🌎 Pushing the Frontier for carbon removal #301

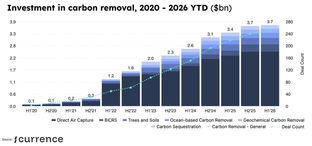

Inside the $915m bet on carbon removal's next phase

Happy pre-turkey Monday!

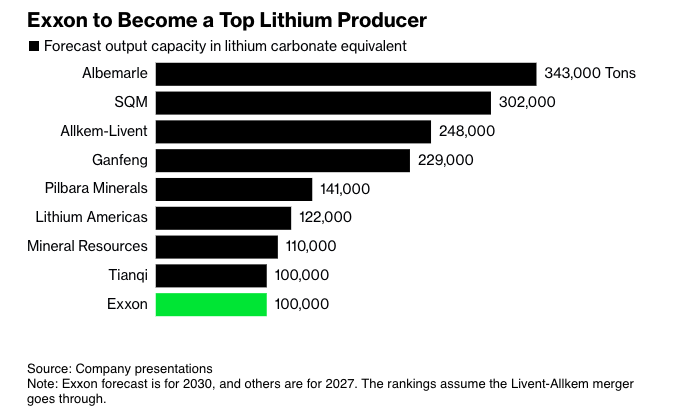

This week, we get nerdy mining ExxonMobil’s lithium announcement - is this lithium’s shale moment? Or a red herring? In either case, this wasn’t on our bingo card…

In the news, the British government passed new reforms to speed up interconnection, Colombia launched a $1B biodiversity fund, the US released $6B in funding for climate resiliency, and the US and China made modest progress on methane reduction at APEC.

In exits, Volvo buys Proterra out of bankruptcy for $210M (13% of its $1.6B SPAC valuation). In deals, more funding fuel for SAFs and batteries, with $191M for SkyNRG’s SAF facilities, $160M for NorthVolt’s battery manufacturing project, and $73M for Element Energy’s battery management technology.

We’re off this Friday digesting Thanksgiving, and won’t be publishing the following Monday as we ruminate on gratitudes. Thanks for reading!

Not a subscriber yet?

📩 Submit deals and announcements for the newsletter at [email protected].

💼 Find or share roles on our job board here.

Last week, ExxonMobil unveiled its first-ever lithium mining operation in Arkansas, marking its first major foray into lithium production. If all goes according to plan by 2030 the largest American O&G major would also be the 10th largest lithium producer in the world.

Low octane change

Don’t read this lithium play as a fundamental strategy swerve, — Exxon just shelled out $60B for Permian powerhouse Pioneer Natural Resources — but rather a hedge against an uncertain future for clean energy incentives staked on the upcoming US presidential race. A Republican win could mean engine failure for the IRA’s $7,500 EV onshoring credit, while a Democrat win would put Exxon in pole position. (In a full circle moment, Exxon scientists actually helped invent the lithium-ion battery, but abandoned it in 1976.)

DLEctable

Exxon is planning to race up the lithium league tables by blending their expertise in conventional drilling with more nascent direct lithium extraction (DLE) technology. They plan to use O&G drilling methods to access lithium-rich saltwater, then utilize DLE to separate lithium from the saltwater and convert it onsite to battery-grade material.

While still early, DLE could be the catalyst for lithium’s “shale” moment, and promises significant benefits compared to existing lithium production pathways like hard rock mining and solar evaporation. By filtering out lithium ions from brine, DLE can minimize water and land use, increase recovery rates (from 40-60% to 70-90%), and unlock production from lower lithium content brines.

Finish lines

Exxon isn’t the only one with a DLE horse in the race. The global race to extract lithium has already kicked off, with numerous DLE project developers and technology providers lining up.

Since Exxon hasn’t announced its DLE provider yet, it’s unclear if they’ll go at it solo or bring on a DLE partner. Early-stage DLE providers should keep an eye on Exxon as to whether they’ll be friend or foe in this race.

For more on DLE, check out the Sightline Climate Sector Compass on Lithium Extraction. (Not a Sightline user? Request demo here.)

⚡ SkyNRG, an Amsterdam, Netherlands-based Sustainable Aviation Fuels (SAFs) producer, raised $191M in Growth funding from Macquarie Group.

🔋 Northvolt, a Stockholm, Sweden-based lithium-ion battery developer, raised $150M in Convertible Note funding from CDPQ.

🔋 Element Energy, a Los Altos, California-based battery management system developer, raised $111M in funding including $73M in Series B equity funding from Cohort Ventures, Mitsubishi Heavy Industries, Edison International, LG Technology Ventures, and Prelude Ventures and $38M in debt from Keyframe.

🛵 Upway, a Gennevilliers, France-based e-bike reconditioning company, raised $30M in Series B funding from Sequoia Capital, Exor Ventures, and European Climate Fund Transition.

⚡ Leap, a San Francisco, CA-based DER aggregation platform, raised an additional $4M in Series B funding from Presidio Ventures.

💨 Deep Sky, a Montréal, Canada-based carbon removal project developer, raised an additional $42M in Series A funding from Brightspark Ventures, Whitecap Venture Partners, Investissement Québec, OMERS Ventures, and Business Development Bank of Canada.

⚡ Tenet Energy, a New York City, NY-based EV financing services platform, raised $30M in Series A funding from Nyca Partners and Debt funding from Silicon Valley Bank.

☀️ Aigen, a Kirkland, WA-based solar-powered autonomous robots developer, raised $12M in Series A funding from ReGen Ventures, New Enterprise Associates, Cleveland Ave, Incite, and Susquehanna Private Equity Investments.

📦 Le Fourgon, a Marquette-lez-Lille, France-based returnable beverage products delivery network, raised $11M in Series A funding from Id4, Teampact, and La Poste Ventures.

🚢 SWITCH Maritime, a Jackson, WY-based hydrogen and electric ferries manufacturer, raised $10M in Series A funding from Nexus Development Capital.

⚡ Zero Emissions Industries, an Alameda, CA-based maritime hydrogen fuel cells manufacturer, raised $9M in Series A funding from Trafigura, Chevron New Energies, and Crowley.

⚡ Optiwatt, a San Francisco, CA-based residential managed charging developer, raised $7M in Series A funding from Navitas Capital, Active Impact Investments, GV, Skyview Ventures, Urban Innovation Fund and other investors.

♻️ SuperCircle, a New York City, NY-based recycling logistics platform, raised $7M in Seed funding from Radicle Impact, Ulu Ventures, BBG Ventures, Earthshot Ventures, Blueprint Ventures .

💨 OCOchem, a Richland, WA-based CO2 into chemicals developer, raised $5M in Seed funding from TO VC, INPEX Corp, LCY Lee Family Office, MIH Capital Management, and Halliburton Labs.

💨 Rewind, a Tel Aviv, Israel-based ocean-based carbon removal developer, raised $5M in Seed funding from Mensch VC, Leap Forward Ventures, and Zora.

🌊 Mocean Energy, a City of Edinburgh, UK-based wave energy convertors developer, raised $3M from Katapult Ocean and Scottish Enterprise.

💨 CarpeCarbon, a Torino, Italy-based Direct Air Capture (DAC) technology developer, raised $2M in Pre-Seed funding from 360 Capital and CDP Venture Capital.

🚗 Proterra, a Burlingame, CA-based commercial electric vehicle manufacturer, was acquired by Volvo for $210M.

BlackRock, a New York, NY-based investment firm, secured $1B for its Evergreen Infrastructure Fund that invests in infrastructure for the energy transition.

SWEN Capital Partners, a Paris, France-based investment firm, closed its $633M fund that invests in renewable gas projects.

Material Impact, a Boston, MA-based investment firm, announced a $352M fund that invests in deeptech and material sciences companies.

Can’t get enough deals? See full listings and deal analytics on Sightline Climate

The British government passed new reforms to speed up the interconnection process. The new law will remove zombie projects unlikely to be developed, or stalled out due to its current “first come , first serve” policy and make room for viable projects to interconnect much quicker. If this works it presents a model for other electricity markets to follow in releasing queue bottlenecks.

In a boost for batteries, the UK also unveiled £4.5B ($5.7B) funding for British manufacturing to bolster economic growth, with £960 million earmarked for clean energy and the bulk of funding aimed at sectors like automotive and aerospace where Britain has a manufacturing history.

Colombia launched a $1B biodiversity fund aiming to close in 2026 drawing from several sources including carbon tax revenue and the federal budget. The fund will be managed by a trust that will oversee greater efficiency in distributing resources and allow projects to receive funding multiple times.

The Biden Administration released over $6B in funding for climate resiliency including a second round of $3.9B funding to the DOE to strengthen and modernize the US electric grid. Some other new funding highlights include $100M for water infrastructure resilience and $300M to help communities impacted by catastrophic flooding.

The US Treasury released updated guidance about the ITC provisions in the IRA. However, the agency has delayed the much anticipated Hydrogen Tax Credit Rule clarifications that were expected by the end of this year to as late as March 2024. The delay stems from a disagreement over whether to restrict the tax credits to hydrogen producers who use new sources of clean electricity, or to allow existing energy sources to qualify as well.

At the APEC Summit outside San Francisco last week, US President Joe Biden and Chinese leader Xi Jinping committed to setting more ambitious methane reduction targets. The only specific action named was to “advance” five large-scale carbon capture projects by 2030 and makes no mention of phasing out fossil fuels or of China’s controversial construction of new coal-fired power plants. However, given the countries’ strained relationship this modest climate collab could be a saving grace ahead of COP28, leaving the door ajar for further cooperation on climate.

Following on from spooky season for clean energy stocks, Siemens Gamesa, the renewable unit of Siemens Energy, suffered a net loss of €4.6B ($5B) for 2023 and is not expected to get back to break-even until 2026. The German government is coming to the rescue with a €15B ($16B) package to support green projects.

In another gust of faltering and strong wind, Orsted senior execs step down (CFO & COO) following cancellation of US projects with request for more funds for UK projects. Meanwhile, Octopus Energy Generation launched an Offshore Wind Fund aiming to invest €3B ($3.3B) both in operational offshore wind farms and developers building new capacity by 2030.

Reality check ahead of COP28, as a trio of major reports published on Tuesday show there has not been nearly enough progress to reduce global GHG emissions. A UN assessment of current country-level climate commitments found that if all commitments were met, global emissions may be about 5% lower in 2030 than they were in 2019. However, to limit global warming to 1.5°C above pre-industrial levels, they would need to be 43% lower.

A somewhat bright spot? New analysis from Carbon Brief concludes that China’s CO2 emissions are likely to fall in 2024, due in large part to clean energy capacity growing fast enough to cover their annual power demand increase for the first time.

Chevron’s $54B carbon capture project falls short for the seventh year in a row. The Gorgon CCS project failed to meet its target to store 80% of captured CO2 as new numbers indicate a capture rate closer to 33%, most likely due to pressure management issues caused by excess water in the subsurface reservoirs.

Gems galore in Breakthrough’s State of the Transition report: “There’s no transition without transmission” and “There are no silver bullets for climate change, but hydrogen comes close.”

Winners of £53M ($66.1M) UK SAF grants fly high towards the goal of 10% SAF supply by 2030.

Namibia courts the EU for $20B green hydrogen investment - more than its entire $12B GDP.

World's largest insect farm set to squirm with 100,000tons/yr of mealworms in France.

Truffles are becoming a climate casualty as conditions for “white gold” in central Italy dry up.

Walewashing. Big Oil spins whale deaths to stall wind power installations.

Lots of familiar faces (hi Jigar!) and some unexpected ones (hi Billie Eilish?) in the TIME 100 Climate list.

Speaking of Time 100 Climate leaders… Kenya's President William Ruto was listed, while the hunter-gatherer Kenyan Ogiek community is being evicted for carbon credits.

NY State sues PepsiCo for end-of-life plastic pollution along the Buffalo River as people toss their Gatorade bottles and Lay’s potato chip packs.

In possibly the best kiss and make up gift of all time, China sends new pandas to the US as a show of goodwill towards improved US-China relations.

Heat stress caused income loss equivalent to 4% of Africa’s GDP, when 2022 losses in Europe and North America were just 0.1% and 0.2% respectively.

JP Morgan released its 2023 Climate Report, but if you look at one thing, look at its Carbon Compass Methodology. It outlines how the bank plans to hit the IEA 1.5°C scenario for each of the sectors it serves – a new benchmark for climate reports! – and it’s really well laid-out and easy to read (also a new benchmark for climate reports??).

💡 Programming for the Planet: Submit proposals by Nov 24th, for this workshop exploring the use of programming in climate tech.

💡 Sustainability Open Innovation Challenge: Apply for the chance to win S$75,000. Information sessions will be held the week of Nov 27th, and applications are due by Jan 31st.

🗓️ MCJ Women in Climate Meetup: Join MCJ’s monthly meetup for women who work in, or want to work in, climate on Nov 29th.

️ 🗓️ Climate Capital Stack: Attend on Nov 30th to learn from and meet folks financing climate across venture debt, project financing, federal and state grants, and venture.

💡 Scale for ClimateTech: Apply by Dec 4th and receive vital support on your manufacturing process, and matching market demand.

🗓️ ️Clean Energy Investment Symposium: Attend from Dec 5th-7th to learn from experts and panelists, and participate in numerous networking events.

️🗓️ Investor Speaker Series: Join Greentown Labs’ installment featuring a startup founder and one of their investors, followed by a happy-hour on Dec 7th.

Founding Chief of Staff @Pika Earth

EVP, Finance @Closed Loop Partners

Analyst / Associate, Research & Innovation @Energy Impact Partners

Senior Associate, Vice President @Spring Lane Capital

Strategic Energy Manager @TeraWatt Infrastructure

Senior Construction Manager, Project Engineering , Sr. Director, High Volume Manufacturing Engineering @Form Energy

Director of SWE, Enterprise Account Executive @Regrow Ag

Mechanical Engineer, Electrical Engineer, Chemical Engineer @Seabound

Specialist, Project Finance , Manager, Renewable Energy Project Development @Intersect Power

📩 Feel free to send us deals, announcements, or anything else at [email protected]. Have a great week ahead!

Inside the $915m bet on carbon removal's next phase

A letter from the co-founders, Kim Zou and Mark Taylor

Newsletter

Newsletter