From CA Gov. Newsom’s EV announcement to the recent surge in SPACs, the new interest and funding into climate tech has made 2020 feel like the year electric vehicles have finally rolled into the mainstream. The technology driving and scaling the fleet? Batteries.

Last week, Tesla had its much-anticipated Battery Day, a bonanza for climate tech nerds rivaling Apple product drop announcements. Despite some disappointment from investors who expected a faster timeline to reach the coveted million-mile battery, Tesla’s presentation maps the route for future battery engineering, highlighting that innovation will come from manufacturing changes vs. chemistry R&D in the run up to scale.

Driving down costs at Tesla’s Battery Day

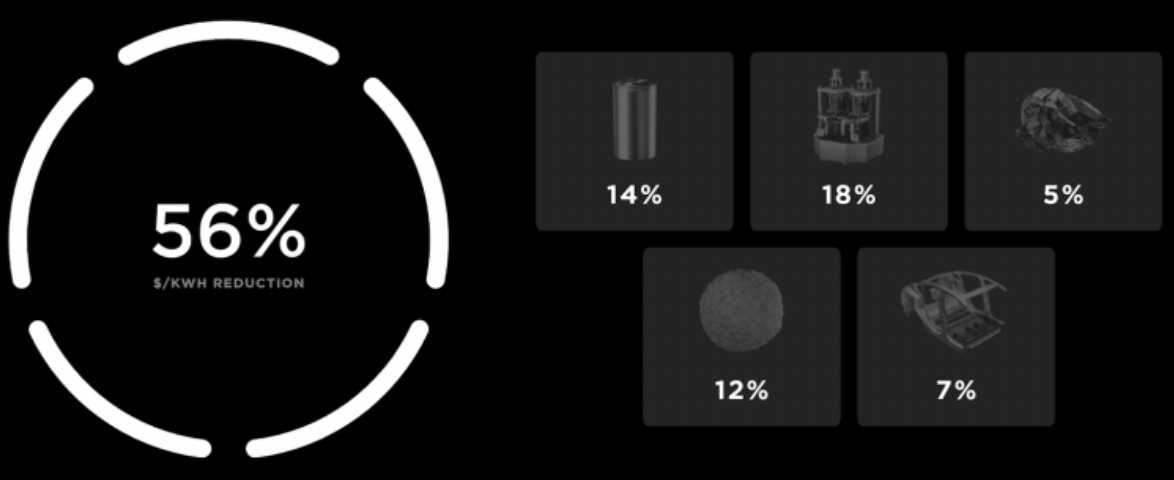

The underlying theme of Tesla’s Battery Day was price – specifically, a 56% reduction in cost / kwh of the battery pack. Musk & Co’s announcements focused on five key engineering challenges which, together, will enable Tesla to reach the coveted goal of a $25K vehicle within three years. “They’ve essentially reimagined the entire manufacturing process of the lithium-ion battery from raw materials to the finished product,” says James Frith, head of energy storage at BloombergNEF (BNEF).

Tesla’s Battery Day presentation centered around 5 key engineering challenges that will reduce battery $/kwh by 56%

Tabless design: A “shingled spiral” design provides uniform current distribution to the 5x longer electrode, reducing heat, and increasing the lifetime of the battery.

Dry coating: Eliminating the coating and drying steps from a wet electrode process reduces both factory and energy footprints by 10x, significantly improving manufacturing sustainability (and speed).

Silicon anode: Replacing graphite with cheaper silicon could increase range ~20% and lower cost ~5%, but the exact approach and anode Si% remain unclear.

Nickel cathode: Removing cobalt from the battery by using a high nickel cathode reduces reliance on expensive and suspect supply chains. Tesla will also adopt a novel saline-extraction process for lithium from clay deposits and repatriate cathode manufacturing in the US.

Structural batteries: Using a cylindrical cell design allows for the battery pack to be integrated into the vehicle chassis and structurally stiffen the car.

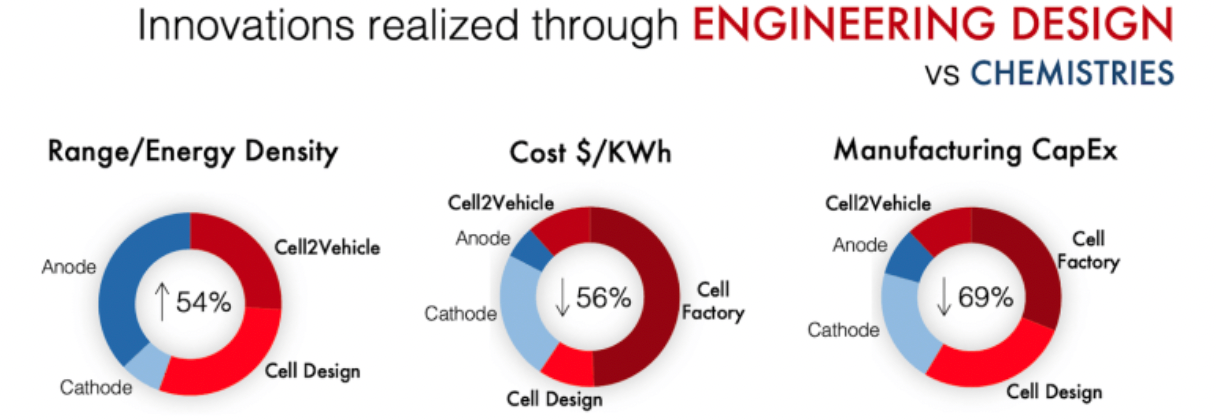

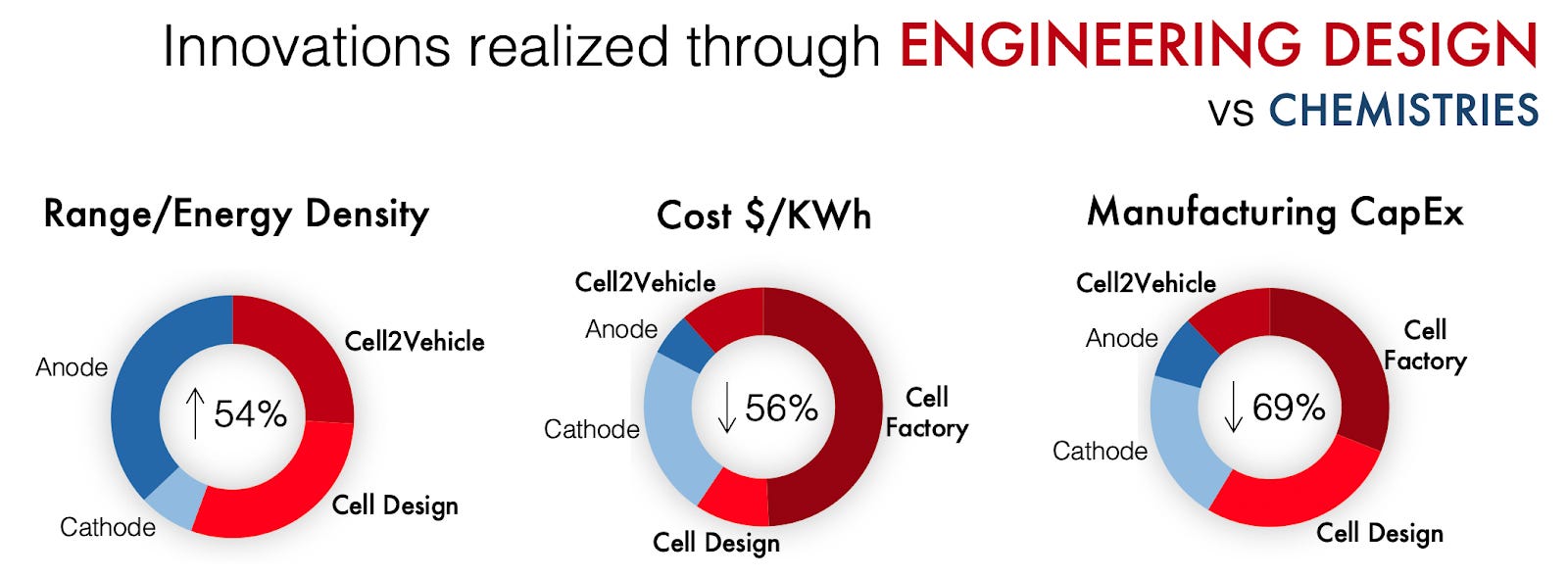

Indeed, as the folks at Intercalation Station visually show in red, most of Tesla’s innovation is realized through engineering design – not chemistry R&D.

Intercalation Station newsletter visualizes how engineering design – not chemistry – drives majority of Tesla’s innovation.

Call (and response) to industry

Tesla’s presentation ended with a call to industry to “help accelerate the transition” to battery power. We’ve outlined below the current and future market movers integral to this call to arms.

China controls ~70% of battery manufacturing capacity. The world’s largest emitter monopolized the industry by investing top-to-bottom in raw material mining and processing for lithium-ion batteries. Outside of their own borders, they crucially control much of the African rare metal supply chains as well as deepsea polymetallic deposits.

Keep your friends close. While undoubtedly the US EV goldenchild, Tesla is in a manufacturing race against a world of competitors to grab market share. If Musk’s notoriously aggressive timelines lag, fast following startups could establish competitive technologies before Battery Day announcements have time to bear fruit.

Two next-gen battery innovation pathways.

Silicon Anode: Like Musk mentioned above, replacing graphite with silicon in the anode would significantly improve energy density and lower cost. However reaching 100% silicon isn’t currently possible, and startups are experimenting with silicon doping – a variable mix of silicon and graphite. Fortunately for these startups, their materials can be dropped seamlessly into the current battery manufacturing process. Innovators: Silar Nanotechnologies, Enovix, Enevate, Amprius Technologies, Advano

Solid-state: Instead of using a liquid electrolyte, solid-state batteries are touted to be safer and have higher energy densities. However, mass adoption of these batteries aren’t expected until 2030 as building cells with a solid electrolyte requires some significant modifications to the current manufacturing process. Most startups will likely license their technology to a manufacturer, but companies like Prologium are looking to build their own facility. Innovators: Quantumscape, Solid Power, Ionic Materials, ProLogium, QingTao Energy Development

Key Takeaways:

Expect to see parallels to the solar market. As we’ve seen happen in the solar market, scaling up manufacturing leads to price declines much faster than expected. In 2011, BNEF predicted battery prices would be $350 / kWh in 2020 – we’re now at $130 / kWh. We will continue to see prices decline faster over the next decade as adoption picks up.

EVs haven’t reached scale yet. EVs only made up 2.5% of global car sales in 2019 and despite Tesla’s prowess, gas counterparts still push out cars at much faster speeds (with Ford producing 25 vehicles per 1 Tesla). EV manufacturing maturity is needed to compete with the rest of the auto market.

But EV (and battery) demand is growing. Last week, China and California both made profound decarbonization commitments which will significantly increase EV demand. Policy and regulation, such as tax incentives, have historically been the main driver of EV sales, but passenger vehicles are only one segment of the battery market. Still to come is the electrification of larger vehicles (buses and trucks) and grid-scale energy storage. Tesla and Nikola have both made splash announcements about their future fleet of electric trucks. On the grid side, 114 gigawatts of solar + storage are coming online in the US alone.

And raw material supplies can be limited. With more battery makers seeking lithium, cobalt, and nickel, Tesla and other EV manufacturers will face difficulties when scaling up to meet increasing demand. Fortunately market forces drive innovation, and lower supply of raw materials will require cell and manufacturing processes to adapt (e.g., companies now switching to lower cobalt chemistries).

TLDR; We’re seeing a dramatic lurch forward in demand for EVs as nations and states commit to climate action. Similar to the dynamics from the solar market, we’ll see the mass market adoption of EVs scale as incremental manufacturing improvements ratchet down the cost curve. The next decade of battery innovation will pave the way for the decarbonization of the transportation sector, but not without the concomitant struggles that any new technologies and industries dependent on raw materials have faced.

Interested in more content like this? Subscribe to our weekly newsletter on Climate Tech below!

{kind=link}

{kind=link}