🌏 The bits and bytes of grid tech

(Bonus edition) Part III: The software “middleware” layer for grid operators / utilities

Software for solar developers with Equal Ventures’ Rick Zullo and Simran Suri

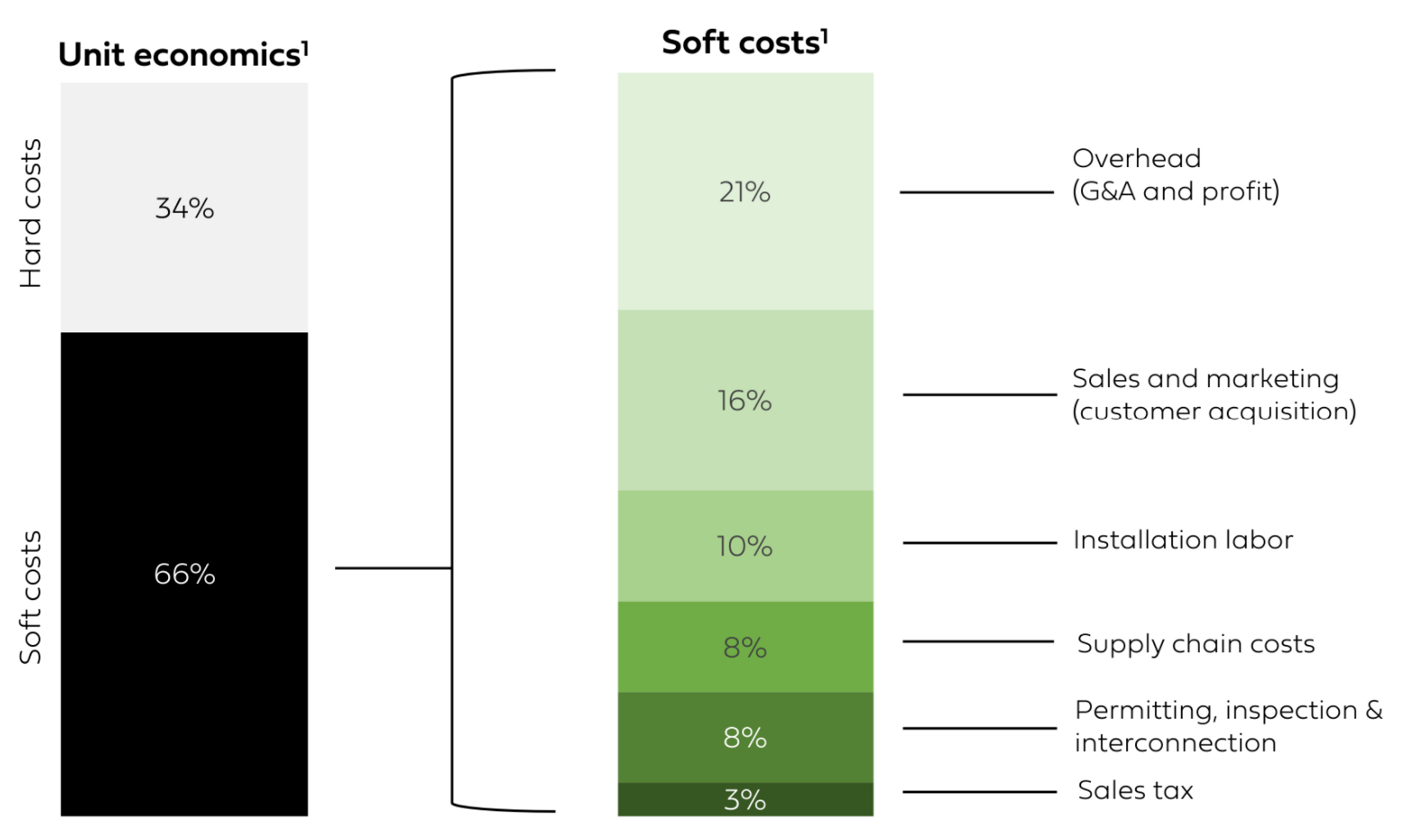

A few weeks back, Energize Ventures joined us to dissect the hard costs of constructing the energy transition. While steel in the ground is (literally) foundational, soft costs like sales and marketing, labor, and permitting account for ⅔rds the cost of residential projects - and can make or break a clean energy project.

In climate circles, clean energy technologies like solar are assumed to be mainstream, yet residential penetration has only reached 3% of the total US market. All signs point to generation capacity growing in the years to come, spurred by legislative initiatives incentivizing increased clean energy installation like Local Law 97 in New York and the recent solar and storage ruling in California. Soft costs like understanding roof quality and EPC relationships, will be a major bottleneck to this increase in development; accordingly, advancement of the green workforce has been a growing topic of discussion, driven by Biden’s clean power ambitions and increased federal funding from the American Jobs Plan.

The opportunity for clean energy developers shines far beyond just solar. In fact, solar represents just 30% of the capacity opportunity in the residential DER (Distributed Energy Resources) market. Solar is a wedge into the residential DER market, which developers can expand into via the fragmented but large addressable market of storage installations, EV charger installations, and more. Industry analysts anticipate $110B of investment to pour into US DERs between 2020 and 2026, with new DER attachments and installations providing even further addressable market upside. Each of these new technologies requires unique forms of project design, installation and underwriting, complicating the existing soft cost bottlenecks.

The added complexity of new DER applications necessitates digital solutions - even for small developers who operate today without any form of digital infrastructure. These developers live in the long-tail, the ~46% of residential solar installations managed by businesses that typically install less than 50 projects a month. These are local mom and pop shops often forced between the choice of hiring staff or investing in software that offers great promise, but no immediate results. To bring the promise of DERs to life, the market must go beyond solving for the needs of enterprise-level, software-first large developers and build digital solutions that embrace long-tail developers. Failing to design products for those SMBs installing nearly half of all residential solar projects puts at risk the promise of DERs, but perhaps even more so, the green workforce itself. Appropriate and affordable technology toolsets will enable the green workforce to upskill to careers, not just low wage jobs.

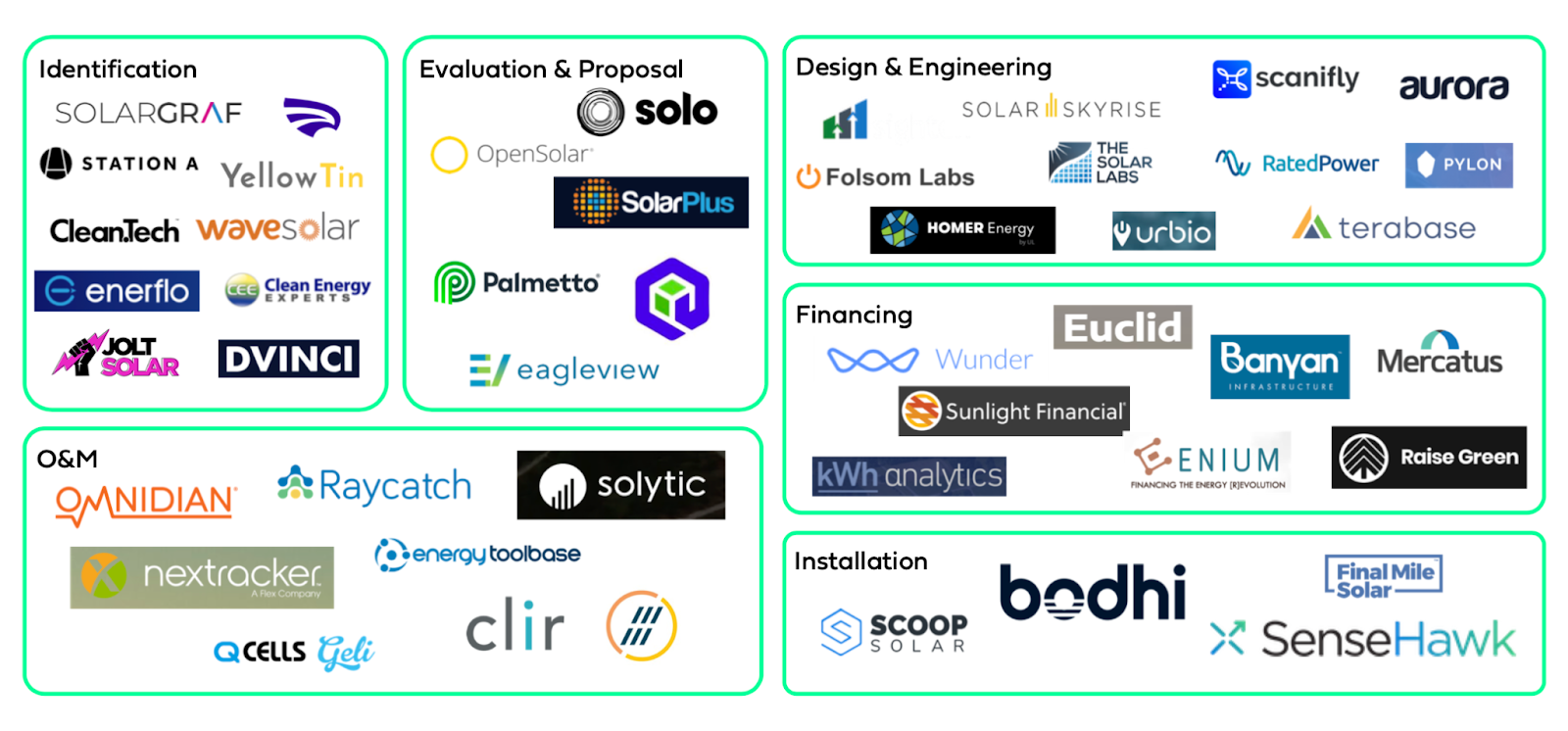

The adage that every development project is different also holds true for developers’ software stacks. The sheer complexity of software solutions servicing the developer market inhibits adoption. The software value chain spans across the life cycle of an installation, from identification through to operations & maintenance (O&M), and are priced primarily on a SaaS basis and/or for a fixed rate per project completed. The abundance of siloed point solutions (see representative market map below) requires developers to piece together a mosaic of multiple tools. Limited integrations between these systems leads to leakage of information, creating friction and inefficiencies in developer workflows and crippling the ROI of digital adoption.

🔎 Identification - qualify leads and help developers or salespeople conduct initial outreach

Example innovators: Station A (qualifying potential project sites), Jolt Solar (educating consumers on solar panel installation options)

🕵️♀️ Evaluation & Proposal - evaluate homeowners and project sites, as well as create digital project proposals for developers

Example innovators: Aurora (digital project proposals), Pylon (digital project proposals and CRM)

💸 Financing - help developers source capital and underwrite and structure deals based on project proposals

Example innovators: Banyan Infrastructure (project roll-up software for project finance), Sunlight Financial (solar project financing)

✏️ Design & Engineering - create digital project designs and offer permitting and interconnection support

Example innovators: Solar Skyrise (project design software), Scanifly (project design software leveraging drone imagery)

🏗️ Installation - focus on the intersection of developer and EPC workflows during the actual installation process to optimize customer support or the procurement and delivery of parts

Example innovators: Bodhi Solar (customer support), Scoop Solar (EPC field management)

🛠️ Operations & Maintenance (O&M) - software or hardware solutions implemented to help developers and/or asset owners monitor their systems and project sites post-installation

Example innovators: Omnidian (real-time system analytics), Clir Renewables (asset monitoring)

It’s no wonder that small developers have shied away from the “analysis paralysis” of engaging and integrating in a multi-vendor procurement of these complex software products. Engaging with these fragmented point solution systems is simply too complicated, too time-consuming, and too expensive to make sense for all but the most established of developers.

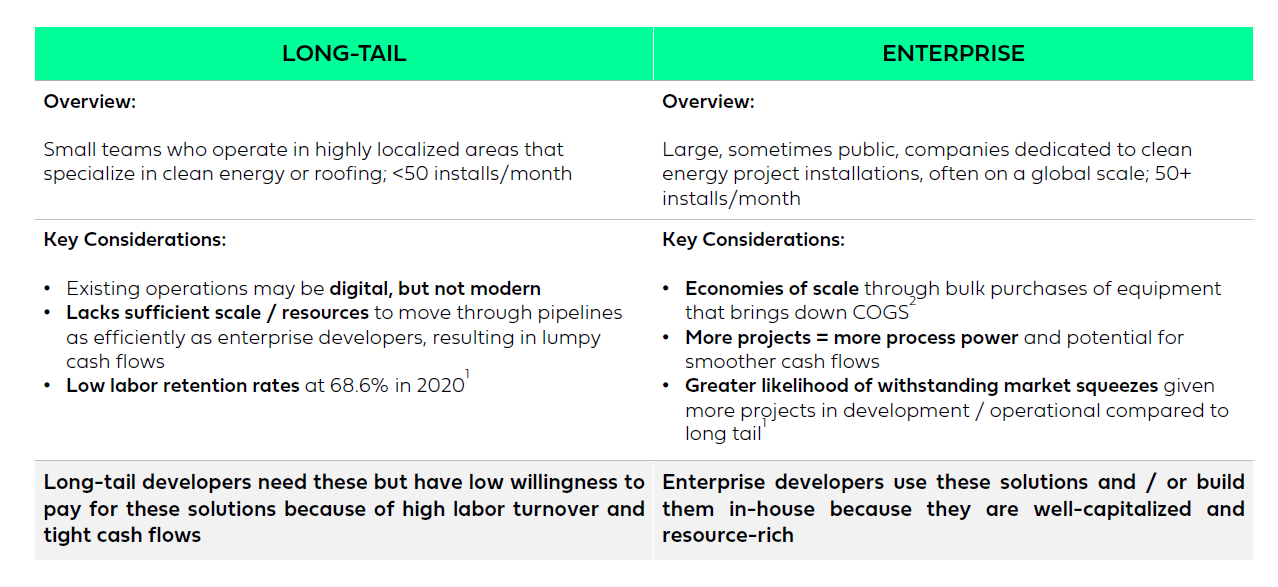

The behavior of the long-tail of solar developers is noticeably different from enterprise developers. Enterprise developers tend to be large, sometimes public, companies dedicated to clean energy project installations, often doing over 50 installations a month globally. Enterprise developers are well-capitalized and resource-rich - they’re able to build solutions in-house to mitigate soft costs (see Sunrun & Vivint merger) or manage procurement processes. Naturally, software companies have historically catered to this market with ample budget and resources. Moving forward, in order to unlock the adjacent pool of addressable customers, software companies must understand the profile and needs of the long-tail of developers:

Underinvested in software. Their existing operations may be digital, but generally lack verticalized software - think Excel, fax, email and/or (in the rare case) an off-the-shelf CRM.

Low labor retention rates. High labor turnover rates (estimated at 31% in 2020) and tight cash flows characterize decision making. These labor and cash flow dynamics have diminished the long-tail’s willingness-to-pay for software solutions. Why would developers invest in multiple solutions with high annual SaaS fees for employees that may leave before the year is over?

Lacks sufficient scale/ resources. Like most SMBs, small developers face operational disadvantages such as higher costs of capital, lack of financing partnerships, limited branding/marketing awareness, minimal leverage of suppliers (often leading to lack of product availability) and a general lack of economies of scale.

Yet, this long-tail of small developers excels in their knowledge of local markets and regulatory processes as well as their trust within their local community. These powerful levers could be buttressed by digital infrastructure. Even without digital adoption, long-tail developers are poised to see double-digit growth over the next 3 years driven by upsell opportunities with batteries and other residential DERs. The market needs the long-tail, with analysts citing the need for an additional 900k employees in the green workforce by 2035 in order to meet Biden’s clean energy goals. If digital adoption for the long-tail of developers can be unlocked, there is an opportunity to accelerate their growth in solar installations and, more importantly, enable them to drive and capture value from additional DERs as the market grows and becomes more fragmented. If accomplished, this could be a catalyst for creating hundreds of thousands of high-paying jobs.

The freemium model. Perhaps the greatest property of software is its low-cost scalability. Once developed (often an expensive undertaking), the incremental cost of distributing to another customer is incredibly low. The more challenging cost center for software is that of acquiring customers. Taking a page out of the enterprise SaaS playbook, startups selling to solar developers should make their software free to democratize access to the end product and significantly reduce the cost of distribution (who can say no to free, right?). This model has worked incredibly effectively in other market opportunities with similar labor properties (often referred to as a “counter-positioning” strategy) and there are ample monetization opportunities available to software platforms that unlock adoption of this base.

Take rate and upsell. Rather than charging SaaS fees upfront, these companies can capture a percentage-based take rate of overall project value, while improving overall developer economics. In some cases, these monetization opportunities are likely to attack other non-IT related cost centers that the developer is already paying for, enabling them to reduce these cost centers, rather than increasing IT spend. Examples could range from supply chain offerings like parts procurement to logistics to lead generation. There is also ample opportunity to embed insurance and financial products. By putting the long-tail on a centralized platform that has meaningful scale (aggregating smaller players into a centralized hub that rivals or passes the economic size of enterprise players), the long-tail may be able to gain access to lower rates on these services that have typically belonged solely to larger enterprise players. In doing so, these platforms have the potential to not just improve digital operations (the core intent of software), but to level the playing field on the major cost advantages as well.

This freemium strategy is one of the many potential ways to remove friction in the purchasing process for developers and drive digital transformation of the green workforce. By aligning itself with the success of its customers (rather than fixed fees), solutions can not only modernize the existing long-tail, but invite new entrants (much like the way Shopify and Amazon have in the commerce space) by significantly lowering the upfront costs for newcomers to compete.

The long-tail of clean energy developers represents an underserved opportunity. They represent close to $6.5B of annual economic activity in residential solar alone. Today’s software solutions are too siloed, costly and complex for these end users.

Solar is a wedge. New DER opportunities will create an even greater need for digital solutions. Expected sustained growth in DERs will require additional services outside of existing software solutions. Use this opportunity to enable the long-tail of solar developers to drive and capture value from growth and fragmentation of the residential DER market with new assets like storage and EVs.

The current (large) market of solar software is not built for SMBs. While many strong software businesses operate in the solar developer market already, they’re complex and fragmented by point solutions which makes them unsuited to long-tail customer needs.

Willingness-to-pay for software solutions by the long-tail is low. The long-tail will not pay for software solutions, but pay significant costs for other non-IT sources such as leads, financing, insurance and hardware procurement.

Freemium represents an opportunity to increase adoption and capture a portion of GMV. There is an opportunity to increase digital adoption by giving away software solutions for free. Long-tail developer activity represents enough GMV that they lend themselves well to a take rate or other forms of monetization that don’t increase IT spend but still capture wallet share.

Special thanks to Rick Zullo, Simran Suri, and the team at Equal Ventures. Equal Ventures’ full research deep dive deck is available at this link. If you’re an entrepreneur building digital technology for the long-tail of clean energy developers, reach out - the team would love to hear from you!

(Bonus edition) Part III: The software “middleware” layer for grid operators / utilities

Part II: How grid tech is the rails of the energy transition

The Goldilocks effect in geothermal HVAC systems