🌎 The UK digs deep for critical minerals #285

England strikes lithium and comes up with geothermal gold

A new weekly briefing on the moves and motives shaping power markets

Happy Thursday!

We launched CTVC in March 2020, six years ago (!) this month. At the time, we wanted to understand the fast-moving, wide-ranging, much-hyped climate tech theme. Since then, each week we’ve brought you breakdowns of new sectors, big innovations, and shifting policies.

But one story has become louder than the others: the power sector.

There’s simply too much happening in power to contain it in CTVC alone – it needed its own title. We once coined the term Climate Capital Stack to describe the layers of capital needed to get new technologies to market. Power has its own multi-layered stack to ensure reliability and meet demand – and each layer is fast-growing and fast-changing.

Today, we’re launching Powerstack.

Powerstack is Sightline Climate's new weekly newsletter on the moves and motives shaping the load growth era. Every Thursday, we distill 10,000+ signals into a clear view of what's changing and what it means. Each edition will include:

Powerstack is Sightline Climate putting a stake in the ground. The power system is where the trillion-dollar buildout decisions will be made over the next decade, and that's where we're going deepest.

This is a preview of Powerstack. If you like it and want to get more like this every Thursday, you can sign up here.

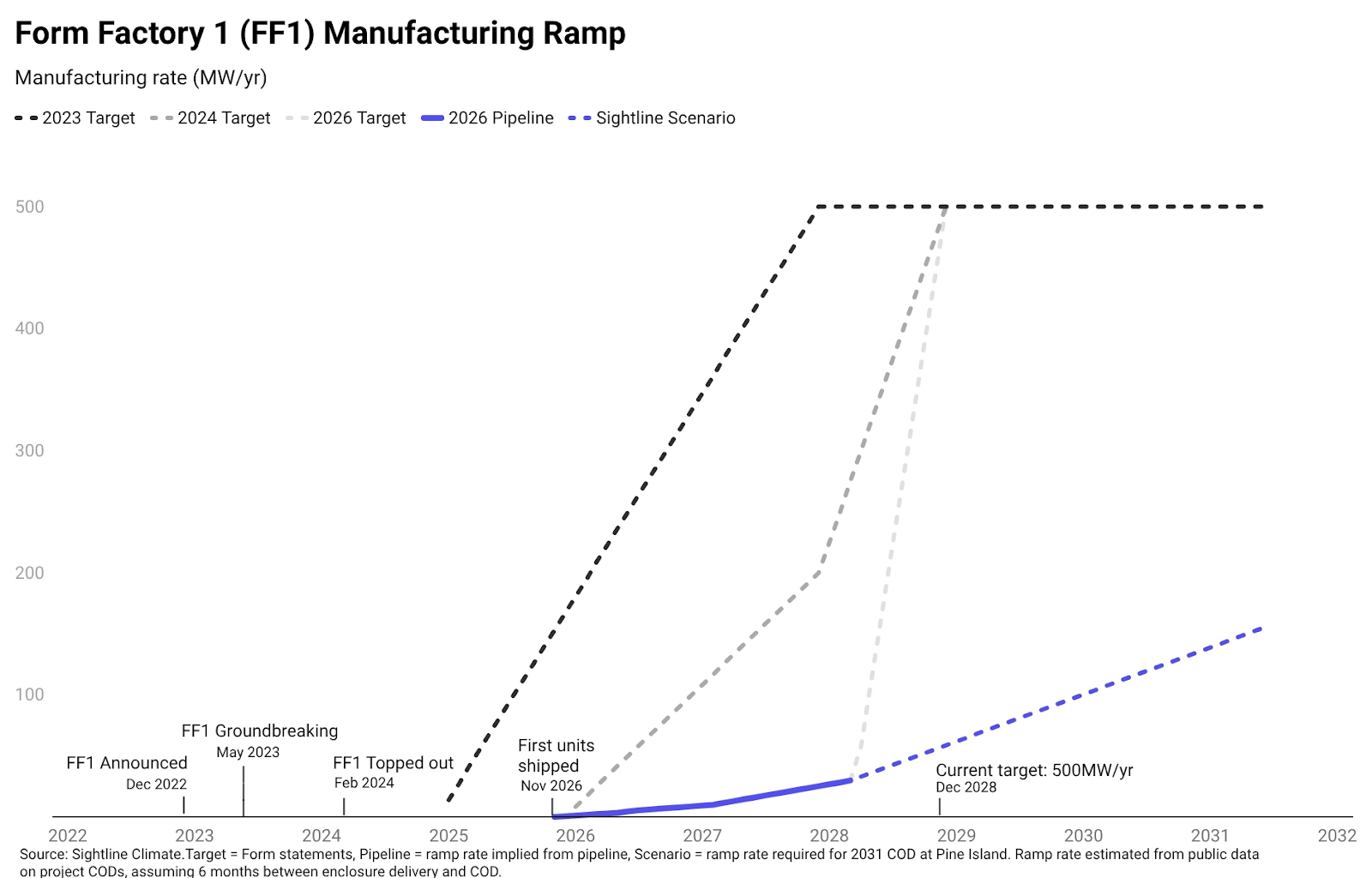

Google made another bet in its all-of-the above power strategy last week, this time committing to offtake 300MW/30GWh of Form Energy’s novel iron-air batteries for a Minnesota data center, powered by Xcel. This marks the largest LDES contract ever signed and the first credible signal that hyperscalers may become a structural demand driver for multi-day storage. Clients can read our full analysis about it here.

What happened

On 24 February, Xcel Energy announced a package of new generation and storage to support a Google data center in Pine Island, Minnesota: 1.4GW of wind, 200MW of solar, 300MW/30GWh of Form Energy iron-air batteries (100-hour duration), and a $50m investment in a Minnesota-wide distributed storage procurement program.

Google will fund this through a bespoke Clean Energy Accelerator Charge tariff with Xcel, which still requires Minnesota PUC approval. The project represents a 30x scale-up from Form Energy's largest previously contracted project, and comes after a difficult 2025 for the company marked by manufacturing delays, lapsed MoUs, and a canceled DOE grant (although now it reportedly plans to go public). Pine Island is planned to come online between 2028 and 2031.

While this alone will not solve Google's near-term power crunch, it’s just the latest move in what is now a remarkably broad portfolio hedge: enhanced geothermal, SMRs, fusion, gas-plus-CCS, hydropower, and LDES (now 2x). Not to mention its acquisition of Intersect Power and partnership with NextEra.

Mark’s take

For me, including Form's iron-air battery in Pine Island comes down to optionality and competition. A 100-hour battery expands the map of where Google can site a data center. It can go to harsher climates, more remote locations, and wind-heavy grids. But really that’s just the start. Right now, in SPP, PJM, and it’s looking like elsewhere as well, data centers that can bring their own capacity are prioritized in interconnection queues. If you can offer that capacity via a few hours with lithium-ion, you’re good – if you can offer it for days with a Form battery, you’re golden. So if this first run with Form works, Google gets a repeatable template for jumping queues wherever it builds next.

And that’s the real prize. A structural competitive advantage. As part of the deal, Google likely holds a right of first refusal with Form, meaning a proven Pine Island gives it a model for getting data centers online faster. In this winner-take-all AI buildout we’re in, this could be the key difference-maker. Yes, rivals could fund their own Form Energy or other LDES tech, but Google has the head start, and the $1bn spending now on Form’s battery will look like an absolute bargain. So while other hyperscalers are still arranging their pieces or figuring out the rules of the game, it looks like Google is a few moves ahead.

Who this helps

Form Energy is the obvious beneficiary as this is a lifeline after a bruising year. The project could generate $1bn in revenue from Xcel plus up to $1.35bn in 45X manufacturing tax credits, providing the working capital and investor confidence Form needs to execute its manufacturing ramp, which has been hampered by delays. If this model works and becomes a template, other LDES suppliers like Eos Energy Enterprises, Energy Dome could also find durable demand.

Who should be nervous

Form Energy itself, paradoxically. A 30x scale-up also means 30x execution risk. Utility dockets suggest Form can produce only around 30MW/year as of early 2028, against a project that requires ~300MW of deliveries. And tbh, Google and Xcel should be a bit nervous, too, should concerns from ratepayers and state regulators around cost passthrough surface during PUC review.

A quick read on the numbers shaping the market. The capex, the contracts, the regs, all anchored in the so-what.

$100bn // Adani Group’s new announcement for renewable-powered, hyperscale AI data centers across India by 2035. It brings India onto the global stage in the global AI infrastructure race, and creates additional opportunities in power generation, storage, and grids.

$26.5bn // DOE's largest-ever loan to subsidiaries of Southern Company in Georgia and Alabama. The utility is building 16GW of firm power across new generation, uprates, and grid upgrades to feed the region’s data center boom. The loan guarantee allows the utility to borrow at below-market interest rates, in an attempt to shield ratepayers while deploying capital, as Southern has voluntarily frozen rate increases through 2028.

$14bn // the price of Engie’s acquisition of UK Power Networks, the UK's largest electricity distribution network operator across 192,000km of network and 8.5m customers. The deal shifts Engie further into regulated electricity infrastructure, while UKPN's existing strengths in data center grid connections and AI-driven network optimization make it a particularly valuable asset as electricity demand surges.

$4bn // the price of CPP Investments and Equinix’s acquisition of Nordic data center operator atNorth, with CPP taking a ~60% controlling stake for $1.6bn and Equinix holding the remaining ~40%. The deal brings CPP and Equinix an 800MW development pipeline coming online over five years, plus 1GW of additional secured power capacity, significantly expanding its footprint in the Nordics, where cheap renewable energy and cold climates make it a prime region for power-hungry AI data center infrastructure.

$171.5m // US DOE funding to advance next-generation geothermal through field-scale testing and exploration drilling. The agency announced this new opportunity for enhanced geothermal systems (EGS) and resource characterization, to derisk development to unlock what it estimates could be 300GW of geothermal capacity on the US grid by 2050, compared to just ~4GW today.

830MW // US-based wind and solar portfolio that Enel is buying from Excelsior Energy Capital for ~$1bn ($1.2m/MW). The deal brings Enel's North American renewable capacity to ~13GW and reflects its broader brownfield growth strategy — buying operating assets in stable markets rather than taking on greenfield development risk. For Excelsior, it helps fund its aggressive greenfield power development strategy. Close expected Q3 2026.

Explore more Signals on Sightline here.

The policies, rulings, and company moves worth watching.

Ohio bill could require a 50% capacity factor. Ohio’s SB 294 is proposed legislation to redefine what counts as “reliable” and “clean” for approvals at the Ohio Power Siting Board. The bill’s “reliable energy source” definition includes a minimum 50% capacity factor and always-dispatchable output with one-hour ramping, a screen that is structurally hostile to most wind/solar projects (and even peakers and coal) absent firming.

New Mexico closer to jumping on the VPP bandwagon. The GRID Act (HB 311) would create a statewide VPP market. Continuing a trend across several states, it directs the Public Regulation Commission to adopt rules by 31 Dec 2026 requiring regulated electric utilities to implement VPP programs that allow DERs to be aggregated by utilities or third parties to provide grid services.

Nevada’s Esmerelda 7 & Greenlink Connection could be back on. The largest solar farm in the US was canceled by the Department of Interior last fall, but movement could be on the horizon. Nevada Governor Joe Lombardo said he met with President Trump, and the President agreed to end the moratorium on solar projects on federal lands in the state.

PJM behind-the-meter reform. PJM has proposed updating its 2004-era BTM rules. Most notably, it proposes introducing a 50MW threshold above which new BTM loads can no longer net on-site generation against transmission and capacity charges. This directly reshapes the economics for large industrial CHP projects and hyperscale AI data centers seeking to colocate with generation inside PJM, which has faced growing pressure around cost-shifting and grid reliability as massive new loads enter the system.

The latest research, features, and data drops on the Sightline Climate platform.

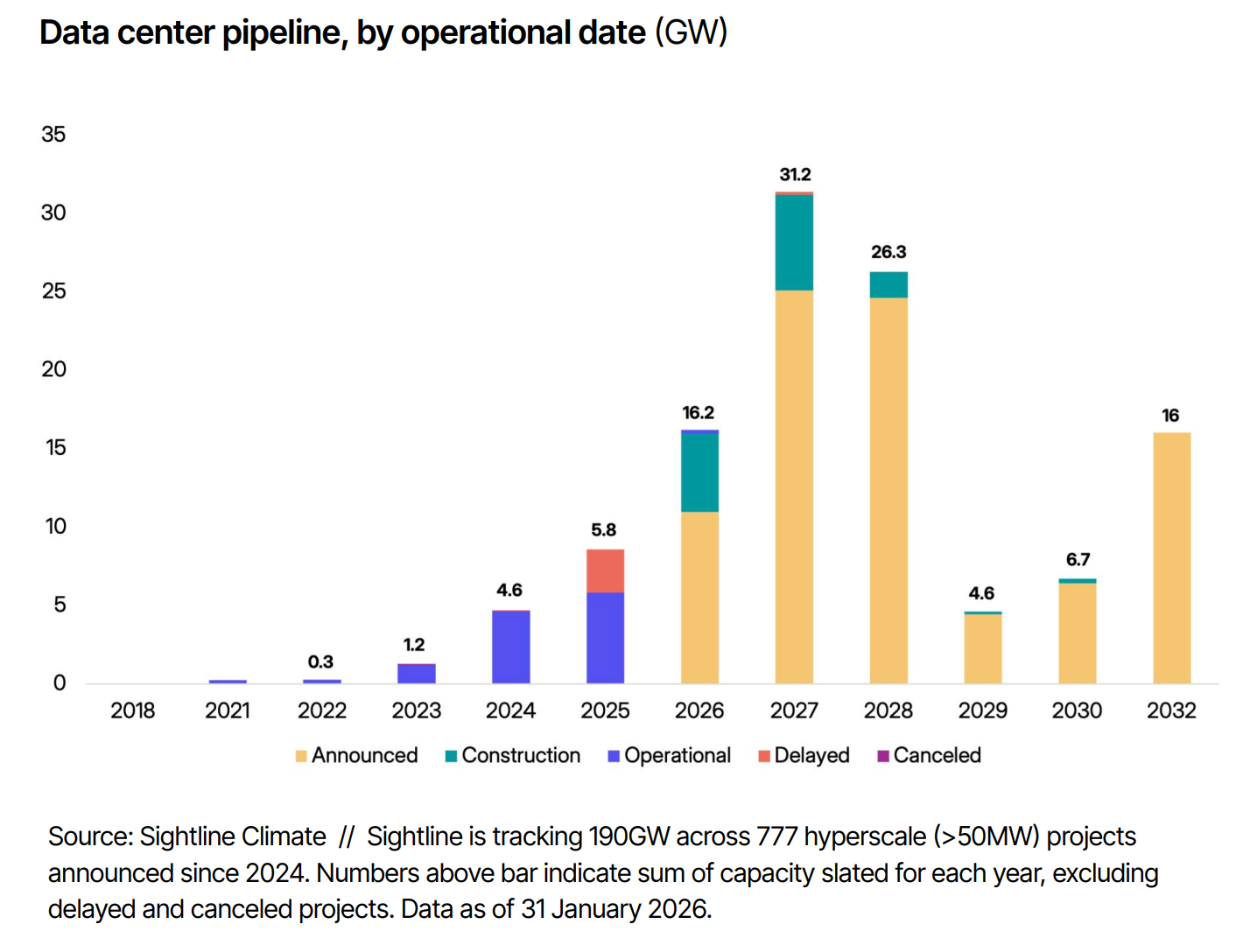

Q1 2026 Data Center Outlook. Our first outlook diving into the data center project pipeline to analyze progress. With 16GW due online in 2026, only 5GW is real right now. Clients can read it here.

Q1 2026 Clean Firm Outlook. The biggest moves and what to watch in clean firm this quarter. With hyperscalers throwing novel clean firm technologies a lifeline in their search for fast clean firm power, standouts are gearing up to hit public markets. Clients can read it here.

Q1 2026 Carbon Outlook. CCS growth has been hyped as part of the data center boom, but it’s a challenging application and CBAM is becoming a real demand driver for industrial CCS. A look at the project pipelines again, with a de-risked pipeline for CCS and DAC. Clients can read it here or covered here in the Financial Times.

Where the market is meeting, and where to find us

📅 Energy Storage Australia 2026 // Sydney, 17-18 March, 2026 // Australia’s largest dedicated storage event returns to Sydney, connecting global technology providers with local project developers and policymakers.

📅 Future of Utilities: Energy Transition Summit // Amsterdam, 18-19 March, 2026 // A key event on the European calendar for utilities, OEMs, and investors in the EU market. Join our Head of Research, Julia Attwood, on site.

📅 CERAWeek // Houston, 23-27 March, 2026 // Dubbed the Super Bowl of energy, where energy executives, policymakers, and technology leaders converge. Join Sightline CEO, Kim Zou, and others at the Sightline clients and friends dinner.

Attending an event? Connect with our team.

That's a preview of Powerstack. Every Thursday, we'll bring you the one signal that matters, the data moving the power system, and what's coming down the docket.

Want this in your inbox every week? Subscribe to Powerstack now.

And if you want the full depth - the research, datasets, and analysis behind every signal - that's what the Sightline platform is for. Request a demo here.

England strikes lithium and comes up with geothermal gold

Stricter foreign sourcing rules reshape clean energy tax credit eligibility

Newsletter

Newsletter