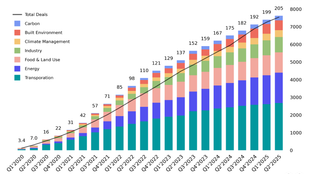

Our annual end-of-year Climate Tech Global Investment Trends reports have uncovered what we call “Big Three” verticals that get the most investment — energy, transportation, and food & land use (although food & land use only overtook industry in 2023).

But global trends don’t tell the full story. At Sightline Climate, we recently released a new feature on the platform, the Investment Dashboard, that provides deeper insights into market trends across different geographies, sectors, sub-sectors, and time frames. Clients use the tool to see top investors in a sector, get the data behind a spike in investment, download the charts to frame an investment thesis or strategic initiative, and more — to learn more and explore the tool, set up a demo here.

For existing Sightline users, check out the Investment Dashboard here.

Here, we're going to be asking the tool to answer a basic question — does climate tech investment vary by geography? Zooming in, distinct local nuances emerge as regional trends start to diverge from each other, and sometimes, those global Big Three.

We pulled the data (find our methodology at the end of this piece) and to understand why it looks this way, we spoke with local investors and founders about what's driving these varying concentrations of climate tech. Overall, regional factors such as government policies, market demand, existing infrastructure and corporates, and the availability of supportive capital play crucial roles in attracting investment to specific sectors by geography.

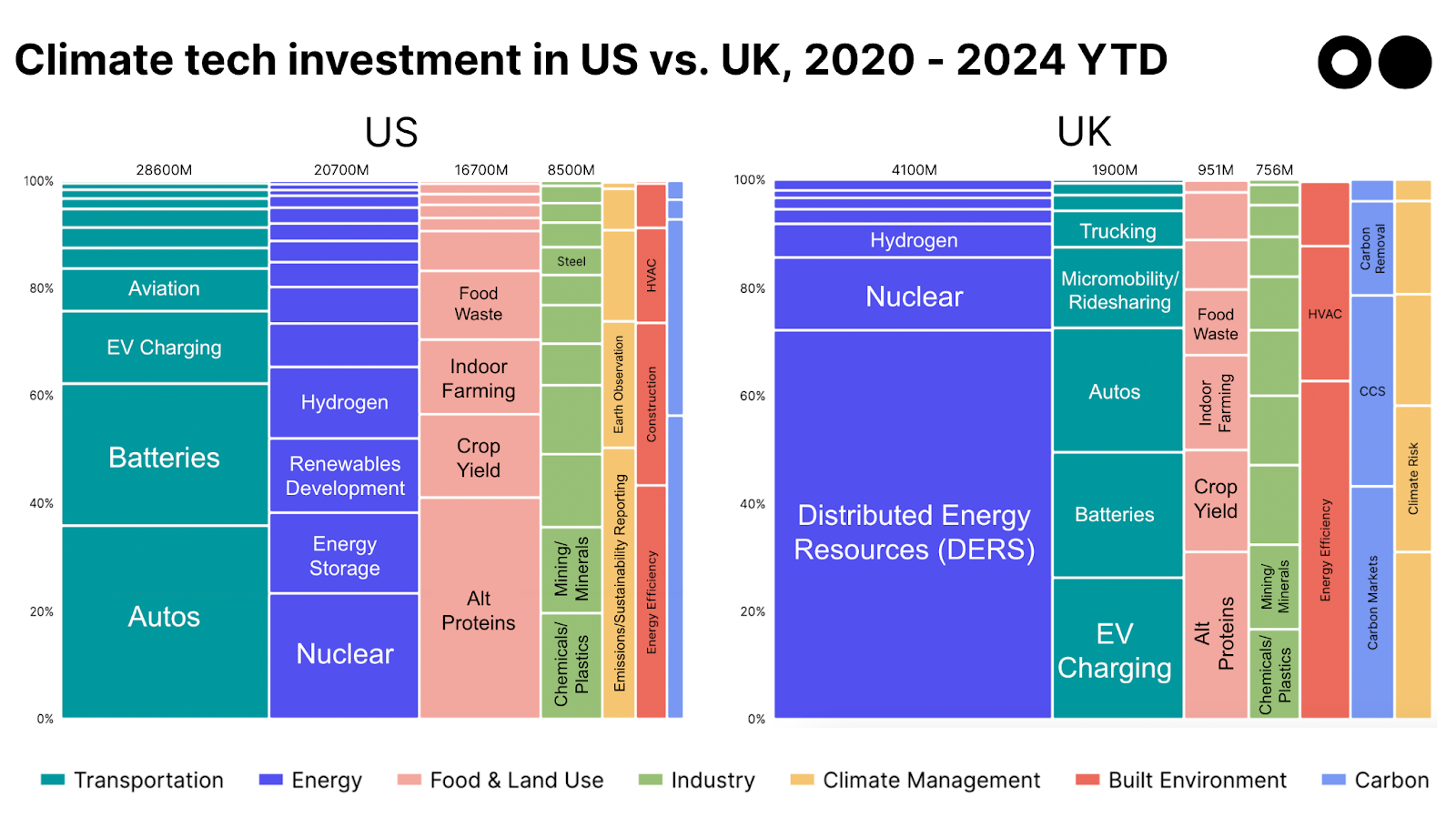

In both the US and the UK, the “Big Three” reign supreme — but not uniformly. The US has much greater investment in EVs, whereas the UK draws more for distributed energy resources. Megadeals in EV autos and trucks like Rivian, Proterra, Nikola, and Lucid Motors topped US charts, while multi-mega-round investment in Octopus Energy swept the board in the UK.

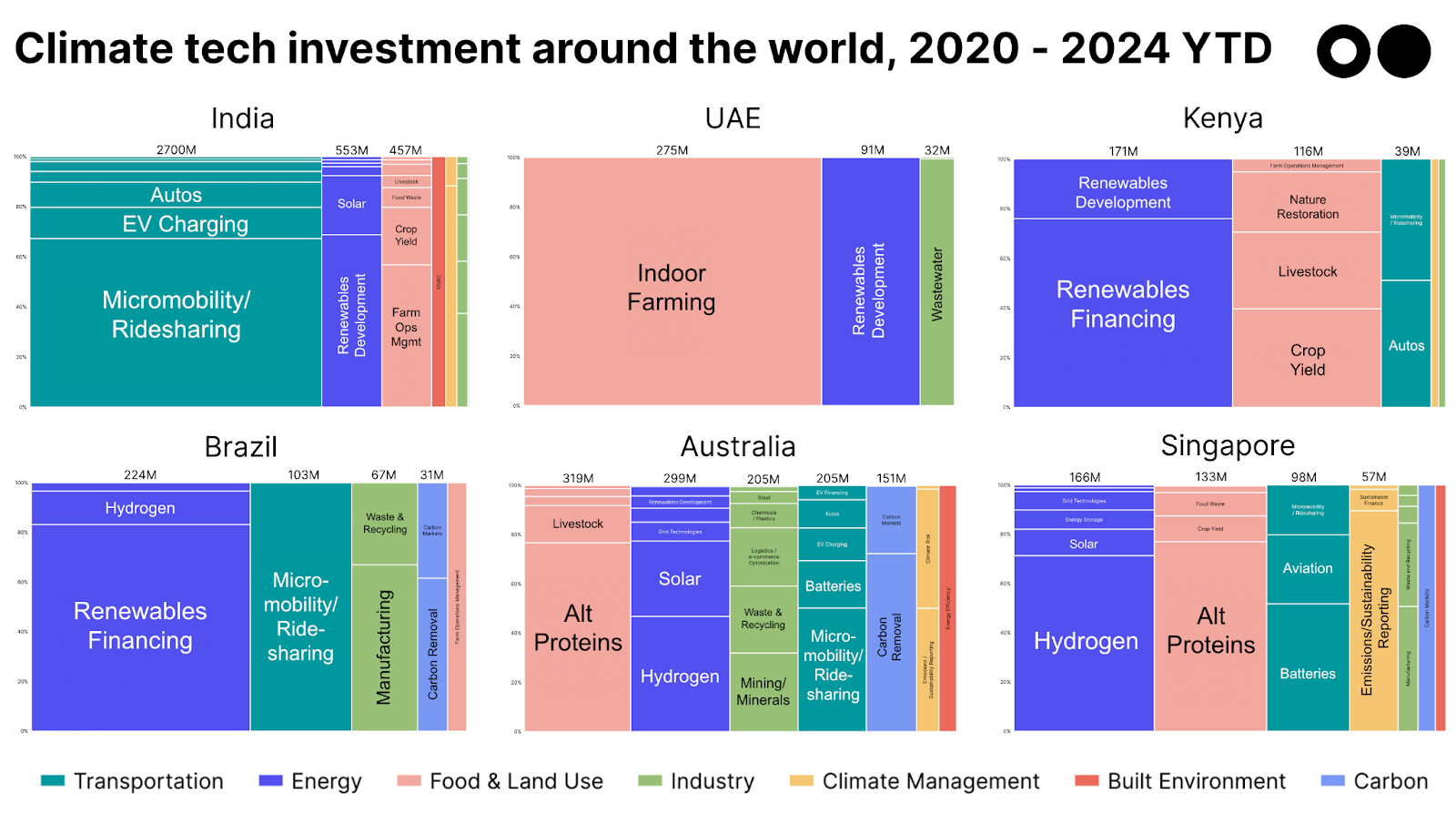

Going on a world tour away from the West, different trends emerge.

Context: “Mobility as a sector has been catalyzed by strong government push promoting clean mobility. Mandates for commercial fleets to transition to electric vehicles (EVs) by 2030, subsidies on lithium-ion cells, and regulations like FAME II are some of the keys steps, leading to increased adoption and investment in this sector,” Swapna Gupta, partner at Avaana Capital, told us. “Additionally, India is largely an agrarian economy and presents a significant market opportunity for disruption, solving for food security as well as water use. This has attracted massive investor interest and startups in agriculture.”

Context: Initiatives like the Dubai Clean Energy Strategy 2050 aim to make Dubai a global hub for clean energy and green economy, targeting 75% of Dubai's total power output from clean energy sources by 2050. Additionally, as a water-scarce region, efficient wastewater treatment and recycling are crucial to meet the growing water demand. And with the country's arid climate and limited arable land, indoor farming technologies attract investment.

Context: As James Mwangi, founder and CEO of Africa Climate Ventures, told us, "Most investment activity in Kenya and across Africa focuses on climate solutions for low-income consumers, addressing their needs with climate-smart solutions. Additionally, voluntary carbon markets offer subsidies or competitive advantages for some technologies, like carbon credits driving fuel transition and reducing deforestation through clean cooking. With new initiatives and commitments such as the Africa Climate Summit’s Nairobi declaration on Climate Positive Growth and resulting policy moves by countries such as Kenya, there’s more opportunity for the region.”

Context: Guilherme Penna, partner at Silence VC, outlined the Brazilian climate tech landscape: “Energy investments are driven by untapped potential and favorable tax incentives in renewables, along with an evolving regulatory landscape in infrastructure and services. The transportation sector is also shifting towards EVs, with sales nearly doubling in 2023, supported by government initiatives. And with only 13% of urban solid waste being correctly recycled, there's immense potential to optimize recycling logistics, supply chains, and industrial processes through AI investments. Meanwhile, the VC landscape has evolved over the past five years, with both global and local funds receptive to digital climate-related investments. However, Brazil's capital stack lags for deep tech and hardware, with limited grants and challenging debt acquisition. Revenue-based financing remains the primary funding avenue for projects, posing substantial obstacles for FOAK initiatives.”

Context: Lucinda Hankin, head of venture at Grok Ventures: “Australia is a major exporter of resources, energy and food — so the concentration of capital and efforts in these sectors is unsurprising. Australia also has one of the most advanced electricity grids in the world, with the highest penetration of residential rooftop solar and incredible solar and wind resources. This makes Australia an attractive first market for technologies solving evolving grid dynamics as well as technologies requiring low cost electrons, like electrolyzers and synbio-based food production. On food, Australia has compelling market positioning within Asia, in terms of trust, brand and existing export channels. Additionally, Australia has a fertile early-stage funding environment – including VCs and HNWs, as well as increasing government support for innovation across institutions like ARENA, CEFC, and the National Reconstruction Fund. On the other end of the spectrum, we have enormous pools of capital seeking to deploy into later-stage, proven technologies, including $3.7 trillion held in super funds.”

Context: As a global food innovation hub, Singapore leads in developing alternative protein sources, supported by government funding and regulatory frameworks. Investments in solar energy, including innovative solutions like floating solar panels, reflect the country’s strategy to adopt renewable energy despite geographical limitations. Addressing food waste is also a priority, with investments in technologies to reduce waste and enhance recycling.

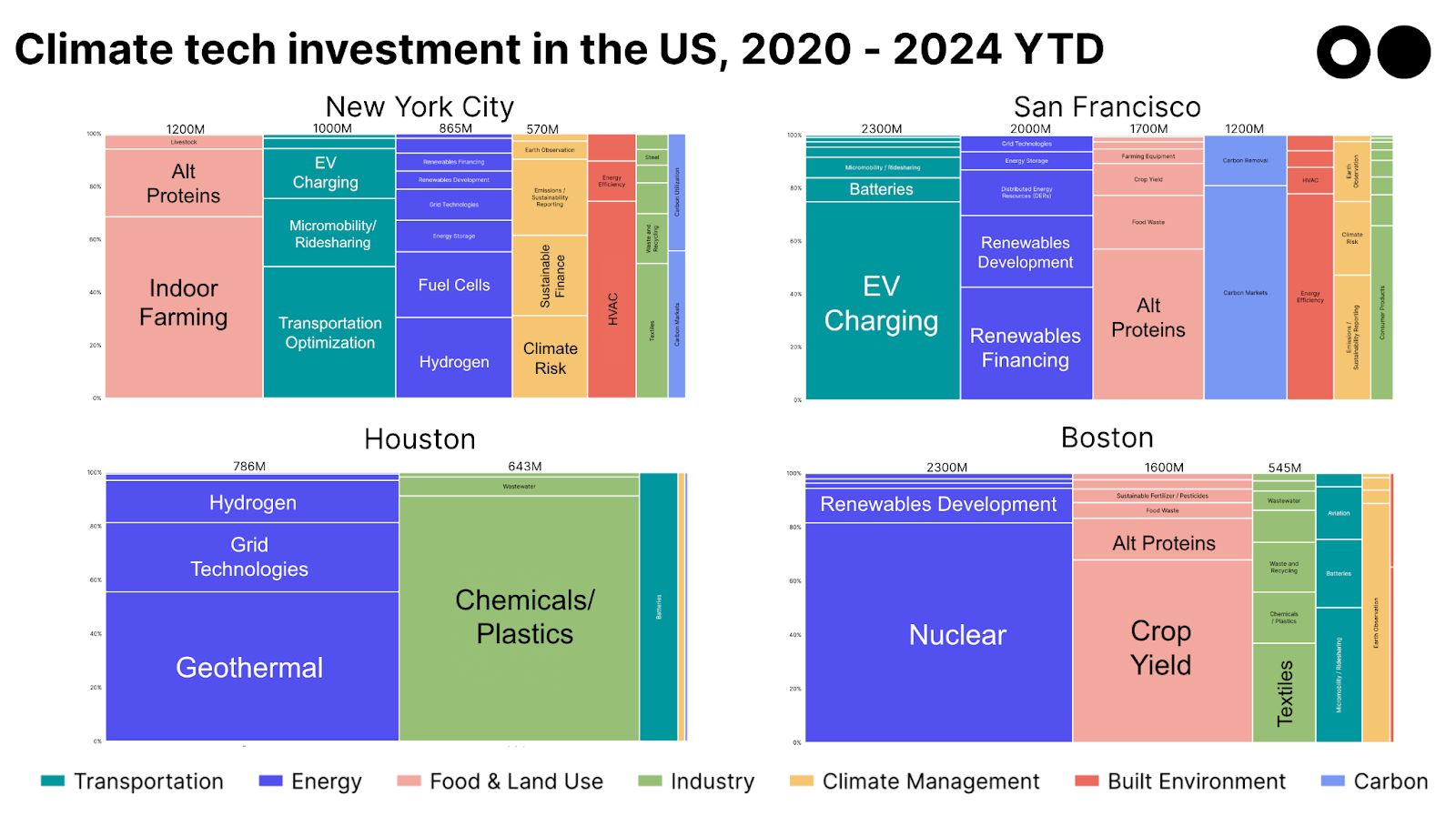

Zooming back into the U.S., trends even differ by city, reflecting different legacy industries, talent pools, corporate players, and local priorities.

Context: As CTVC’s co-founder and current NYC-based investor at Planeteer Capital, Sophie Purdom, said of the city’s climate tech landscape: "Second only to the Bay Area's level of climate activity, New York's climate company bench is deep and diverse. Unsurprisingly in a city where 70% of emissions come from buildings, NY climate startups skew towards built environment and resiliency solutions like climate risk, transportation optimization, indoor farming, and heating & cooling. Interestingly, NY founders mirror heavy fintech undertones, and prioritize creative ‘hardware-enabled software’ business models. In comparison to the Bay Area's heavy breakthrough hardware skew, NY climate companies lean immediately commercial, with deep corporate and local government partnership."

Context: San Francisco has long been recognized as a bastion for not only tech, but specifically climate tech. Within the US, the city has (predictably) drawn the largest pool of funding and been home to the highest number of deals. Investments in batteries and EV charging infrastructure lead the way in San Francisco, likely due to several factors, such as California’s regulatory pushes for electric vehicles and clean energy, and the “Tesla effect.” The success of Tesla, based in the broader Bay Area, has provided a North Star for the abundant startups and investors in the region, as well as funneled talent (Tesla mafia anyone?) into the climate tech startup ecosystem.

Context: In the US’s oil and gas capital, geothermal and chemicals/plastics are the most funded sectors, as expected. The skills, technology, and infrastructure from the oil and gas industry are highly transferable to projects with a subsurface component, like geothermal or CCUS, which can help reduce costs and risks. Houston is also a hub for the chemical and plastics industries, leveraging access to raw materials, established infrastructure, and potential partnerships with incumbents. Additionally, the capital stack in the region lends itself well to these types of startups; some of the most active local investors include Evok Innovations and Shell Ventures (Shell’s venture arm).

Context: Boston, with its strong academic and research institutions, directs significant investment towards deeptech, including nuclear fusion plays, such as the Boston-based Commonwealth Fusion Systems, which spun out of MIT.

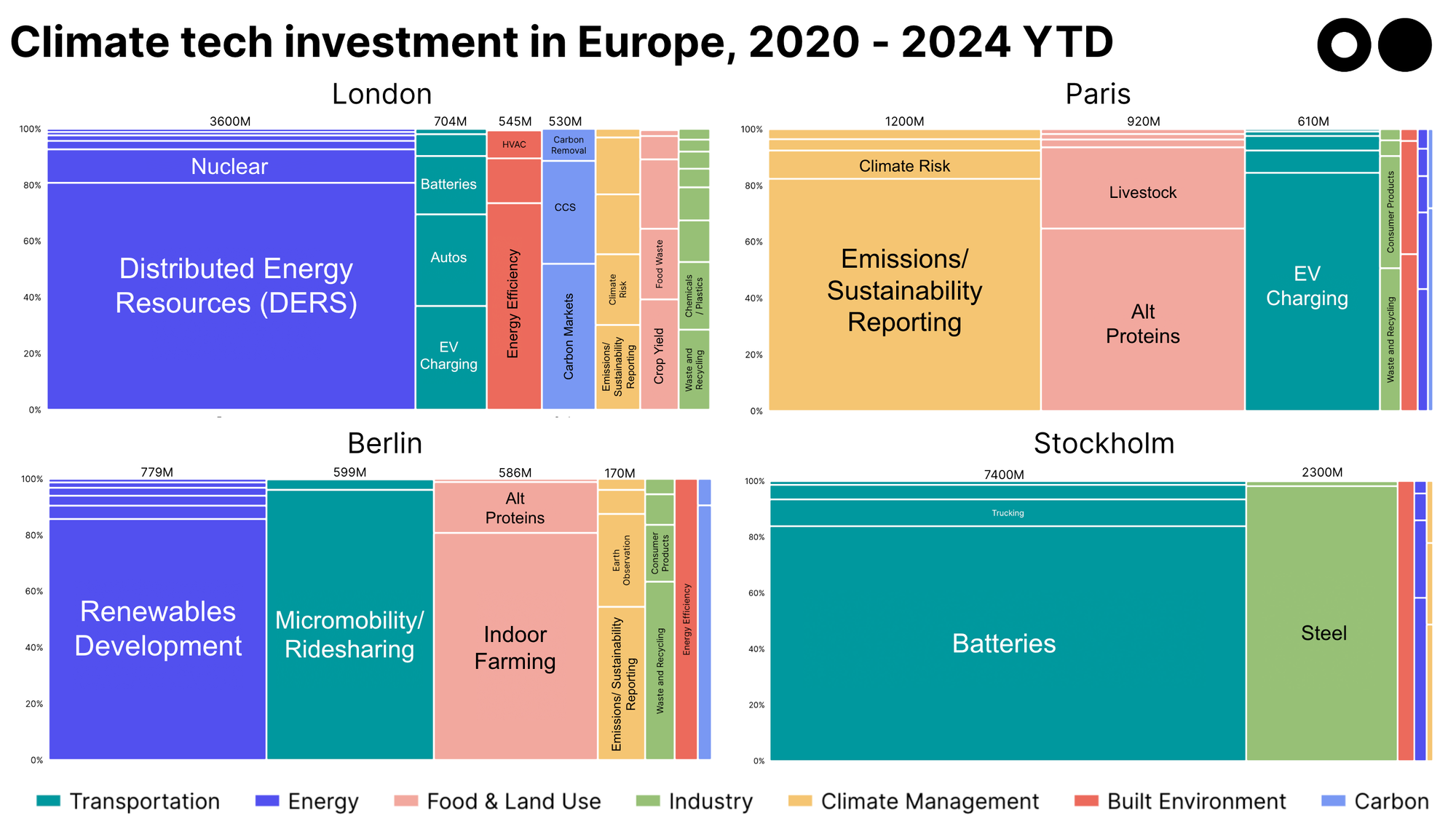

In Europe, each country's climate tech mix is shaped by a combination of regulatory support, market demand, and active investment communities.

Context: London has emerged as a significant global climate tech hub, partly due to its active investment community, abundant government grants, and supportive policies, according to George Chalmers, VC at Molten Ventures. Stafford Lloyd from UKRI’s Innovate UK highlighted how policy shifts towards renewables, such as contracts for offshore wind, and a national law requiring the phase-out of new fossil fuel vehicles by 2035, contribute to the dominance of energy and transportation. "Energy and transportation are more well-known by investors – there’s more knowledge, strong track records, and proven market traction," he added. “Meanwhile, the built environment is also a growing focus: “Historically, the (almost) implementation of laws like the Zero Carbon Homes Target means there’s a rich innovation environment in this sector,” he noted.

Context: France’s stringent regulations on corporate sustainability reporting and environmental impact assessments, drive demand for sustainability reporting services that help companies comply with these regulations.

Context: Berlin is characterized by strong government support and a well-established ecosystem of accelerators and incubators, such as ClimateX, Impact Hub, and EIT Climate-KIC Germany. Legislation, such as the German Act on Immediate Measures for an Accelerated Development of Renewable Energy and Further Measures in the Electricity Sector, sets ambitious targets for Germany to achieve climate neutrality and provides a supportive environment for renewable energy investments.

Context: Stockholm’s strong focus on energy-intensive sectors like batteries and steel, are enabled by “access to solid infrastructure and an abundance of green energy,” said Sandra Malmberg, partner at EQT Ventures. “More than 60% of Sweden's energy mix is renewable.” Agate Freimane, general partner at Norrsken VC, added: “A lot can be attributed to the success of Northvolt, Europe's largest green battery manufacturer. Northvolt's achievements have not only put Sweden on the map as a leader in sustainable energy, but have also paved the way for more electrification startups. Sweden’s vibrant VC ecosystem supports with the necessary capital to grow and scale, while the supportive angel investor community, influenced by the success of local unicorns like Spotify, Klarna, iZettle, and King, offers valuable mentorship and connections. Additionally, Sweden's government plays an active role in fostering innovation through grants, subsidies, and incentives. Programs from Vinnova, the Swedish Energy Agency, and Innovationsbron provide startups with financial support and resources, particularly in sectors aligned with national priorities like sustainability.”

A quick note on methodology: We calculated active investors based on the number of deals, and top companies by total funding, in the region since 2020, when we first began tracking.