🌍 Rise of the robots, NY Tech Week edition

What happens when climate tech meets robotics

China is - and must be - part of the climate solution with Alex Li

This week, China will determine its top leadership for the next five years. As senior officials convene for the Party Congress (a once every half-decade event), the eyes of the world turn to Beijing. It’s a pivotal moment for China, and comes as the country commands a particularly pivotal influence globally. What happens in the halls of the Party Congress will have an acute effect worldwide on the management of the global economic downturn, tensions with the West, pandemic recovery, and - of course - climate change. In short, what happens this week matters globally. The role that China plays in the global economy and specifically, the transition to net-zero, is center stage.

Two years ago, China committed to carbon peaking by 2030 and net zero by 2060. China is at the epicenter of the climate crisis and a case study in managing its simultaneous opportunities and challenges - generating emissions, deploying mitigating climate tech at-scale, and adapting to threats while suffering from the current climate catastrophe.

💨 Emissions: China is the world’s top carbon emitter, generating about 25% of global emissions, more than double that of the US. Last year China built more coal plants than the entire rest of the world, combined.

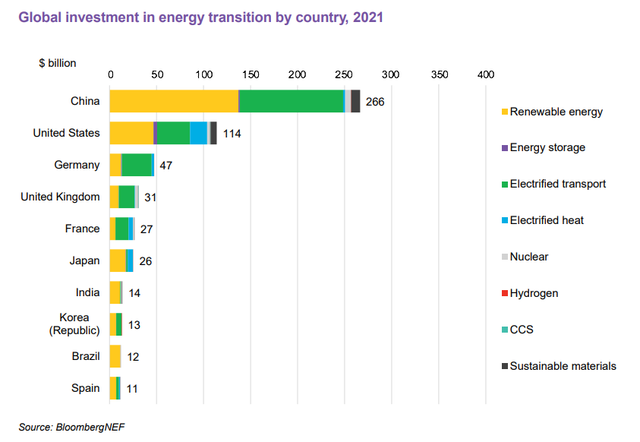

⚡ Climate tech: Simultaneously, China is a climate deployment juggernaut - producing record volumes of EVs and renewable energy infrastructure. According to BNEF, China is by far the world’s largest energy transition investor, spending $266B on the deployment of low-carbon technologies in 2021, more than a third of total global spend.

☔ Catastrophe: This summer, China was ravaged by two months of record heat waves that dried up the Yangtze River and shut down manufacturing (ironically for a lot of those same climate tech solutions). The prior summer, the country suffered the opposite catastrophe, with torrential downpours flooding subway cars and causing over $25B of losses.

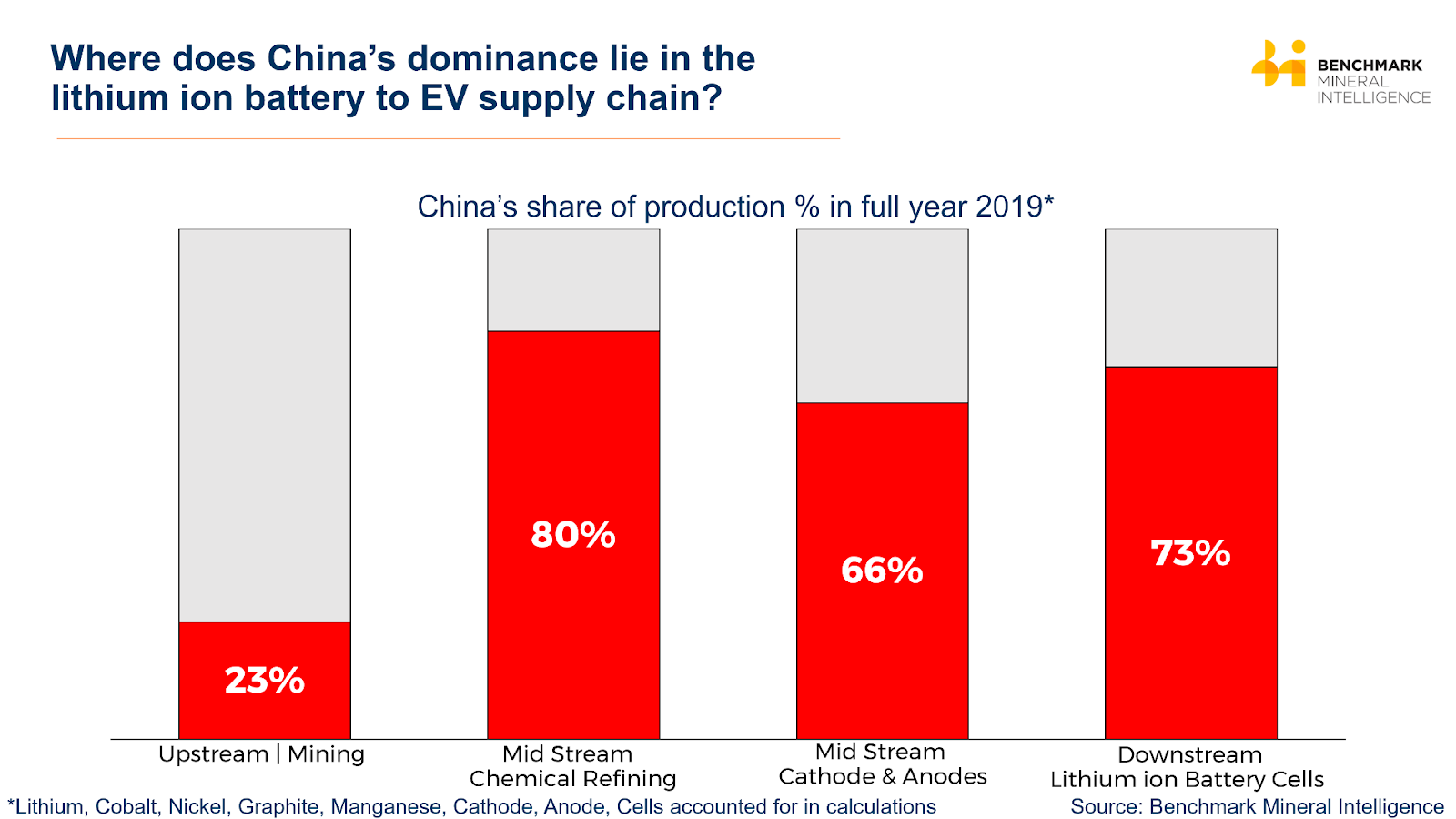

China first put a heavy thumb on the scale during Cleantech 1.0, leveraging its manufacturing prowess to drive solar PV prices way down and causing high-flying cleantech startups to topple one by one (along with venture returns). Now the country has become the world’s manufacturing powerhouse for several key climate technology areas, such as solar photovoltaics (PV), wind turbines and batteries for electric vehicles (EVs). China controls 80% of the manufacturing critical to solar panel production (polysilicon, ingots, wafers) and ~80% of both the world’s lithium-ion cell capacity and raw lithium refining. China-based CATL is the largest battery maker in the world supplying the majority of auto OEMs - even counting vertically-integrated EV darling Tesla as a core customer.

China dominates not just from the supply side, but leads in demand as well. The world’s most populous country produces 307 GW of solar capacity, a commanding lead over the US at 95 GW (~30% of China’s share). On EVs, more vehicles were sold in China in 2021 (3.3 million) than in the entire world in 2020. Today, the streets of large cities like Shanghai are filled with EVs made by XPeng, NIO, BYD, Li Auto, SAIC, and Tesla, to name a few. Outside of apartment buildings, it’s common to see battery swapping stations that can fully charge a car in five minutes. In China electric driving is the present, not the future.

Despite China topping the world’s charts in climate tech supply and demand, there’s a surprising lack of outside coverage on China’s climate tech innovation and development landscape.

There is no equivalent word for “climate tech” in Chinese. The most popular phrase is “new energy” (新能源) but that leaves out sectors like manufacturing and agriculture. Other words like “net zero” (零碳) and “ecological” (生态) are starting to get mixed in to broaden the category, but there’s no general consensus on the definition, even within China.

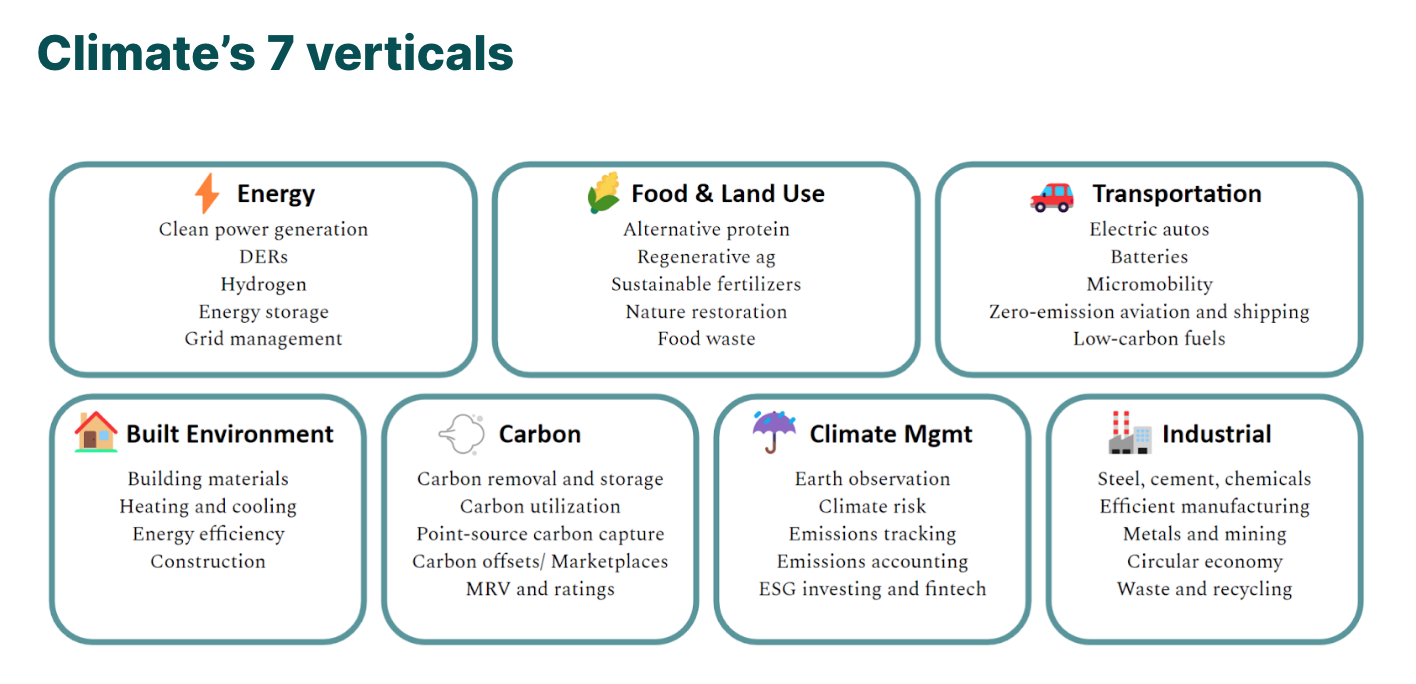

We’ve used the CTVC categorization of “Climate’s 7 Verticals” as a framework to investigate China’s climate developments.

Exploring each of these sectors reveals that major developments in China may not look like climate tech successes in the West. The big players are not venture-backed startups. Rather, they are industrial giants, state-owned enterprises, or government-led initiatives. These organizations may be overlooked externally as they blend in with the rest of China’s state-sponsored economy - but we must look more closely, as these organizations will play a critical role in the global response to climate change.

China’s approach across climate verticals comes in two predominant forms. First are industrial players with large manufacturing capabilities. These organizations may either be private companies or state-owned enterprises (SOEs). Second are government-led environmental or climate initiatives. These often require the coordination of various government agencies and private sector companies (e.g. China’s national emissions trading system). Below are examples of China’s industrial and state presence across climate’s verticals.

⚡ Energy: new energy giants manufacturing the global energy transition

🏭 Industrial: producing critical materials and inputs for climate supply chains

🚗 Transportation: rapid deployment of electric vehicles into the domestic market

🏠 Built Environment: supplying the raw inputs for construction

💨 Carbon: the world’s largest regulated carbon market

🌾 Food & Land Use: nation-wide movement to increase tree coverage

Despite China’s outsized role in climate, many of these industrial and state-owned giants didn’t start as climate-first. Beifang Rare Earth supplied rare earth elements decades before they were core elements in high-efficiency wind turbine generators. CATL began as ATL, a company that mostly made lithium-ion batteries for retail electronics.

For decades, China’s core competency has been big industry and big government. With the shift to net zero requiring the same industrial and manufacturing prowess, China subsequently has taken on an outsized role in climate tech.

In addition to scale, climate deployment in China is characterized by speed. The electric Wuling HongGang MINI started production in 2020, and in just 2 years challenged Tesla as the top-selling EV model (granted, it’s a different customer value proposition!)

A host of factors enable China to rapidly deploy new climate tech. The country has built up manufacturing capacity and an experienced workforce. Its domestic supply chains are robust and can locally source many of the necessary inputs. However, two factors in particular stand out:

Adaptable consumers: China’s economy has undergone immense change over the past half century. 700m people have been lifted out of poverty and urbanization has expanded throughout the country. This hyper-adaptable population is ready to try new technology and products - first with the widespread adoption of WeChat and mobile payments, now with EVs and e-mobility. Consumers are adopting EVs at an increasing rate, with sales this year on track to triple sales from 2020.

Adaptable government: China’s various governmental institutions react quickly to strategic initiatives set by the central government in Beijing. On climate, China’s core policy is called “dual carbon,” which sets goals for the country to peak carbon emissions by 2030 and achieve carbon neutrality by 2060. Likewise, the government has made climate a top priority in its most recent Five-Year Plan, which is used to guide the country’s overall economic development. To support these goals, China’s government plays several roles in the deployment of climate solutions:

China’s climate tech deployment prowess extends far beyond the country’s borders. In 2021, China exported 182GW of solar modules, more than 3x the solar module capacity installed domestically. NIO is now offering EVs and installing battery swapping stations in Europe and CATL, the world’s top battery maker, is planning build battery manufacturing capacity in North America to supply Ford.

But engaging in the reverse is a trickier feat. Ultimately, accessing China’s market or supply chains is best done through cooperating with the government. This can be done in several forms:

🤝 Partnerships: For non-Chinese climate companies to establish themselves in China, it is critical to establish partnerships with China’s SOEs and industrial giants. These industrial players may have ideal use cases for climate solutions such as low-carbon steel production, green hydrogen, and CCS. Lanzatech, a US CCUS startup, found the first application for its technology with Shougang, a steel manufacturer outside Beijing.

🏗️ Demo Zones: China has precedent piloting new policies and technology in limited regions or demo zones. Within these zones, the government actively promotes international trade and technology innovation. Companies looking to find a foothold in China can consider demo zones such as the “Yangtze River Delta Integrated Ecological and Green Development Demonstration Zone,” which covers 4 provinces including Shanghai. Within these zones, the government offers benefits such as cheap land, simplified permitting, and modern infrastructure.

As engaging China requires government cooperation, changes to the central leadership this month will likely affect the country's stance towards foreign investments and partnerships. While much is uncertain, we can count on climate remaining a high priority. At the same time, we can count on state-owned enterprises to keep manufacturing materials for the energy transition. And we can count on new models of EVs to keep appearing on the streets of Shanghai. All this makes China a key climate tech player to watch.

Chinese industrials are the next frontier for decarbonization. These players are both the root of and the solution to the climate crisis - producing ~25% of global carbon emissions but also enabling global supply chains to produce low-carbon technologies. These organizations don’t shine with the “climate tech” veneer of similar players in the West. They might be decades old and sit further up the supply chain to produce basic inputs. Yet it’s these types of companies that McKinsey calls “the next frontier for decarbonization.”

There’s plenty of decarbonization headroom. The country does not expect to peak carbon emissions until 2030 before making a hard-turn to achieve net zero by 2060. To eliminate 25% of global emissions, China will need to invest an additional $17T towards climate tech and 5x its current renewable energy production.

Precedent for China and the West to partner and succeed together. Despite current tensions, there is precedent for very successful collaborations between China and the US/West on climate. The company that produces the top-selling Wuling HongGang MINI is a Sino-US joint venture between the SOE SAIC, GM, and Wuling. For non-Chinese players looking to expand into China, it is critical to engage the government, which can be done through partnerships with SOEs or by landing in a state-sponsored demo zone.

This is a key moment in time. China’s domestic climate sectors have seen rapid growth over the past several years. However, economic downturns, the pandemic, and geopolitics have notably deteriorated China’s foreign business relationships. Meanwhile, climate has fallen under the spotlight of US-China competition as both nations vie for global influence and economic leadership. With the passing of the Inflation Reduction Act, the US is revving to play catch up with China in critical climate sectors. Fortunately, competition between two global superpowers with opposing deployment and innovation offensive strategies should lead to one hopeful winner: rapid global decarbonization.

Reporting on the state of anything in China from abroad gets distorted through the looking glass. Massive thanks to Alex Li who is a researcher and engineer focused on climate solutions, and currently based in Shanghai. Alex works in China’s new energy sector and studied China’s role in climate tech as a Schwarzman Scholar. Follow along with @alexfieldli for more insights on the ground.

What happens when climate tech meets robotics

$90bn in climate dry powder in Q1 2026, after record fundraising in 2025

A breakdown of China’s new FYP and what it means for the next decade of the energy transition

Newsletter

Newsletter