The Energy Transition is a Metals Transition, with Tem Tumurbat at Nomadic Venture Partners

If you’re bullish on the energy transition, you’re bullish on mining. With every new battery pack and wind plant, it’s becoming more apparent that the energy transition is a metals transition.

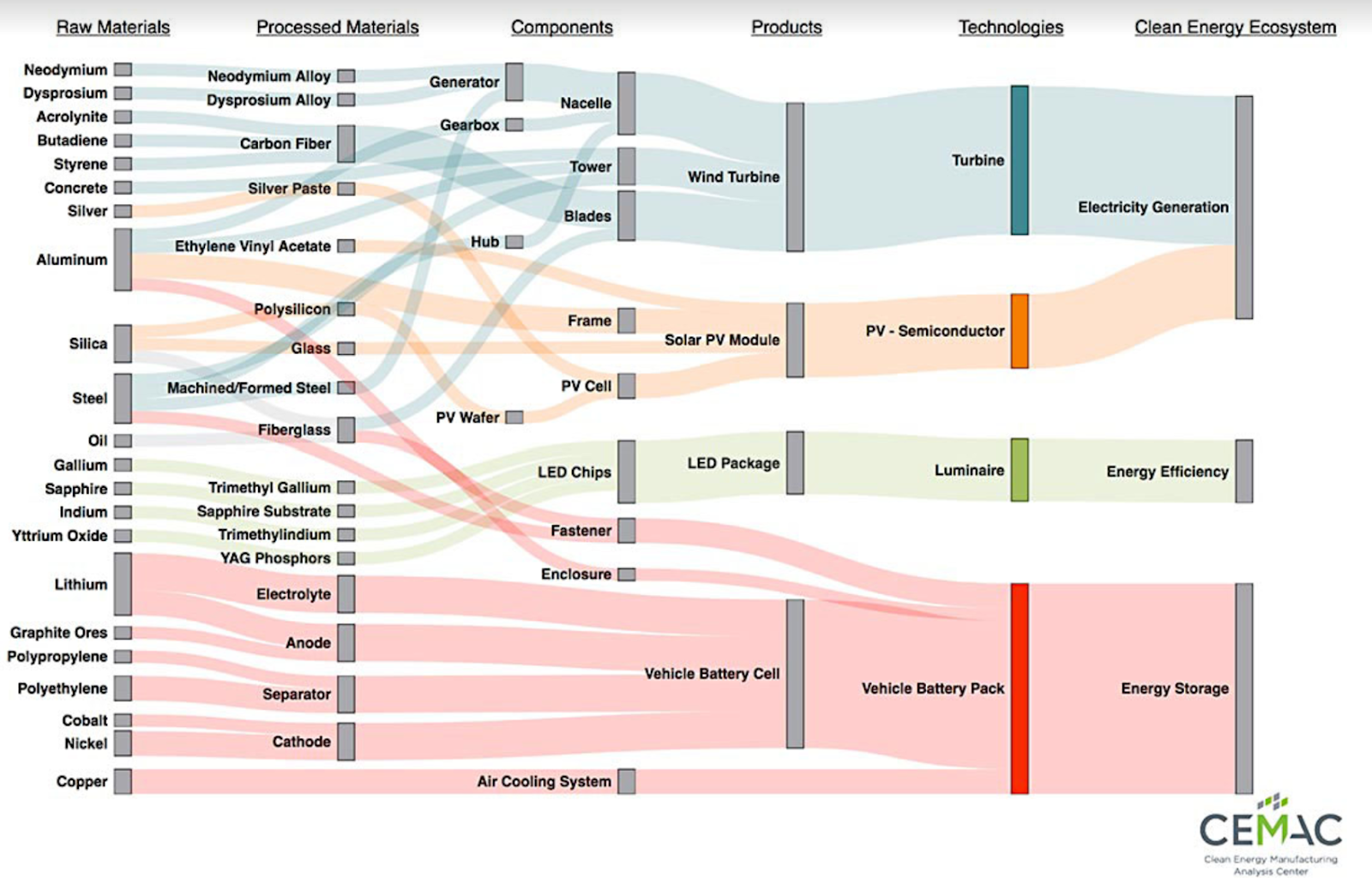

Over a lifetime, an American born today will consume 2.96 million lbs of minerals, metals, and fuels - a shocking mineral-intensity only exacerbated by the clean energy transition. Electric cars need 6x the mineral inputs of conventional cars. An offshore wind plant requires 13x more mineral resources than a similarly sized gas-fired plant. Critical minerals (lithium, cobalt, copper, nickel, graphite, REEs, aluminum, zinc, PGEs, etc.) are building blocks of most clean tech darlings that dominate the roadmap to net zero: solar PVs, wind turbines, EVs, batteries, power lines – even hydro, geothermal, nuclear, and hydrogen have a hefty appetite for critical minerals.

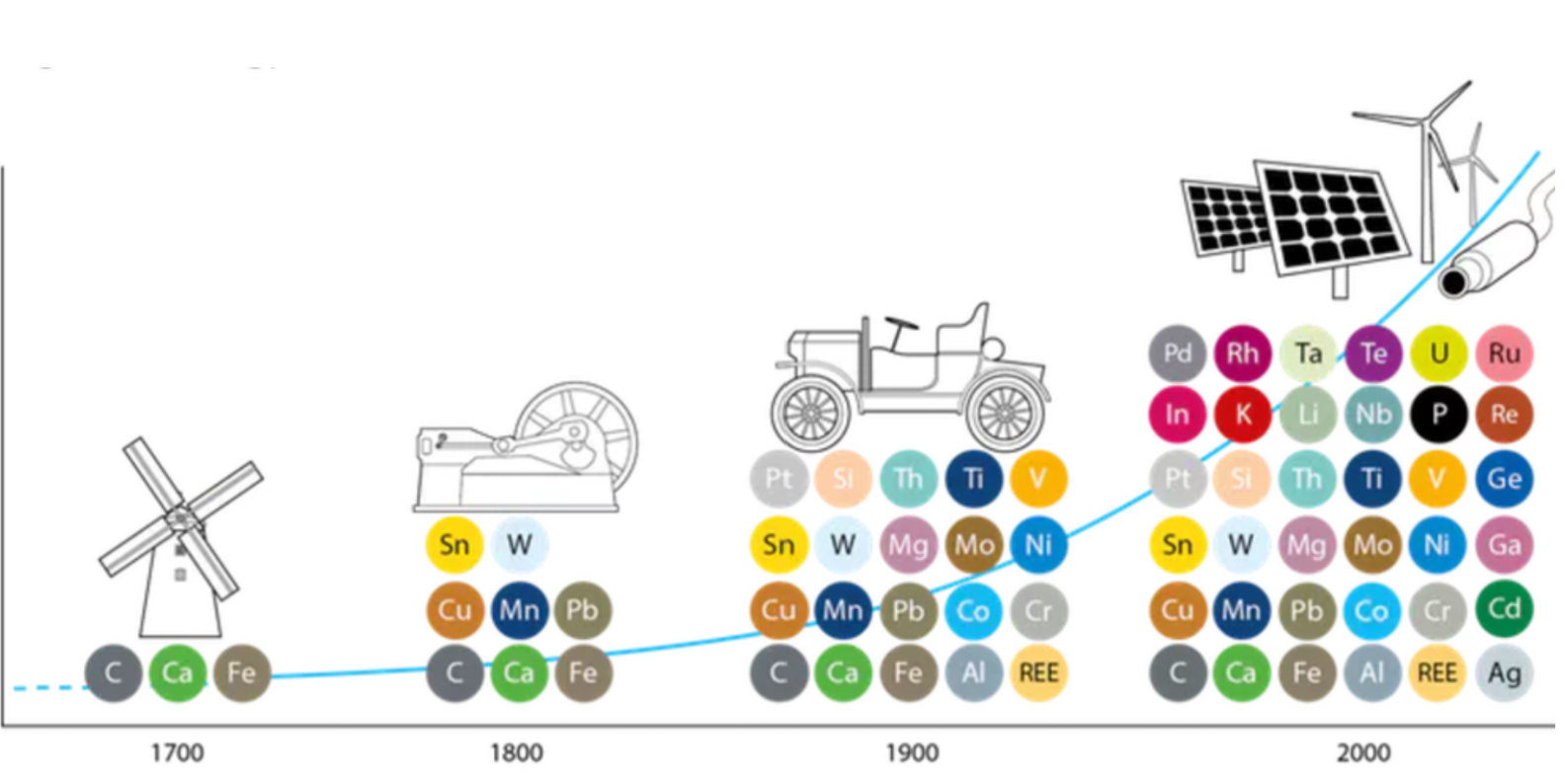

As consumer and industrial use cases for minerals become more technologically advanced (think: improved computer chips, more efficient solar panels, longer range EV batteries), mining and processing methods must keep pace with the increasing sophistication.

Solving for net zero means solving for minerals demand. Annual copper demand is set to balloon 53% by 2040 to 40 million metric tons (Mt) - a 14 Mt supply shortfall. Lithium supply will need to increase 5.9x to meet the 4 Mt demand by 2035. Other metals like cobalt, nickel, and graphite will likely experience similar growth profiles. Close to 300 new lithium, cobalt, nickel, and graphite mines would need to be up and running by 2035 to bridge the supply-demand gap.

To make matters more complicated, the availability and accessibility of these minerals are a function of geological accident. Mineral deposits are unevenly scattered globally with political instabilities and unforeseeable events like the pandemic already straining fragile global supply chains. Today the US imports >50% of its critical minerals, and is 100% import-reliant on 13 of the 35 critical minerals that the Department of Interior has classified - with a near complete dependence on China for rare earth elements (REEs). A group of more than a dozen REEs make up high end magnets used in EVs, advanced weaponry, and electronics. Countries like the US and EU that net import critical minerals will be hard-pressed to secure strategic metals and minerals resources to build their planned climate technologies.

The Inflation Reduction Act (IRA) explicitly acknowledges this geopolitical complexity. IRA now requires at least 40% of the value of an EV battery’s applicable critical minerals to be extracted, recycled or processed in the US or a country that’s party to a US free trade agreement. The minimum value requirement increases 10% each year (e.g. 80% in 2027 and beyond). EV batteries containing “any” critical mineral sourced from Russia and China entirely forgo the $3,750 tax credit. Cue US automakers scrambling to secure limited qualified supplies.

Rapidly increasing minerals supply will require pulling three levers at once:

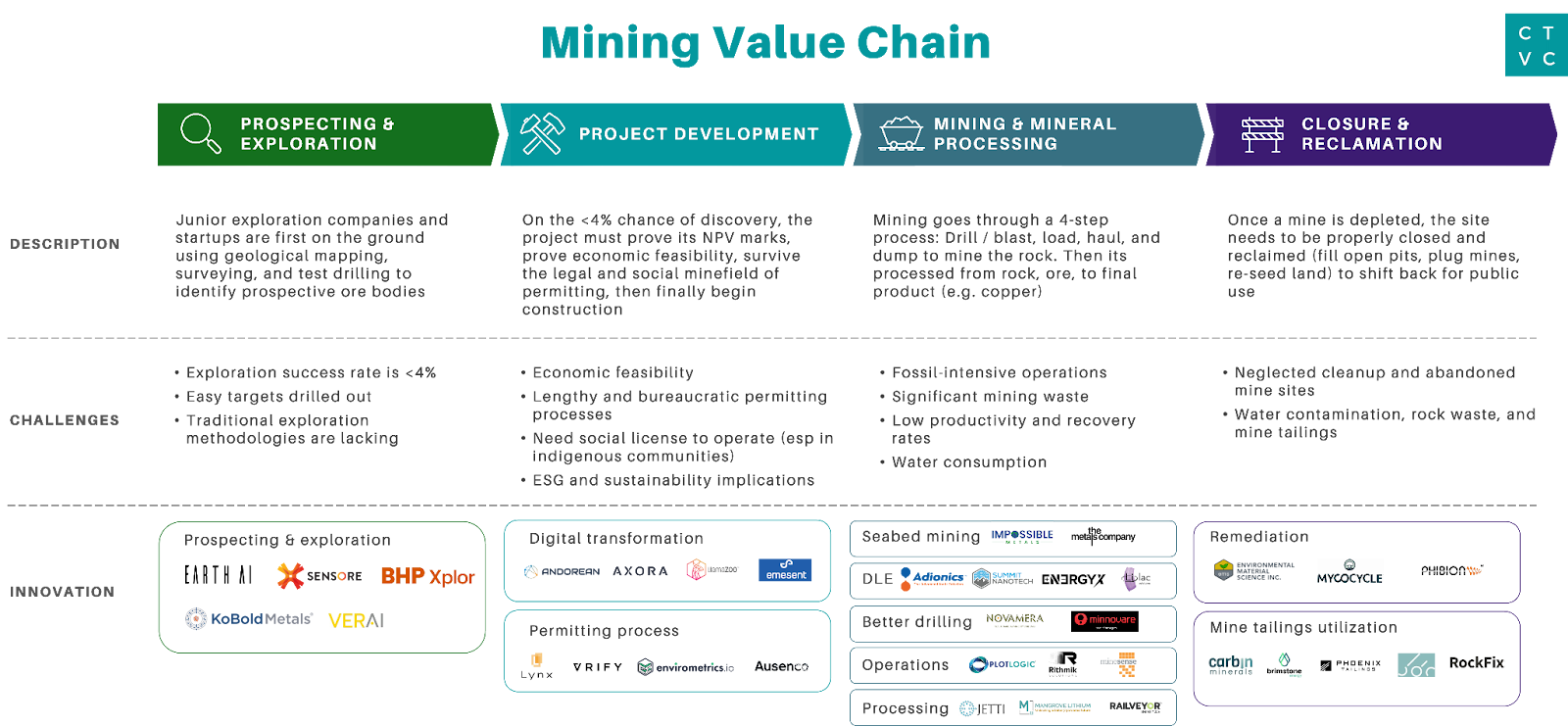

The mining value chain mimics the mine life cycle, and can take decades:

🔍 Prospecting and Exploration

🏗️ Project Development

⚒️ Mining and Mineral Processing

🚧 Closure and Reclamation

The mining value chain starts with prospecting and exploration for mineral resources, which is typically the domain of ‘junior’ exploration companies and start-ups. Such companies require ‘seed’ capital in the tens of millions to identify and prove prospective ore bodies.

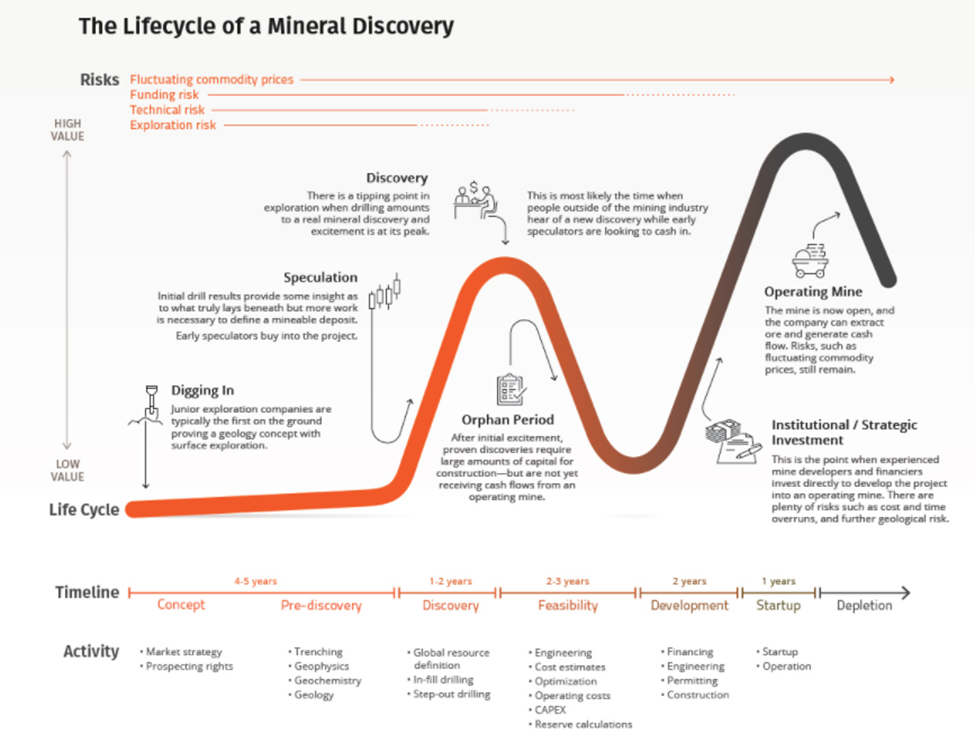

Mining companies dispatch geologists to an area of interest to kick off exploration, perhaps near a historically mined area (brownfields), or a new territory (greenfields). With the assistance of geological mapping, geophysical surveying, geochemical sampling and testing, the geologists gather surface and subsurface data to identify targets and test for signs of mineralization. The prospecting process can take five to ten years, often with no pot of gold at the end of the rainbow. In most cases (and somewhat similar to many pre-seed stage startups), drilling programs fail to find an economic discovery, even if drilling along a known mineralization trend where the odds are somewhat improved.

Exploration has always been a risky venture. The proportion of exploration targets that eventually become mines range from 4% for brownfields to <0.03% for greenfields. The odds of identifying a deposit in an uncharted territory with legacy technology are roughly 1 in 3,300. Despite increases in exploration expenditure since the early 2010s, we’re not on track to discover the 300 new mines needed to meet net zero targets. This calls for more risk tolerant capital to fund advancements in exploration to bring a step-change in success stories.

Innovators: KoBold Metals, Earth AI, SensOre, and Ver AI are using AI/ML to improve the odds of making discoveries, shortening the exploration timeline, and reducing the discovery cost of a resource.

Larger technology providers (e.g. IBM Watson) are doing the same, offering their platforms as a service to mining companies. Mining companies are internally exploring expedited discovery efforts: BHP (the world's largest mining company) recently launched Xplor, an accelerator to source and grow the next generation of mineral exploration opportunities.

After the <4% chance that the lucky explorer discovers a mineral resource worth developing, the project owner then needs to raise more capital to plan, permit, and build the project. Permitting requires regulatory support and local community consultation, which is contentious in the developed world (‘not-in-my-backyard’ (NIMBY)) and is politically ‘delicate’ in the developing world, where many of the newer large discoveries have been found.

This stage consists of four critical steps:

Miners can boost output across a handful of innovation levers:

Seabed mining innovators: The Metals Company, Impossible Metals

DLE innovators: Lilac Solutions, Summit Nanotech, EnergyX, Adionics

Better drilling: Novamera, Minnovare (acq by Hexagon)

Innovators: Andorean, LlamaZOO, AXORA, and Emesent.

Innovators: Lynx Global Intelligence, Envirometrics, VERIFY, and Hemmera (acq by Ausenco)

Development can span from five years to decades, and often requires hundreds of millions in financing, if not much more, and ends with the construction of a new mining operation. At this point, metal production can commence with the mining and processing of ore.

Generally speaking, there are three different mining methods:

A mine operates using a four-step process carried out by large diesel equipment operated by highly skilled operators:

Fleet electrification and autonomy are clear, low hanging opportunities for mining decarbonization. Newmont (the world’s largest gold mining company) announced a partnership with Caterpillar to develop and deploy electric autonomous haul trucks. In harder-to-reach settings, First Mode is delivering the first hydrogen haul truck.

Mining innovators: Plotogic, Rithmik, Minesense

Processing methods change depending on the quality of the ore, but occurs in five basic steps:

Different mining and processing techniques require varying amounts of energy, largely supplied by fossil fuels. Processing technologies (e.g. grinding and smelting) are heat and energy intensive, exacerbating their direct CO2 emissions.

Processing innovators: Jetti Resources, Rail-Veyor Technologies, Mangrove Lithium

After all of that drilling, loading, hauling, and dumping the global mining industry generates 72 Gt of waste every year. With today’s inefficient surface and underground mining practices, waste totals will increase as the grade (mineral content in a ton of rock) of ore bodies steadily declines alongside mining productivity. Waste materials divvy into 55% conventional overburden waste rock, 37% processing tailings, and 8% metallurgical waste. Most historic waste storage areas are left unreclaimed, potentially polluting the environment and the nearby communities. Global tailings total 282.5 Gt across 8,500 facilities - enough to fill a 6km high cube.

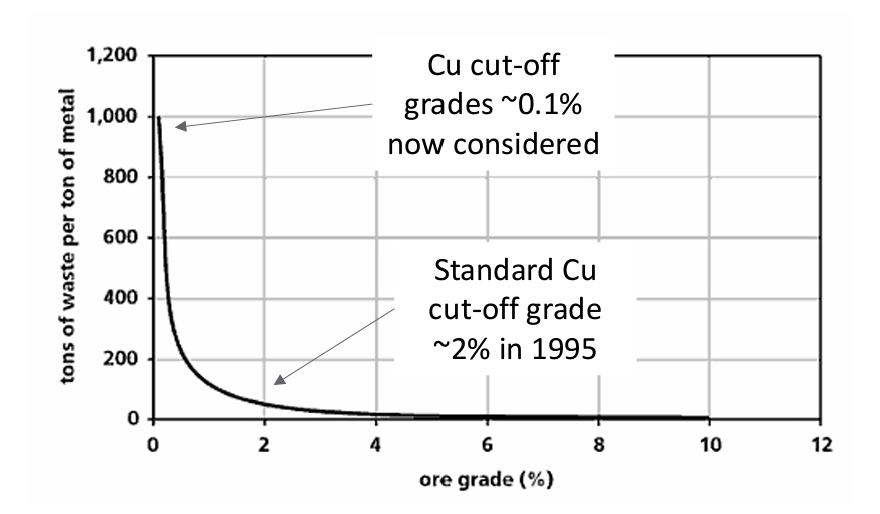

An ore’s grade is synonymous with the mineral’s concentration. Put another way, a lower grade means smaller needles in a larger haystack.

Copper is a frightening case study. The average copper ore grade has declined by almost ⅔ from 1.6% in 1920 to 0.5% in 2019. Soon mines will be mining copper with 0.2-0.3% grade. If average copper grade falls to 0.1% and if demand for copper rises to 100Mt by 2100, copper mines will generate 20 Gt of waste - excluding tailings. As waste grows, so will scope 1 and 2 emissions.

How will mining increase productivity, reduce its water consumption and waste generation, all while decarbonizing? Miners are replacing fossil fuels with renewable energy, focusing on reducing waste, and reusing and recycling old materials, all while undergoing digital transformation to boost productivity and collectively reduce CO2 emissions.

In-situ methods like direct lithium extraction (DLE) are garnering attention in both the climate tech and mining sectors. DLE extracts lithium from underground brines, and promises to perform in a more sustainable way. While still in its infancy, if commercialized, DLE can boost lithium supply through higher recovery, faster production rates, and lower opex while reducing evaporative ponds and using less water and reagents.

After the mine is depleted, the mining company closes and reclaims the land to an equal if not better than original condition. This entire mine-life cycle can take decades.

Reclamation can take many forms from resloping large waste dumps, filling open pits, plugging underground mine workings, contouring man-made “mountains” to mimic nature, replacing topsoil, and reseeding with native species of plants. Once a site is properly reclaimed, it can be reopened for general use. Since 1978, almost 3m acres of mine lands have been restored for wildlife areas, wetlands, parks, golf courses, farm lands, and for other recreational uses.

Addressing ecological or downstream impacts can be a gnarlier involvement. Contaminated water cases can require building and operating treatment plants followed by years of careful monitoring. Even with modern regulation mandating cleanups, miners have escaped culpability by liquidating through bankruptcy or dissolving, leaving the cost of cleanup to the taxpayer. In 2008, it was estimated that there are >161,000 abandoned hardrock mine sites in 12 Western states and Alaska. During the prior 10 year period, the US government spent $2.6B reclaiming other abandoned hardrock mines. Required financial assurance products (e.g. cash deposit, letters of credit, certificates of deposit, surety bonds) have since improved the mining industry’s proper closure of operations and reclamation. If a miner abandons their site, the bond is released to cover reclamation costs.

Key challenges with abandoned sites today revolve around water, rock waste, and tailings facilities. Fortunately, innovators on the ground are reusing and recycling mine waste to generate value while cleaning up abandoned sites.

Innovators: Phibion, Environmental Material Science, Mycocycle, Carbin Minerals, Brimstone, Rockfix, Travertine Technologies, Phoenix Tailings

The energy transition is a metals transition. Achieving net zero on any meaningful timeline requires solving for the mounting demand for critical minerals like lithium, cobalt, copper, nickel, graphite, REEs, aluminum, zinc, and PGEs that are integral to producing clean technologies like solar PVs, wind turbines, EVs, batteries, power lines, hydro, geothermal, nuclear, and hydrogen.

Mining mimics climate tech’s valleys of death. Scaling a successful mining project looks like the path to scaling a climate tech startup - but with even deeper Valleys of Death. Each step along the mining value chain requires 5+ years, millions of upfront investment, permitting and regulation challenges, and low probabilities of discovery.

Efficient and domestic will be the name of the game. The mines of the future must look vastly different from the mines of today. More ore deposits will need to be discovered, at a much higher success rate and with a lower cost profile. In order for the US to regain its grip on a domestic supply chain of critical minerals and reduce reliance on China, financing for exploration and project development must exponentially increase in tandem.

Don’t take digital optimization for granite. Mines today are less productive than they were a decade ago. Digital services and solutions that exist today (AI/ML, automation, robotics, IoT, sensors, drones, etc.) have the potential to reduce 1/3rd of mining emissions by 2030. More efficient and productive mines will also help reduce the massive 72 Gt of mineral waste the industry produces every year.

All stakeholders matter in this transition. Almost all the copper and nickel, and most of the lithium and cobalt resources in the US are located within 35 miles of Native American reservations. In our relentless pursuit of critical minerals for climate tech, we need to remember to ensure this transition is sustainable and equitable.

Mining is ready for its breakthrough moment. If critical minerals are the unlock to the energy transition, innovation in mining is the key. In order to ensure a sustainable and scalable mining value chain, investment and innovation must accelerate.

Massive thanks to Tem Tumurbat and the team at Nomadic Venture Partners (NVP) who moved mountains and turned over every stone for this feature. Tem and Batchimeg Ganbaatar founded NVP to accelerate decarbonization through investing in pre-seed to Series A digital solutions in the mining, manufacturing, and transportation sectors. Reach out if you’re a climate tech entrepreneur or a geoscientist building digital solutions and hard tech in these sectors, or if you’re a fellow investor focused on decarbonizing mining. Likewise, thanks to Grace McCleary for chipping away at this feature as we dug deep.