🌎 Two climate investors on raising in today's tough market

Q&As with Sophie Purdom, who just closed first-time Planeteer Fund I, and John Tough, who recently closed Energize Capital's mega-fund Ventures Fund III

How Forum Mobility is electrifying a big industry that you’ve never heard of

These days, there’s a subscription for everything. Forum Mobility is building a network of heavy duty charging depots around California’s ports and along common trucking routes, then supplies the trucks and chargers to drayage operators for a monthly subscription fee. Think of their solution as the first mile of fleet electrification. Doing so isn’t capital light - Forum just announced a hefty $400m JV with CBRE IM alongside their $15M Series A to electrify ports and trash the tailpipes of California’s 33,000 drayage trucks. We dive into drayage with CEO Matt LeDucq this week.

What, exactly, is drayage? And what’s the size of its climate problem?

Drayage is finally getting its time in the sun. This complex problem is much bigger than people realize, though simple enough to explain: containers arrive on ships into a port terminal where they’re lifted by big cranes onto the back of a truck. Those trucks drive a lot of miles shuttling to and from the port, moving a lot of containers - everyone heard about last year’s port congestion. To put the scale into perspective, where we’re focused in California, there are 33,000 registered drayage trucks driving ~1 billion miles per year on California roads. These trucks burn a couple hundred million gallons of diesel every year, emitting 3 billion pounds of carbon. Much of these emissions are concentrated in port-adjacent communities such as West Oakland, Wilmington - places with double the asthma and cancer rates of the broader LA basin.

Drayage is an essential backbone of the supply chain, yet on the flip side, 80% of trucks are run by mom and pop independent operators. It’s a particularly difficult and fragmented market to transition from diesel to electric, but so important from an efficiency, emissions, and health impact perspective.

Why is drayage so hard to decarbonize? Why is heavy duty fleet electrification so persistently challenging?

If you think about all the things that come into play to make zero emission heavy duty transportation cost-effective, there are a couple of factors involved. You’ve got high capital costs for trucks and relatively low maintenance costs, new charging infrastructure but lower cost of fuel, and then a maze of incentives like Low Carbon Fuel Standard (LCFS) credits, grants, tax benefits, depreciation, etc. When you put these all together it’s quite economical from a total cost of ownership perspective, and it’s a lower cost per mile to move goods with an electric truck, but it’s easy in theory but hard in reality. It requires cumbersome paperwork, the ability to monetize LCFS credits, and awareness of where this information sits. With 33,000 truckers moving goods in and out of California ports, most carriers aren’t on the California Air Resources Board website trying to figure out how to monetize a carbon credit. They don’t have analysts sitting in warehouses trying to put this all together, they’re driving all day and moving goods.

Our model of building large depots, filling them with lots of trucks, and synthesizing the financial inputs and incentives creates scale. We create staffed facilities with lots of chargers and lots of power, and we can scale those facilities on capital costs, operating costs, and financial optimization. Optimizing financially is what helped a lot of renewables achieve the lowest levelized cost of electricity, so by creating scale in third-party depots, Forum Mobility can deliver a value proposition to independent owner-operators and large fleets alike.

What part of this structure came first? How did Forum Mobility come to life?

I started in 2003 in renewables as an installation supervisor. At the time, what was happening in renewables was remarkably similar to what is now happening in electrification. There were a lot of pieces to the puzzle, and a lot of people who knew something big was coming but were trying to make sense of all of it. When I later led distributed generation at NextEra, I came across electrification in transportation, and had a very familiar feeling to what we were seeing two decades ago in renewables. The more you looked at it, the more you realized that billions of dollars in capital were going to be required to upgrade the distribution system, bring onsite distributed energy resources, and pursue actual electrification. I knew this was the next big thing, and that I’d kick myself if I didn’t take a leap. That was the beginning of Forum Mobility alongside my three other cofounders, Topher Wood, Bobby Batista and Tom Dodson. A lot of the learnings from those early decades in renewables are insights we’re applying now in a similar, yet more complicated space. It isn’t just a technological shift, but the development of a business model that will make the benefits affordable and accessible to customers, the same way that third-party PPAs or community solar did for renewables.

Walk us through how a drayage operator would engage with Forum from start to finish.

So let’s say you’re a trucking operator in Livermore, California, and you realize your 10 trucks will be out of compliance soon. You would come to Forum Mobility and say, “I need some electric trucks.” We’d learn about the type of lanes you run and your typical mileages per day, and help you select the right truck out of our different options. We’d then put you in our depot, either where your drivers start their day or right next to your yard, and you’d get a fully charged truck with a maintenance package and secure lot every day for a fixed price per month.

What is the back end technology and process?

Forum handles everything except making the trucks. Think of us as a traditional independent power producer in the sense that we get the land, permit the land, title the land, get power for that facility, manage the engineering procurement construction, operate the facility, and maintain the facility for our customers. The facility purchases the trucks from the OEMs after which we match the truck with the carrier based off of its best application. We do everything from getting the dirt, to putting the chargers on it, to sending the bills every single month.

Buying and leasing electric trucks is not a capital-light model. Why not just provide the charging infrastructure?

If fleets want to bring their own trucks, we are happy to provide just the charging. But we do what’s needed. Charging depots need high utilization in order to pencil out, and with about 80% of the drayage fleet consisting of independent owner-operators, for many of them the upfront capital costs of an electric Class 8 is still out of reach. They need a one-stop solution. We turn challenging cap-ex into manageable op-ex. Building is in our DNA as a company. My background is in infrastructure, and as a team, we’ve collectively put $20 billion of clean energy infrastructure in the ground. There’s plenty of people developing climate tech software and we need them to focus on that and do it well. Our goal is to create a value proposition that makes electric trucking immediately consumable for fleet operators and carriers.

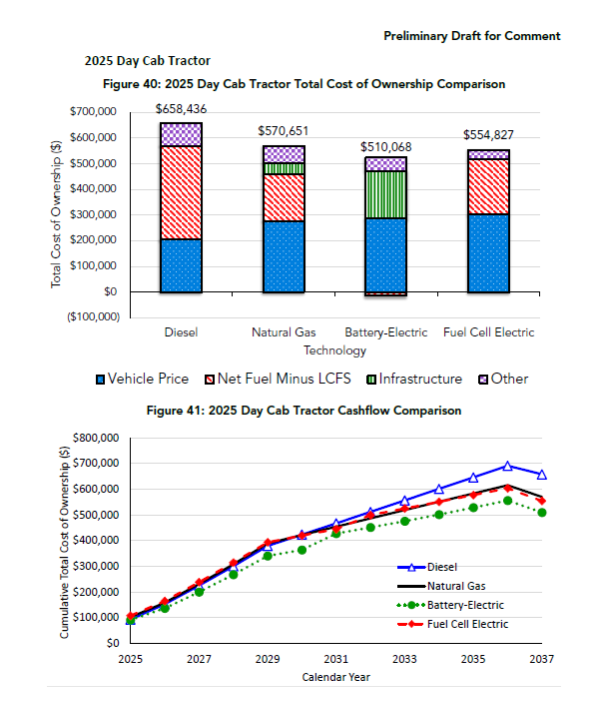

How do drayage fleet owners think about the TCO [total cost of ownership] of switching to electric? What are the critical assumptions that are factored in?

They look at the price of diesel, the price of trucks and the price of maintenance. You might also have a note on the truck, or be paying clean truck fees at the port. There's also just the fact that you're not going to be able to access the port at some point if your truck is older than 14 years or over 800,000 miles. A lot of this is competing against diesel, but a lot is just driven by the question of how people are going to get a nicer truck, or a zero emission truck, economically in the future.

Another really big part is that the people who own the goods that are inside of those containers – folks like IKEA, Target, Walmart, and Amazon – care deeply about Scope 3 emissions, which are notoriously difficult to manage. Our hope is that by getting somebody into an electric truck, we can bring them additional work from cargo owners who have ESG goals.

What do you say to the skeptics who question whether a defensible business can be built squarely on the back of potentially volatile regulation?

If you’ve worked in renewables over the past few decades, you’d probably disagree with that statement. Solar regulations and incentives, for example, have had their desired effect such that solar is now the cheapest way to generate new electricity. Staying power of regulations of course matters, but these policies don’t tend to stop once they’re in place. States don’t roll back their renewable portfolio standards, or roll back cap and trade. It's what the voters want, the state wants, and, in our case, it’s what the state needs. We need ports to be cleaned up. It's unacceptable to suffer health effects from living adjacent to a port. We’re confident in CARB’s due diligence and long term intent to jumpstart an industry delivering a lower cost per mile, cleaner air, and better financial position for truckers. That's a win win win.

Everything is some sort of regulated business model - whether it’s recognized as such or not. We saw a similar story with solar, which is now the bedrock upon which our global decarbonisation hopes rest. In transportation, drayage decarbonization through electrification is our beachhead approach. We're going to create the ecosystem and business models that create the scale to bring down costs that will then be exportable across not just other geographies, but other transportation sectors.

What are the key “carrots and sticks” that enable Class 8 electrification to be competitive with diesel? Similarly, how does the Inflation Reduction Act impact drayage?

The California Air Resources Board is starting with a heavy stick - the proposed Advanced Clean Fleets rule would require 100% of the state’s drayage fleet to be zero emission by 2035. That’s a lot. At the same time, the state is bringing a full ecosystem of carrots like incentives for buying trucks, incentives for installing chargers, and then incentives to help lower the cost of fueling. These are not going to be permanent, but it’s about creating a market that gains enough scale to reduce costs, and take off on its own. We have a lot of work to align the incentives with the speed and scale needed, as well as address utility interconnection bottlenecks.

The IRA delivered surprising wins for us. There is a heavy-duty tax credit of $40,000 per truck, and transferable tax credits of up to $100,000 for projects in disadvantaged communities. Collectively, the IRA made a lot of projects financially possible that weren’t possible a year ago. It’s a force accelerator and will help in places where state support is not as robust.

What was behind the decision to form a JV with CBRE Investment Management and what does the partnership entail? How did it come to life?

The technology here is pretty well established - the trucks themselves are essentially huge lithium-ion batteries on wheels and DC fast chargers are really inverters that run in reverse. At our core, we were building assets that look good to infra investors, which is different to other startups that are creating new technologies and have a lot of technology risk.

We still needed somebody who had a greenfield developer mindset, which isn’t every infra investor. You have to think about your investor’s appetite for real estate, technology, regulatory, and market risk, and make sure you’re dovetailing with someone who understands where you are and where the market is.

We found that in CBRE IM. They believed wholeheartedly in the electrification space and understood it well. There’s also no one who understands real estate better as an asset class. Homecoming is also committed to this space in a deep way, and they gained a lot of confidence in us by co-leading our Seed and seeing our financial discipline.

How did you think about the capital stack for financing this type of infra-heavy model? How can this be an exportable financing model?

The way we’ve capitalized the company is pretty special and creative. We had CBRE IM lead the Series A, with participation from all our existing investors and new investors including Amazon’s Climate Pledge Fund. The $15m Series A gave us the corporate equity to grow from a staffing standpoint.

We still needed capital to build the infrastructure, which requires buying land, lots of chargers, and trucks. This is why we created a joint venture with an infrastructure fund. Most of the time, infra investors like to infuse capital through the corporate entity. But one of the things we did creatively was raising a Seed round to test our model with the Hight Logistics project and validate the business and unit economics.

Investors had the ability to look under the hood and see the financial discipline that we used. This allowed us to create this JV structure that Forum Mobility manages, but is funded by CBRE IM to the tune of $300m and $100m from Homecoming Capital. We get a carried interest and fees to keep our business liquid through that JV.

So how does the joint venture with CBRE IM work?

In the words of CBRE IM, they “give us money, and we go do stuff with it”. We find quality assets, develop those in partnership with CBRE IM, drop those assets in, and those assets create cash. It's a really great structure where we’re incentivized to do well and run a good facility for the long-term. We’re going to be running these assets with CBRE IM for a long time.

What does success for Forum look like at scale?

Success looks like thousands and thousands of electric trucks on the road. There are over 100,000 trucks in the United States moving containers, we want those trucks to be electric and moving goods within our networks. In the coming year, we’re planning to get hundreds of trucks worth of facilities up and running or in construction. Then we can replicate that model in other countries and beyond non-drayage markets. We’re building networks for fleets to operate, and there’s nothing about Forum that doesn’t work for garbage trucks, municipal fleets, or ferry systems. We’re building networks of electrified transport, and starting with drayage first.

What do you wish folks understood about this space?

I want cargo owners to know that there is an option, and to ask their carriers to implement it. One of our investors, Andrew Beebe, invested in a company that sells algae-based feed to cows. When the algae company went to cattle farmers, the farmers didn’t care what the cows ate but only what In-N-Out tells them to feed the cows. So if you want cows to eat algae, you need In-N-Out to tell them to feed them algae.

There’s a strong parallel here. All these big cargo owners need to know that they now have a zero-emission shipping option. Walmart, Target, Ikea, etc. should be telling their carriers that this is what they want and carriers will want to do this too. The demand-side pull will be fundamentally market changing.

Interested in joining the team of Engines That Could? Forum is putting their fresh Series A capital to work building the team, and are particularly eager to meet their future Manager of Incentives and Finance Associate.

Q&As with Sophie Purdom, who just closed first-time Planeteer Fund I, and John Tough, who recently closed Energize Capital's mega-fund Ventures Fund III

A Q&A with Precursor's David Yeh and Mark1's Julian Ryba-White, new strategic partners in the ecosystem

A Q&A with the DOE LPO director Jigar Shah and Solugen CEO Gaurab Chakrabarti