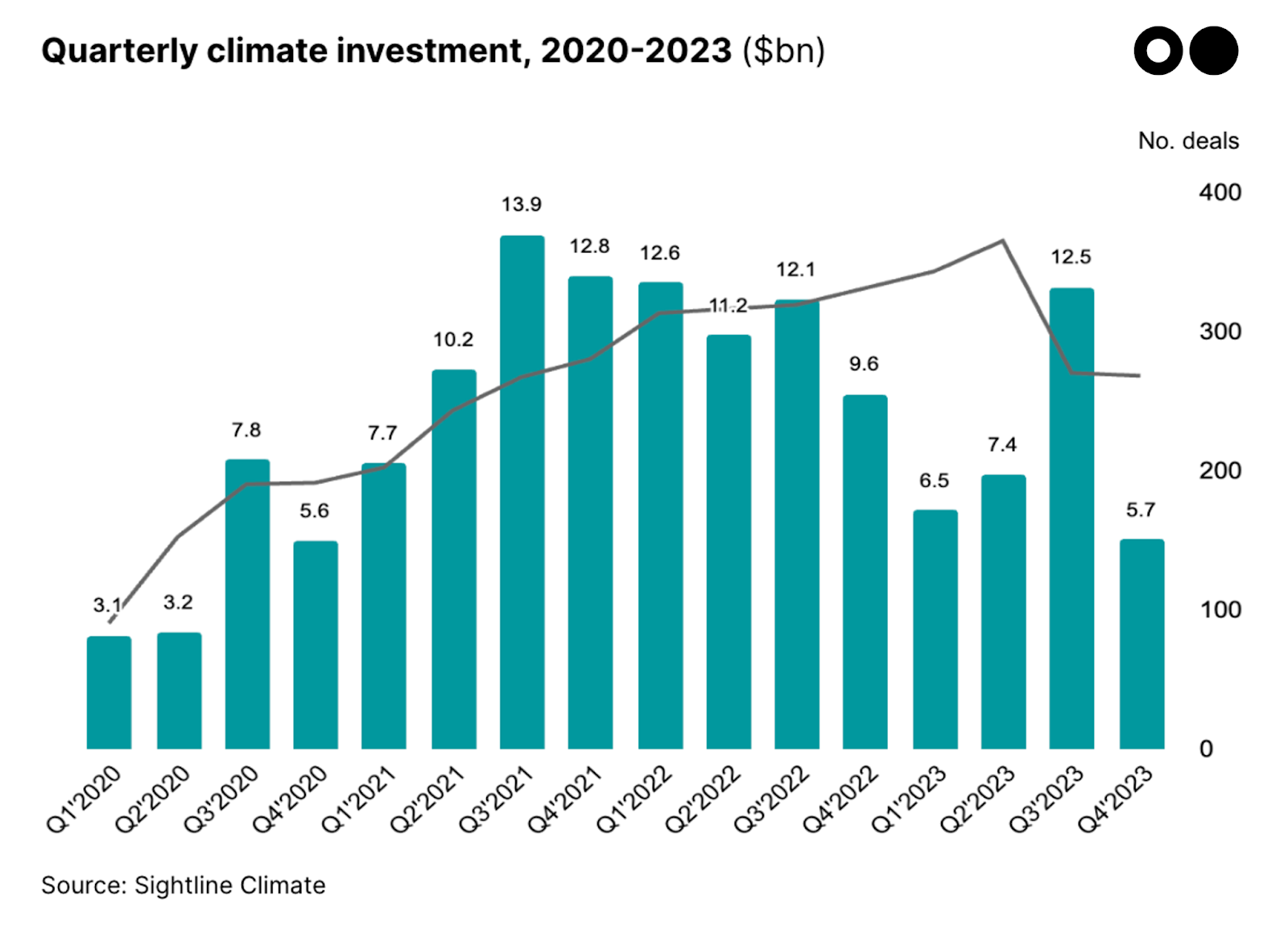

Climate tech venture and growth investment totaled $32bn in 2023, down 30% from 2022

2023 investment was down 30% compared to 2022, marking the first annual investment and deal count declines in climate tech since 2020.

There was a notable peak in Q3 at $12.5bn, boosted by mega rounds including H2 Green Steel and Ascend Elements, continuing Q3’s consistent top rank for quarterly funding.

Climate tech fell in line with the overall venture market. End of year reports aren’t out yet, but as of Q3, the overall venture market declined 39% YOY, similar to the 30% decline we’ve seen in climate tech this year.

Climate tech investment continues to grow, but slower

Total funding from 2020 to 2023 is $142bn. 2023 saw a 29% increase in the cumulative total.

The market is still warm, but cooling. CAGR since 2020 is 23%, but has slowed since the end of 2022 which was 32%.

Jury is out on whether investment will keep cooling or heat back up. Views on this for 2024 are a mix of bulls and bears, buoyed by expectations of large raises from companies and investors who held off in 2023, but pushed down by public market conditions and continued investor caution.

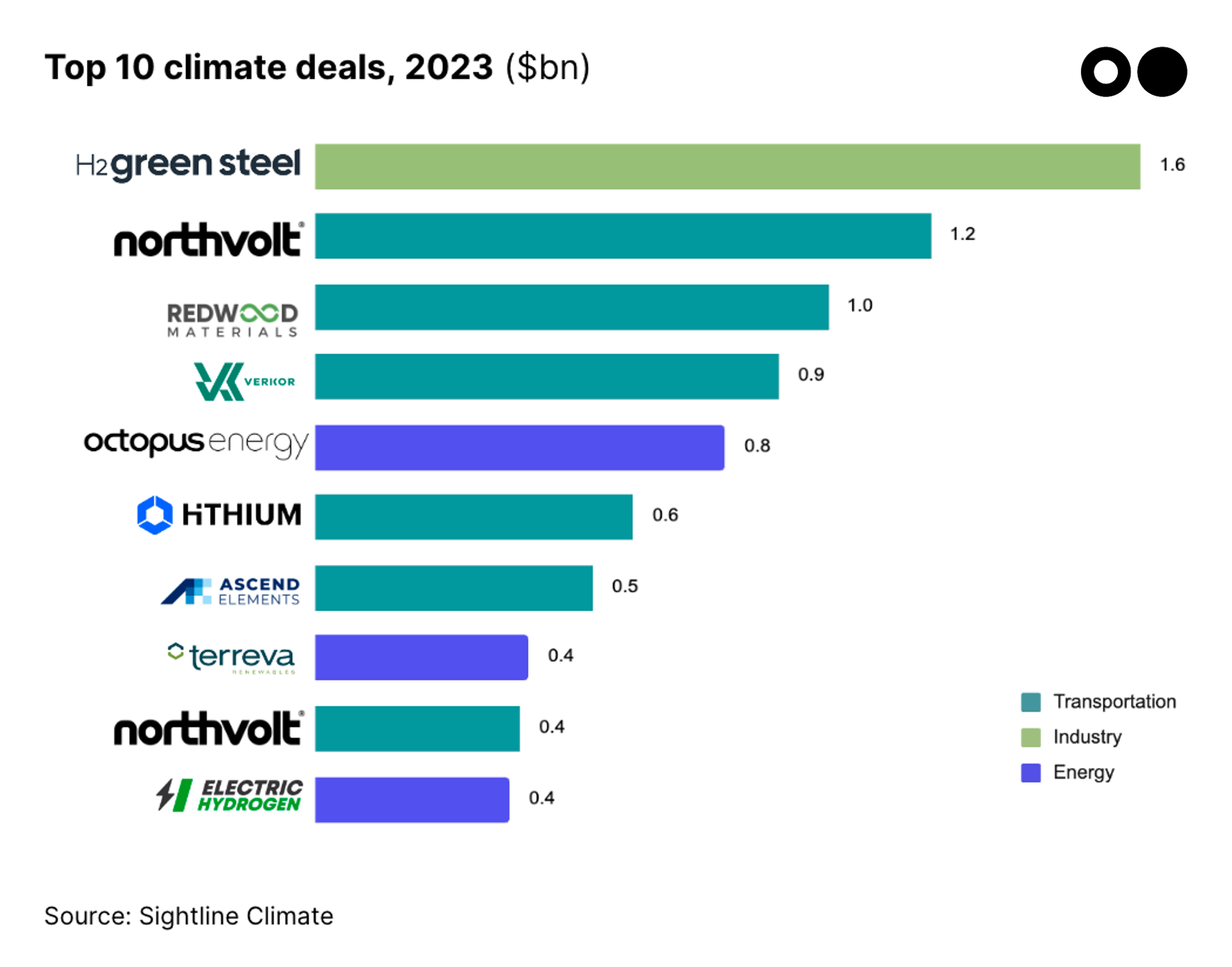

Batteries topped the charts for mega deals

Mega rounds were mega investment drivers. The 10 largest deals made up 24% of total climate investment in 2023.

The largest deals of 2023 were dominated by transport, in particular, batteries. Transportation accounted for 6 deals and slightly more than half the share of investment out of the top 10.

Marquee battery companies are diversified across major global markets. Northvolt raised $1.6bn over two rounds this year to scale battery manufacturing in Europe. Redwood Materials raised $1bn to build its US battery materials and recycling facility. China’s Hithium raised $621m to manufacture battery cells and storage systems.

Government funding catalyzed major private rounds. Of the top 10 rounds, 4 received government funding in the last two years. Redwood Materials received a $2bn loan from the US Department of Energy in Feb 2023. Verkor received a $717m grant from the French government in Sep 2023. Ascend Elements received a $480m grant from the US Department of Energy in Oct 2022.

Stage

Market freeze has reached early-stage investments

The macro freeze has been making its way to earlier-stage investments. Investment decline was felt across almost all stages, with an average 33% drop across Series A to Growth investments compared to an 13% increase in 2022. Series A investment decreased for the first time, a whopping 41% drop.

A slowing public market continues to hit Late-Stage Venture and Growth, both experiencing ~31% decline. Growth funding shrank as a share of overall funding, making up 39% of total funding in 2023, compared to its 50% share in earlier years. Many companies suffering valuation overhangs from previous earlier rounds are opting to extend runway and grow into their prior valuations rather than attempt to raise more large rounds.

Seed investment was the resilient exception, experiencing a 7% increase this year but noticeably tapered off relative to its 26% increase the previous year.

Seed and Series A deal activity tapered for the first time

Seed and Series A deal activity tapered. While early-stage previously grew at a consistent clip, 2023 marked the first decline in Series A deal count, down 11%. The number of Seed deals grew by 12%, but at a much lower rate than the 40-50% increase seen in both 2021 and 2022 as early investors raise their bar for quality over quantity.

Late-Stage and Growth continued to decline, amid higher expectations for milestones achieved and clear pathways towards profitability. The later the stage, the higher the drop off, with Series C and Growth deals both falling 30% or more. Rising interest rates and increased supply chain costs make it harder for companies to build early plants and projects, as demonstrated by recent project cancellations (Li-Cycle, NuScale), which may further deter investors from deploying late-stage capital.

Downsized rounds contributed to the investment decline

Downsized rounds combined with declining deal activity created a double whammy for investment decline. Overall deal size in 2023 decreased by about 28% following a 23% decline the previous year. Profitability has become increasingly important relative to growth, with investors and founders prioritizing smaller fundraises tied to milestones.

Series A deal sizes fell for the first time in four years. The average deal size for Seed investments dropped by 5% to $4.5m while Series A dropped 32% to $16.1m.

Continued declines occurred in Late-Stage and Growth, with a notable exception in Series C. Average deal sizes continued to fall, down 11% compared to the previous year, as mega rounds have largely dissipated since the SPAC and PIPE frenzy in 2021.

Series C deal sizes were the positive exception, growing by 11%, the only stage that saw an increase. This was mainly driven by a handful of large Series C deals from capital-intensive verticals such as Transportation and Energy, including Verkor ($905m), Hithium ($621m), and Electric Hydrogen ($380m).

Vertical

Everything was down, but not out, in 2023

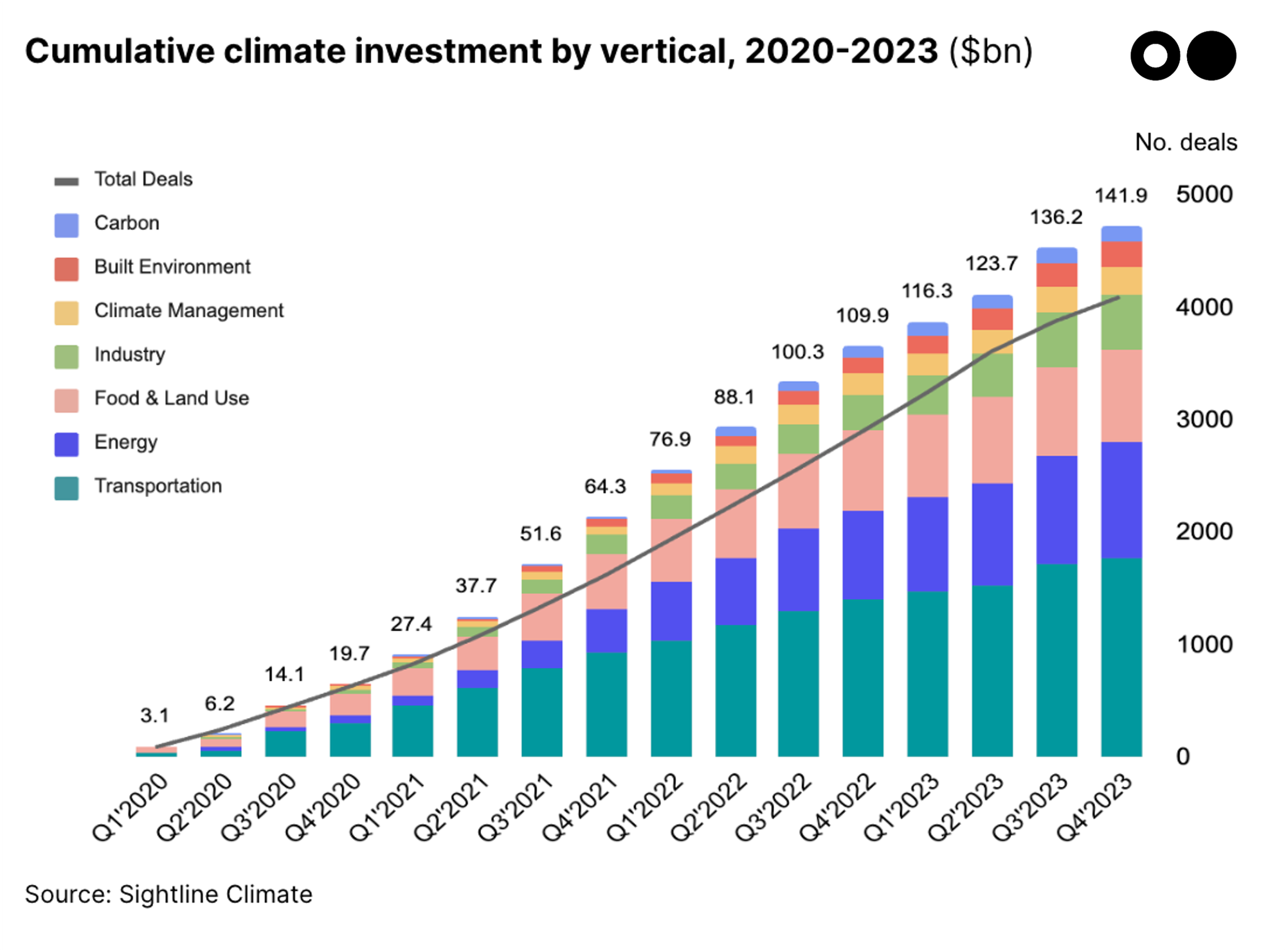

Industry was up in 2023, but everything else was down. The average drop across everything was 30%. Removing Industry, the average was 34% down.

Despite the downward trend, most verticals are still up on where they were in 2020. Food & Land Use is the only vertical whose investment was lower in 2023 than in 2020.

Food & Land Use replaced by Industry in the big three in 2023. Traditionally the big three were Transportation, Energy, and Food & Land Use, having raised the most funds each year. But Food & Land Use was replaced in 2023 by Industry, which received $2.2bn more investment. Should trends continue, Industry could overtake Food & Land Use in overall investment in one to two years.

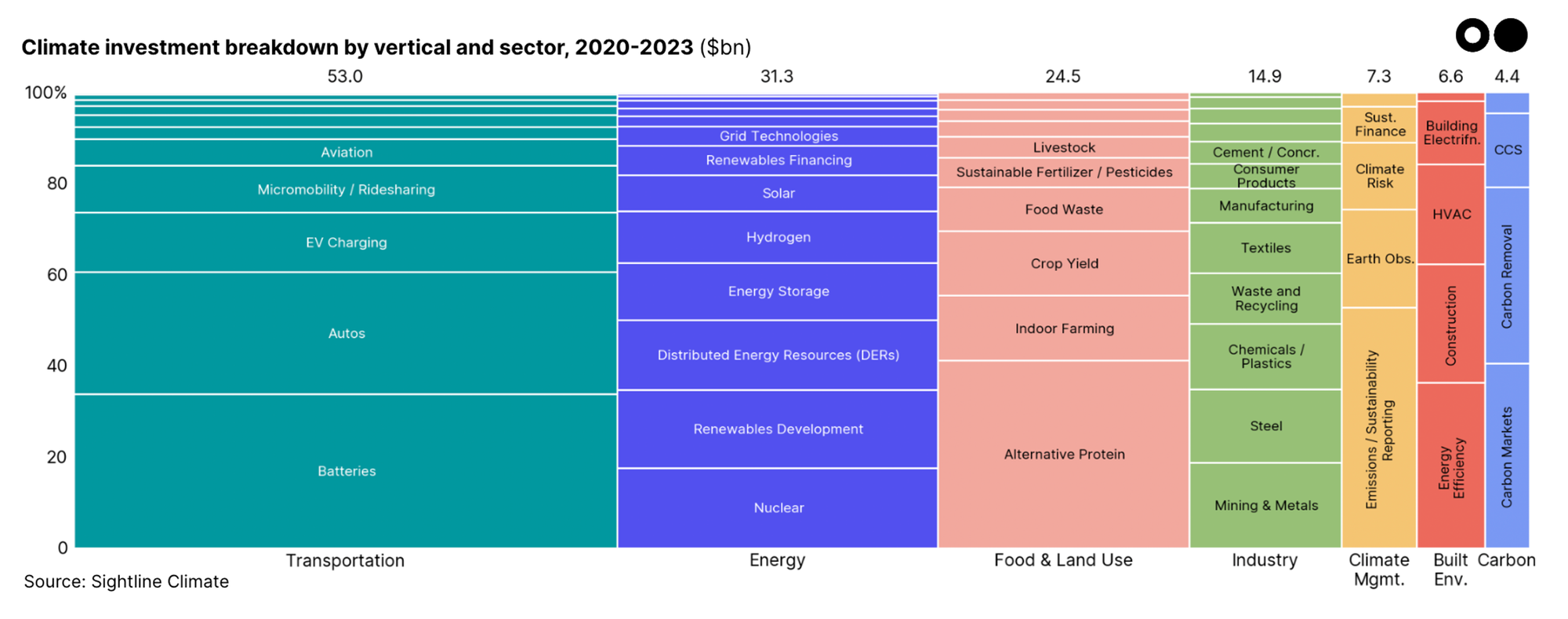

Transportation & Energy got 60% of investment since 2020

Batteries and autos received 23% of the total investment since 2020. Transportation as a whole accounted for ~40% of all climate-tech venture funding.

Despite its seeming popularity in the press, Carbon gets more headlines than funding. It received just 3% of investment, most of it for Removal and Markets.

The big three could see a change in 2024 or 2025, as Industry continues to attract capital and could overtake Food & Land Use in total investment. This could change if Food & Land Use sectors like Nature Restoration and Livestock continue to gain traction.

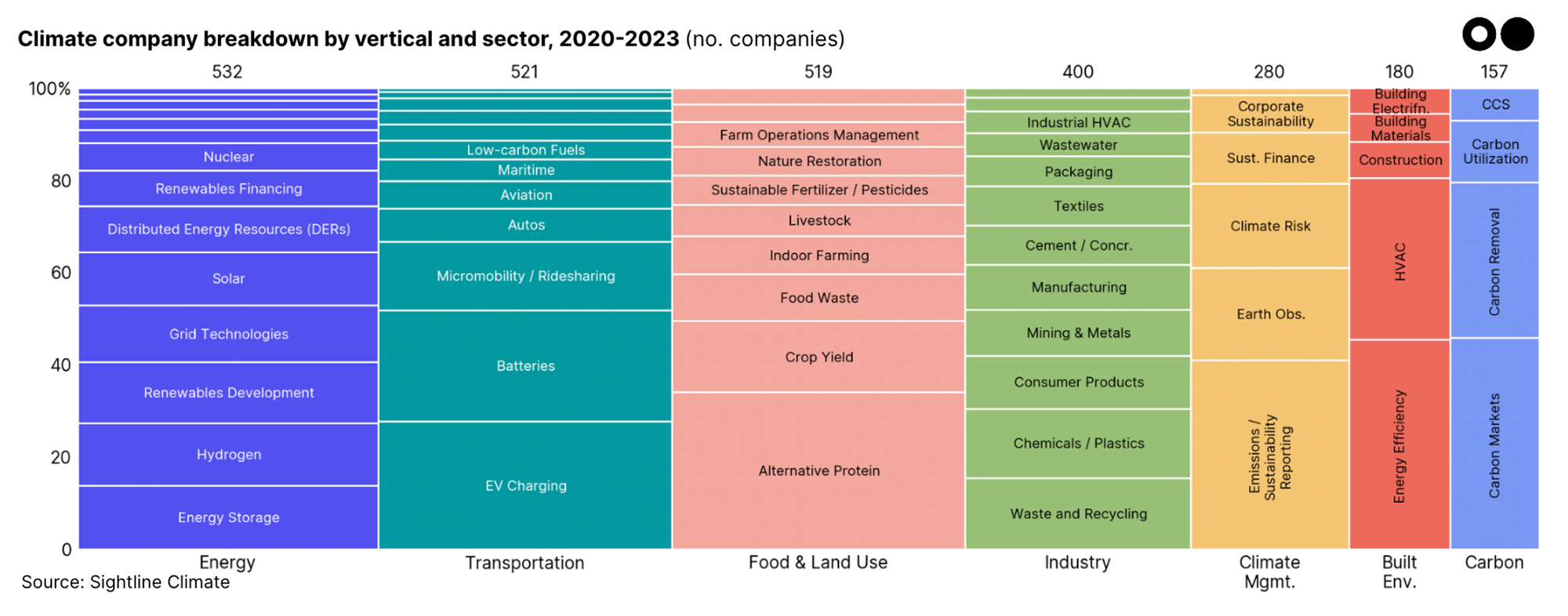

Almost 700 companies raised a first round in 2023

679 climate tech companies joined the ranks in 2023. At the end of 2022 we counted 1,910 active climate tech startups since 2020. By the end of 2023 that total jumped 36% to 2,589. So while total investment is down, activity in the climate ecosystem is way up.

Energy had the most movement, specifically in Hydrogen and Energy Storage. In our H1 Report, Hydrogen had the 4th most companies of any sector within Energy, but has now moved up to the no.2 spot behind Energy Storage, which rose from no.2 to to no.1. Those sectors might be crowded, but perhaps not overinvested – lots of companies relative to middling investment (previous chart) suggests big ticket deals could be coming.

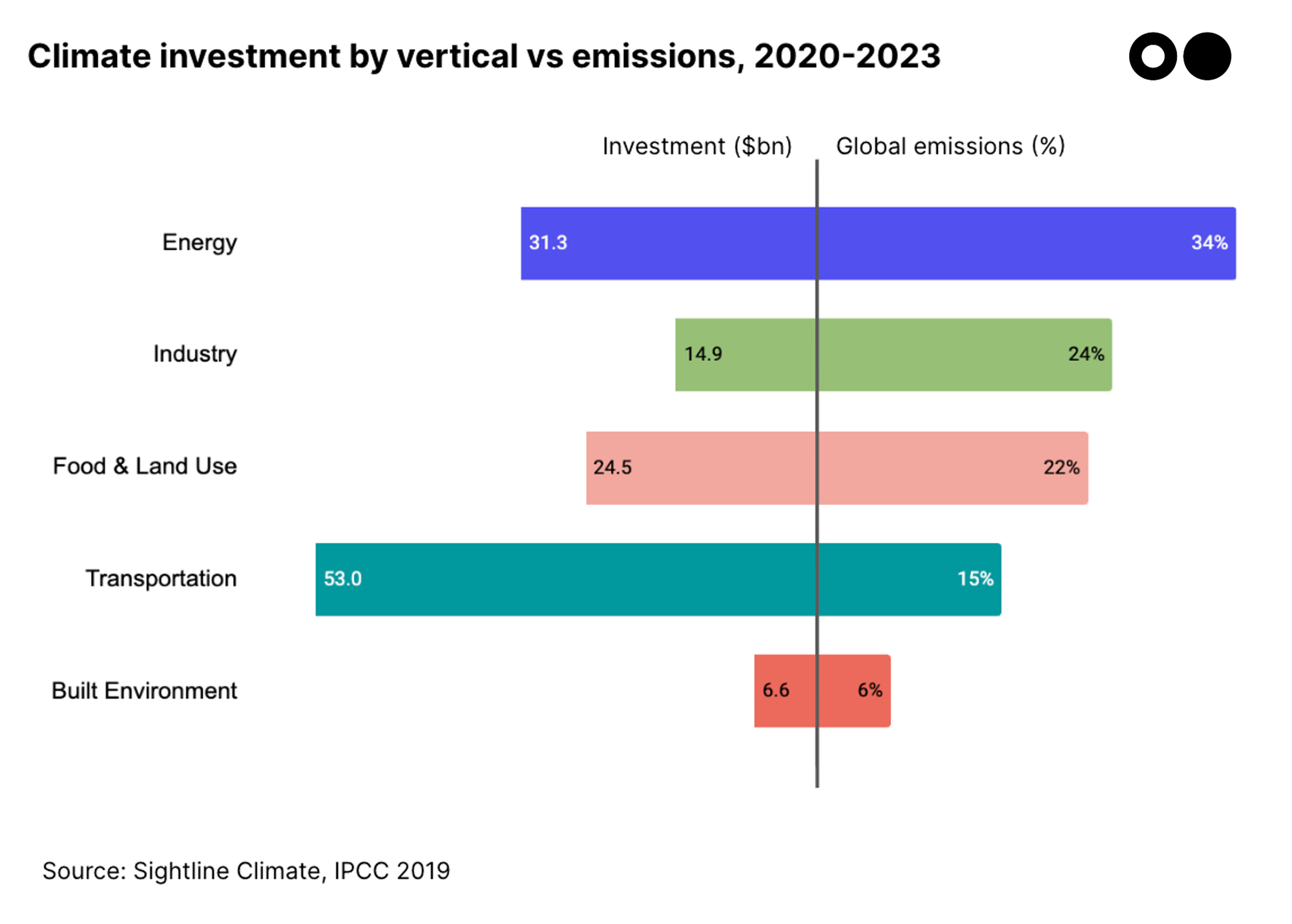

There is a mismatch between investment levels and emissions

Transportation is arguably overfunded relative to emissions, in a move to the familiar. Transportation accounted for 15% of total emissions in 2019 according to the IPCC, but received 37% of private investment from 2020-2023. During this initial wave of climate tech investment, investors jumped on the Tesla bandwagon and gravitated towards what they were more familiar with (cars).

Energy and Industry were both underfunded relative to emissions. Energy deals made up 22% of investment but 34% of emissions, and heavy industry was at 10% and 24% respectively. This could be due to the relative maturity of renewables and sentiment that decarbonizing energy was past the innovation stage. Whereas for Industry, capital-intensive assets with long replacement cycles and a slower pace of innovation have held industrial decarbonization back. However, in 2023 we witnessed a positive tick in the right direction, with increased investment in Industry and in non-renewable Energy sectors such as Hydrogen and Energy Storage.

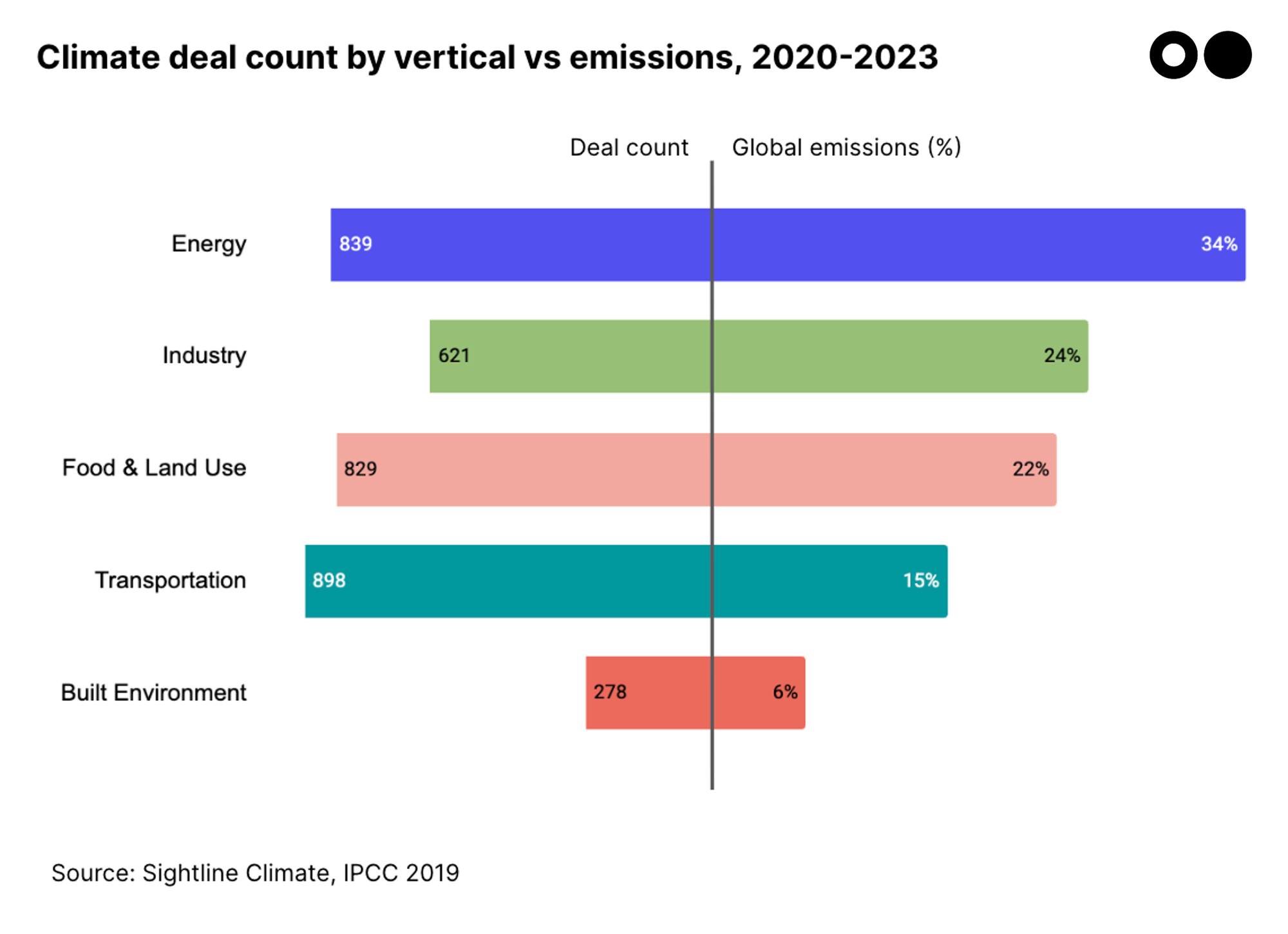

Deal activity is more closely aligned with global emissions

Deal activity relative to emissions is more balanced across all verticals. The top three emitting verticals were in the same ballpark for number of deals from 2020-2023, and the deal count for Industry continues to rise at the fastest clip.Transportation is still disproportionate in terms of deals relative to other verticals, contributing to 15% of emissions, but attracting 22% of the deals.

Product Type

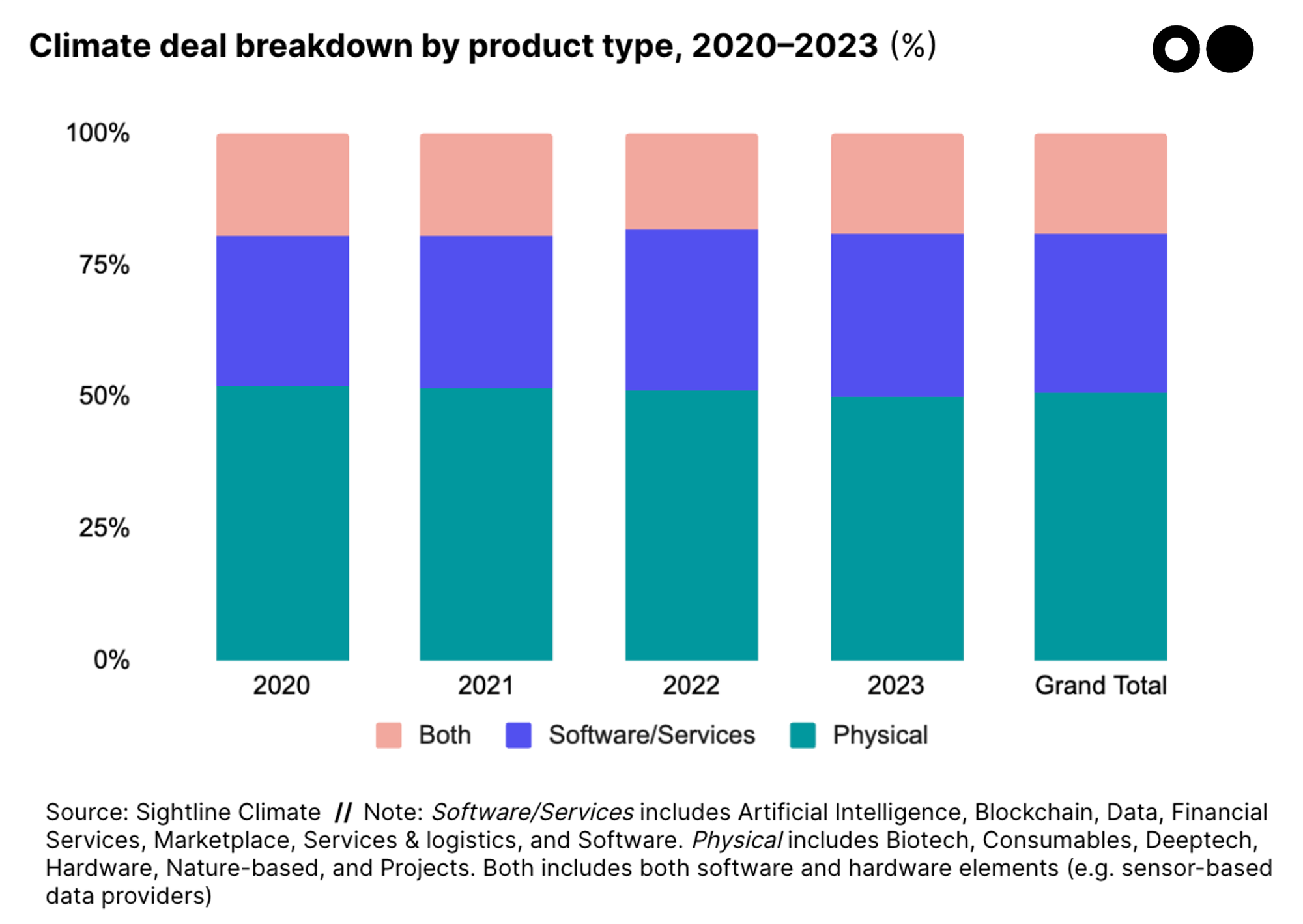

Capital-intensive ‘Physical’ climate tech companies made up half of deal activity since 2020

Capital-intensive ‘Physical’ climate tech companies make up half of deal activity. Despite traditional venture’s focus on software and asset-light business models, half of the deal activity in climate tech goes towards sectors requiring physical assets such as hardware, deeptech, biotech, consumables, or project development.

The share of Software vs Hardware has stayed consistent even in the market slowdown. In the last four years, Physical climate tech made up ~50%, Software/Services made up ~30%, and Both (using both Software & Hardware) made up ~20%.

Deals related to physical-based / hardware technologies faced a marginally higher decline. Physical-based technologies marginally underperformed in terms of deal activity compared to Software, declining 6% in deal count relative to Software’s drop of 3%.

Graduation Rates

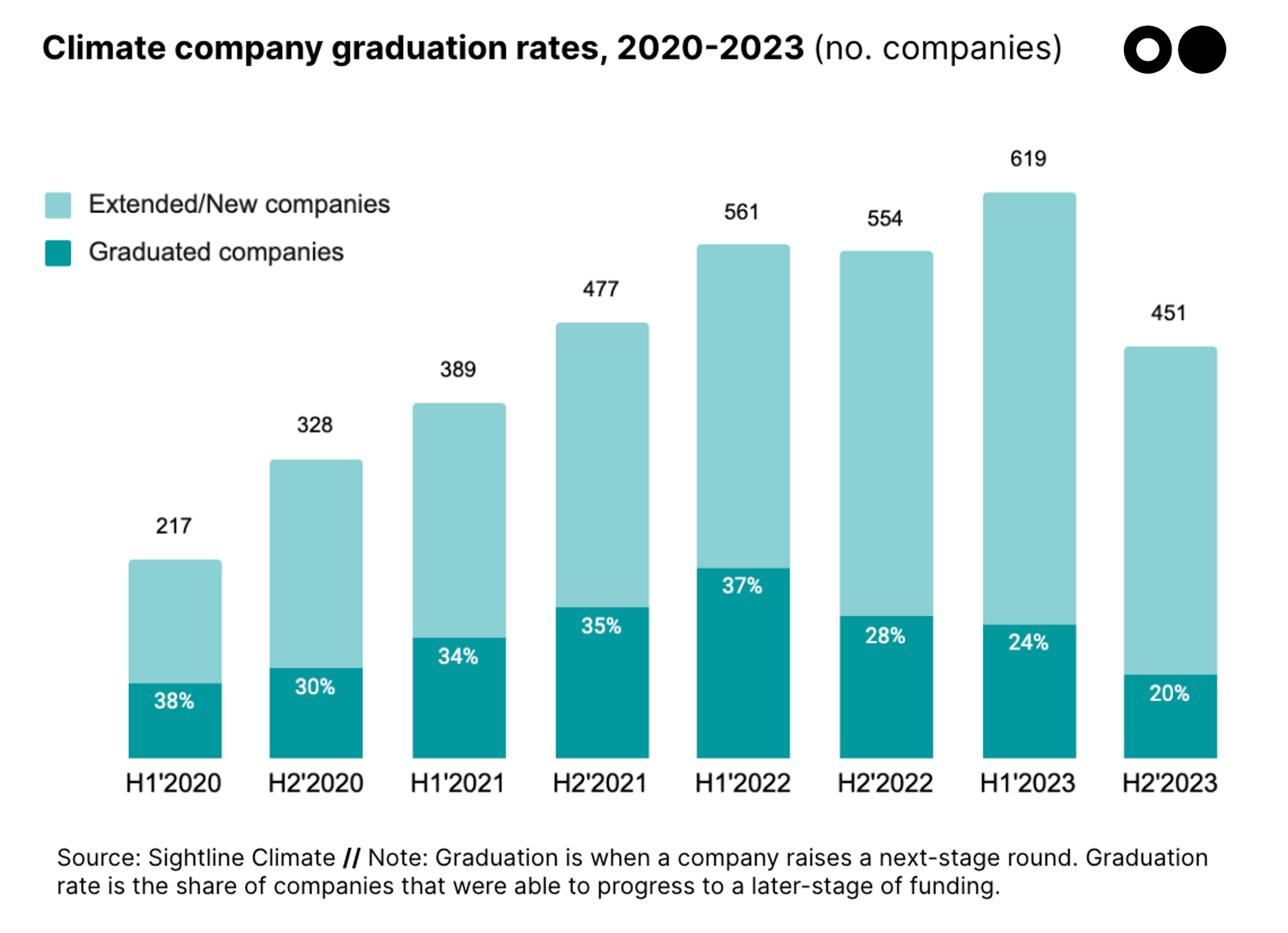

Graduation rates have been decreasing since 2022

Graduation rates have declined since 2022. The proportion of companies that were able to progress to a later-stage of funding reached 37% in H1’2022 at the peak of the market, but has since fallen to 20% in the most recent 6 months.

Declining graduation rates are a symptom of investment health. Lower rates may indicate several underlying issues, ranging from tighter funding conditions to an oversaturated market where too many startups are competing for investor attention. A decline in graduation rates could also suggest startups are falling short of the benchmarks required by later-stage investors.

Extensions and new companies make up a larger share. The total number of companies raising capital remains high, but a higher proportion of ventures are raising bridge rounds from existing investors to extend runway and avoid re-pricing, with new early stage companies still able to come to market.

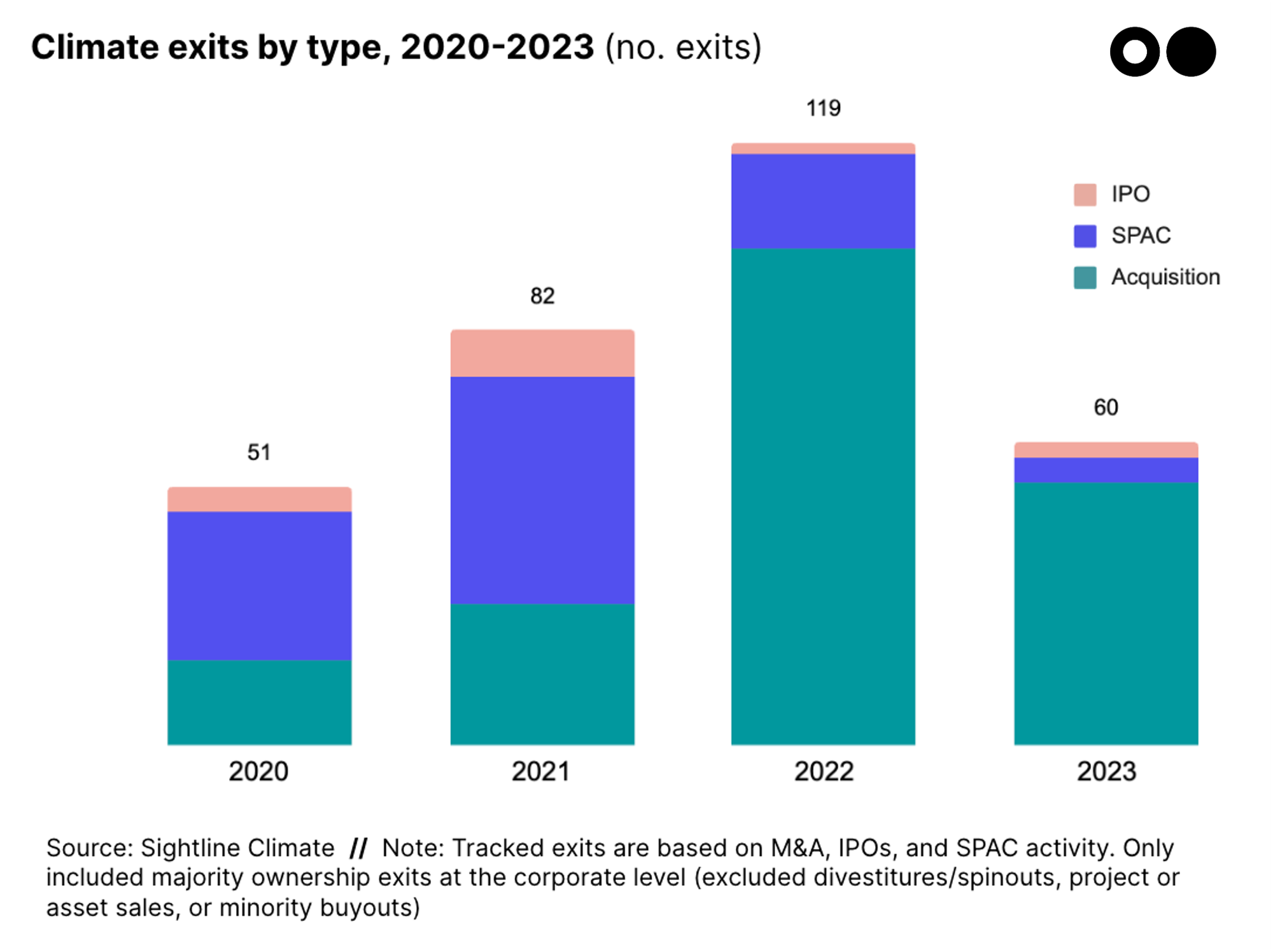

Exits

Fewer exits, with smaller tuck-in acquisitions making up the count

2023 cast a shadow over climate tech exits, with the total number of IPOs, SPACs, and M&A transactions down by about 50% this year compared to last. 2022 proved to be a bumper year for all types of exits, with climate tech investment reaching its peak last year.

SPAC boom fizzles out, down this year 89% from 2022 and 74% from 2021. The SPAC market has collapsed with attention shifting towards M&A activity, and climate tech companies straying away from the pre-2021 SPAC frenzy.

Over 80% of climate tech M&A deals were undisclosed. M&A activity continues rising, up 86% from 2021 levels but the majority flew under the radar with smaller, tuck-in acquisitions. Although not a hard and fast rule, undisclosed acquisitions – with no dollar amount listed for the deal – can often signal mediocre outcomes for the target. Given the early status of the climate tech market, many of these transactions may have been bargains for the buyers rather than successes for the sellers.

Corporates demonstrate their buying power, fueled by O&G majors

Big O&G companies inching into the energy transition game through acquisitions. Shell has bought seven climate tech companies since January 2021 – the largest of any acquirer in our analysis. It began pushing into the renewables market with Savion, Daystar Power, and Inspire Clean Energy. BP also bought five climate tech companies between December 2020 and October of last year, including Archaea Energy, Amply Power, and Open Energi.

Corporates sweeping up climate tech companies. Acquisitions are seen as a way for corporates to transition their offerings for the new climate economy.

Nasdaq has been busy buying up climate tech software companies, with acquisitions such as Metrio Software, Puro.earth, and OneReport.

Schneider Electric has acquired four climate tech companies that include EnergySage, EV Connect, Autogrid, and Zeigo, spanning across Energy, Transportation, and Climate Management.

BorgWarner focuses on integrating acquisitions into its automotive and mobility offerings with all three acquisitions, drivetek, Akasol, and Rhombus Energy in Transportation.

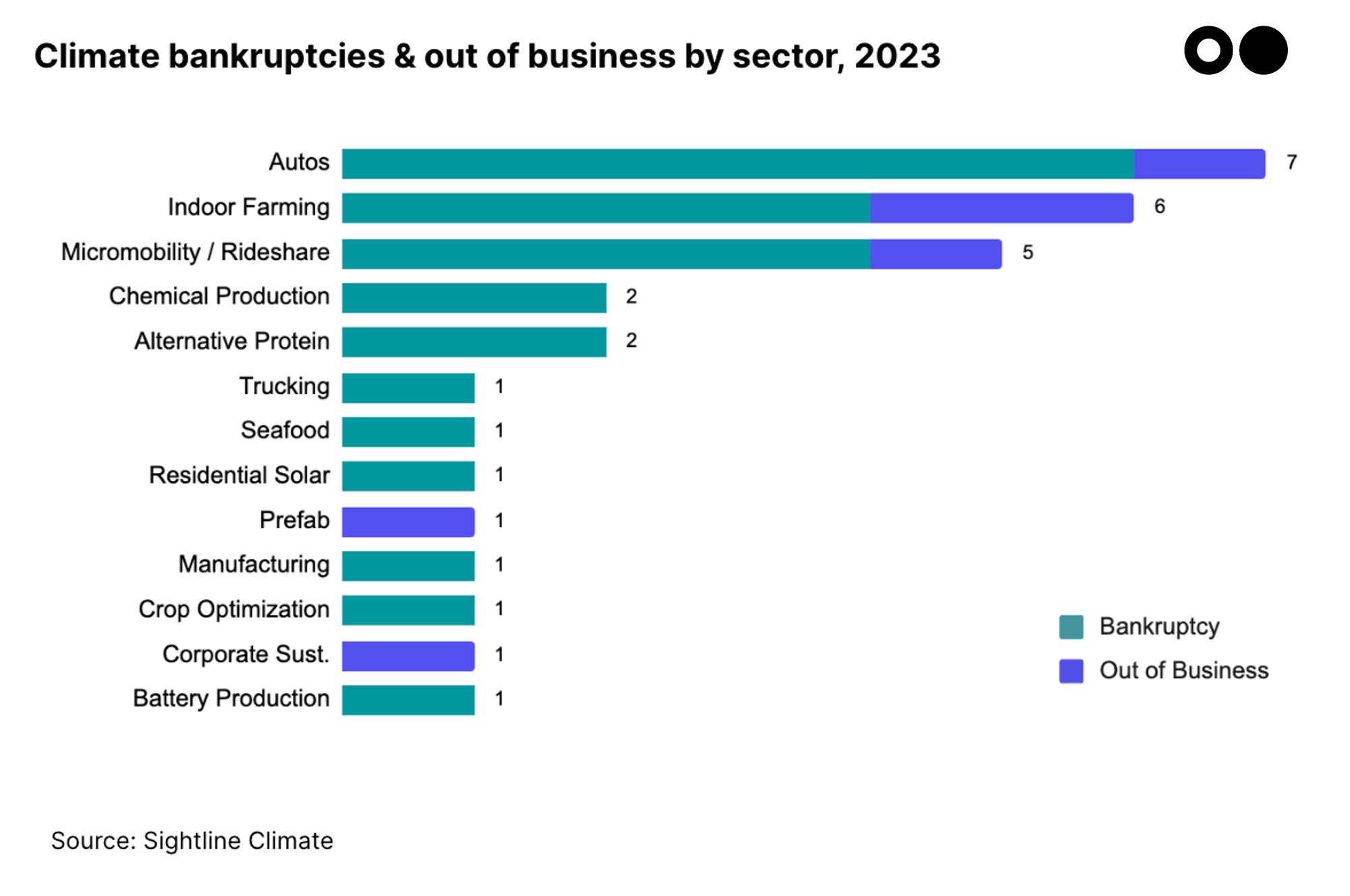

Autos has highest Bankruptcy & Out of Business count, followed by Indoor Farming and Micromobility / Ridesharing

60% of bankruptcies / out of business (OOB) are concentrated in Autos, Indoor Farming, and Micromobility / Ridesharing sectors. These three sectors faced supply chain disruptions, inflationary pressures on costs, and production delays.

Autos ‘top’ the charts. There were 7 EV bankruptcies / OOB in our analysis which include Proterra, Lordstown, and Electric Last Mile Solutions. Underlying factors included production delays and inability to secure finance for production plans.

Food & Land Use sectors made up 32% of all bankruptcies / OOB. IndoorFarming followed close behind EV companies with a count of 6. Companies such as Infarm, Upward Farms, and Aerofarms struggled to keep costs down, despite raising more than $1bn in total.

Investors

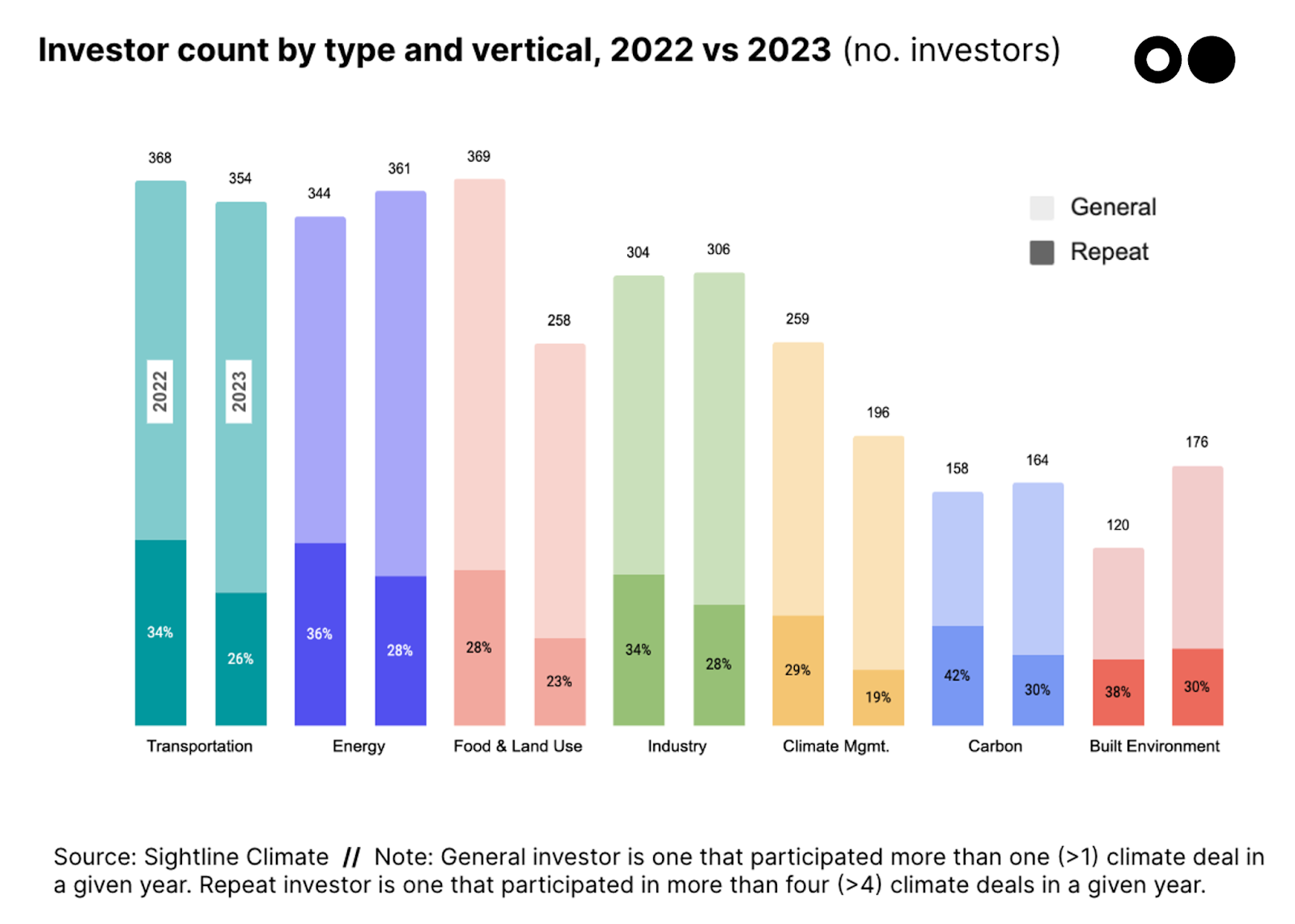

Fewer investors planting seeds in Food & Land Use

Repeat investors (5+ deals in one year) are down across all verticals as investors slow deployments. In 2022, these repeat investors accounted for 20% of general investors (2+ deals in one year), declining to 15% in 2023. In 2023, the number of general climate investors decreased by 4% to 833 unique investors, mostly due to a drop in investor interest in Food & Land Use.

Transportation and Energy continued to attract the most investors. But Energy beat Transportation for the first time, topping the leaderboard with 361 investors.

Industry and Food & Land Use also traded places on the leaderboard. Food & Land Use, which has historically attracted tourist investors more comfortable with consumer risk, experienced a massive 30% drop from 371 to 258 investors, mirroring the notable funding decline and bankruptcies in the vertical.

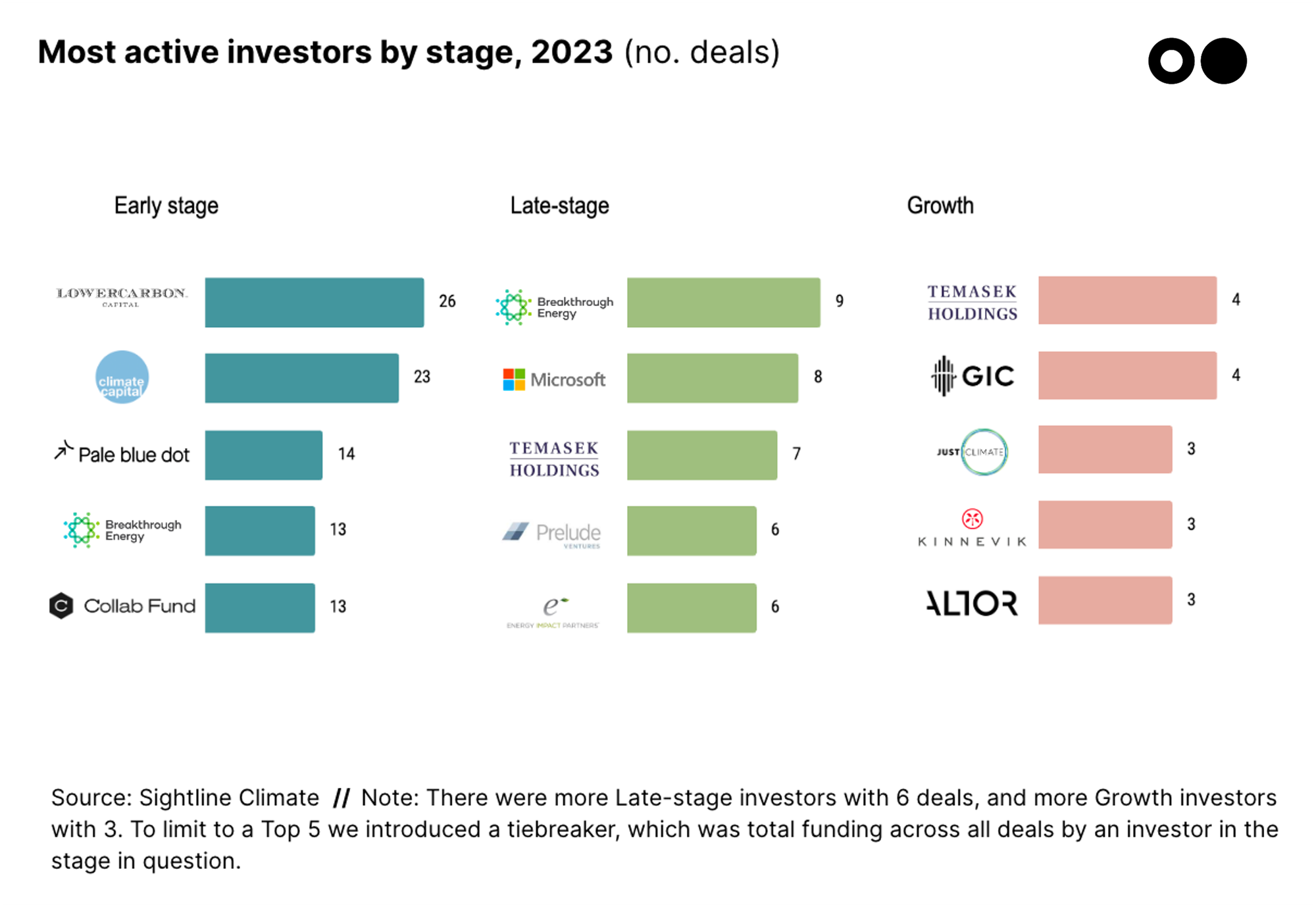

Climate funds led early rounds, institutional investors led growth

Climate generalists led in the earlier stages, with Lowercarbon and Breakthrough taking the lead in early and late-stage venture capital, respectively. Other climate generalists such as Climate Capital and Microsoft’s Climate Innovation Fund also took top spots.

Institutional Investors got involved in Growth including players who have been historically active in climate tech (e.g. Temasek, GIC, and TPG Rise) and newer entrants such as Goldman Sachs and Altor.

Corporates have been increasingly active in Late-stage and Growth rounds. Aramco Ventures announced their $1.5bn Sustainability Fund, and Microsoft, Exor, and SK Ventures have been active in the largest deals of the year.

Methodology

Asset class

This funding report captures only Venture Capital and Growth Equity deals that have been publicly announced through regulatory filings or press releases as of December 31, 2023. We also verified deals directly with the most active investors. Where other market observers may promote larger climate market sizes, we stay true to our Climate Tech VC name and carefully exclude:

We’ve long held that climate tech is a theme not an industry. Our definition of climate tech comes with two filters: 1) climate impact and 2) climate vertical. Companies must tick the box in at least one category for both filters in order to make the cut.

Climate Impact

To be counted as climate tech, companies must fulfill one or more of the following “climate impacts”:

Mitigation - Directly decarbonize across key emissions sectors.

Examples: electricity & heat, ag & land use, industry, transportation, buildings

Adaptation - Adapt to a changing climate with new products and economic models.

Examples: New insurance products, producing food to use, geo-engineering

Monitoring - Gather information / data about emissions or climate risks and impacts to generate insights.

Example: Emissions and sustainability reporting, climate risk and intelligence

Removal - Remove existing emissions from the atmosphere

Regeneration - Enhance general environmental “positive externalities” and “do more good, not just less bad”

Examples: Regenerative ag enhances biodiversity & sequesters carbon

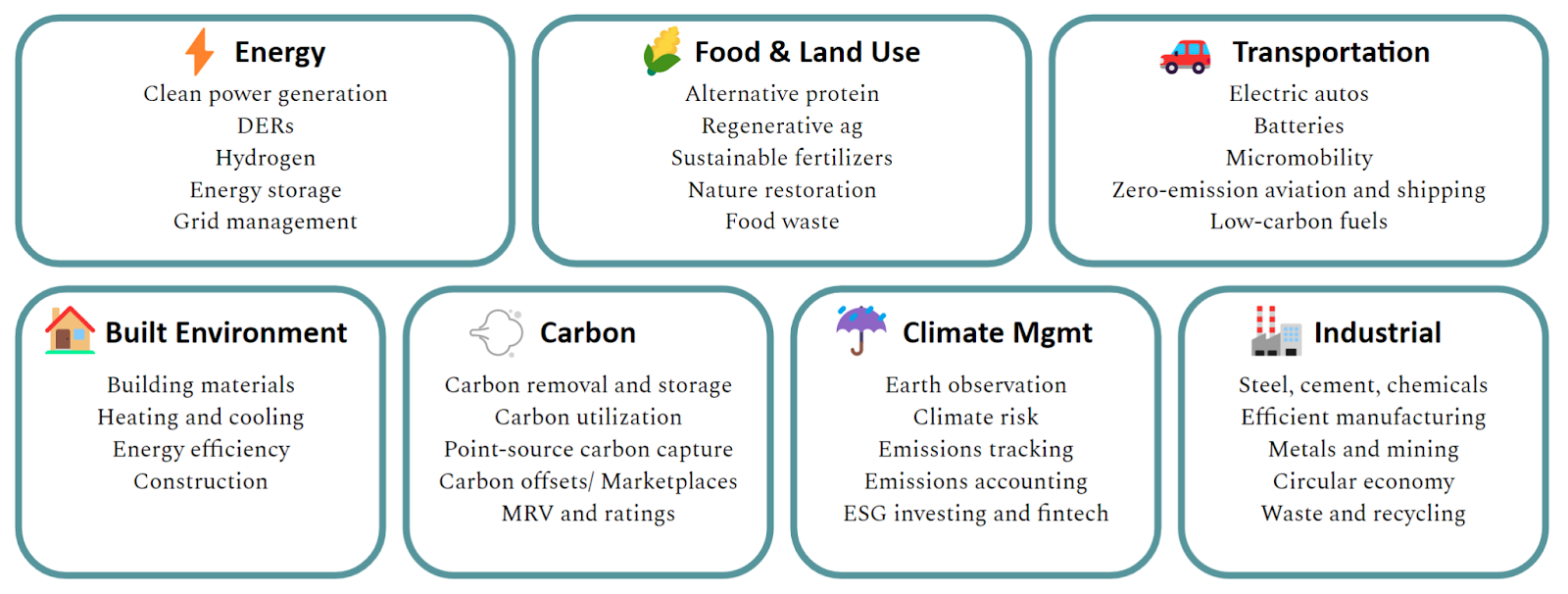

Climate Vertical

In addition to having climate impact, companies must fall into at least one of the seven broad climate verticals below. These verticals encompass 60+ sectors and 250+ technologies helping us mitigate, adapt, monitor, remove, and regenerate in our warmer and weirder world.

⚡ Energy - The electrons and fuel that power us

Sectors: new generation technologies (e.g., nuclear, solar, geothermal), energy storage, hydrogen and other low-carbon fuels, enabling renewables software, marketplace, and grid management platforms, DER and demand response tools, utility transmission and distribution services

🚗 Transportation - The movement of people and goods

Sectors: battery technologies, EV autos, EV charging and fleet management, electric micromobility and ridesharing, zero-emission planes, boats, and trains, urban public transport

🌾 Food & Land Use - The nutrients and resources that give us life

Sectors: alternative proteins, regenerative farming, vertical farming, sustainable fertilizer and animal feed, nature restoration and ecosystem services, remote sensing for crop yield optimization, autonomous farming equipment, water tech, and food waste reduction

🏭 Industry - The goods and raw materials we use every day

Sectors: low-carbon cement, chemical and plastics, steel, manufacturing, metals and mining, circular economy commerce, sustainable textiles and packaging, waste and recycling

☔ Climate Management - The data, intelligence, and risk associated with a changing climate

Sectors: emissions and sustainability reporting, earth observation through remote sensing, climate risk and intelligence platforms

🏠 Built Environment - The places we live and work

Sectors: sustainable building materials, low-carbon heating and cooling, prefab construction, energy efficiency, building electrification and energy optimization

💨 Carbon - The avoidance and removal of emitted carbon

Sectors: carbon offset marketplace and procurement platforms, carbon utilization, carbon removal and storage technologies, point-source CCS, verifiers and ratings enablers

NOTE: You may notice that some of our numbers are larger in this update than previous editions. We constantly update the dataset to have the most accurate data possible, including adding post-dated deals.

Have a different take on what’s driving these trends? Or questions about our analysis? Drop us a note at [email protected] if you’re looking to dig deeper into the 2023 investment numbers.

Special thank you to all the report contributors including Kim Zou, Mark Taylor, Mudit Agrawal, Jessie Bailey, Oliver Booth, Guy Cohen, Scott Gigante, Sophie Purdom, John Tan, and Sarah Wotus.

Newsletter

Newsletter