It took a container ship getting wedged in the Suez Canal and slowing our Prime delivery for us to collectively consider the scale of infrastructure needed to link global trade. We’re quick to rush to fix the things we see day-to-day (EV SPACs, anyone?), but shipping’s gotten less of the green treatment, in part because it’s out of sight and mind and in part because it’s really, truly “hard-to-decarbonize.”

But maritime’s moment to decarbonize has come, like it or not, as regulation has moved swiftly to turn the industry a few degrees greener. Even when existing solutions today are slim.

With the growth of e-commerce and demand for faster shipping (which means burning more fuel), maritime emissions increased nearly 5% between 2020 and 2021. Current decarbonization efforts alone set the industry on a course to increase emissions ~10% from today’s levels by 2050.

🚢

Some traits of the maritime industry make it especially difficult to cut down emissions, including:

-Heterogeneous equipment. With many different types of boats, different approaches are needed. - Long lifespans. Vessels operate for decades, which means a slower replacement cycle than other industries. -International waters. The inherently global nature of overseas shipping makes it challenging for individual countries to regulate maritime activity. - Infrastructure complexity. Even shipping companies looking to decarbonize today will struggle due to the lack of infrastructure for alternative fuels at many ports.

Rules Refresh

The shipping industry has undergone major regulatory shifts already.

Despite fears about cost increases and low-sulfur fuel availability, the change was a success in terms of decreasing pollution that contributes to ocean acidification and harms the health of humans and marine life.

The drop in sulfur oxide emissions, which ironically have a cooling effect in the atmosphere by reflecting light, has also played a role in record high ocean temps this year.

What’s new?

New regulations focused on CO2 are taking effect this year.

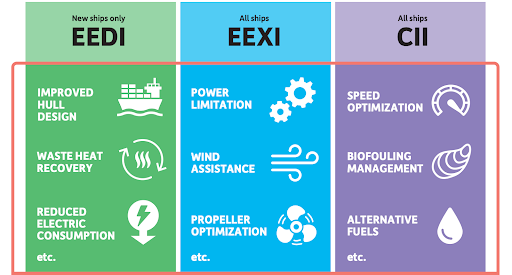

Energy Efficiency Existing Ship Index (EEXI) and Carbon Intensity Indicator (CII): Adopted in 2021 through the IMO, these measurements build on prior standards and became mandatory beginning Jan 1, 2023.

EEXI reflects the energy efficiency of ship design.

EEXI builds on the Energy Efficiency Design Index (EEDI) framework which was developed to help improve efficiency and decrease pollution in new vessels by requiring a minimum energy efficiency level per capacity mile of ships.

EEXI extends this to existing vessels and mandates that ships of 400 gross tons or greater meet the EEDI standards for technical efficiency (based on the design of the vessel, rather than operating methods).

Ships need a one-time EEXI certification that they’ve attained the required level of energy efficiency, and existing vessels may need to implement new technologies like power limitation or waste heat recovery to meet these standards.

CII reflects the energy efficiency of ship operation.

Ships larger than 5,000 gross tons must calculate their CO2 emissions per unit of nominal transport work (e.g., the ship’s cargo or passenger capacity across the total distance traveled in nautical miles) each year.

IMO will assign a CII rating, with A being the best, least carbon-intensive and E being the worst, most carbon-intensive. E-rated ships will have to submit a corrective action plan to achieve a C or above and D-rated ships will have a two-year period for improvements before they’re required to submit a corrective action plan.

This annual assessment acts as a “stick” policy to push shippers to decarbonize and ratings will become more stringent over time, with the threshold for each decreasing by ~2% each year—meaning ships that receive an A in 2023 could get a B rating in 2024 with the same CII score.

New requirements for maritime shipping decarbonization (Source: IMO)

2050 net-zero targets set by IMO

This summer, the IMO agreed on an additional industry-wide net-zero target for 2050—a major improvement compared with the previous goal of a 50% cut, but still behind in terms of Paris Agreement targets.

Next year, the existing EU MRV system will be applied to 40% of shipping emissions under EU ETS, increasing to 70% in 2025 and 100% in 2027.

While it’s a policy specific to the EU, the interconnected nature of shipping means it will have ripple effects throughout the fleet.

Setting the seascape

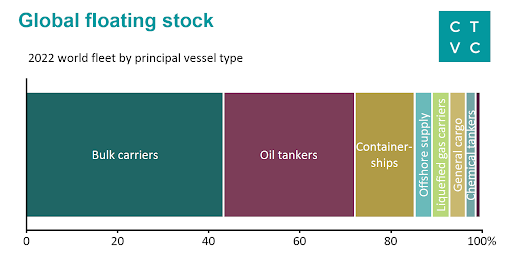

For those of us who don’t operate freighters, it can be hard to comprehend the sheer scale of the shipping industry. More than 100,000 ships over 100 gross tons sailed the seven seas in 2022. This massive fleet includes tankers, bulk transport, and container ships, and the size is growing—both in terms of the total number of ships and in the capacity of the largest vessels.

The shipping fleet is large, but control of the market is extremely concentrated. The biggest shipping companies (i.e., Maersk, Mediterranean Shipping Company, Evergreen) dominate the maritime industry, controlling ~80% of total container fleet capacity. Further, many of the largest businesses are state- or family-owned, beholden not just to the laws of the free market, but political dynamics to boot. While total capacity is concentrated, the long tail of small vessels is widely fragmented across global smaller fleet operators or individuals.

🚢

Key Players in shipping

- Freight or cargo owners are the customers of the container vessels in the shipping industry (e.g. retailers like Amazon, Walmart, or Home Depot). Companies that need to ship goods lease containers for their cargo and can pay a green premium to ensure their container is transported on a more efficient, eco-friendly vessel. Therefore, freight owners are a critical demand lever for pulling decarbonization forward.

- The shipowner can be an individual or a group that owns registered merchant ships, which carry cargo or passengers for a fee (e.g., Maersk, MSC, Evergreen). These entities pay for upkeep of the vessels and often cover the costs of the crew. Shipowners have to ensure their fleets comply with new and existing policy rules and may be incentivized to adopt alternatives by high demand from their customers (freight owners) for lower-emissions shipping.

- The charterer or ship operator is someone who wants to rent a ship to move cargo or passengers. Sometimes the charterer owns the cargo the ship will carry, other times the charterer may make the arrangements for the voyage and the handling of cargo on behalf of someone else or re-rent the vessel to another party for a profit.

- Shipbrokers help connect customers with shipowners who want to lease vessels and charge shipowners a fee or commission for their services.

- Bunkering companies supply fuel to ships. Some bunkering entities also produce the fuel they sell, but many are just intermediaries. These players are likely the most hesitant to transition since they are sensitive to price changes.

De-bunking Fuels

Fuel is the largest expense for a shipping journey, making up 30-50% of a vessel’s operating costs. Fuels used by marine vessels are known as bunker fuels. Those commonly used today are typically produced by refining crude oil—heavy fuel oils are essentially what’s left after the distillation process that separates out kerosene or gasoline, which contributes to the lower prices—and are differentiated by their sulfur content.

Types of bunker fuel:

HSFO (High Sulfur Fuel Oil) is a heavy fuel oil (HFO) with a high sulfur content, as much as 4.5%, which is higher than IMO regulations allow. HSFO has been more affordable than low-sulfur alternatives, driving adoption of vessels with scrubbers that remove sulfur contaminants from the engine’s exhaust (though they often just end up in the ocean rather than the air). This year, the price spread has contracted, shrinking the savings gained by investing in scrubber installations.

LSFO (low sulfur fuel oil) is an HFO with less than 1% sulfur content. LSFOs can be burned in open waters, but there are stricter restrictions on the sulfur content of fuels burned closer to shore.

IFO (intermediate fuel oil) has a sulfur content of up to 0.5%. These fuels are a blend of cleaner distillates—the components of crude oil that evaporate during the distillation process and are then condensed from a gas to a liquid, like marine gas oil (MGO)—and heavy fuel oil. IFOs are the most commonly used fuel in shipping vessels.

MDO (marine diesel oil) is sometimes used interchangeably with IFO. MDO is a distillate blended with a smaller proportion of HFO than some other intermediates and is more expensive than HFO. Depending on the type of MDO, the sulfur content ranges from 3.5% to less than 1%.

MGO (marine gas oil) has the lowest sulfur content at a maximum of 0.1%. MGOs are made up entirely of distillates. These fuels are the most expensive and the only type allowed to be burned in most ports.

Currently, shippers buy fuel on the spot market, where prices fluctuate day-to-day. Alternative fuel costs will likely be based on longer-term offtake agreements and require ship owners and operators to work more closely with bunker suppliers. Bunkering companies play a role in dictating the price spread between traditional fuels and green fuels, which are typically 3-4x the price. Without favorable longterm offtake agreements for the bunkering middleman, their investments in safe storage infrastructure for green fuels will take longer, slowing the ship owners’ investments in vessels with compatible engines and the maritime transition overall.

Levers on Well-to-wake

Well-to-wake sounds like a good night’s rest, but it’s actually the scope of measuring maritime’s lifecycle emissions—from production (the oil well) through powering a vessel at sea.

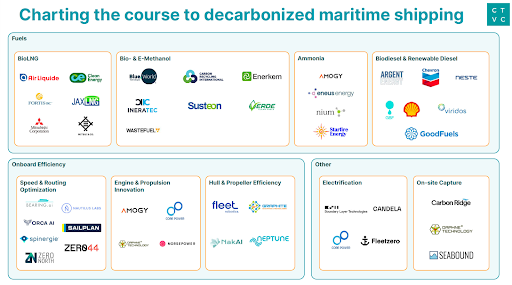

The tech pathways for decarbonization are being quantified and relayed by industry itself as they set sail to reach IMO’s and EU ETS’ high bars. The two primary levers are fuel alternatives and operational efficiencies.

Representative landscape of maritime shipping decarbonization solutions (Source: CTVC)

The blue bullet: Alternative fuels

According to Mærsk Mc-Kinney Møller’s Center for Zero Carbon Shipping (CZCS), alternative fuels have the disproportionate potential to reduce the entire industry’s GHG emissions by over 80%. In maritime, alternative fuel pathways are really a suite of new technologies (such as engines) and ways of producing molecules (such as bio-methanol). Notably, alternative fuel levers are highly dependent on innovation in the O&G industry happening upstream (closer to the well) than the wakes on open sea.

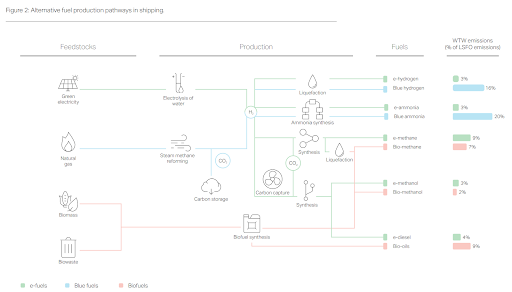

Liquid fuels are critical and sticky. Technologies like hydrogen and batteries don’t have a high enough energy density to volumetrically power vessels. We wrote extensively about the differences between liquid biofuels and e-fuels in our recent feature, but how do these maturity, availability, and integration challenges translate to maritime?

BioLNG

Engine Maturity: Compatible as a drop-in replacement for LNG in engines.

Fuel Maturity: Less mature. Using BioLNG as a replacement is still in its infancy.

Availability: Production of BioLNG is dependent on feedstock limitations which are limiters to biogas and biomethane production. Costs for preparation and delivery of BioLNG still remain high.

Ease of Adoption: Easiest. BioLNG can be used as a drop-in fuel replacement and due to the higher methane concentration, BioLNG is often a better burning fuel. Adoption will rest upon bridging the gap between biogas/biomethane production facilities and coastal fueling stations.

Emissions Impact: A report by SEA LNG found that BioLNG can reduce GHG emissions by up to 80% compared to MDO. BioLNG derived from animal manure could achieve negative emissions in the range of -121% to -188% compared to MDO.

Innovators: Companies such as JAX LNG are moving biogas/biomethane facilities to the coast, decreasing delivery costs. Companies such as Air Liquide, Clean Energy Fuels, FortisBC, Mitsubishi, and Mitsui Group are working with fleet operators to run pilot tests. Biomethane/biogas producers will continue to work on reducing the cost of conversion and upgrading.

Bio & E-Methanol

Engine Maturity: Mature. Engines have been in operation for 10+ years. In addition, retrofits are relatively accessible, with increasing orders being placed for newbuilds.

Fuel Maturity: Less mature.Globally, there’s ~110M metric tons of fossil-derived methanol production capacity, but bio- and e-methanol pathways need more technical derisking.

Availability: Bio- and e-methanol availability is extremely limited at only ~110K metric tons of production capacity, meaning the demand for Maersk’s order of methanol ships alone could suck up the total supply of green methanol today, and it can be 3-4x more expensive.

Ease of Adoption: Relatively easy, either with retrofits or fuel blending. Last year, 35 new vessels compatible with methanol were ordered—a distant second to LNG ships in total orders for vessels compatible with alternative fuel. Methanol is liquid at ambient temperatures, easing storage requirements. Bunkering is demonstrated but not yet happening at scale.

Emissions Impact: CZCS found that bio- and e-methanol have the highest well-to-wake emissions reduction potential compared to low sulfur fuel oil (LSFO).

Engine Maturity: Testing, with new expected engines coming online in 2025. Onboard bunkering and safety are still being evaluated, and innovators are building out new ammonia fuel cells and retrofitting ships.

Fuel Maturity: The least mature. No green or blue ammonia is being produced at scale today, though construction on new plants are underway.

Availability: Green ammonia is still scarce-to-nonexistent.

Ease of Adoption: Difficult. Entirely new engines and engineering. Ammonia is a highly toxic substance, with more potential to harm humans and marine life than traditional maritime fuels, so more safety considerations are required.

Emissions Impact: There’s uncertainty about the emissions impact of ammonia as a maritime fuel. It doesn’t consume or re-emit carbon, but with no ammonia engines operating at scale, measuring nitrous oxide (N2O) emissions at nearly 300x the warming potential of CO2 is yet to be determined.

Engine Maturity: Drop-in compatible with existing diesel ships.

Fuel Maturity: Mature.

Availability: Biodiesel is commercially available with renewable diesel less so, but there are significant concerns about scale due to feedstock limitations.

Ease of Adoption: Easy. Diesel ships can run off of high blends with biofuels, sometimes up to 100%, with little to no retrofitting. Availability and cost are seen as the two main barriers to adoption.

Emissions Impact: Biodiesel and renewable diesel release similar amounts of CO2 when burned, but can reduce life cycle emissions by up to 90%. They also reduce sulfur dioxide and carbon monoxide emissions compared to fossil diesel.

Innovators: The push for biofuels in the early 2000s and a series of acquisitions led to O&G majors like Chevron and Shell taking leading roles in the space, along with Finnish oil refiner Neste. Other innovators include Argent Energy, Viridios, GoodFuels, and GBF.

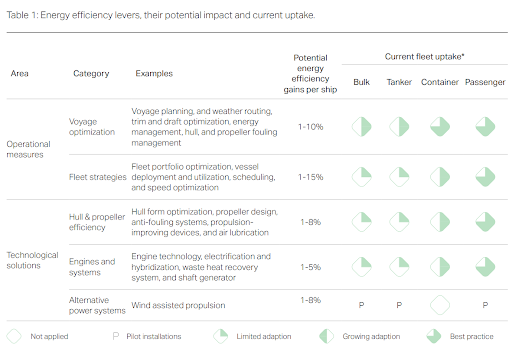

CZCS estimates that operational measures offer energy efficiency of up to 15%. However, a few factors make adopting energy efficiency challenging:

Ship owners and shipyards are risk-averse and don’t like to be a testing partner. They often want to see full-scale demonstrations before they’re willing to adopt.

Non-standard solutions requiring new engineering or design can increase overall cost and make payback periods longer.

Coupled with volatile fuel prices and charter rates, asset managers have a hard time making long term bets, especially if they intend to own the asset for a shorter period of time.

There are split, temporal incentives when a vessel owner pays for the capex upfront but the charterer pays the fuel costs over the long-haul.

Efficiency gains can often be hard to measure, especially if they’re derived from consistent onboard actions or are a derivative calculation from fuel prices—and most stakeholders are reluctant to share precious data.

More consensus is needed across the various efficiency-recommending bodies, and enforcing mechanisms and compliance reporting are still being developed.

Regardless, a handful of innovators are building the tools to help maritime pull these operational levers for energy efficiency:

Speed & routing optimization

Includes: Weather and sea-currents data analysis for route planning, slow steaming (letting the vessel slow down while glide into port and burn less fuel), draft and trim optimization, vessel selection and fleet management, and automated CII ratings platforms.

Includes: coatings and biofouling management for hull cleaning, hull bubblers and/or air lubrication, modifying propeller systems, new hull designs, and biofouling remediation

Smaller-impact improvements include energy efficient light bulbs and waste management aboard, or other renewable energy applied for auxiliary and accommodation services. Each operational change has between a 1-15% energy impact and varying adoption and fit, depending on the type of vessel (e.g., a tanker vs passenger vessel).

More Coming Soon: Applying mitigation measures from adjacent industries

Some are charting a course irrespective of fuel types or efficiency gains.

Electrification: Hydrofoil technologies, battery electric, and even nuclear-powered ships are charging up, but are typically more suitable for short-duration voyages.

Onboard Capture: Another solution is putting point-source carbon capture processes on the ships themselves. The primary challenge with carbon capture on a maritime vessel with limited space is storing and transporting the captured CO2. Rather than trying to offload liquid CO2 in non-existent pipelines at ports, Seabound is one company solving for this by using calcium looping to produce a solid carbonate form of CO2.

Carbon Credits: Shippers can also buy carbon credits as a way to "decarbonize," similar to other industries like aviation. But this option is plagued with all the same challenges we see in the application of carbon credits in other industries (i.e., permanence, leakage, additionality, etc.).

Industry adoption

As with other climate tech solutions, some shipping players are first movers for lower-emissions innovations while others are waiting to see how the transition goes.

Doers: Shipping giants like Maersk and MSC are already purchasing ships outfitted for alternative fuels, but these players are outliers in the industry. MSC remains focused on purchasing LNG-compatible newbuilds, while Maersk has opted for 25 new vessels with methanol engines that will be delivered in 2024 and 2027.

Wait-and-seers: Smaller shipping players with smaller balance sheets are less able to make purchases and conduct the R&D necessary to incorporate these new solutions into their operations.

Safer bets

More than 200 LNG ships were ordered last year, making up ~80% of all orders for vessels compatible with alternative fuels. The number of LNG ships on the water is nearing 900 vessels, marking ~40% growth YOY in 2022, but still a small fraction of the total sailing fleet.

While LNG is a fossil fuel, the adoption of LNG ships is growing most rapidly because it’s a safer bet for future decarbonization. Shipowners know LNG is available and get the option to swap in lower-carbon-emitting bioLNG in the future. That removes the big question mark on whether ammonia or methanol will win out as an alternative fuel. Some shipyards are also experimenting with making LNG ships compatible with green ammonia, which requires smaller tweaks than other types of retrofits.

Dual fuel: In 2022 almost 60% of all newbuild orders by tonnage were for dual-fuel vessels. With differences in maturity, storage, price, and availability among these alternative fuels, many ship builders today are casting a wide net, keeping options open for the future of low-carbon fuel alternatives.

These ships are marketed as ammonia-ready, methanol-ready, or LNG-ready and allow ship owners flexibility to try out different fuels and figure out which will fit best with evolving cost and policy constraints.

Who bears the cost

With all these different players looking to make their cut of shipping profits, who pays for the current green premium associated with cleaner ships and fuels?

Consumer goods vs commodities: Consumer-led supply chains create stronger demand pull for maritime decarbonization as customer sentiment and cost pass-through capabilities help absorb the costs of investments in cleaner shipping alternatives.

A major retailer selling shoes could pass on the cost of more eco-friendly maritime transport onto buyers. Distributing the cost of higher-priced alternative fuels across thousands of pairs of shoes moved by the vessel could test the willingness of consumers to pay for sustainable shipping and may mean that even 2x the fuel costs translate to a price increase of a few cents for each pair of shoes.

The further from the end customer, the harder it is to pass on that cost, so the economics of green fuels for commodities is more difficult. If you’re shipping oil, for example, intermediaries along the way, like refiners, don’t have any incentive to pay a green premium on transporting it. Plus, dividing the price increase across barrels of oil rather than thousands of shoes creates a less attractive shared cost model.

Racing SAFs: Beware the opportunity costs of limited supply

Sustainable aviation fuels command a higher market price today than the slimmer margins afforded to maritime, incentivizing sustainable fuel developers to prioritize sales of limited volumes into SAFs.

Because jet fuel is so expensive relative to bunker fuel, the marginal cost of switching from traditional fuels to SAFs is less than maritime.

Refueling for jets can hypothetically happen anywhere, but the cost of landing and taking off is so high that refueling will need to happen at the aircraft’s destination. Because these locations are often in the US and EU, regulations in these countries can basically control the market.

That’s not the case with maritime, where international waters make it much easier to dock somewhere unregulated to refuel, making it more difficult to shift with national-level policies.

Deployment challenges

The maritime industry is complex and requires long term planning, which creates difficulties in the transition to cleaner technologies.

Ship lifespans

Building a new vessel takes years and costs tens of millions to hundreds of millions of dollars. It’s a significant investment, and shipowners want to maximize the lifespan of these ships, which are ~25 years on average, but can be as long as 70 years.

The maritime fleet is aging, which is a challenge for decarbonizing because it means older, dirtier ships are remaining in service longer. The replacement rate is slow and it’s very expensive to sunset boats more rapidly, though rising fuel costs could contribute to quicker turnover.

Retrofitting: Most ships are financed with a payback period of 5-10 years. Most shipowners are unlikely to put a new engine in a vessel that’s 10 years old, which means that the timeframe where shipowners can recoup the investment of retrofitting vessels with more efficient or lower-emissions tech is much shorter than the lifespan of the ships.

Waste: Some shipowners may begin scrapping their older vessels as regulations push their cost of operations up, which will exacerbate the shipyard crunch.

Workforce

Transitioning to cleaner technologies isn’t just about thes costs. It also requires a workforce with different skills to build and operate ships that run on new fuel types. There is a shortage of ship yards that are prepared to retrofit vessels. Once a ship is ready to set sail, it needs a crew that’s trained to use the new equipment safely.

Port infrastructure

Ports need to be updated to service new vessels running on different types of fuels. It’s a chicken-and-egg game for ports to pick a fuel when shipowners and fuel providers are still playing wait-and-see. Replacing a port’s fueling infrastructure will be a capex-intensive feat, made worse by low utilization in the early days (a challenge that was all too familiar to the early-movers in EV charging as well). Not to mention the fueling infrastructure built at different ports is also highly influenced by the energy transition strategies of the nations in which they are located.

Ports with government backing are likely to have more incentive and more resources to make these changes, which will essentially develop separate storage and bunkering systems for different types of alternative fuels. The ports with land to dedicate to separate infrastructure will be in a better position than land-constrained ports to execute this shift.

Ships & Engines

Along with the necessary onshore infrastructure, the industry is still working on engines compatible with alternative fuel sources. Engine makers like Man Energy Solutions, WinGD, Wärtsilä are rushing to make initial ammonia engines ready for purchase, with commercial availability kicking off from late 2023 to early 2025.

Accountability & Verification

Just measuring the starting point for maritime emissions is a major challenge. In an ever-changing environment out at sea, baselining is very difficult due to factors like weather patterns, currents, and marine life impacts, like barnacles growing on the hull. This makes validating carbon reductions tricky, especially when thinking about additionality. Switching to verified alternative fuels could also be a barrier if ship owners and operators are unable to prove the blending rate and traceability of greener fuels—a tricky challenge considering bunkering fraud is rampant.

Key takeaways

Regulations are pushing adoption forward. Policies designed to be sticks or carrots for alternative fuels are recalibrating the risk considerations in an industry where planning has to take a longer view, even when there’s not yet a clear technology frontrunner, especially in fuels.

Infrastructure is a chicken-and-egg problem. Decisions made today about the types of fuels ports need to prepare for can lock in industry outcomes for decades to come. Not to mention just how complex and massive the new distribution, storage, and safety set of infrastructure will be.

Existential supply shortages. The supply of “new” fuels—particularly green methanol and, to some extent, ammonia—is wildly short of projected demand. Anticipate green gold rushes and collapses in the inefficient sprint to shore up supply.

National rules are tough to apply to an international industry. In an industry that spends most of its time operating outside of any national borders, global standards and regulatory enforcement can be challenging to implement. Further, countries’ maritime policies and energy transition policies are often deeply rooted in national security and don’t always play nice cooperating with others, which makes for different experiences port-to-port.

It’s a margin call. Compared to jet fuel, bunker fuel is dirt cheap, which makes for a challengingly low pricing baseline and margin reality for sustainable maritime fuels vs their SAF cousins. Furthering the “green premium” disadvantage, SAFs can often pass through their higher costs to willing consumer goods beneficiaries, while sustainable maritime solutions must sell into margin-sensitive commodities distributors.

A massive, maritime-scale thank you to Sanjay Kuttan at the Global Centre for Maritime Decarbonisation, Taline Filipovic at CREO, Joe Bettles and Daniel Barcarlo at the Mærsk Mc-Kinney Møller Center for Zero Carbon Shipping, Alisha Fredriksson at Seabound, and Ross Berger at I Squared Capital for sharing their insights and expertise on the maritime industry and to John Tan and Oliver Booth for research and data analysis support.