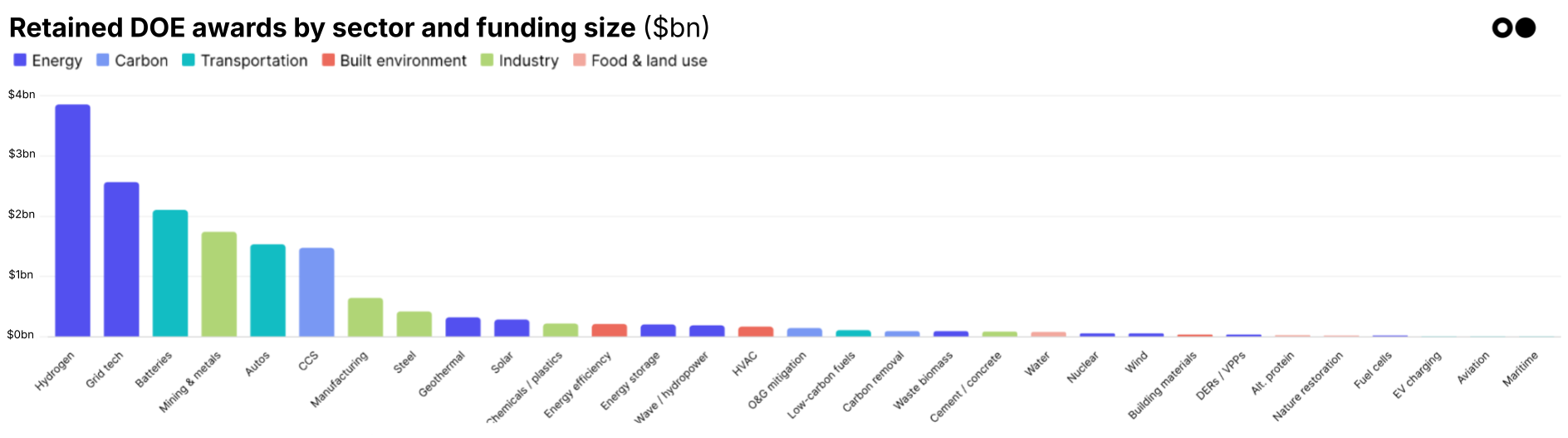

A breakdown of the Biden-era grants DOE plans to keep and cut

Happy Monday - coming to you live from San Francisco Climate Week, and hope to see a lot of you there throughout the week!

In this edition, we ran the numbers on the DOE's reinstated grants by sector and value. The breakdown below.

In deals, $678m in solar and battery development, $650m in EV manufacturing, and $170m in autonomous transportation system development.

In other news, the Strait of Hormuz closure's impact on oil prices and Europe's decarbonization goals, plus data center backlash. (We're trying out a new format for our news links this week. Respond to this email and let us know what you think!)

Thanks for reading!

Not a subscriber yet?

📩 Submit deals and announcements for the newsletter at [email protected].

💼 Find or share roles on our job board here.

CTVC is powered by Sightline Climate, the tactical market intelligence platform for energy and investment decision-makers.

This week, the Department of Energy released a list of the 1,951 Biden-era grants it plans to "retain or modify," representing over $23bn in funding awarded under the Inflation Reduction Act and Bipartisan Infrastructure Law. We’ve got a closer look at what was kept, what was cut, and what’s still unclear in this new portfolio reconstruction.

After 15 months of delays, freezes, and cancellations, DOE told Congress it had completed its review of 2,271 total grants and intends to move forward with 86% of them.

Latitude published the list of the projects and decisions, and it’s telling of the administration’s priorities:

Winners

Losers

With oil markets rattled by the Iran conflict and grid operators warning of capacity shortfalls from the data center buildout, energy security has become the dominant frame in Washington. It's visible in this data too. Critical minerals stay safe, and supply-side infrastructure gets protected: grid hardware, industrial manufacturing, hydrogen production, carbon capture at point sources. They’re also mostly fossil-adjacent programs. But the ones that got frozen are largely ones that would reduce American households' exposure to fossil fuel price spikes -- building efficiency, home electrification, demand-side adoption programs that Congress explicitly mandated and funded.

The administration is making an energy security argument while defunding the programs that could help deliver it. And even for projects officially retained, 15 months of delays and widespread staff departures have left questions about what’s possible, operationally.

There’s also a legal question: A federal court already ruled that DOE's October terminations were unconstitutional, as the department admitted the primary basis was state political affiliation. DOE's response was to restore 18 of 321 canceled projects, but so far, every retained project is in a red state and every non-retained one is in a blue state. (See the DOE Alumni Substack for a full breakdown).

🚗 Slate Auto, a Troy, MI-based electric vehicle manufacturer, raised $650m in Series C funding from TWG Global.

🚆 Glydways, a South San Francisco, CA-based autonomous transportation system developer, raised $170m in Series C funding from ACS Group, Khosla Ventures, Suzuki Motor Corporation, Gates Frontier, Mitsui Chemicals, and other investors.

⚡ Nova Fusion, a Shanghai, China-based modular nuclear fusion reactor developer, raised $103m in Pre-Seed funding from Alibaba Group, DragonBall Capital, Gaorong Ventures, Guanghe Capital, Hillhouse Investment and other investors.

🌡 NanoTech Materials, a Houston, TX-based insulative and fireproof coatings developer, raised $29m in Series A funding from HPI Real Estate & Investments, GOOSE Capital, and Milliken & Company.

⚡ Critical Loop, a Long Beach, CA-based industrial power solutions provider, raised $26m in Series A funding from Conifer Infrastructure Partners, Hanover, Adapt Nation Capital, Better Ventures, Climate Capital, and other investors.

🧪 Hybron, an El Segundo, CA-based automated composite manufacturing technology developer, raised $25m in Seed funding from Marque Ventures, American Center for Manufacturing & Innovation (ACMI), Bravo Victor Venture Capital (BVVC), DTX Ventures, First In, and other investors.

🛰 Kelluu, a Joensuu, Finland-based autonomous airship aerial monitoring platform, raised $18m in Series A funding from NATO Innovation Fund (NIF), Gungnir Capital, Keen Venture Partners, and Tesi.

🌾 Agriodor, a Rennes, France-based odor-based biocontrol products developer, raised $18m in Series A funding from Crédit Mutuel Impact, CAAP Création (Crédit Agricole Alpes-Provence), CapHorn, Capagro, Région Sud Investissement, and other investors.

⚡ Sora Fuel, a Cambridge, MA-based DAC SAF technology solutions provider, raised $15m in Seed funding from Inspired Capital, Spero Ventures, Engine Ventures, and Wireframe Ventures.

⚡ Sharing Energy, a Minato-ku, Japan-based distributed solar energy provider, raised $5m in Series C funding from AG Capital, Dai-ichi Life Insurance Company, Fintech Global, GMO Venture Partners, JOYO Bank, and other investors.

🍎 Fermtech, an Oxford, England-based solid-state fermentation ingredients developer, raised $3m in Seed funding from Elbow Beach Capital, Carbon13, and Empirical Ventures.

⚡ Aliste Technologies, a Noida, India-based home automation technology software, raised $3m in Seed funding from Big Global JSC, Hbeon Labs, and YourNest Venture Capital.

⚡ Ecoil, a Jaipur, India-based used cooking oil supply chain organizer, raised $3m in Series A funding from Fundalogical Ventures, Caspian Impact Investments, Momentum Capital, and The Chennai Angels.

♻️ MAECONOMY, a Heerlen, Netherlands-based financial infrastructure for circular materials provider, raised $2m in Seed funding from Limburg Investment and Development Company (LIOF) and LUMO Labs.

🌡 BurnBot, a South San Francisco, CA-based wildfire mitigation technology developer, raised an undisclosed amount in Series A funding from Elemental Impact.

⚡ Elgin Energy, a London, England-based solar projects designer, raised $678m in Debt funding from BNP Paribas, NatWest, Siemens Bank, Société Générale, and Standard Chartered.

⚡ Elevate Renewables, a Boston, MA-based battery energy storage project developer, raised $50m in PF Debt funding from Rabobank.

⚡ Zanskar, a Salt Lake City, UT-based geothermal site development platform, raised $40m in Debt funding from Just Climate, Spring Lane Capital, and Tierra Adentro Growth Capital.

⚒️ pH7 Technologies, a Vancouver, Canada-based critical mineral extraction technology developer, raised $8m in Debt funding from RBCx.

🔋 Harmony Energy, a Knaresborough, England-based battery energy storage operator, raised an undisclosed amount in Debt funding from Navigator Energy Debt Finance (NEDF).

⚡ Acea Energia, a Rome, Italy-based electricity and gas supplier, was acquired by Plenitude at an implied valuation of $688m.

🌞 Sigenergy, a Shanghai, China-based integrated home energy solutions developer, filed for IPO raising $562m.

⚡ 45-8 Energy, a Metz, France-based helium exploration and production service provider, was acquired by Ad Terra Group for an undisclosed amount.

♻️ Ascend Elements, a Westborough, MA-based sustainable battery material recycling manufacturer, has filed for Bankruptcy.

Vesper Infrastructure Partners, a Milan, Italy-based mid-market clean energy and sustainable infrastructure investment firm, completed a final close of $1.2bn for the Vesper Next Generation Infrastructure Fund I, targeting pan-European investments in clean energy, decarbonized mobility, digital infrastructure, and sustainable living from European Investment Fund.

Australian Ethical Investment, a Sydney, Australia-based impact investment firm, completed a first close of $441m for the Australian Ethical Growth Opportunities Fund, targeting growth-stage unlisted assets in decarbonization, circular economy, and climate tech via funds, co-investments, and direct investments from Australian Ethical Investment and Clean Energy Finance Corporation.

Triodos Investment Management & Fondaction, a Zeist, Netherlands & Montreal, Canada-based impact investment firms, completed a first close of $18m with $351m target size for its Value Nature Fund I, a natural capital fund from Fondaction, focusing on biodiversity, sustainable agriculture, and ecosystem restoration.

EIG Geothermal Catalyst Partners, a Washington, DC-based institutional investor in energy and infrastructure, completed a close of undisclosed amount for its geothermal-focused fund, EIG Geothermal Catalyst Partners (the “Fund”), from undisclosed investors, focusing on geothermal power projects.

This is a sample of deals available for Sightline clients. Can’t get enough deals?

⛽ Oil and gas prices surged again amid continued stop-starts in the Strait of Hormuz. Iran shut the waterway in response to the ongoing US naval blockade, and Trump escalated further by announcing the seizure of an Iranian cargo ship attempting to breach it. The ceasefire expires tomorrow, but last week saw Brent whipsawed nearly 20%. [Link]

The structural damage is the bigger concern: nearly two months of ~13m barrels/day shut in, with cumulative lost supply now above half a billion barrels. Even a deal won't unwind that quickly — tanker backlogs, shell-shocked insurers, and damaged infrastructure mean elevated energy prices are baked in well into summer.

⚡ Europe is split on how to respond to the energy shock from the Iran war. Brussels is using the crisis to push harder on the clean energy transition, while member states are quietly subsidizing their way through it. [Link, Link]

The EU Commission is supposed to drop a new proposal tomorrow to slash electricity taxes and accelerate renewables. But on the ground, 22 of 27 member states have rolled out 120+ crisis measures totaling €9bn+, mostly fossil fuel subsidies and VAT cuts, with almost no structural clean energy investment attached. Europe also came into this with gas storage at historic lows, so the pressure is to reach for short-term relief over long-term transition.

🏗️ Local backlash to data centers is intensifying, from laws to protests. Maine passed a moratorium on new large data center construction, a Wisconsin city passed the first anti-data center referendum, and violent protests against data center infrastructure are emerging as a new risk factor. [Link, Link, Link]

As AI drives massive load growth, the bottleneck is no longer just power supply, it's siting. Communities are pushing back on land, water, and energy use, and as digital infrastructure becomes more critical, it's increasingly exposed to both physical and political threats.

🏔️ China has begun building a high-altitude solar project in Tibet under extreme conditions, near half the height of Everest. [Link]

💡 BCap’s 6 new principles for energy tech investing, from efficiency to scalability to timing. [Link]

👟 Sustainable shoemaker Allbirds is flying the coop for AI, with a complete business redesign towards making AI compute hardware. [Link]

📅 Women CEOs in Climate – Hard Lessons Learned: Join other CEOs, founders, and aspiring entrepreneurs on April 24 from 11:30-12:30pm EST on Zoom. Learn from four women CEOs who have built and sold ventures. Speakers will discuss topics ranging from raising capital without losing leverage to building teams that can actually execute.

📅 Metrics that Matter for Climate Deep Tech at Series A & B+: On April 30 from 1:00-2:30pm EDT, learn from experienced deep tech founders about the challenges and opportunities in scaling climate deep tech. The panel will cover questions on what milestones actually unlock funding and how to think about financial metrics when scale is non-linear, plus more.

💡 The Electric Innovation Awards: Apply by June 3 to be recognized for innovative leadership in electrification. Eligible ventures span sectors such as transportation, buildings, manufacturing, public fleets, and grid modernization or resilience efforts.

Data Analyst – Late-Stage Finance, @Sightline Climate

Marketing Lead, @Glimpse

Strategic Finance Engagement Lead, @Planetary Scale

📩 Feel free to send us deals, announcements, or anything else at [email protected]. Have a great week ahead!

Our new report ft. low-carbon data center megadeals, reopened public markets, and rise of adaptation

Get our new report on offtake, with HSBC

Newsletter

Newsletter