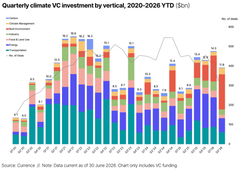

🌎 H1'26 climate tech funding up 55% to $26bn, thanks to data centers

Our new report ft. low-carbon data center megadeals, reopened public markets, and rise of adaptation

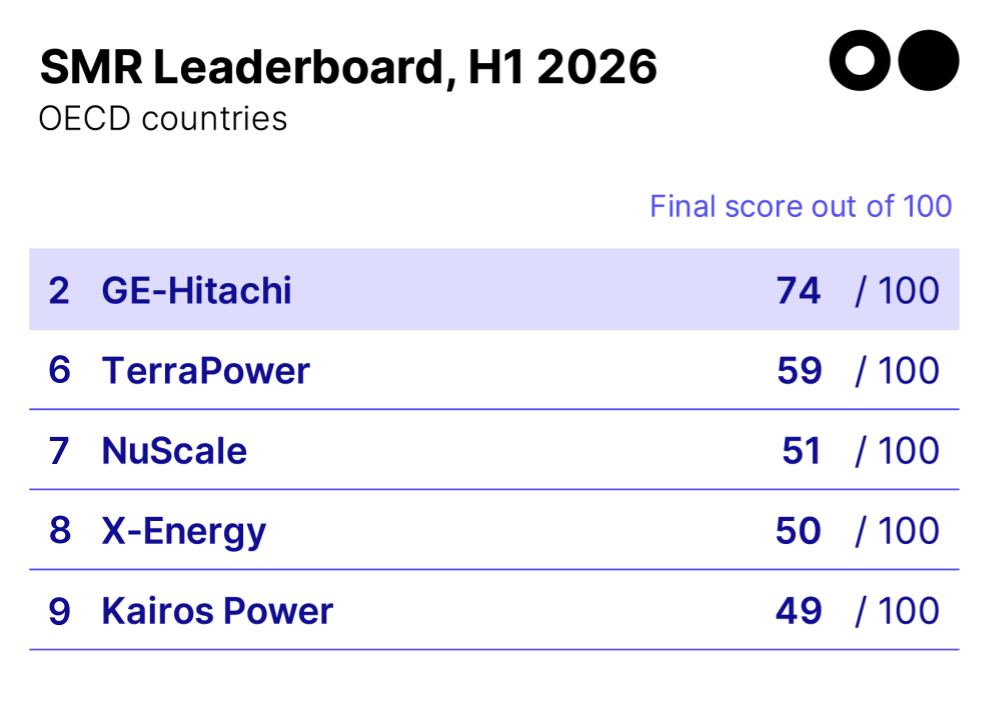

How Fervo, newcleo, Deep Fission, X-energy, General Fusion, and TAE stack up

Happy Monday!

The IPO window has officially swung open, with more nuclear SPACs announced in the last week. We get into the good, the bad, the ugly, and the bubbly below.

In deals, $240m for laser fusion energy in Germany, $200m for intelligent heavy-duty electric trucks in China, and $100m for stellarator fusion energy in New Jersey.

In other news, California’s CCS site, a massive Michigan BESS deal, and Exxon's move to Texas.

Thanks for reading!

Not a subscriber yet?

📩 Submit deals and announcements for the newsletter at [email protected].

💼 Find or share roles on our job board here.

CTVC is powered by Sightline Climate, the tactical market intelligence platform for energy and investment decision-makers.

In the space of three weeks, the public markets have absorbed a geothermal blockbuster, a second-time-lucky nuclear fission IPO, and the first European advanced reactor developer to SPAC:

AI data center demand has handed clean baseload power companies a price-insensitive customer base. Clean firm power companies are leveraging this unprecedented demand to vacuum up institutional capital on the public markets.

Sometimes, it’s before they see real revenue, hit commercial deployment targets, or get regulatory rubber stamps.

Sky-high valuations for pre-revenue companies? To the untrained eye, it looks like a textbook bubble.

But to the trained eye, there's different capital realities and motivations pushing these companies onto the public markets. It's the good, the bad, and the ugly. Or, the ready, the opportunistic, and the squeezed.

🟢 The ready: Fervo Energy

Fervo Energy represents the gold standard of this public cohort, pulling off a massive $1.89bn IPO on the back of its operational project data and a 320MW PPA with SoCal Edison and partnerships with Google. Fervo has had better economics, earlier revenue, and cheaper capital than any comparable startup. It faced its first minor speed bump, per Axios’ reporting of a recent well-control incident at its flagship 500MW Cape Station project in Utah, but that’s not expected to delay the plant's first scheduled power deliveries later this year.

🟡 The opportunistic: X-Energy, General Fusion, TAE Technologies/Trump Media, and Newcleo

New nuclear that hasn’t been deployed at scale is wildly expensive - but these advanced fission and fusion plays want to catch the macro tailwinds of AI data center mania and bridge the notoriously brutal private funding gap.

🔴 The squeezed: Deep Fission

Deep Fission seems to be looking for a lifeline as it runs out of private runway. The public offering reveals a company facing a steep cash burn, and last time it tried to go public in August, external auditors attached a stark "going concern" warning to their filing.

⚡ Focused Energy, a Darmstadt, Germany-based laser fusion energy company, raised $240m in Series A funding from BMH Hessen, European Innovation Council (EIC), Futury Capital, Prime Movers Lab, RWE, and other investors.

🚗 Zeron Truck, a Suzhou, China-based intelligent heavy-duty electric trucks start up, raised $200m in Series B funding from Aurahonorfund, Gaocheng Capital, InnoVen Capital, Ondine Capital, Oriza Holdings, and other investors.

⚡ Thea Energy, a Kearny, NJ-based stellarator fusion energy developer, raised $100m in Series B funding from US Innovative Technology Fund, Alumni Ventures, Calm Ventures, Climate Capital, Divergent Capital, and other investors.

🏭 Boston Metal, a Woburn, MA-based developer of electrified metals production technology, raised $75m in Series C funding from Tata Steel.

⚡ Utilidata, an Ann Arbor, MI-based power grid AI software and technology provider, raised $40m in Series C funding from Renown Capital Partners and Keyframe Capital Partners.

🧪 P2 Science, a Woodbridge, CT-based sustainable chemicals technology developer, raised $23m in Series C funding from Sofinnova Partners, BASF, CHANEL, Connecticut Innovations, Elm Street Ventures, and other investors.

💨 D-CRBN, an Antwerp, Belgium-based plasma-based CCUS technology company, raised $20m in Series A funding from Astaia, European Innovation Council (EIC), and SFPIM.

⚛️ Otrera, a Cherbourg, France-based sodium-cooled fast neutron reactor developer, raised $20m in Series A funding from EDF, Exergon, Normandie Participations, Groupe ADF, Ingérop, and other investors.

🥩 Pacifico Biolabs, a Berlin, Germany-based mycelium fermentation protein startup, raised $8.2m in Series A funding from FoodLabs, Simon Capital, Sprout and About Ventures, Stray Dog Capital, and other investors.

🌊 Caudal Energy, an Oxford, England-based next-generation biomimetic tidal energy developer, raised $5.8m in Seed funding from Creator Fund, Empirical Ventures, Kibo Invest, Oxford Innovation Finance, Oxford Science Enterprises, and other investors.

🍄 Mykor, a Bristol, England-based waste-based construction materials developer, raised $5.4m in Seed funding from Clean Growth Fund, Green Angel Ventures, Innovate UK, and South West Investment Fund.

⚡ Goshe Energy Storage, a Boulder, CO-based utility-scale battery energy storage developer, raised $40m in Debt funding from S2G Investments.

🔋 ACL Energy, a Milan, Italy-based utility-scale battery energy storage (BESS) developer, raised an undisclosed amount in PF Debt funding from Qualitas Energy.

🚗 Secured Transportation Services (STS), a Winder, GA-based nuclear logistics and transportation services provider, was acquired by NANO Nuclear Energy at an implied valuation of $13m.

🐟 Biomar, an Aarhus, Denmark-based aquaculture feed solutions developer and supplier, announced an IPO at an implied valuation of $1.7bn.

🥩 Bosque Foods, a Berlin, Germany-based mycelium fermentation food developer, was acquired by Infinite Roots for an undisclosed amount.

Transition Ventures, a London, England-based early-stage venture capital firm focused on AI, robotics, energy, and deeptech, closed a $150m Fund II to back early-stage founders building technologies at the intersection of software and the physical world.

Copenhagen Infrastructure Partners (CIP), a Copenhagen, Denmark-based energy infrastructure investment manager, launched its Advanced Bioenergy Fund II with a $1.7bn target to invest in biomethane and advanced bioenergy projects across Europe.

This is a sample of deals available for Sightline clients. Can’t get enough deals?

💨 California Resources Corporation achieved the first landmark carbon dioxide injection at Carbon TerraVault I (CTV I), a first-of-its-kind CCS project in Kern County, CA. [Link]

While a massive milestone for domestic carbon management, the commercial reality of CCS is still tough. For CRC, this project is a crucial regulatory and technological proof-of-concept, but long-term scaling will depend on sustained corporate offtake demand and getting past regional infrastructure bottlenecks in California.

⚡ LG Energy Solution Vertech and DTE Energy signed a $1.6bn, 6GWh supply deal in Michigan, the largest utility BESS agreement in US history. [Link]

This shows the hoops that everyone’s jumping through around data centers. The deal would leverage local manufacturing from LG’s Holland, MI facility to clear strict IRA domestic content hurdles and lock in a massive 10% tax bonus. And the BESS capacity funded directly by Oracle for its Saline Township campus would be so big it completely satisfies DTE’s entire utility obligation under Michigan’s 2030 Clean Energy Standard for battery storage. Plus, DTE wants to freeze ratepayer hikes until 2028, if regulators approve the package.

🛢 ExxonMobil shareholders overwhelmingly backed a proposal to redomicile the company's corporate charter from New Jersey to Texas. [Link]

This moves Exxon to a friendly jurisdiction: Texas’s newly updated business courts and corporate laws make shareholder lawsuits and climate-related proposals significantly harder to bring, effectively neutralizing the type of ESG activism that led to the Engine No. 1 board fight back in 2021.

📜 The OBBBA’s July 4 cliff is 33 days away, forcing wind and solar developers to rush physical construction to lock in tax credits before the One Big Beautiful Bill Act’s strict new deadlines hit. [Link]

☢️ China launched a competitive bid to build Serbia's first nuclear reactor, an SMR, indicating that Beijing may look to leverage its massive domestic infrastructure momentum to turn nuclear tech into its next global clean tech export front. [Link]

💻 A new breed of AI "neocloud" infrastructure companies is bypassing traditional hyperscalers to aggressively gobble up global power capacity. They’re redrawing the energy map by acquiring retired coal plants, cheap Nordic hydropower, and rural pockets of Texas, and overall acting more like real estate developers. [Link]

📅 NY Tech Week: We’ll be at events throughout the city this week, so let us know if you’re in town! Some that caught our eye: NewLab’s Critical Mass, LACI and CTEN’s Climate Scaling Summit, and (we’re not biased!) our own Planeteer Capital & Foley Hoag’s Bagels>Panels: Physical AI x Robotics.

📅 Trellis Impact 26: From Jun 23-25 in San Francisco, Trellis Impact brings together 3,500+ leaders powering the future of sustainable business, from AI-enabled solutions to emerging technologies reshaping decarbonization, energy, circularity, and beyond. Get practical insights and hard-won examples of the technologies and strategies that are influencing sustainable business transformation. Register and you can get 20% off with our partner code: TI26SCP

📅 Building & Financing AI in the UK: AI has become the largest driver of new power demand. While the UK aims to compete in this global buildout, it faces steep challenges—including high industrial electricity prices and a grid connection queue stretching into the 2030s. Join Sightline Climate at LCAW for the afternoon of June 23 to explore these issues.

Software engineer @Althea

Head of Finance, Investor @Gigascale

Analyst Trainee, Program Specialist Trainee, Bureau Chief of Budget & Procurement, Deputy Director of Grid Scale Resources, Deputy Director of Virtual Power Plants, Director of Clean Energy Planning & Analytics, Bureau Chief of Grid Scale Resources - Division of Clean Energy, @New Jersey Board of Public Utilities

Marketing Lead, @Glimpse

Senior Associate – Infrastructure, Capital Projects & Climate Advisory @KPMG

Risk Management – Climate, Nature & Social @JPMorgan Chase

📩 Feel free to send us deals, announcements, or anything else at [email protected]. Have a great week ahead!

Our new report ft. low-carbon data center megadeals, reopened public markets, and rise of adaptation

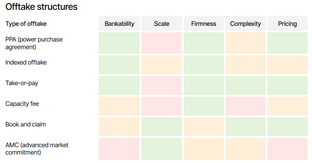

Get our new report on offtake, with HSBC

Inside the $915m bet on carbon removal's next phase

Newsletter

Newsletter