Valuations across the early stage market are wildly divergent and shifting in real time. Since the first half of 2022, each week feels singular and the fundraising dynamic is ever evolving. When the waters are choppy, CTVC anchors on the data. While our mid-year funding update found climate tech to be relatively insulated compared to the overall market environment, deal announcements are often lagging indicators of current market sentiment.

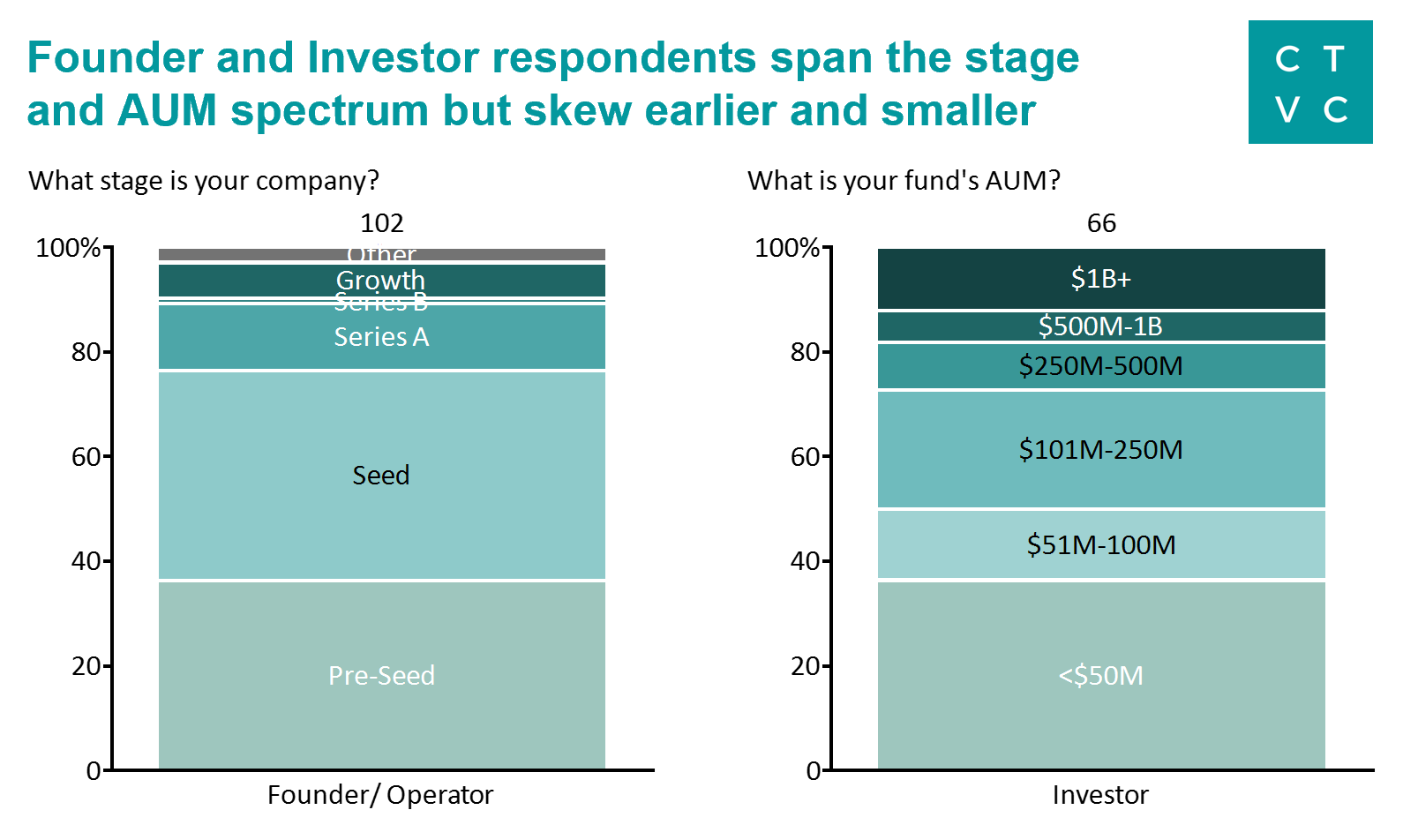

A week and a half ago, we opened a market sentiment survey to get behind the numbers and understand where investors and founders think the climate world is today. 168 of you responded (thank you!), to capture a real-time, quantified pulse check on the climate tech funding environment.

Our goal is to understand and enable climate builders to do their best work, especially as each week seems to change the answer around what’s fundable. We believe in the longer horizons of climate tech, but recognize that the most obvious numbers can sometimes mask the feelings that drive the numbers further out. With no further ado… the cuts!

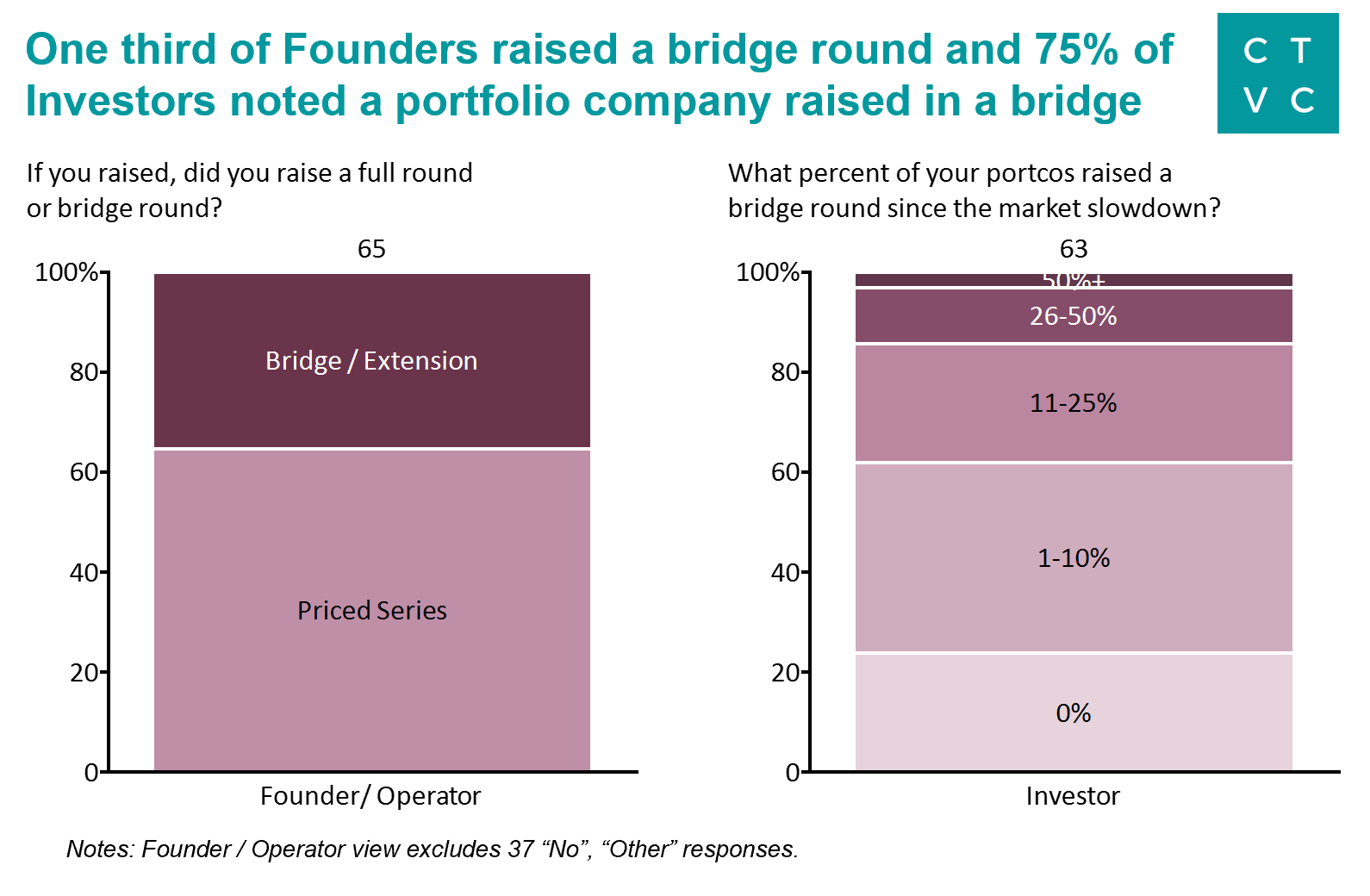

Founders have indeed taken the common advice to add more cash to the coffers in anticipation of a potentially cold fundraising environment, via raising bridge and extension rounds

33% of surveyed founders raised a bridge or extension round over the last 12 months

Meanwhile, 72% of investors have had at least one company in their portfolio raise a bridge - some as high as half of the portfolio!

[Note: Bridge rounds help startups “bridge” the gap between larger, often priced funding rounds and are an indicator of less certain future guarantees of capital or longer time horizons between rounds.]

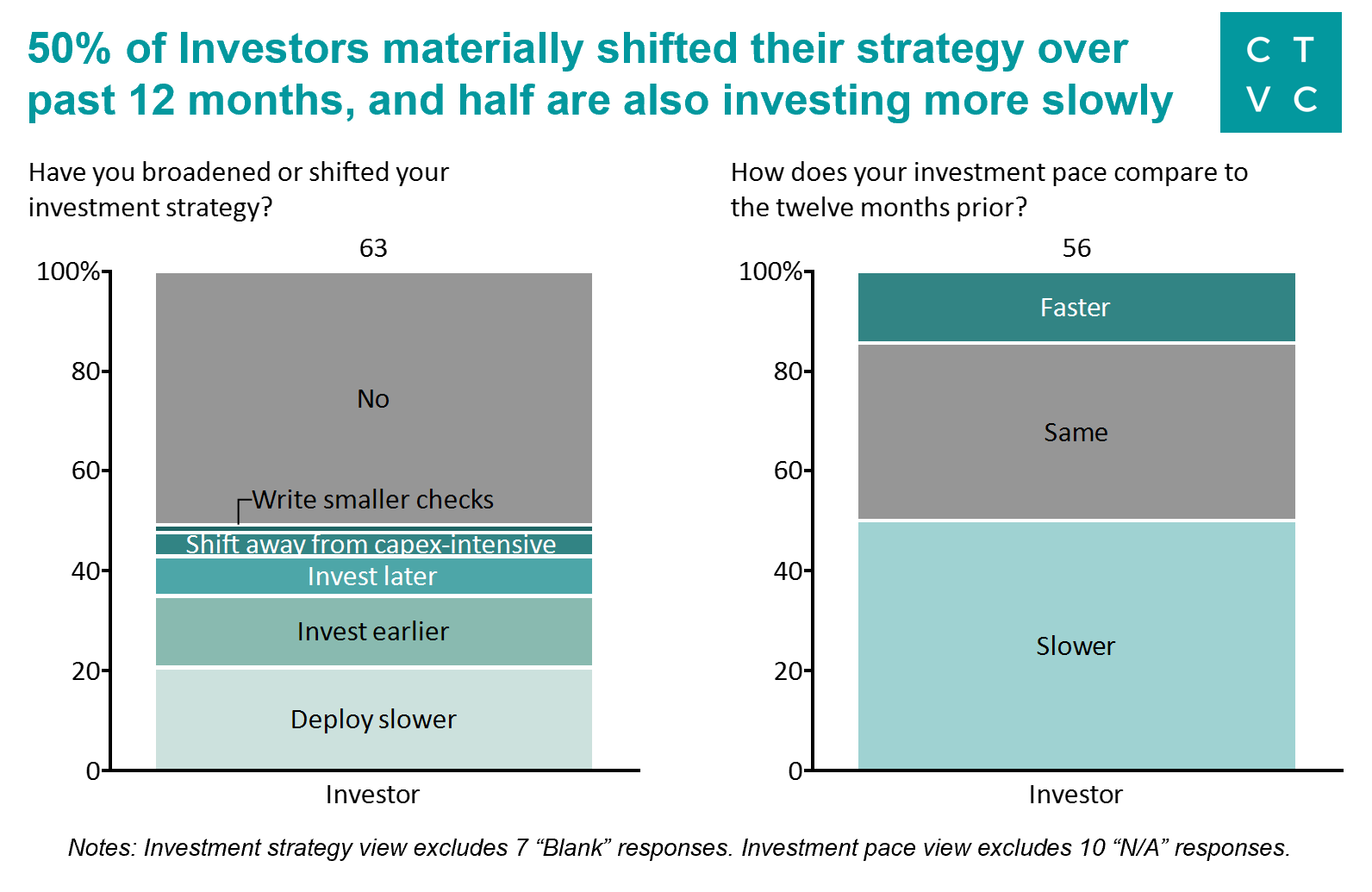

Mimicking the “batten down the hatches” behavior of founders’ bridge rounds, half of investors deployed more slowly in the past 6 months versus the prior twelve months - although 14% of VCs invested faster (👀)

Even in cases where the pace of deployment did not change, the round construction often shifted towards extension rounds in existing companies verses new company relationships

The slowest days may be yet to come. Many investors who reported a stable rate of deployment predicted that deployment would slow in the future, especially since many of their recent investments started diligence in H2’22 before the market had fully turned

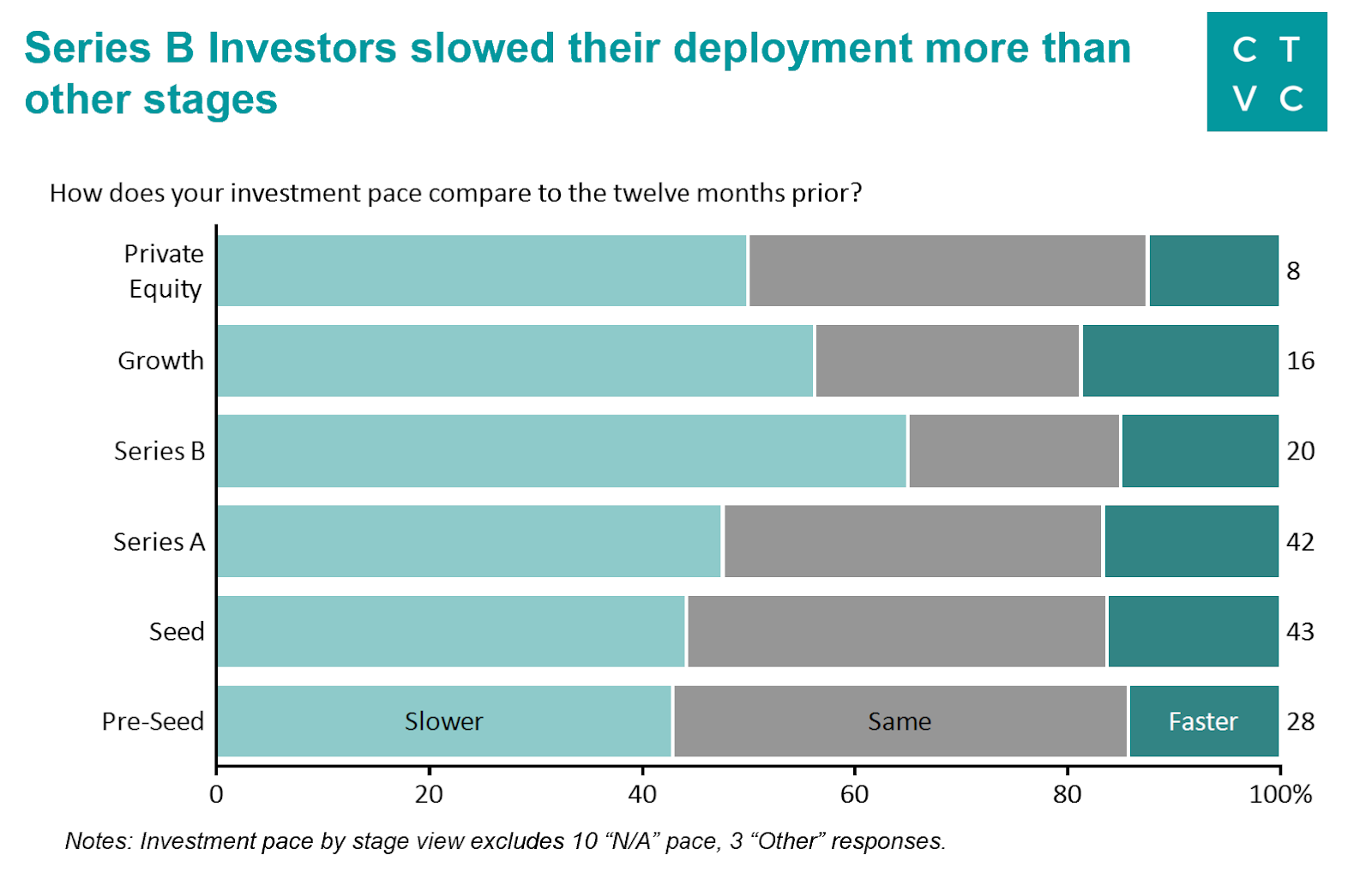

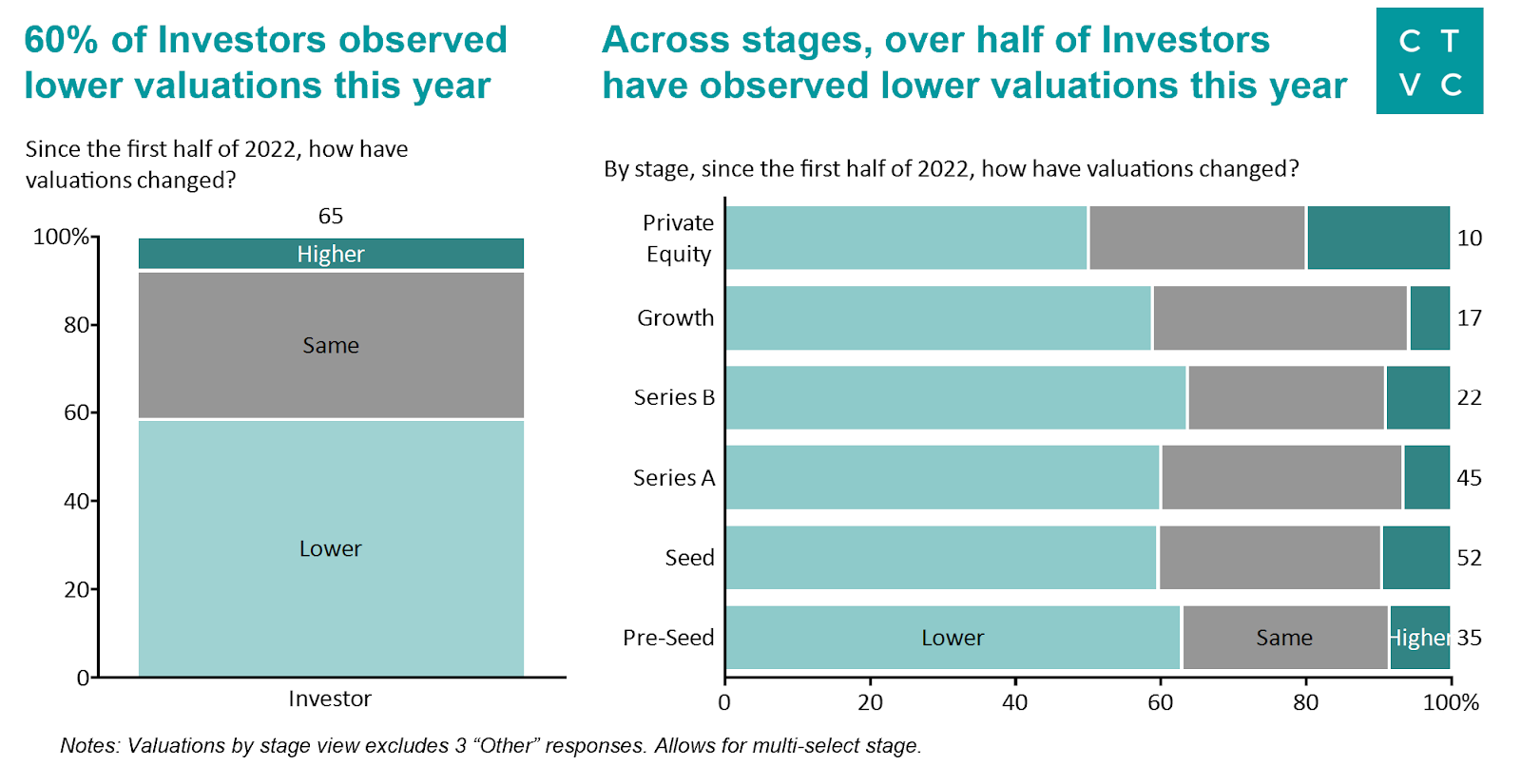

While all stages experienced slower deployment, early stage (pre-seed, seed, Series A) investors retained a relatively consistent pace

Mid-stage Series B deals are stuck in the dry funding valley of death with two-thirds of investors deploying more slowly

Similarly, 60% of investors noted lower valuations across the board, although with a host of caveats:

Many investors commented on a “quality” valuation bifurcation between highest-confidence deals retaining (if not increasing) their previous price highs while lower-confidence deals faced price cutbacks

Valuations for IRA-supported companies (e.g., battery materials, EVs, home electrification) reaped an IRA-sweetened sector valuation premium as investors anticipate a ~40% cost reduction from IRA’s multiple carrots (call it IRA-hot 🔥)

Founders are punting on valuation decisions by taking extension capital and raising via non-priced bridge rounds

Investors expected a greater drop in valuations than experienced, with many noting climate tech’s valuation premium relative to the broader market

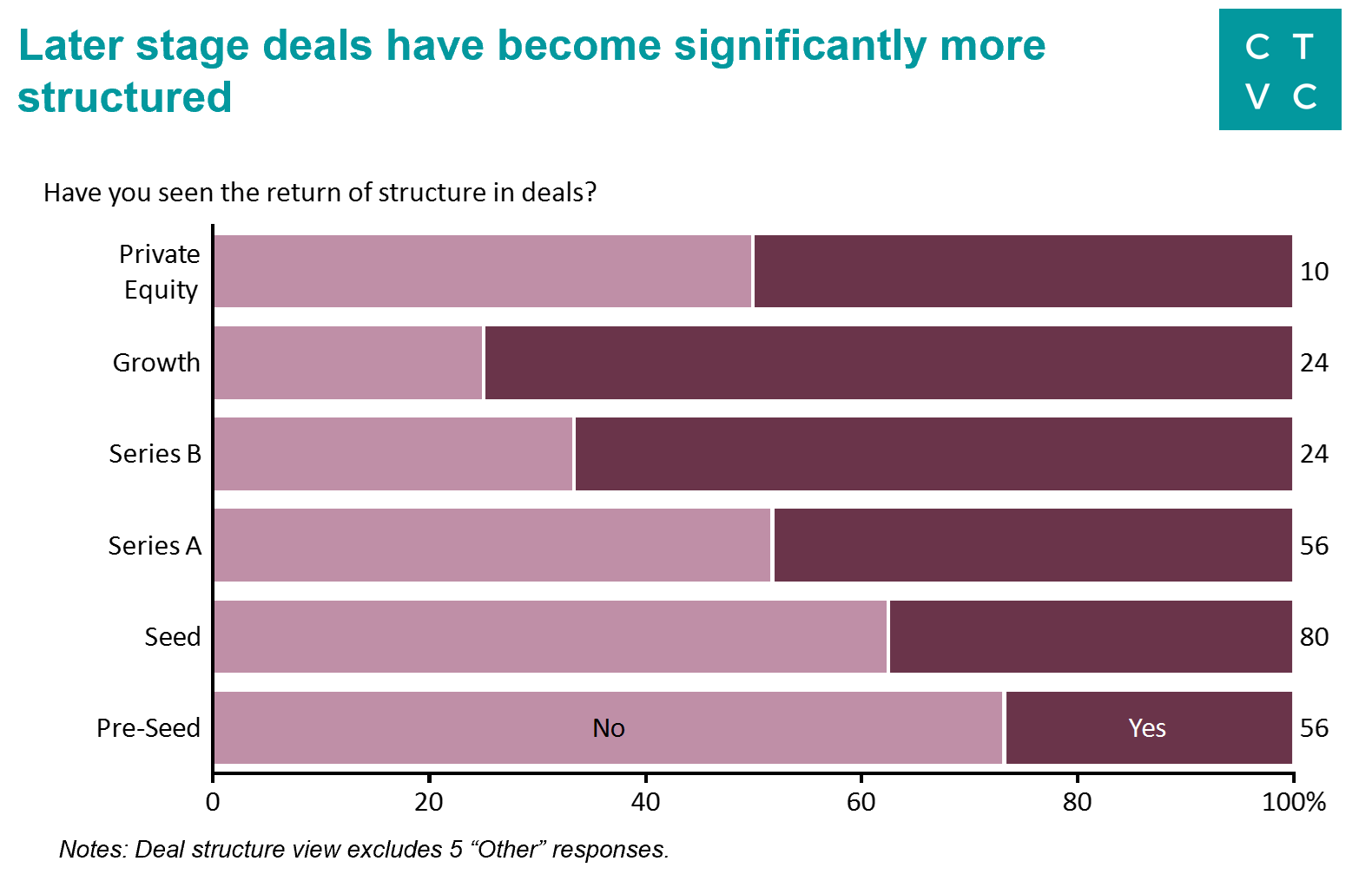

To no one’s surprise, later-stage and growth deals saw a lot more structure including the usual term suspects: higher prefs, PIKs, seniority, minimum returns, etc.

Later deal stages saw a (literal) step-change in structure prevalence, with early-stage deals leaning towards the “SAFE” end of the structure spectrum

Of the founders and investors who saw the return of structure, 30%+ noted higher liquidation preferences and 10% experienced more convertible rounds

1x+ liquidation preferences made a comeback, with 2-3x liq prefs for internal extension rounds

Many of the later-stage deals experiencing more structure fall into highly capital-intensive sectors

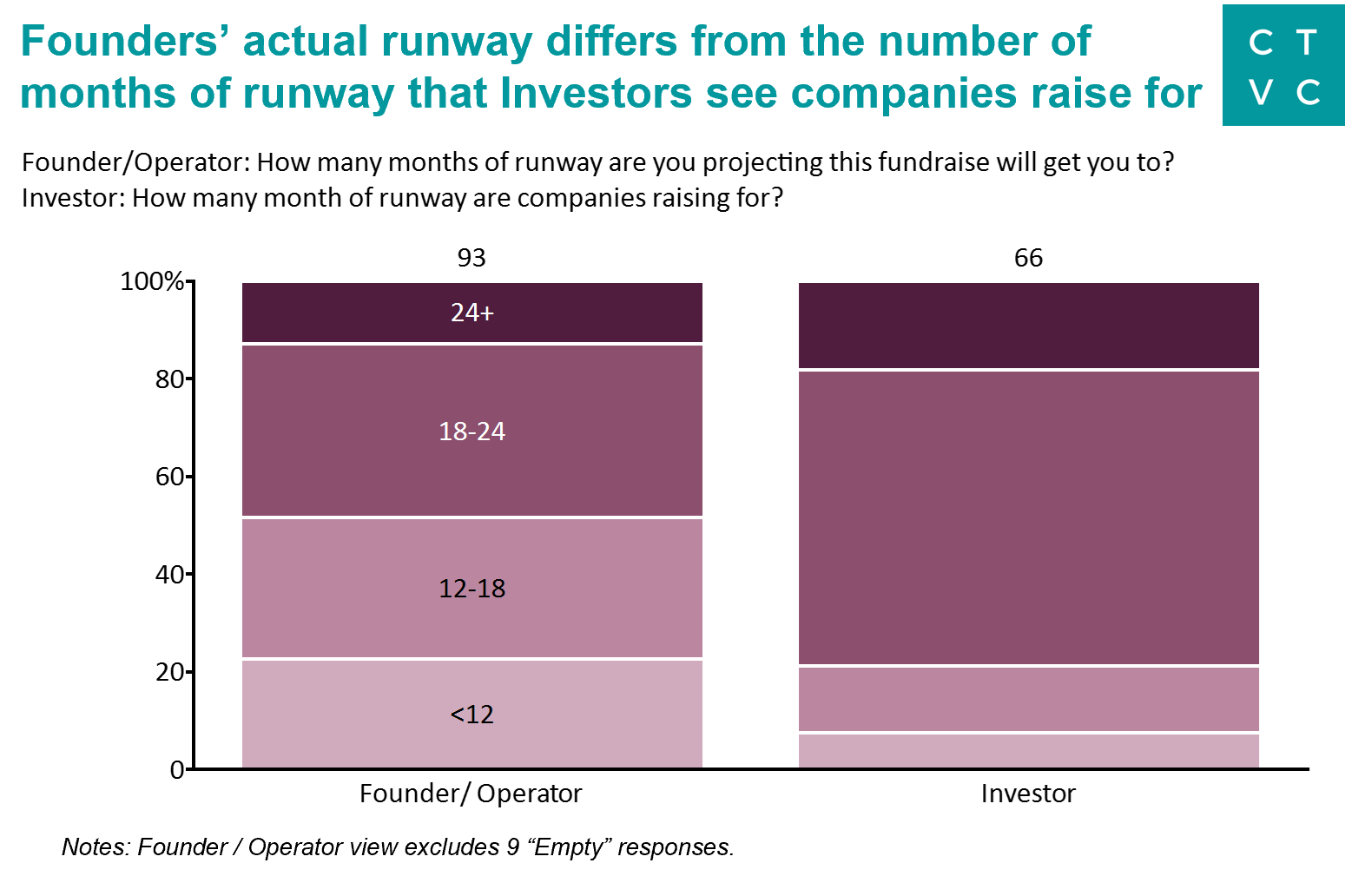

Half of founders have cash in the coffers for 18+ months of runway, though a quarter of founders are running low on juice with just <12 months of runway left

Meanwhile, 80%+ of investors saw companies fundraising for 18+ months of cash on hand

Investors are unsurprisingly placing critical emphasis on capital requirements and runway during diligence, alongside market traction and earlier proof of revenue - a signal of potential pull back from high technology’s longer and riskier timelines to revenue

Investors specifically called out the importance of quality, experienced, and resilient management teams - hopefully indicating a return to founder-investor relationship building and the end of the same-day term sheet

When asked about business models of greater interest, investors resoundingly parroted a reversion to the tried and true SaaS pastures of low-capex models. Interestingly, to the same question, some investors bemoaned the oversaturation of climate tech software (particularly accounting and carbon markets) and are instead taking the opposite tack and capitalizing on recently less competitive hardware opportunities

Across the board, investors are hanging high hopes on non-dilutive funding sources growing to meet pilot or FOAK facility build outs for high tech risk and high capex innovations (more non-dilutive funding tracking to come from CTVC soon)

Key Takeaways in your (abbreviated, anonymized) words

👩🏫 Reversion to the norm

“It’s back to normal. Great deals are coming together at strong valuations... not the insane valuations we saw in the SPAC era. Deals are taking a little longer, but are getting done.“

“I think the biggest collective mistake we can make is forgetting some key lessons we learned 10 years ago e.g. it's very tough for a business ultimately selling a commodity to sustainably be priced at 10x revenue.”

💭 Climate insulation

“Climate tech seems more insulated and less negatively affected from a valuation and pace perspective than other real-asset sectors we look at.”

“We’re still seeing great teams with good ideas, so hopefully early-stage climate remains insulated from the overall market environment.”

“We’re experiencing more investor caution, though the consensus seems to be that climate VC has not felt the pullback that other industries have. Nevertheless, the advice has been to increase our runway to get through a solid 18-24 months before the next raise.”

🔮 Oversaturation of capital vs opportunities

“There's an overabundance of money entering climate tech for the number of quality companies that exist. I worry there will be a reckoning or retreat of capital in the next 2-4 years.”

⏬ Further funding slowdown

“People seem to be overegging climate tech dry powder and instead don't discuss the effects of the denominator effect - LPs pushing for slower deployment, a general shift back to slower deployment of vintages that were raised recently, and many fund announcements before hitting their AUM target”

📉 Series B cliff

“Early stage still seems pretty hot, as does late stage growth capital deployment. I'm sensing that there is currently less climate VC money available for mid-stage (Series B/C) companies.”

💸 Flight to quality

“Fellow founders are all talking about how the best companies aren’t having trouble raising, but the next tier down is struggling.”

🔋 Specific interest in IRA sectors

“Everyone is thinking IRA. In general, we still think valuations in anything IRA-adjacent are inflated. That’s battery materials, EVs, transport, built environment, hydrogen etc.”