🌏 Spinning CO2 into clothes

Scaling “symbiotic manufacturing” with Rubi Laboratories

Wrangling the wild west of the voluntary carbon offset market

Fusion energy. Electric airplanes. Fertilizer from air. The world of climate tech overflows with mind-bending technologies. But perhaps the most mind-bending of all? The voluntary carbon market.

The scientific consensus that we need to drain the bathtub (in addition to turning off the tap) couldn’t be clearer. Nearly every legitimate corporation has pledged to be Net Zero, but won’t get there through emission reductions alone. Funding rounds and job postings alike for “CDR” startups are white-hot with VCs and candidates tripping over themselves to be a part of carbon drawdown. Yet, fundamental open questions around definitions, regulation, and verification make any hard predictions about the voluntary carbon market a fool's errand.

But where there’s uncertainty, there’s upside.

And the trappings of a good deep dive ;) Readers beware: this one runs longer than usual, so it might be a good post bookmark and keep coming back to. Readers beware again: this one includes more editorial predictions than usual. We’ve spent the past 3 months huddling up with founders, consultants, policy makers, and investors operating at the cutting edge of this market trying to capture a perfect snapshot, but it keeps blurring - the market is moving too quickly. Undoubtedly you’ll find things to disagree with and bits that we omitted in the below. In the spirit of speedily but steadily bringing this new carbon market online together, call us out to update this picture!

If we closed the faucet on global GHG emissions tomorrow, we’d still need to drain the tub and remove CO2e from the atmosphere to avoid catastrophic global warming. Since 1850, we’ve filled the proverbial atmospheric tub with 2,500,000,000,000 tons of CO2 – half just from the last 30 years - and we continue to dump in 50bn tons of CO2e per year. For most 1.5ºC pathways, even with drastic decarbonization (e.g., electrify everything, H2, etc.), we will still need to remove 6-10 Gt of CO2 per year by 2050. If you don’t happen to think in Gt CO2 units, that’s equal to stopping GHGs and removing ~10-20% of global emissions annually. Accordingly, mitigation is on the mind.

This article focuses exclusively on the voluntary carbon market. You might be curious about the inverse - an involuntary carbon market, you say? The compliance or regulated carbon markets exist in response to laws (California, EU, Quebec) requiring emission reductions, managed through emission trading systems. These cap and trade systems dwarf the size of the voluntary markets and are rife with their own set of peculiarities, though tend to be more stable and, well, regulated. Now, forget all about the compliance market for the rest of this article.

The voluntary carbon “market” (VCM) has been around for as long as do-gooders have opted to purchase additional emission reduction credits. In response to recent corporate net zero commitments, voluntary carbon market activity has spiked. Governments and corporates accounting for >$14 trillion in sales are now under net zero targets. To net their emissions out to zero, entities will take a series of operational decarbonization actions - largely the rest of what we write about in CTVC. At a certain point (so the math goes), the cost of the next marginal unit of emissions abatement breaks even with the price of buying a carbon credit equivalent to doing the hard work internally of reducing emissions. Mitigation is the bulk of the work, but credits are the backstop to fill the gap.

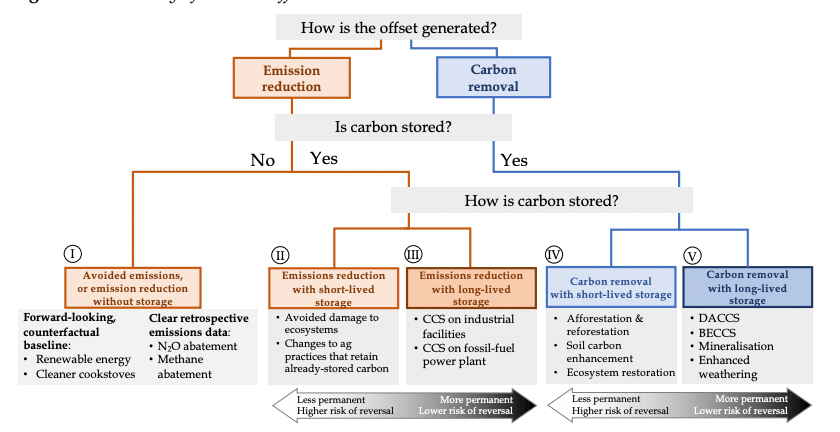

Confusingly, not all “carbon offsets” are created equal. There are two fundamental types: emission reductions and carbon removals. Simply put, traditional offsets result in emitted carbon staying in the system. Carbon removals actually take carbon out from the system.

Thus, this unravels the multifold problems with carbon offsets.

Additionality: Would that carbon be offset if the credit wasn’t generated?

If an offset is issued from a forest preserve protected in perpetuity, that offset is not “additional.”

Leakage: What is the risk of displacing activities that cause greenhouse gas emissions from the project site to another site?

If an offset is meant to protect a patch of the Amazon from deforestation from soy cultivation, but a separate patch of the Amazon is cut down for soy instead, then that offset resulted in “leakage.”

Verification: Can the offset be verified through a registry and science-based methodology?

New methodologies for removals (e.g., sinking carbon-dense kelp to the ocean floor, etc.) can be difficult and time consuming to verify, delaying actual removals.

Permanence: What is the risk of stored carbon being re-released into the atmosphere?

How do you account for the flux in durability of storage either through voluntary (intentional) or involuntary (extreme weather, exogenous biotic or abiotic factors) reversal events?

With corporates racing to get to net zero, the easiest path forward so far has been through the VCM. Carbon offsets have historically centered on avoided emissions rather than removed emissions and cost as low as $3-5/ tCO2. Despite the question marks around carbon offsets, a ton of avoidance and a ton of removal have thus far been treated equal in the corporate net zero ledger. Pricing per ton incentivizes companies to buy the lower-quality avoidance offsets.

To frame this in real world terms, Amazon’s carbon footprint in 2020 was 60M metric tons of CO2. Assuming no decarbonization activity, if they spent $3/ tCO2, they would have only needed to spend $180M to offset their Scope 1-3 emissions – a 0.05% drop in the bucket compared to their $386B in revenue. The carbon offsets market as it stands today provides an ‘out’ for corporates to falsely claim Net Zero while paying pennies on the dollar.

“The reason most people buy offsets is to compensate for tons of CO2 emitted in their internal processes. Because those fossil emissions will have a permanent impact on climate, and companies sometimes buy impermanent offsets purely based on price, that trade is quite bad for the environment and the net carbon arithmetic doesn’t tie,” notes Jonathan Goldberg, CEO of Carbon Direct.

As buyers grapple with the multifold problems of the VCM (above), corporates have started to demand quality. With some leading buyers willing to pay a premium, the carbon market is gradually bifurcating between legacy emissions reductions and the evolving supply of carbon removals. But removals don’t come cheap today, with engineered carbon removal at $500+ per ton, and nature-based removal running at $20+ per ton.

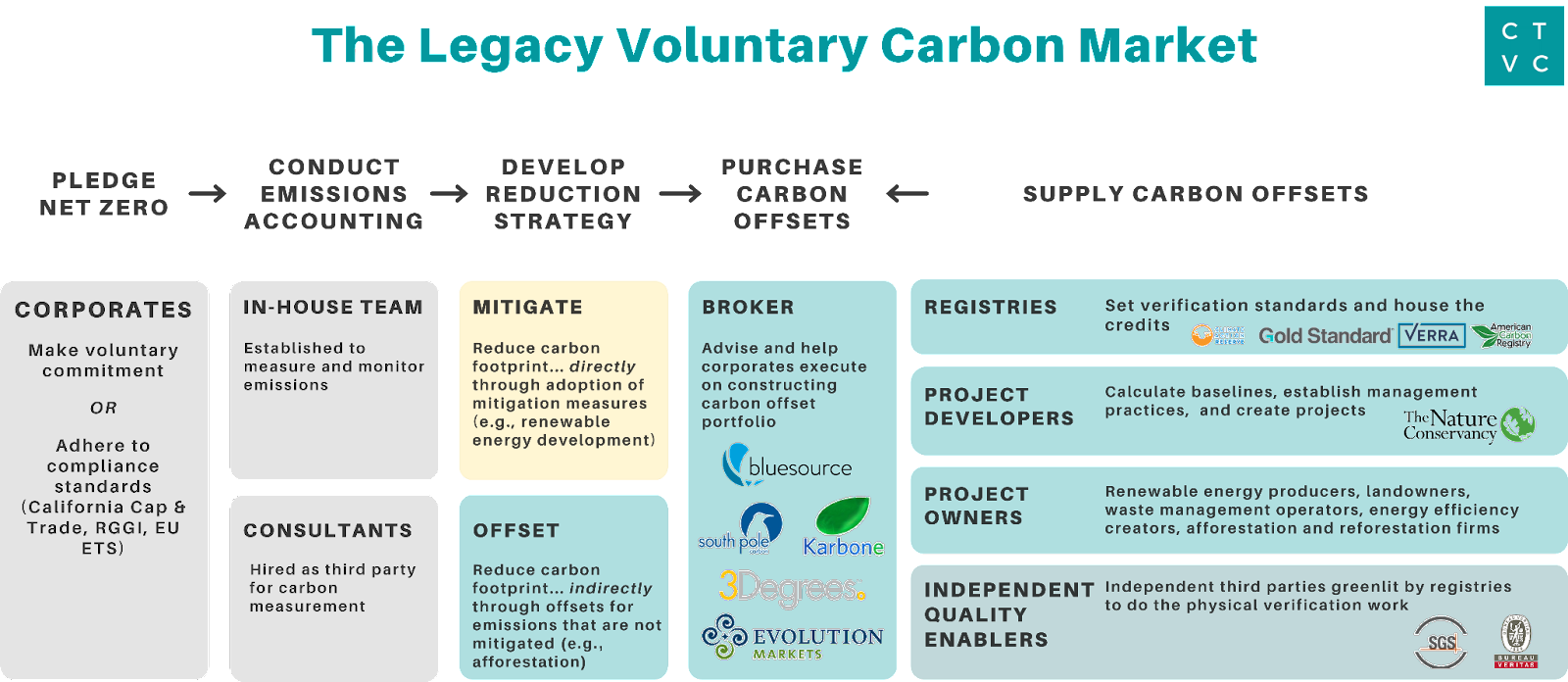

In the legacy market, a corporate with net zero commitments can set their carbon budget for offsetting, work with middlemen to find offsets at the cheapest price, and wipe their hands clean to continue operating as usual and pumping out emissions.

Pledge net zero and conduct emissions accounting. The first step after any feel-good corporate net zero announcement is to actually understand their emissions footprint. It’s extremely heterogeneous and challenging work, especially when relying on off the shelf emissions factors which can vary a carbon footprint by many multitudes.

Purchase carbon offsets. Once corporates have completed the hard work of measurement and mitigation, the carbon offsets market can plug the remaining gap. Brokers advise and help corporates construct carbon offset portfolios - think of them as carbon asset managers who help corporates purchase OTC carbon credits. Corporates give their target amount and price point, so brokers can hunt down credits from project developers. Given these budgetary dynamics, brokers must prioritize offsetting emissions at the right cost over legitimate quality.

Examples: 3 Degrees, South Pole, Bluesource, Karbone, Evolution Markets, Natural Capital Partners

Supply carbon offsets. On the other side of the market, the Registries act as the gatekeepers for certified credits. They’re typically nonprofit orgs that oversee the registration and verification of carbon offset projects. Certified projects have to go through the hoops of meeting the registry’s methodology including a manual validation/ verification process (think people on the ground wrapping measuring tapes around trees). Only then are the credits eligible to be listed and traded on the registry’s marketplace.

Examples: American Carbon Registry, Verra, Gold Standard, CAR

Where there are credits and projects, there are developers. Project developers work with landowners to assess projects, bring in investors, and develop/sell the credits generated. The two broad types of carbon offsets are renewable energy projects and land use projects (e.g., improved forest management). Developers get to take a hefty 20-40% cut since they have the inside scoop in what’s otherwise a very opaque market. Similar to the renewables world, developers will build a 20 tab excel model to project cash flows - but instead of electrons they estimate carbon. Since the math is hard to check, there’s wiggle room and loopholes for developers to exaggerate assumptions for optimal carbon credit generation (for example, a higher growth rate factor makes the avoided emissions pie much bigger).

Given the flaws in the legacy market, corporates are seeking quality from their stakeholders and numerous innovators have heeded the call to create new carbon management, removal, marketplace, and verification tools. A few forces at work are driving the evolution of this new carbon market:`

Accessibility: new tech-enabled entrants with the ability to span farther down the value chain (e.g., platforms acting as both ratings agencies and verifiers)

Technology: technology developers developing removals rather than project owners, ‘upping’ the tech level across the chain (e.g., permanent direct air capture and sequestration)

Transparency: better tools and methodologies enabling clarity and quality in the market (e.g., Stripe and Microsoft open sourcing removal RFPs and publishing through Carbonplan )

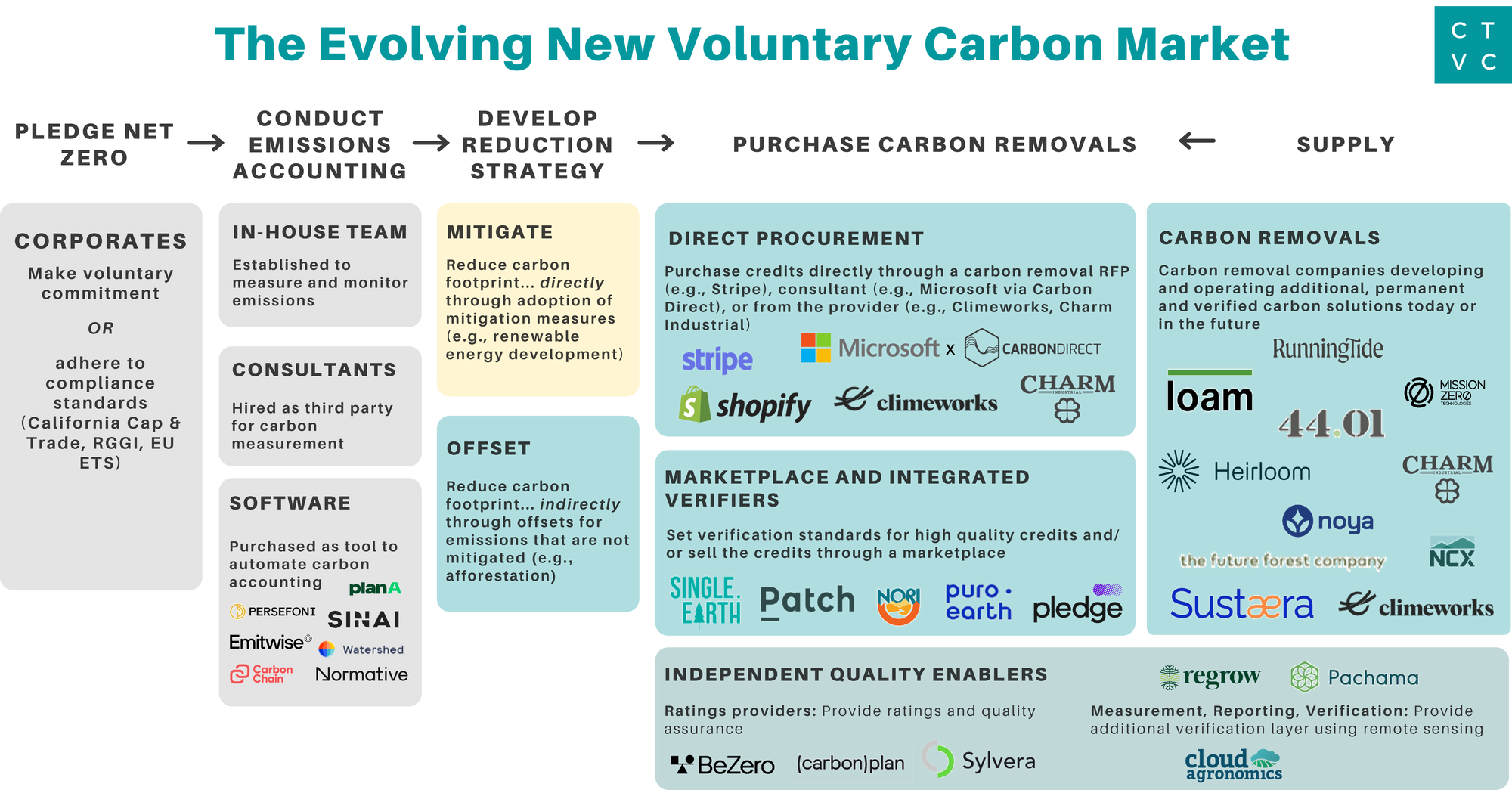

Pledge net zero and conduct emissions accounting. A new ecosystem of carbon accounting software has sprung up overnight to automate what was once the job of consultants with spreadsheets. After the data is served, platforms like Watershed have started to slip downstream by developing an in-house carbon removal marketplace directly integrating removals purchasing into the carbon accounting flow.

Purchase carbon removals - Direct Procurement

In typical SaaS D2C nature, new tech entrants are enabling corporates to directly procure carbon credits sans brokers and middlemen. Unlike the legacy market of carbon offsets with vintages or emissions reductions generated in the same year that the credits were issued, carbon removals are often sold as “future vintages”. Many of Stripe and Microsoft’s purchases are commitments to supporting projects removing carbon in the future. Think of it like a removals version of a renewables PPA - or CPA (Carbon Purchasing Agreement) - where the offtaker signs a long-term contract to purchase carbon removal directly from the generator.

Stripe sparked the carbon removal conversation when they kicked off their RFP for carbon removal credits and set their willingness to pay at >$1000/ tCO2 to accelerate these technologies down the cost curve. Instead of working backwards from a carbon budget to match the lowest cost offset portfolio, Stripe committed $1M (independent of tonnage volume) to prioritize actual removal of emissions. Their first purchases included Climeworks, Project Vesta, Charm Industrial and Carbon Cure ranging from $75-$750 per ton of carbon removed. Since then, over 10,000 of Stripe’s own customers now contribute to purchase carbon removal through Stripe Climate. Stripe and its customers have now contributed a total of $15m across 14 carbon removal projects: with a batch of purchases in Spring 2021 followed by one in Fall 2021.

Microsoft holds the most ambitious climate pledge, committing to be “carbon negative” by 2030. To do that, Microsoft contracted Carbon Direct for advice on high quality carbon removal projects, open sourced their criteria so other interested parties could follow on and replicate, and purchased the removal of 1.3m metric tons of carbon from 26 projects. Many more, like Shopify and Swiss Re, are catching on and prioritizing quality over quantity to seek out the best carbon credits.

On the supply side, technology providers like Climeworks and Charm Industrial are also starting to offer direct purchasing options, but given the low volume and high price tag, only individuals and corporates with deep pockets can afford it. To remove the equivalent of 1 person’s emissions, plan to shell out $1175/ month for Charm or $2176/ month for Climeworks.

Purchase carbon removals - Marketplace and Integrated Verifiers

Since registries like Verra don’t certify carbon removal projects, new overlapping entrants in this wild west have emerged to take their place. CarbonPlan and Carbon Direct operate as third party orgs with no direct skin in the game ensuring better quality carbon projects through data and scientists. Meanwhile companies like Patch and Pledge are creating marketplaces and bundling services to supply high quality removal credits to a wide pool of buyers. Others are vertically integrating further to combine marketplaces with verification and ratings, including Puro Earth and offset rating agencies like Sylvera and Be Zero. Pure-play MRV startups are also leveraging new remote sensing technologies to drive cheaper, more accurate measurement, reporting, and verification at scale.

New players in Web3 have driven a renaissance in the voluntary carbon market, including Toucan, Flow Carbon, and Single.Earth. [Look out for a feature soon on climate x web3]. These groups help with market transparency and liquidity but do not necessarily improve offset quality.

Ultimately, these tech-enabled entrants point to the remaining open question of who fills Verra’s verification shoes for the carbon removal market. We’re still in the early innings of understanding for mechanical and nature-based removal processes like DAC, biochar, soil carbon, ocean CDR, etc. so the jury is still out on whether a standardized methodology can even be applied.

Verifiers are incentivized for quantity, not quality. Incentives matter. Today, verifiers get paid only when they bring new credit volume into the market. They’re disincentivized to keep low quality stock out of trading. A quality-aligned alternative would see verifiers compensated for action (evaluating submissions) rather than outcomes (approving new credits).

Counterfactuals don’t exist, so avoided emissions are fatally flawed. Fundamentally, in order to believe in traditional offsets, one must buy into the validity and verifiability of a counterfactual. Let’s take an example: you own some trees containing 1 ton of carbon. I want to buy 1 ton of offsets so I can pollute 1 ton of carbon elsewhere. You sell me 1 ton of emission reduction traditional offsets, backed on the promise that not only you’ll protect the trees but that if I didn’t pay you, you would cut down the trees. The counterfactual backs the offset, but of course counterfactuals are hard to prove. What happens if you’re The Nature Conservancy with a stated mission of protecting forests? Could you prove that you’d clearcut without my cash? What if I bought the rights to a new geological formation filled with methane and threatened to drill a hole down to the gas and release it? Who pays me to not drill the hole?

The voluntary carbon market only exists because of corporate Net Zero pledges. Unlike compliance carbon markets, which are driven by government-regulated cap and trade systems, voluntary carbon markets have no other price or quantity driver beyond corporate’s Net Zero pledges. Compliance systems control the total number of credits in circulation; voluntary systems have no control over the total number of credits.

The definition of Net Zero is still being written. In the absence of regulatory language to define the dos and don’ts of Net Zero, every company has taken pen to paper and written their own strategy – leading to variability in definition and approach.

1 ton of carbon emitted yesterday isn’t the same as 1 ton of carbon captured today. Climate damage occurs immediately. However, the time-cost of additional atmospheric carbon is not accounted for. We need to prorate emissions.

Value likely accrues to those who vertically integrate. Anticipate startups with business models doing everything from originating projects from landowners to selling packages of offsets directly to corporates. If they can defend a specific offset thematic niche (e.g. forestry, soil carbon, etc.) through performing high-quality verification or accounting, startups can circumvent intermediates from taking a cut of revenue.

Corporates buy offsets based on two criteria: price or story. After assessing their current carbon footprint, corporates either approach their offset purchasing with a financial imperative (to spend as little per credit but purchase the full volume of carbon offsets) or marketing imperative (to buy the credits with the strongest aligned secondary messaging e.g. biodiversity, jobs, significant region). Stripe is a rare outlier that separated total spend from volume of offset purchases, in order to purchase credits (often as the first customer) from CDR technology companies with scaling potential.

Carbon removals make for cheap recruitment marketing and retention. Employees want to align their work and values. By going carbon neutral, and telling a compelling story along the way, corporates can attract and retain climate-concerned employees. In a market constrained more by human capital than dolla dolla bills, 0.06% of revenue is a strong ROI (math: Microsoft’s $1b carbon removal fund, annualized, is $100m per year compared to $168b FY’21 revenue).

This piece wouldn’t exist without our tireless co-authors Clea Kolster from Lowercarbon Capital and CTVC’s own Kobi Weinberg from Nephila Climate. Huge thanks to Jonathan Goldberg from Carbon Direct, Julia Reichelstein from Piva Capital, Keeton Ross from Patch, Ryan Orbuch from Lowercarbon, and Nan Ransohoff from Stripe, and numerous founders for contributing their wisdom about the carbon craze.

Scaling “symbiotic manufacturing” with Rubi Laboratories

How to build trust and collaboration in CDR with Isometric, starting with the science

Exxon’s acquisition of Denbury fuels CO2 transport ambitions

Newsletter

Newsletter