Amidst the crypto crash and backdrop of the market downturn, venture capital funds broke a record - for the largest amount of capital raised ($151b) in any prior full-year, and the year’s not done yet! The surge has lined the pockets of venture funds with nearly $300b of dry powder, a cash pile that’s ready to deploy.

Over the past ~2 years, we’ve tracked 135 new climate investment funds with an explicit decarbonization focus. Given the time it takes to raise a new investing vehicle, fund announcements arrive as lagging indicators after cycles of strong market promise - likewise, as the crossovers and sector tourists retreat to more familiar pastures, these dedicated funds will delay any ensuing waves and maintain stability of capital flowing to climate cos.

TL;DR climate deals will keep happening, despite the market backdrop.

$94B of new private climate AUM across 132 VC, Corporate VCs, Growth, Infra, and Private Equity funds since Jan 2021

While the count of new climate funds (65 and 63) was nearly identical between FY’21 and ’22 YTD, the $AUM more than doubled from $30B FY’21 to $64B ’22 YTD

A majority of the $AUM is concentrated in a few, mega funds. ~20% of the count of new funds are >$500m, but control ~80% of the $AUM

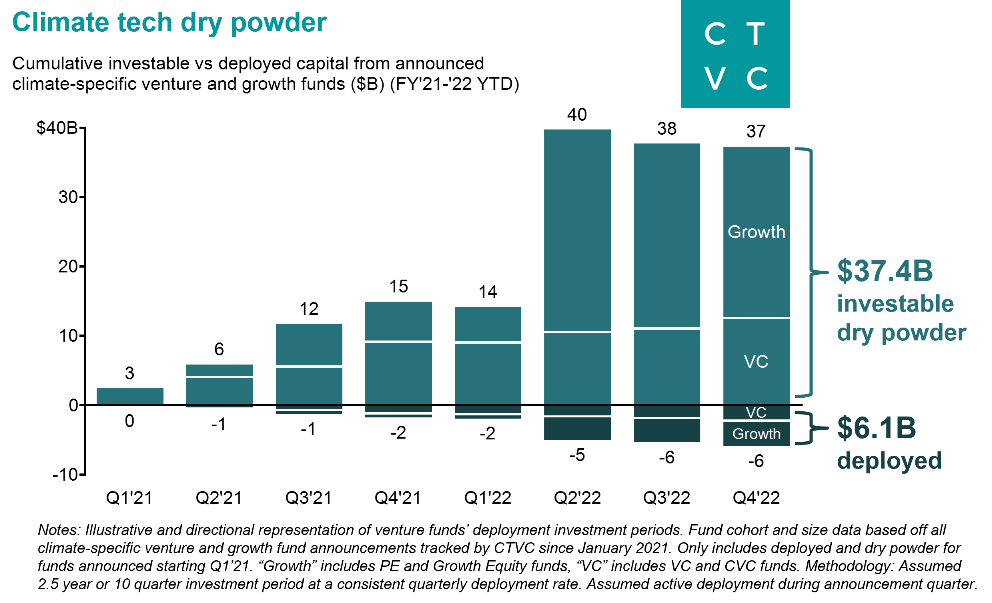

Following some standard deployment assumptions, we expect that $6b of that reserved capital from VC and Growth funds has been plowed into climate companies. Which means that there’s $37b of investable dry powder ready to deploy

Climate tech’s new money in the game

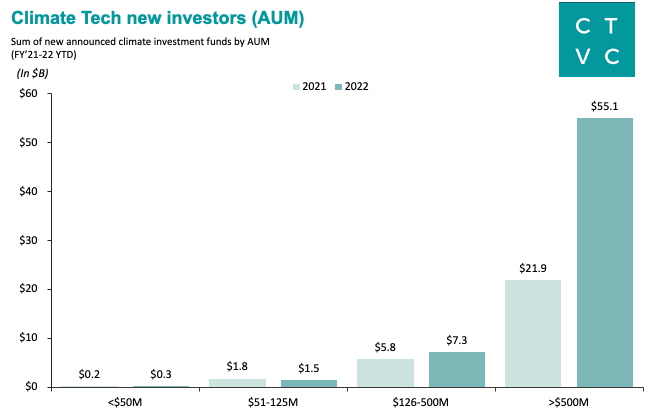

The new announced climate funds distributed relatively evenly across AUM sizes, with a majority of the count of funds concentrating in the $126-500m large-scale venture, small-scale growth sweet spot

Interestingly, the number of announced new funds both years stayed relatively flat, including across fund sizes

Numbers alone can be deceiving. While the count of new $500m+ funds stayed static between years, the total AUM size of $500m+ funds more than doubled (2.6x) from 2021 to 2022

Just 4% of new private climate capital is managed by <$125M sized funds, 14% by mid-range $126-500M managers, and 82% of AUM is concentrated into >$500M mega-funds

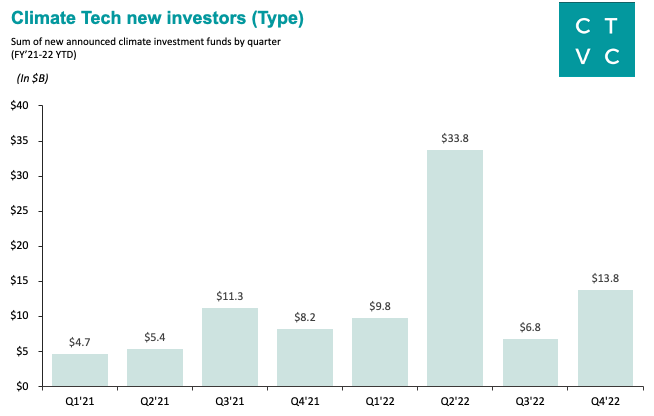

$34B of growth capital (36% of the total capital raised in the last two years) hit in Q2’22 alone with the launch of a whopping 5 unicorn ($1B+) sized funds: Brookfield Global Transition Fund ($15B), TPG Rise Climate’s ($7B), Temasek GenZero ($3.6B), Energy Capital Partners ($3B), Generation Investment Management ($1.7B)

The climate capital stack

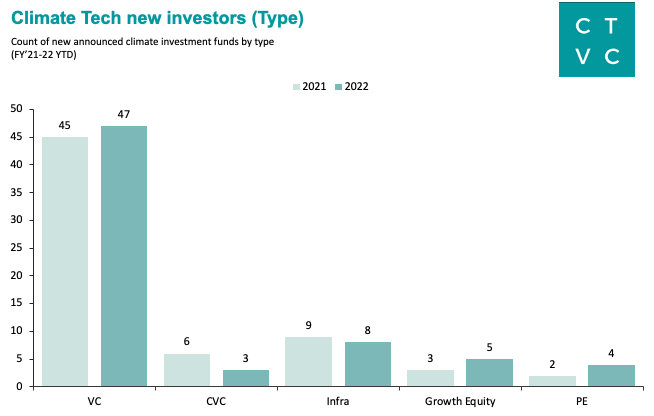

Curiously, the count of new funds by asset class stayed almost entirely identical between 2021 and 2022. A slight pickup in Growth Equity and PE funds could signal more supply at the end of the capital stack ready to fund the next maturing cohort of climate unicorns, seeded earlier in the climate capital stack

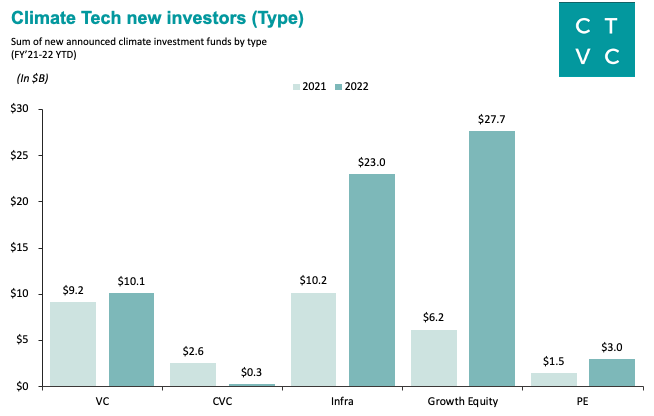

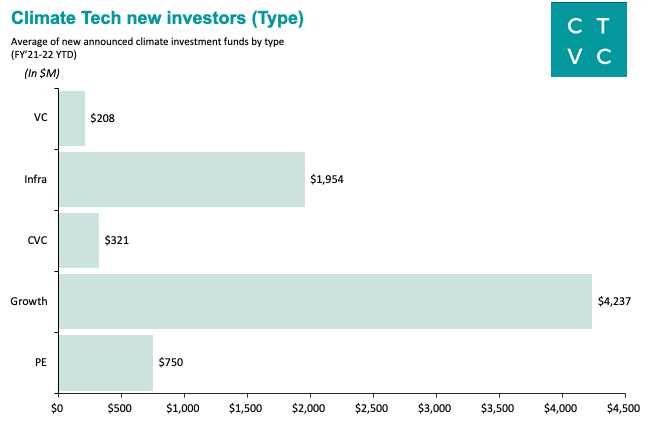

VCs and CVCs made up ~75% of the count of new funds but just 20% of $AUM, while Growth made up ~5% of the count and over 1/3rd of $AUM.

The 80/20 rule holds. Growth, PE, and Infra funds together account for ~25% of funds, but control ~80% of total AUM

Majority of the increase in new fund dollars were driven by 2X+ step up in PE and Infra funding and 4X+ step up in Growth capital

Average fund sizes shows a fundamentally different structure across asset classes with VCs averaging $200M per fund, CVCs $300M, Infra $2B, Growth $4B, PE $750M

Dry powder abounds for early and growth

Back in mid-June we ran the math on dry powder. Turns out that that calculus came in the middle of the hottest AUM announcement quarter in the past two years ($34B of growth capital, 36% of all total capital raised since 2021). Now that the deluge has settled, our updated analysis reflects data from the funds’ final close date (vs first announcement date), hence the updates to our dry powder estimates. (For example, TPG Climate Rise Fund first announced in August 2021 at $5.4B, but closed in April 2022 at $7.3B). We follow some standard deployment assumptions to reach a conservative dry powder estimate:

2.5 year or 10 quarter investment period at a consistent quarterly deployment rate

Deployment starts in the final close announced quarter (most significant assumption, as large funds from existing firms typically deploy into warehoused investments pre-final close, and certainly pre-announcement)

Assumes 100% AUM is invested, using recycling to make up for management fee costs

We excluded Infrastructure funds from the dry powder analysis due to their different deployment approaches, though included in count and AUM throughout the rest of this post

Since the start of 2021, 101 climate VC and CVC funds (“VC”) totaling $22B and 14 Growth Equity and Private Equity funds (“Growth”) totaling $38B have been announced. We expect that ~$6.1B of that new reserved capital has been plowed into climate companies since the start of 2021. Which, if assumptions hold, means that there’s at least ~$37.1B in the tank to fuel climate tech innovation.

Of note, this dry powder only includes net new capital that’s specifically marked for climate. As we’ve written about before, strong syndicates are built on diversity of capital, which the past 2 years have enjoyed - as 2,000+ unique funds have participated in at least 1 climate deal. In our midyear update we showed that 80%+ of the investment firms that have participated in at least 1 deal in Food & Land Use are “general investors” who infrequently join other climate deals (vs Carbon deals where 55% of investors frequently join other climate-specific rounds). Even in the most conservative of scenarios, where no further climate funds were raised, the sector would still be able to support growth.

All in all, over the past two years, the rate of new fund creation and the size of new funds has not slowed down at all. In particular, the market is flush with net-new Growth capital ($34B) to fund that first cohort of climate companies now about to reach growth stage. LPs continue to back new climate vehicles, though it’s important to remember that committed capital is not called capital. Only cold hard wires will tell the story of whether dry powder actually fuel the cannon of climate new cos.