🌎 What the dire straits in Hormuz mean for new energy flows #287

Who wins and loses as clean fuels and electrons gain ground

Fervo banks $421m in biggest project finance deal for sector

Good morning from Houston!

We’re in town all week for CERAWeek. Come find us - Kim, our lead carbon analyst Dr. Paola Sáenz, and other members of the team - if you're around. Plus, stay tuned for key themes and our takes here in your inbox, in our new power newsletter, and on LinkedIn.

In this edition: we’re digging deep into advanced geothermal, as Fervo’s new non-recourse debt deal just set the bar for bankability.

In deals, $1.93bn for solar plus energy storage across three deals, $1.9bn for data centers across two deals, and $512m for battery storage.

In other news, ripple effects from the Iran war, Google’s big week, and the US’ first new coal plant in over a decade.

One more thing: Sightline Climate is hosting a webinar on April 2nd on China Robotics & Physical AI. Sign up now to save your spot.

Thanks for reading!

Not a subscriber yet?

📩 Submit deals and announcements for the newsletter at [email protected].

💼 Find or share roles on our job board here.

CTVC is powered by Sightline Climate, the tactical market intelligence platform for energy and investment decision-makers.

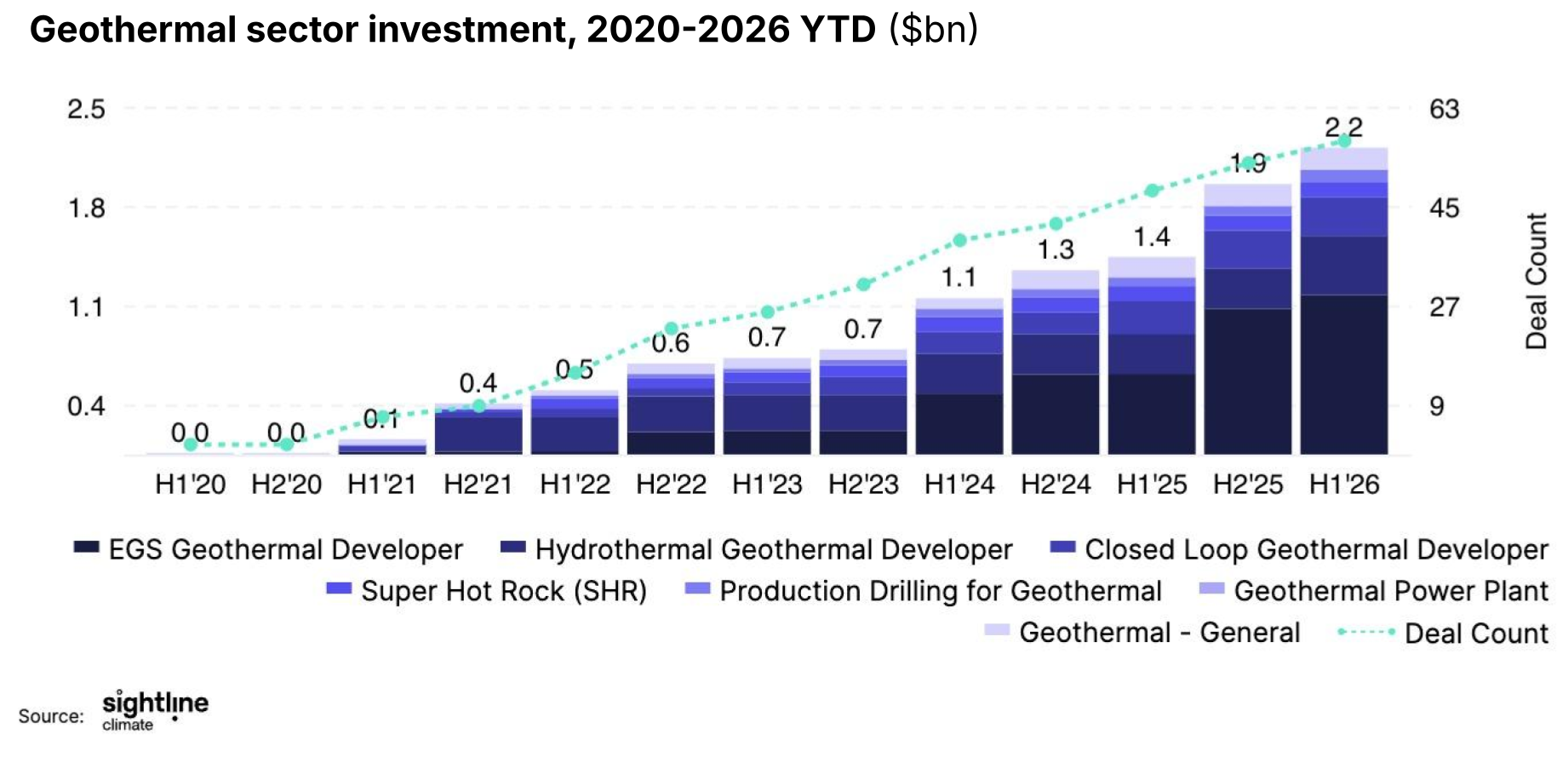

Last week, Fervo Energy closed $421m in non-recourse debt financing for Cape Station, its flagship enhanced geothermal systems (EGS) project in Utah. Apart from the commissioning of Cape Station, this might be the sector’s biggest signal yet: the first time a next-generation geothermal project has cleared the bankability bar.

Most of us probably know this by now, but just in case, Fervo’s innovation was to use horizontal drilling and controlled stimulation techniques borrowed from oil and gas, to create engineered reservoirs that maintain high flow rates without losing injected brines into the subsurface. That's what makes EGS different from conventional geothermal: it doesn't need a naturally occurring hydrothermal resource (i.e. brine already in place), which dramatically expands where it can be used. Beyond the innovations, Fervo’s superpower is continuous execution, from snapping up land leases for cheap, to setting standard after standard for drilling rates, to signing offtake agreements with utilities and hyperscalers.

Now, it’s all paying off (literally): Non-recourse debt financing is the gold standard of infrastructure capital, and a who's-who of global project finance backed this deal. The deal was oversubscribed, with RBC, Barclays, BBVA, HSBC, MUFG, Société Générale, JPMorgan, Bank of America, and Sumitomo Mitsui all participating. They assessed the technology risk, the revenue stack, and the construction timeline and said, take our money.

This $421m package includes a $309m construction-to-term loan, a $61m tax credit bridge loan, and a $51m letter of credit facility, funding the remaining construction of Phase 1. Output is fully contracted through PPAs with Southern California Edison, Shell Energy, and community choice aggregators, with plans to scale from 100MW to 500MW at the site.

We’ve been watching geothermal closely since 2007 – we’d written off EGS, but Fervo changed things. Back in 2023, we were in a client meeting, giving a presentation on what’s going on with all forms of next-gen geothermal. At the end, the client said ‘I’ve just gotta know – which one do you think will win?!’ And we said ‘listen, we’re in a situation now where we’ll look back years down the road and Tim [and Jack] will be known as ‘the father of.’

Too early to fully call it, but so far the statement seems to be directionally correct.

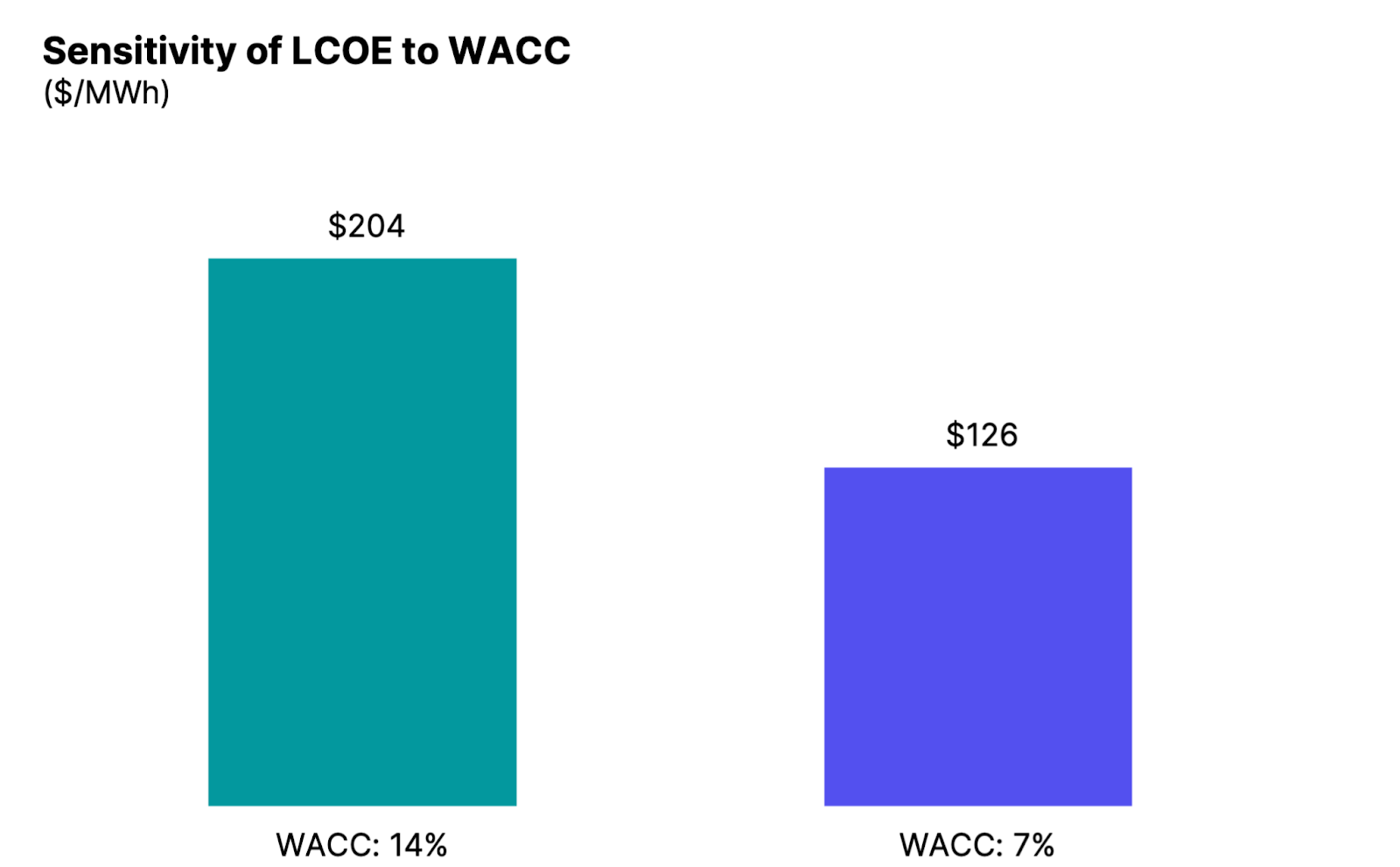

EGS is emerging as arguably the best shot hyperscalers and utilities have at building scalable clean firm generation to meet surging data center demand this decade. There’s lots of nuclear hype and hope, sure, but it’s still a decade away. Next-gen geothermal, if (or when) it technically works, checks every box: firm, clean, small footprint. And access to project finance fundamentally changes the economics.

Financing drilling and surface infrastructure through project debt rather than corporate equity or venture capital can reduce the weighted average cost of capital by as much as 50%, that in turn can significantly reduce LCOE, making once unaffordable projects viable.

Investor interest may also partly reflect limited opportunities elsewhere. Just as developers in oil & gas and renewables are searching for the next growth sector, lenders are doing the same, and clean firm power obviously benefits from the data center boom. With relatively few geothermal companies currently active, and so much development in other sectors going to private credit, several institutional investors are willing to take on greater risk to establish relationships early and position themselves as preferred lenders as the sector scales.

For instance, last week, Ormat Technologies also priced an upsized $875m convertible senior notes offering. It was up from the $750m originally announced, driven by strong demand. The notes carry an initial conversion price of ~$140.40 per share, representing a 30% premium to the company’s share price. As the sector's incumbent, the only vertically integrated geothermal company at scale, it's been signaling its own move into EGS through pilots with SLB.

⚡ Utility Global, a Houston, TX-based global economic industrial decarbonization platform, raised $100m in Series D funding from Ara Partners and APG Asset Management.

💩 Solugen, a Quebec, Canada-based liquid ammoniacal nitrogen fertilizer producer, raised $50m in Growth funding from Idealist Capital, and Canada Growth Fund (CGF).

🚤 Arc Boats, a Los Angeles, CA-based electric tugboat manufacturer, raised $50m in Series C funding from Eclipse, a16z, Menlo Ventures, Lowercarbon Capital, Necessary Ventures, and other investors.

⛴️ Candela, a Stockholm, Sweden-based electric ferry manufacturer, raised $35m in Series C from Beneteau, CalPERS, EQT Ventures, International Finance Corporation, SEB Private Equity, and other investors.

🍎 WayCool, a Chennai, India-based agri-tech and food supply chain solutions platform, raised $23m in Growth funding from Lightrock India.

⚡ GridBeyond, a Dublin, Ireland-based AI-based energy optimization platform, raised $14m in Series D funding from Samsung Ventures, ABB, Act Venture Capital, Alantra, EDP Ventures, and other investors.

♻️ WeSort.AI, a Würzburg, Germany-based AI-powered waste sorting service platform, raised $11m in Seed funding from Green Generation Fund, Infinity Recycling, SPRIND, and Vent.io.

🌌 Mantis Space, an Albuquerque, NM-based orbital power grid infrastructure developer, raised $10m in Seed funding from Rule 1 Ventures and Montauk Climate.

🌾 AgZen, a Somerville, MA-based AI-driven precision spraying technology developer, raised $10m in Series B funding from DCVC, Astanor Ventures, Material Impact and Syngenta Group Ventures.

🌾 Wikifarmer, an Athens, Greece-based digital platform for agri-food supply chains, raised $8m in Series A funding from Brighteye Ventures, Piraeus Bank, Metavallon VC and Point Nine Capital.

🛵 Euler Motors, a New Delhi, India-based electric commercial vehicle manufacturer, raised $8m in Series D funding from BlackSoil.

👕 Rubi Laboratories, a San Francisco, CA-based CO2-to-textiles technology developer, raised $8m in Seed funding from AP Ventures, FH One Investments, CMPC Ventures, H&M Group, Talis Capital, and Understorey Ventures.

🧪 Level Nine, a Berlin, Germany-based bio-nanotechnology catalysts developer for green chemicals, raised $5m in Seed funding from Visionaries Tomorrow, IBB Ventures, better ventures, Zero Carbon, and Rockstart.

💨 Sequestra, a Vienna, Austria-based CO2 sequestration technology developer, raised $4m in Seed funding from VSE Beteiligungs.

🧪 Elea & Lili, a Helsinki, Finland-based cellulose-based absorbent materials developer, raised $3m in Seed funding from Lifeline Ventures, Baltiska Handels Sverige AB, and Ikorni Invest.

🏠 AirTrunk, a Sydney, Australia-based hyperscale data center operator, raised $1.2bn in PF Debt funding from Crédit Agricole CIB, MUFG Bank, Société Générale, Sumitomo Mitsui Banking Corporation (SMBC), BNP Paribas, and other investors.

☀️ ENERPARC AG, a Hamburg, Germany-based large-scale solar power plant developer, raised $1.15bn in Debt funding from EIG Global Energy Partners (EIG), Eiffel Investment Group, Landesbank Baden-Württemberg, and Schroders Capital.

⚡ Primergy, an Oakland, CA-based renewable energy developer, raised $760m in PF Debt funding from BofA Securities, KeyBanc Capital Markets, MUFG Securities Americas, BNP Paribas and SMBC Nikko Securities America.

🏠 Digital Edge, a Singapore-based energy-efficient Asia-Pacific data center developer and operator, raised $665m in PF Debt funding from BNP Paribas, Sumitomo Mitsui Banking Corporation (SMBC), Mizuho Bank, DBS Bank, Crédit Agricole CIB, and other investors.

🔋 Hedley BESS LP, a Haldimand County, Canada-based battery energy storage facility, raised $512m in PF Debt funding from Canadian Imperial Bank of Commerce, Sumitomo Mitsui Banking Corporation, Desjardins Group, Industrial and Commercial Bank of China, National Bank of Canada, and other investors.

⚡ Fervo Energy, a Houston, TX-based geothermal project developer, raised $421m in PF Debt funding from MUFG Bank, HSBC, Société Générale, Banco Bilbao Vizcaya Argentaria, Barclays, and RBC Capital Markets, JPMorgan, and other investors.

🔋 Nouveau Monde Graphite, a Saint-Michel, Canada-based green graphite producer, raised $335m in PF Debt funding from Canada Infrastructure Bank and Export Development Canada (EDC).

☀️ Clenera, a Boise, ID-based utility-scale solar farm developer, raised $304m in PF Debt funding from HSBC, ING Capital, KeyBanc Capital Markets, and MUFG Bank.

☀️ Heritage Energy Storage, a Texas City, TX-based distributed solar and storage developer, raised $29m in Debt funding from Eagle Point Credit Management.

☀️ Smartsolar, a Ho Chi Minh City, Vietnam-based solar developer, raised $1m in Debt funding from SECO Startup Fund and SKR Reisen.

⚡ Viridi Energy, a New York, NY-based full-service RNG platform, raised an undisclosed amount in PF Equity funding from HASI.

🏠 American Intelligence & Power Corporation, a Houston, TX-based AI power infrastructure developer, was acquired by Nscale for an undisclosed amount.

🌬 Talveg Wind, an Issoire, France-based wind turbine maintenance services company, was acquired by Nadara for an undisclosed amount.

🏗 Teleo, a Palo Alto, CA-based supervised autonomy platform for heavy equipment, was acquired by Havoc for an undisclosed amount.

Partech Impact Fund, a Paris, France-based growth-stage impact venture capital firm focused on decarbonization, green mobility, and European B2B technology, completed a final close of $346m for its inaugural Article 9 impact fund targeting European B2B technology companies focused on decarbonization, green mobility, and health.

UVC Partners, a Munich, Germany-based multi-stage venture capital firm investing in European B2B DeepTech, ClimateTech, Mobility, and Software/AI companies, announced the first close of $89m towards a $173m growth extension fund, allowing UVC to participate in later-stage rounds while maintaining its early-stage investment strategy.

GVC Gaesco Resilient Infratech Ventures Fund, a Barcelona, Spain-based early-stage venture capital firm investing in European infratech startups across energy, industry, and digital infrastructure, launched a $81m fund targeting capital-intensive technology companies across energy storage, industrial electrification, automation, and data infrastructure in Europe.

Montis VC Fund, a Warsaw, Poland-based early-stage venture capital firm investing in European energy and industrial tech startups, completed a first close of $58m backed by the European Investment Fund (EIF) through the REPowerEU programme and the Polish Development Fund (PFR).

This is a sample of deals available for Sightline clients. Can’t get enough deals?

The US and Iran have been at war for about four weeks, and despite threats back and forth, the Strait of Hormuz remains closed. Oil prices swung wildly on Monday, with Brent crude dropping over 7%, after Trump posted about having "productive" conversations and pausing planned strikes on Iranian energy infrastructure for five days. The IEA says at least 44 energy assets across nine countries have been severely damaged, and the disruption extends beyond oil to natural gas, petrochemicals, fertilizers, and beyond.

Google had a big week, closing several clean energy and climate deals. It completed the $4.75bn acquisition of Intersect and the simultaneous spinout of IPX Power, the new independent power producer launching with 4.4GW of solar and 8.8GWh of storage. Separately, Google signed a deal with AMP to divert landfill waste and convert it into biochar, targeting removing 200,000 tons of CO₂e by 2030 while cutting landfill methane emissions. The moves highlight the new hyperscaler playbook of owning the developer itself.

Terra Energy Center is investing $1bn in a new coal power plant in Alaska, which would be the first new coal facility built in the US since 2013. The project represents a striking reversal for the US coal industry, which has been steadily declining as utilities shift to cheaper and cleaner energy sources, but the move is backed by the Trump administration's push to promote fossil fuels.

Advanced nuclear developer X-Energy filed for an IPO, looking to capitalize on growing investor interest in nuclear power. The company is developing over 11GW of new nuclear capacity in the US and UK, and has partnered with major players like Amazon and Talen Energy. The filing comes amid a broader nuclear renaissance driven by surging electricity demand from AI data centers and the Trump administration's goal to quadruple nuclear energy output by 2050, but going public means more disclosures and can bring risks.

Nearly half the US states are now suing the EPA over its repeal of the endangerment finding, the legal basis for essentially all federal carbon emissions limits. The 24-state coalition follows a similar suit from the NRDC and allied nonprofits, and the cases are expected to be consolidated and end up before the Supreme Court.

Uber is investing over $1.2bn in Rivian through 2031 and has agreed to purchase 10,000 to 50,000 autonomous R2 robotaxis, as Waymo pushes forward. The fleet would launch in San Francisco and Miami in 2028, scaling to 25 cities by 2031. Uber's CEO cited Rivian's vertical integration as the key draw.

Whisky meets hydrogen, cheers to low-carbon spirits.

Critical minerals get a circular economy boost.

Rising oil prices give EV demand a jolt.

A survival guide for stranded DOE funding.

The grid has more to give, if we unlock it.

JPM’s 16th annual energy paper is out now: Big finance weighs in on a turbulent world.

Form Energy’s iron-air batteries land in Europe.

Polluters named as methane detection scales up.

Massachusetts clean energy game plan: Faster permits, fewer bottlenecks.

Corporate carbon offsets grow 181% as AI race sets off emissions.

A 64% increase in Mexico’s monarch butterfly population shows numbers migrating in the right direction.

💡Carbon13 Venture Accelerator: Apply by March 27 to be considered for an accelerator that supports and invests in founders building solutions to the climate emergency. The program has personalized support and the opportunity to pitch for investment ranging from €150,000– €250,000.

💡The Clean Fight Energy Storage Venture Accelerator: Join The Clean Fight’s accelerator program focused on increasing the pace of energy storage deployment in New York State over the next 18 months. Apply by March 30. one-on-one

📅 China Robotics & Physical AI: Join Sightline Climate and the Asia Climate Tech Initiative on April 2 at 01:30 PM for an invite-only webinar featuring new research from Sightline’s upcoming China Robotics & Embodied Intelligence report and live presentations from Chinese companies, including ANU, InsightOS, and Aoyi.

📅 ClimateTech Connect: In National Harbor, MD, on April 8-9, be a part of the first dedicated conference on climate risk and resilience for the re/insurance, financial services, real estate, and public sectors. Join thought leaders, tech innovators, and industry experts to advance climate adaptation and resilience strategies at scale.

💡EarthScale: Apply by April 13 to join the second cohort of EarthScale’s UK-based 12-month program supporting climate tech ventures. Get support with navigating manufacturing and raising Series A funding. The program brings together a powerhouse network of regional hubs, building an ecosystem for scaling the UK’s most promising climate tech ventures.

📅 Planeteer @ SF Climate Week: Kick off San Francisco Climate Week on April 20 from 6:50-8:00 am with Planeteer Capital for a 5k fun run at Joyride Pizza, Pier 1. To keep it going, join our co-founder and managing director of Planeteer Capital, Sophie Purdom, and many others for two events on April 22: the Female Founders & Funders Gathering from 2:00-4:30 pm PDT and the Cost of Compute dinner at 7-9 pm.

Software / Machine Controls, @Dig Energy

Growth Associate, @Coral

Investment Associate, @Energy Impact Partners

XIG Imprint Business Development Lead - Vice President @Goldman Sachs

Junior Account Executive, @3V Infrastructure

Summer Research Intern, Senior Associate – Clean Fuels, Principal Analyst – Data Centers and Power Markets, Data Analyst – Late-Stage Finance, @Sightline Climate

Associate, @Prelude Ventures

📩 Feel free to send us deals, announcements, or anything else at [email protected]. Have a great week ahead!

Who wins and loses as clean fuels and electrons gain ground

A breakdown of China’s new FYP and what it means for the next decade of the energy transition

Beijing lowers growth targets while doubling down on AI, energy, and advanced industry

Newsletter

Newsletter