🌎 How corporates drive demand for FOAK projects #303

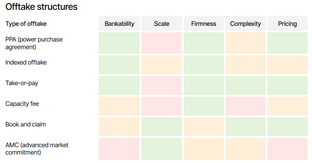

Get our new report on offtake, with HSBC

Happy Monday! Congratulations to Mexico’s first female, IPCC contributing, climate scientist president!

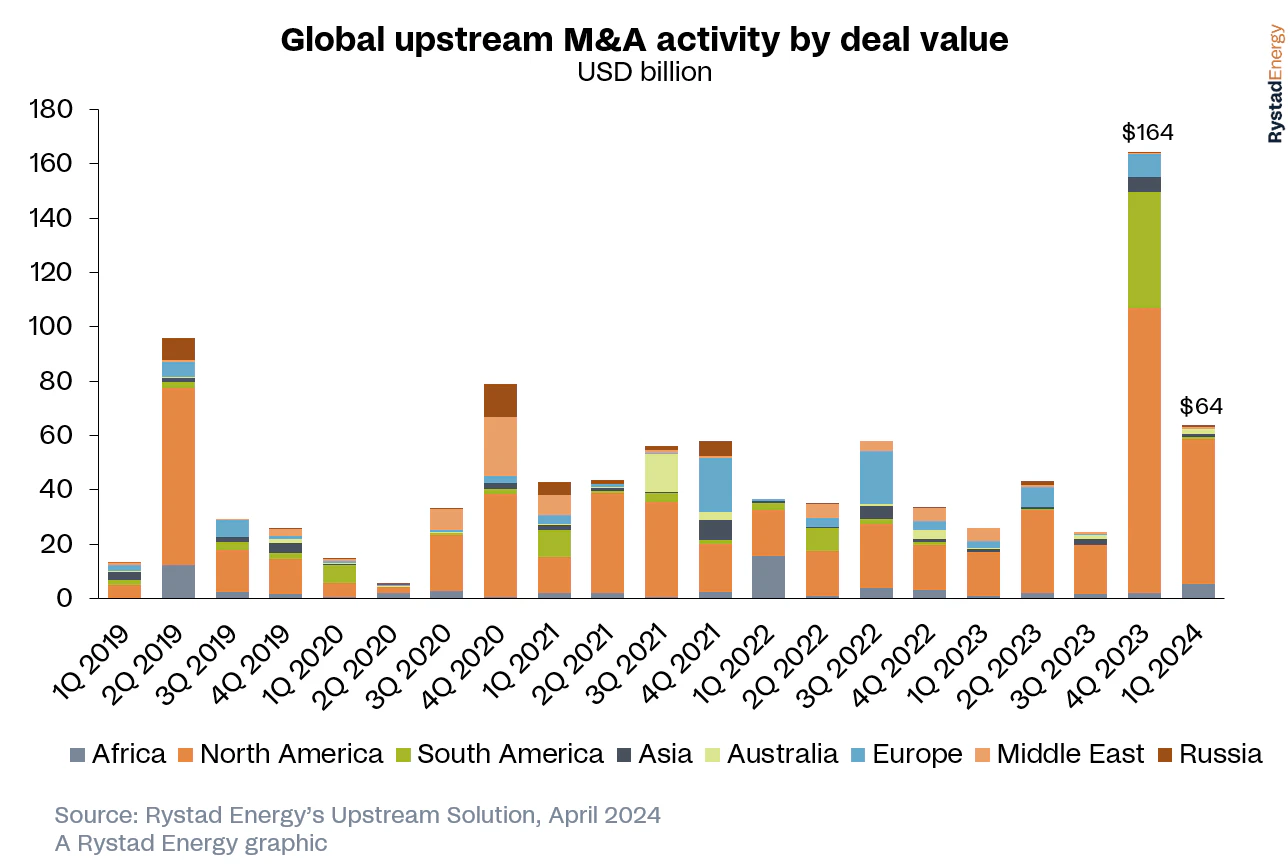

This week, we’re riding the wave of mega-mergers among oil & gas majors. Looking at swells ahead as the industry pours money into maturing basins and consolidates assets in a bet on continued energy demand (in the short term, at least). We dive into what makes shale's big deals a big deal.

In other news, Shell fights with activist shareholders, Oklo nuclear power for data centers, and e-SAF deals.

In deals, $7.7bn for climate tech across five new funds, $80m for cooling chips, and $37m for climate credit cards.

Thanks for reading!

Not a subscriber yet?

📩 Submit deals and announcements for the newsletter at [email protected].

💼 Find or share roles on our job board here.

A wave of mega-mergers and acquisitions is crashing through the energy sector. In just the past week alone, two notable deals were announced:

These recent deals come in the wake of a record high of oil and gas upstream M&A activity in Q1 2024, which saw over $54bn in US deals. Highlights include:

This flood of consolidations follows a 21st-century high deal total of $192bn in 2023. Exxon's $59.5bn purchase of Pioneer Natural Resources was announced in October (now pending FTC approval), and Occidental Petroleum's agreement to acquire CrownRock for $12bn in December.

The US shale revolution, starting around 2005, transformed the global energy landscape. Initially driven by numerous small-time drillers, now a handful of major players are racing to acquire valuable assets and reserves to bolster their inventories and production capabilities. Factors driving this include:

While the drivers for the wave of consolidation has not been directly related to climate technologies, climate solutions may still be affected.

Special thanks to Mudit Agrawal and Oliver Booth for their contributions to this piece.

🏠 Frore Systems, a San Jose, CA-based active device cooling maker, raised $80m in Series C funding from Fidelity, Addition, Alumni Ventures, Clear Ventures, MVP Ventures, and others.

💸 Doconomy, a Stockholm, Sweden-based climate-focused credit card provider, raised $37m in Series B funding from CommerzVentures, UBS Next, Motive Ventures, PostFinance, S&P Global Inc., and Tenity.

🚗 Euler Motors, a New Delhi, India-based electric 3- and 4-wheelers maker, raised $24m in Series C funding from Blume Ventures, British International Investment, and Piramal Alternatives India Access Fund.

🏠 Cloover, a Stockholm, Sweden-based renewable energy financing platform, raised $108.5m in Debt funding and $5.5m in Seed funding from 9900 Capital, Lowercarbon Capital, and QED Investors.

🏭 EthonAI, a Zürich, Switzerland-based AI-powered manufacturing analytics platform, raised $17m in Series A funding from Earlybird Venture Capital, Founderful, General Catalyst, and Index Ventures.

🛰 WindBorne Systems, a Stanford, CA-based long-duration smart weather balloons maker, raised $15m in Series A funding from Khosla Ventures.

🌱 Lumo Ag, Napa, CA-based connected irrigation platform company, raised a $7m funding round from Active Impact Investments and Fall Line Capital.

🚗 Turno, a Bengaluru, India-based commercial EV distribution and financing platform, raised $6m in Series A funding from B Capital Group, British International Investment, Quona Capital, and Stellaris Venture Partners.

🌱 Vizcab, a Lyon, France-based carbon impact analysis software platform, raised $4.9m in Series A funding from KOMPAS, Brick & Mortar Ventures, and Global Brain.

⚡ Delta Green, a Prague, Czech Republic-based grid stability software platform, raised $2.4m in Seed funding from Tilia Impact Ventures, Credo Ventures, and Purple Ventures.

⚡ Plural Energy, a San Francisco, CA-based blockchain platform for climate assets, raised $2.3m in Pre-Seed funding from Compound, Maven11, Necessary Ventures, and Volt Capital.

⚡ Eneryield, a Lund, Sweden-based grid monitoring solutions platform, raised Seed funding from ABB and Chalmers Ventures AB.

💨 Chloris Geospatial, a Newton, Massachusetts-based natural capital carbon MRV provider, raised an undisclosed amount of Seed funding from AXA Investment Managers, At One Ventures, Cisco Foundation, Counteract, NextSTEP, and Orbia Ventures.

🔋 Zenobe Energy, a London, England-based battery storage developer, raised $523m in Debt funding from ABN AMRO, Aviva, CIBC, Lloyds Bank, MUFG Bank, NatWest Group, Rabobank, Santander, Scottish Widows Investment Partnership, Siemens, and Societe Generale.

🍎 FarMart, a Gurgaon, India-based SaaS-based food supply chain platform, raised $2.9m in Debt funding from responsAbility Investments.

🌱 Traace, a Paris, France-based emissions traceability and management platform, was acquired by Tennaxia.

Energy Capital Partners, a Summit, NJ-based investment firm, held a final close of their $6.7bn fifth flagship fund that invests across energy transition, electrification and decarbonization infrastructure assets.

Eurazeo, a Paris, France-based investment firm, announced the launch of their $800m fund that will invest in solutions that promote planetary stability.

ETF Partners, a London, UK-based investment firm, held a final close of their $309m fund that invests in companies working on environmental challenges.

Clean Energy Ventures, a Boston, MA-based investment firm, held a final close of their $305m second fund that invests in decarbonization solutions.

The Bezos Earth Fund, a Washington, DC.-based investment firm, announced an additional $100m for new research on plant-based alternatives.

Can’t get enough deals? See full listings and deal analytics on Sightline Climate

In a blow to investor activism, Shell shareholders rejected a climate resolution brought by activist shareholder Follow This, which sought more aggressive emissions reduction targets, at its annual shareholder meeting last week. A majority of Shell shareholders also supported its decision to weaken climate targets, with 78% voting for a revised energy transition strategy that reduces emissions more slowly than initially planned.

Duke Energy announced agreements with Amazon, Google, Microsoft, and Nucor to accelerate the adoption of clean energy through new rate structures designed to lower the long-term costs of investing in technologies like new nuclear and long-duration storage through early commitments. This effort signals a new industry mechanism for how major players can buy RECs, reflecting a shift in how capital is deployed for new deals.

Google is investing $1.1bn in a data center expansion in Finland, leveraging the country’s abundance of renewable energy, as well another $2bn in Malaysia to establish the first data center there. Meanwhile, Microsoft and G42 announced a $1 billion initiative to develop a digital ecosystem in Kenya, aiming to enhance the country's technological infrastructure and capabilities with focus on AI-climate innovation.

Oklo announced a partnership to supply 100MW of nuclear power to a hyperscale data center in Wyoming, a significant step towards integrating advanced nuclear energy into data center operations.

In a major demand signal, BCG signed a purchase agreement with Twelve to buy E-Jet sustainable aviation fuel (SAF), a power-to-liquid jet fuel made from CO2, water, and renewable electricity.

One of the UK’s largest wind farm operators, Beatrice Offshore Windfarm Limited (Bowl), had to pay $42m for overcharging the government for curtailment of their generation. This is the largest payment the UK has mandated from an energy company for license breaches.

Leading energy developer RWE announced it would build the first eight-hour lithium battery in Australia, with a planned capacity of 50+ megawatts (MW) and 400+ megawatt hours (MWh). RWE also reached an FID for a large, two-phase, 1.6 GW offshore wind farm in Germany’s North Sea.

Automakers seem to be making a macro play for hybrids in the short term amid broader EV troubles, with BYD launching a next-gen plug-in hybrid system with 2100-km range, while Subaru, Toyota, and Mazda said they’re building new internal combustion engines for the “electrification era.”

A new federal partnership with 21 states will expand the use of grid-enhancing technologies (GETs) and advanced conductors to improve the existing transmission system's efficiency. It aims to increase cooperation on transmission planning, explore innovative partnership models, and jointly plan infrastructure development.

The European Commission approved up to $1.5bn in developing hydrogen technologies for various transport means, including vehicles, ships, and aircraft.

The National Grid announced plans to raise $8.9bn to strengthen electricity networks in the US and UK as part of a $76.4bn investment plan over the next five years, driven by the transition to renewable energy.

In a big move to secure fuel supply for advanced nuclear, TerraPower and Framatome North America are building a pilot plant to metallize high assay low enriched uranium (HALEU) from uranium oxide in Washington. This initiative aims to demonstrate Framatome's metallization capabilities and advance TerraPower's efforts to develop a domestic HALEU supply chain.

China’s CO2 emissions may have peaked in 2023, but manufacturing could threaten that.

Crude cargo tankers are stranded in the North Sea, as European and Asian refinery thirst dries up.

Hydrogen's hype, a superbubble quietly popped.

Buckle up — climate change is turning air travel into a rocky ride.

Google, Meta, Microsoft, and Salesforce pledged to contract 20m tons of carbon credits by 2030.

New Climate Capital Guidebook for all federal government programs dropped.

Students drill into action, aiming to seal abandoned wells.

Deep-sea mining gets a nod from Congress, aiming to chip away at China's mineral monopoly.

From rubble to reusable, scientists from Cambridge find a concrete solution.

As EV sales slow, the future of policy incentives for the sector is hitting a roadblock.

Meanwhile, California's bright solar future looks uncertain.

📅 ClimaTech 2024: Register to attend the 2024 ClimaTech conference in Boston alongside Massachusetts Governor Maura Healey and Boston Mayor Michelle Wu on June 3-5th to network with thinkers, leaders and innovators in the climate tech industry.

📅 Ecosummit Berlin: Join startups and investors driving decarbonization on June 4-5th, 2024, at Spindler & Klatt in Berlin.

📅 Founder Dinner: Apply to attend the Early Climate Tech Founder Dinner hosted by Lowercarbon Capital on June 5th to meet, share ideas with, and collaborate with other early-stage founders.

📅 Blue Tech Happy Hour: Register to attend the Blue Tech Happy hour in SF on June 5th to engage an network with the local blue economy community.

📅 Sustainability Conference: Register to attend the Sustainability World Summit from June 5-7th for a conference that aims to shift the conversation from sustainability rhetoric to actionable change through engaging discussions, case studies, and innovative presentations.

💡 Compute for Climate Fellowship: Apply to the Compute for Climate Fellowship co-hosted by the IRCAI and AWS by June 7th to participate in a pioneering program designed to fund R&D projects for Climate Tech startups using advanced cloud computing and AI.

📅 43North Accelerator: Startups in Buffalo, NY can apply to this accelerator by June 7th.

📅 Planet Jam: RSVP to join Planet Jam on June 12th for a casual get together of professionals working in climate or sustainability-related roles in startups, corporates, policy.

📅 The Forest Valley Institute’s Sandbox: Early stage B2B startups with a focus on climate impact Startups can apply to the Forest Valley Institute’s network by June 23rd

💡 Hack for Clean Energy: Apply to join Lowercarbon Capital, OpenAI, and Crusoe on June 28th this summer for an AI hackathon aimed at accelerating the scale-up of solar, wind, batteries, and other renewable energy technologies in the US.

💡 Stripe Climate Fellows: Apply to be a Stripe Climate Fellow by July 15th and receive grant funding to work on ambitious yet feasible proposals to catalyze voluntary or policy actions, aiming to increase carbon removal demand.

📅 Greentown Labs Climate Tech Summit: Register to attend the Climate Tech Summit at Greentown Labs on October 22nd in Houston and October 24th in Boston to explore climate tech solutions from 200+ startups and network with climate-action trailblazers.

Revenue Operations Manager, Backend Engineer, Research Intern @Sightline Climate

Climate Technology Investor @Vectors Capital

Accounting Associate @Clean Energy Ventures

Vice President of Engineering @Relyion Energy Inc

Head of Strategy @Dioxycle

Analyst @Energy Capital Ventures

CFO @Greentown Labs

📩 Feel free to send us deals, announcements, or anything else at [email protected]. Have a great week ahead!

Get our new report on offtake, with HSBC

Inside the $915m bet on carbon removal's next phase

Inside the $915m bet on carbon removal's next phase

Newsletter

Newsletter