🌎 Taking the temperature at LCAW #302

Inside the $915m bet on carbon removal's next phase

Happy Monday!

We’re back from CERAWeek in Houston, where more than 11,000 people packed into two conferences, against a backdrop of war in the Middle East, oil at ~$100/bbl, gas up 30%+, and an AI power arms race that's remaking what an "energy company” is. We've got everything you need to know below.

In deals, $385m for utility-scale energy storage project development across two deals, $250m for energy efficiency as a service, and $52m for physical AI-powered robo-labor.

In other news, the US’ new equity stake in critical minerals, TotalEnergies’ complicated offshore wind shutdown, and Dominion Energy’s offshore wind acceleration.

Thanks for reading!

Not a CTVC subscriber yet?

📩 Submit deals and announcements for the newsletter at [email protected].

💼 Find or share roles on our job board here.

CTVC is powered by Sightline Climate, the tactical market intelligence platform for energy and investment decision-makers.

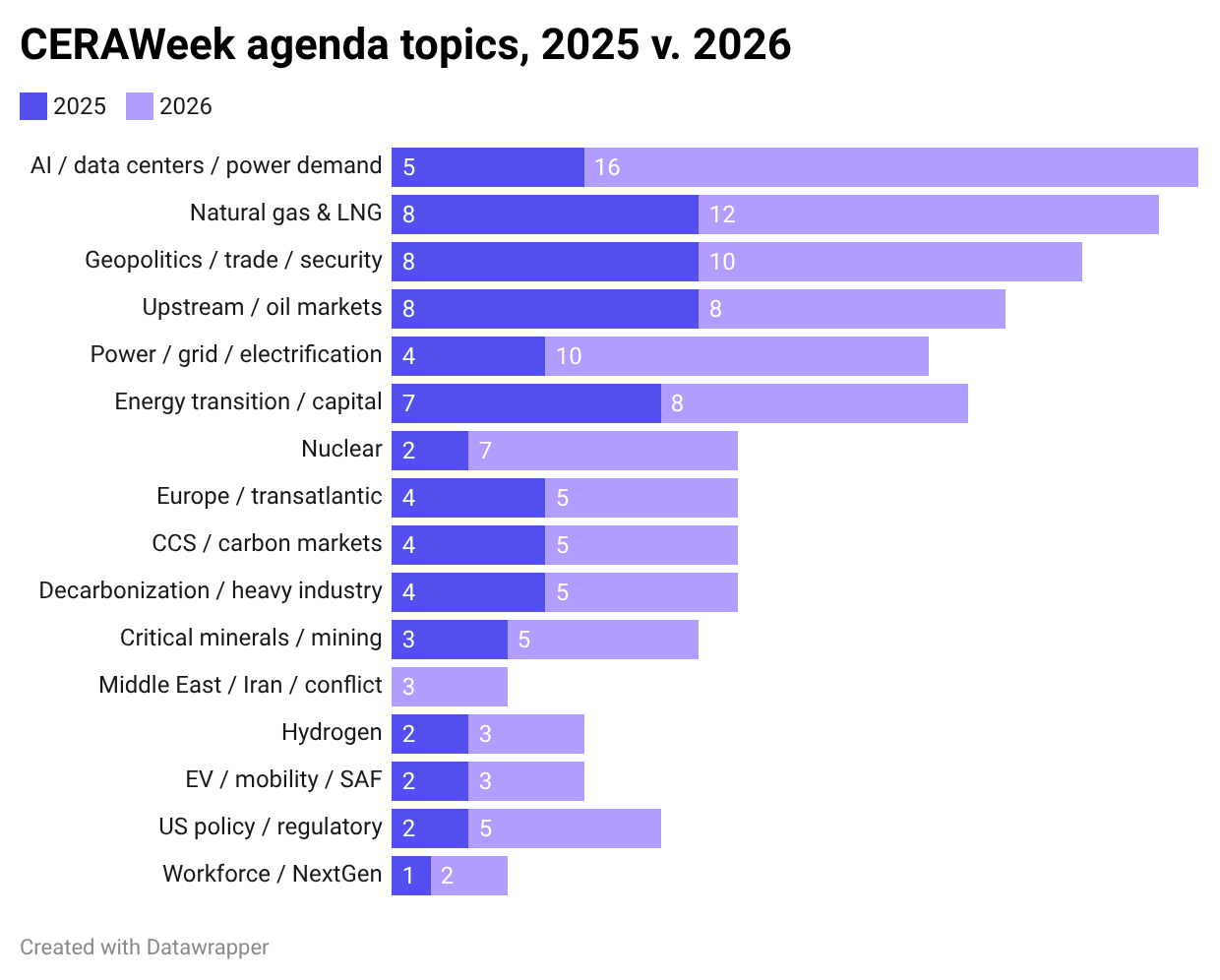

CERAWeek just made one thing clear: Houston, we have a queue problem.

This year, the “Super Bowl of Energy” was set against the backdrop of a war in the Middle East, the continued race to power AI, and of course 4+ hour TSA lines at the Houston airports.

The main throughline: Disruption is increasingly the new normal. And you can see and feel it most clearly in the queues. People around the world waiting for fuel supply. Generation and data center projects stuck in years-long interconnection queues. TSA lines stretching all the way from the basement amid yet another government shutdown.

This year, CERAWeek laid bare the return to the New Joule Order, as Carlyle’s Jeff Currie and James Gutman have laid out. Energy security first, affordability second, environment (unfortunately) third. And all on an increasingly regional scale. But even if the energy world is no longer putting environment first, don’t call it a trilemma. Look at Pakistan saving $6.3bn this year by using solar instead of buying O&G at current elevated prices. Or the need for speed and off-grid data centers delivering the next battery boom, even in long-duration. Here’s what else came up again and again.

1. Geopolitics makes the energy map multipolar. The Iran war and near-closure of the Strait of Hormuz made the geopolitical fragility of hydrocarbon dependence viscerally real. Countries that built renewables buffers are looking smart, and everyone else is scrambling.

2. Power and molecules continue to converge as AI creates opportunities. Tech companies are becoming energy companies. Google has 1GW+ in demand response. NVIDIA is designing grid-aware chips. Hyperscaler capex is the new gold rush, and every O&G major, renewables developer, and utility is angling for a piece of it.

3. Gas is America's self-proclaimed superpower. Energy Secretary Chris Wright said the quiet part loud: hydrocarbons first, AI second, everything else later. But backstage, people were more honest — new gas turbines have a 6-7 year lead time and costs have tripled. The "just build more gas" story is messier than the keynote made it sound.

4. Next-gen clean firm power and critical minerals had the strongest showing in years. Nuclear and geothermal had their moment. Wright flagged three next-gen reactors targeting early operation by July 4. Fusion showed up credibly for once. And geothermal, with a new standardized resource framework and a dedicated conference house, might have stolen the week.

5. The devil's in the permitting, labor details. Permitting and labor are the real bottlenecks. Willow took 5 years to permit and 4 to build. Grid infrastructure assumes a skilled workforce that doesn't exist yet. Google is training 130,000 electricians to try to close the gap. The hardware is almost the easy part.

🏭 RoboForce, a Milpitas, CA-based Physical AI-powered Robo-Labor platform, raised $52m in Series A funding from YZi Labs, Carnegie Mellon University, Gary Rieschel, Jerry Yang, and Myron Scholes.

🔋 Entrix, a Munich, Germany-based AI-powered energy storage optimization platform, raised $50m in Series A funding from Junction Growth Investors, Korys, ABACON CAPITAL, AENU, Allianz, Arvantis Group, and other investors.

🏠 Claros, a McLean, VA-based data center power management platform, raised $30m in Seed funding from General Catalyst, Red Cell Partners, Aero X Ventures, Systemiq Capital, and Trenches Capital.

🛰 Dronus, a Trieste, Italy-based autonomous industrial drone infrastructure provider, raised $17m in Series A funding from Algebris Investments, Azimut ELTIF, CDP Venture Capital, ENI Next, and SIMEST.

🧱 Cocoon Carbon, a London, UK-based low-carbon building materials manufacturer, raised $15m in Series A funding from 2150, Brick & Mortar Ventures, Celsius Industries, Gigascale Capital, SOSV, and other investors

☀️ Leapting, a Huzhou, China-based solar PV cleaning and installation robot developer, raised $15m in Series A funding from Capital Today, Glory Ventures, and Long Capital.

🚗 Scalvy, an Austin, TX-based distributed power delivery service provider, raised $14m in Series A funding from Silicon Badia, Azolla Ventures, Climate Capital, and SkyRiver Ventures.

🥩 Cauldron, an Orange, Australia-based next-generation biomanufacturer with a continuous hyper-fermentation platform, raised $13m in Series A funding from Main Sequence Ventures, Horizons Ventures, NGS Super, and SOSV.

♻️ Epoch Biodesign, a London, UK-based enzyme biorecycling platform company, raised $12m in Series A funding from Lululemon, Extantia, Happiness Capital, KOMPAS, and Leitmotif.

🌾 Miraterra, a Vancouver, Canada-based high-fidelity soil measurement solutions provider, raised $12m in Seed funding from At One Ventures, Farm Credit Canada, iSelect, S2G Investments, and Sitka Foundation.

♻️ Renasens, a Stockholm, Sweden-based CO2-based recycling technology developer, raised $12m in Seed funding from Extantia, Course Corrected VC, and Norrsken Launcher.

⚡ Applied Atomics, a Los Angeles, CA-based co-located nuclear power plants operator and developer, raised $8m in Seed funding from Morpheus Ventures, Transition VC, and Alpaca VC.

⚡ Pranos Fusion, a Bengaluru, India-based compact tokamak-based nuclear fusion technology developer, raised $7m in Seed funding from Ankur Capital, pi Ventures, Bhukhanwala Industries, Founders of Razorpay, Industrial47, and other investors.

⚡ Doral Renewables, a Philadelphia, PA-based renewable energy developer, owner, and operator, raised $245m in PF Debt funding from MUFG Bank, Ally, HSBC, IDB, and Santander.

🏠 Budderfly, a Shelton, CT-based energy efficiency as a service platform, raised $250m in Debt funding from Global Infrastructure Partners (BlackRock) and Vantage Infrastructure.

🔋 esVolta, an Aliso Viejo, CA-based utility-scale energy storage projects developer, owner, and operator, raised $140m in PF Debt funding from MUFG Bank.

⚡ HD Renewable Energy, a Taipei, Taiwan-based integrated renewable energy solutions platform, raised $34m in PF Debt funding from Nomura.

⚡ Verso Energy, a Paris, France-based renewable energy and synthetic fuels developer, raised an undisclosed amount in PF Equity funding from Technip Energies.

♻️ 800 Super, a Singapore-based integrated environmental management platform, raised an undisclosed amount in PE Buyout funding from Actis.

⚡ Revolv, a San Francisco, CA-based commercial fleet electrification platform, was acquired by Zenobe Energy for an undisclosed amount.

Climate Investment, a London, UK-based climate-focused investment firm, announced the final close of $450m for its Decarbonization Acceleration Fund (DAF), CI’s second fund and its first Growth Equity vehicle, focusing on scaling breakthrough decarbonization technologies and bridging climate tech’s “missing middle.”

360 Capital, a Paris, France-based venture capital firm, announced the first close of $98m for its Poli360 2 fund, focusing on early-stage deeptech university spinouts across Europe with a strong focus on Italy.

VitaminºC, a Zurich, Switzerland and San Francisco, CA-based early-stage venture capital firm, announced the first close of $21m for its debut VitaminºC Climate Fund, focusing on pre-seed and seed climate mitigation and adaptation startups across Europe and North America.

This is a sample of deals available for Sightline clients. Can’t get enough deals?

The US government's development finance agency (DFC) announced it was taking another equity stake in a critical minerals company, this time Australia’s Syrah Resources. The miner’s Louisiana facility is the first US supplier of key battery material, natural graphite. The deal highlights the US government’s push to secure critical mineral supply chains and reduce reliance on China.

TotalEnergies is exiting its US offshore wind projects and pivoting toward LNG investment after an intervention from the Trump admin, while also reassessing its net-zero strategy. The deal kills ~4GW of planned offshore wind capacity and sets a precedent -- the government will pay you to not build, but it’s not clear whether this is a template or a one-off.

In positive news, Dominion Energy’s Coastal Virginia Offshore Wind project has begun delivering its first power to the grid, which will become the largest offshore wind farm in the U.S. at 2.6 GW. The project highlights continued offshore wind progress, even in the face of political and legal challenges, as utilities push to meet rising power demand.

Form Energy will supply long duration iron-air batteries to data center company Crusoe, supporting its “bring-your-own-capacity” (BYOC) strategy to speed grid interconnection. With battery deliveries starting in 2027, the deal grows Form’s near-term pipeline and gives Crusoe a new option to power its data centers.

A growing number of ESG-focused funds are being liquidated in the US, with 91 funds shutting down in 2025 compared to just nine new launches. The trend reflects political backlash, weaker demand, and consolidation across ESG products after years of rapid growth.

Europe’s cleantech boom stalls, with Sightline data featured.

From sewer to carbon capture, Norway deploys first of its kind BECCS project

Climate insurance scales up for millions in Lagos.

The one kind of pod we'd like to hear more about: a whale’s birth, backed by a pod.

New species emerge from Cambodia’s hidden caves.

Getting hot in here: Heat pump economics.

📅 SOSV – Heat Beneath Our Feet: Join us on April 9th from 6-8pm EST in NYC for a fireside chat with Carlos Araque (CEO, Quaise Energy). Learn why conventional geothermal has stalled, how companies are designing for deeper and hotter wells, and how Quaise is building the country’s first super hot geothermal power plant.

📅 Europe Energy Tech Summit: Attend Europe's premier energy innovation event, hosted at the Euskalduna Conference Centre in Bilbao, Spain from 15-16 April, 2026. CTVC subscribers can get 15% discount with the code: SIGHTLINECLIMATE.

Reporter @ Grist

Software / Machine Controls, @Dig Energy

Growth Associate, @Coral

Investment Associate, @Energy Impact Partners

XIG Imprint Business Development Lead - Vice President @Goldman Sachs

Junior Account Executive, @3V Infrastructure

Data Analyst – Late-Stage Finance, @Sightline Climate

Associate, @Prelude Ventures

📩 Feel free to send us deals, announcements, or anything else at [email protected]. Have a great week ahead!

Inside the $915m bet on carbon removal's next phase

Inside the $915m bet on carbon removal's next phase

A letter from the co-founders, Kim Zou and Mark Taylor

Newsletter

Newsletter