🌎 How corporates drive demand for FOAK projects #303

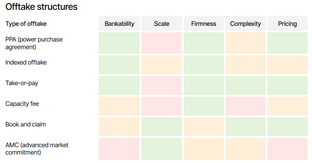

Get our new report on offtake, with HSBC

Our new report ft. low-carbon data center megadeals, reopened public markets, and rise of adaptation

Happy Monday!

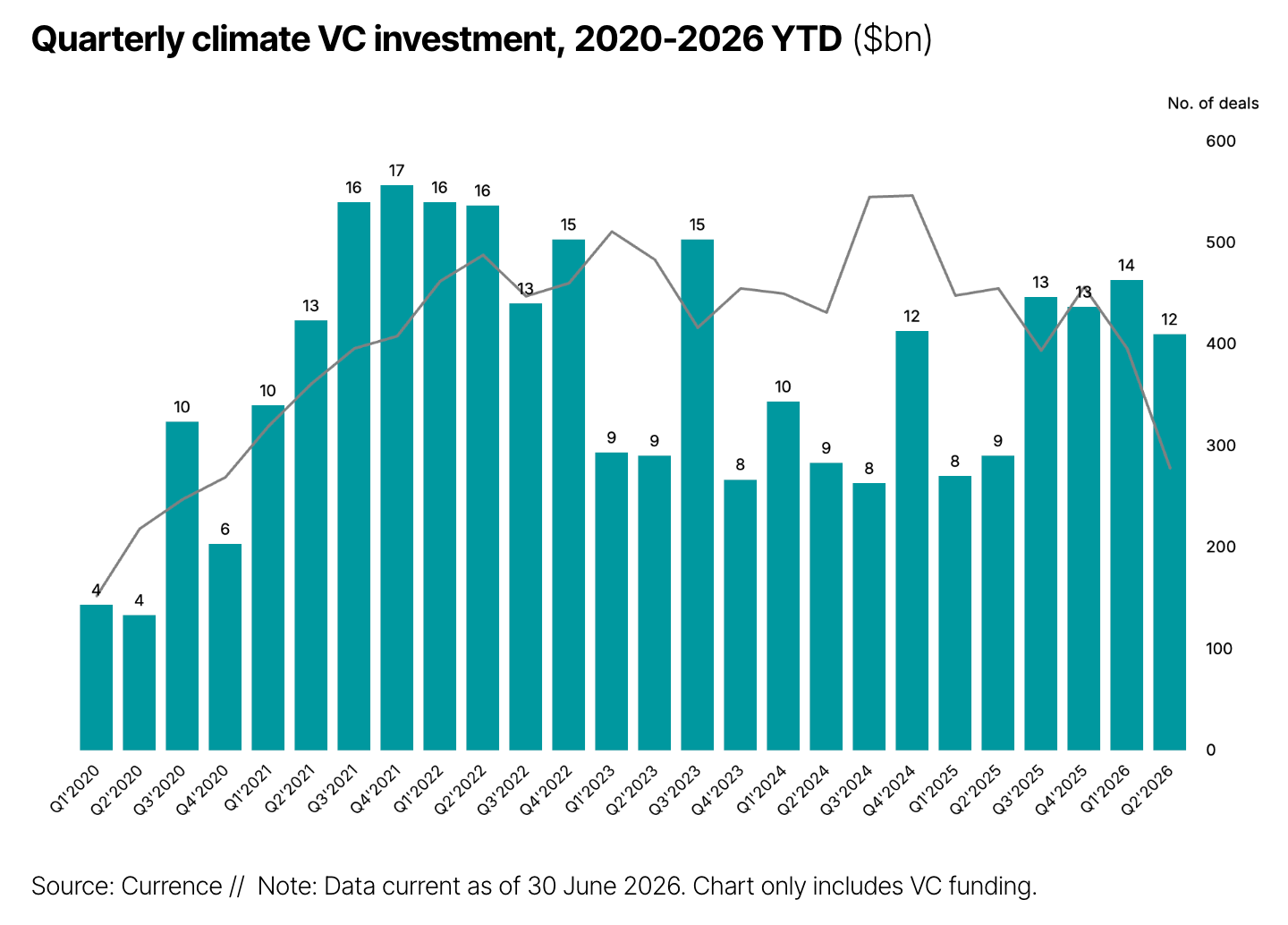

We've just dropped a new report today: our H1 2026 Climate Tech Investment & Innovation Report. Climate tech VC hit $26.1bn in the first half, up 55% year-on-year, and there are already some clear winners (ie, low-carbon data centers). Download it here.

In deals, $470m for stellarator fusion energy systems in Munich; $134m for geothermal drilling technology in Houston; and $30m for indoor farming operations and robotics in Half Moon Bay.

In other news, the UK sets a price for its plant extension, Western state governors agree on permitting reform, and startups achieve criticality.

Thanks for reading!

Not a subscriber yet?

📩 Submit deals and announcements for the newsletter at [email protected].

💼 Find or share roles on our job board here.

CTVC is powered by Currence, market intelligence to power the AI era.

Everyone's watching the World Cup semifinals, but we’ve got our own halftime report to share: our new H1 2026 Climate Tech Investment Trends Report is out now!

It shows that climate tech VC put $26.1bn on the board in H1'26, up 55% year-on-year, and that there are already some pretty clear winners.

Read on for the highlight reel (no VAR, sorry), or check out the findings in Bloomberg.

Currence clients get access to the full version of the report and all the data underlying it on the platform here. If you’re interested in becoming a client, talk to our team here.

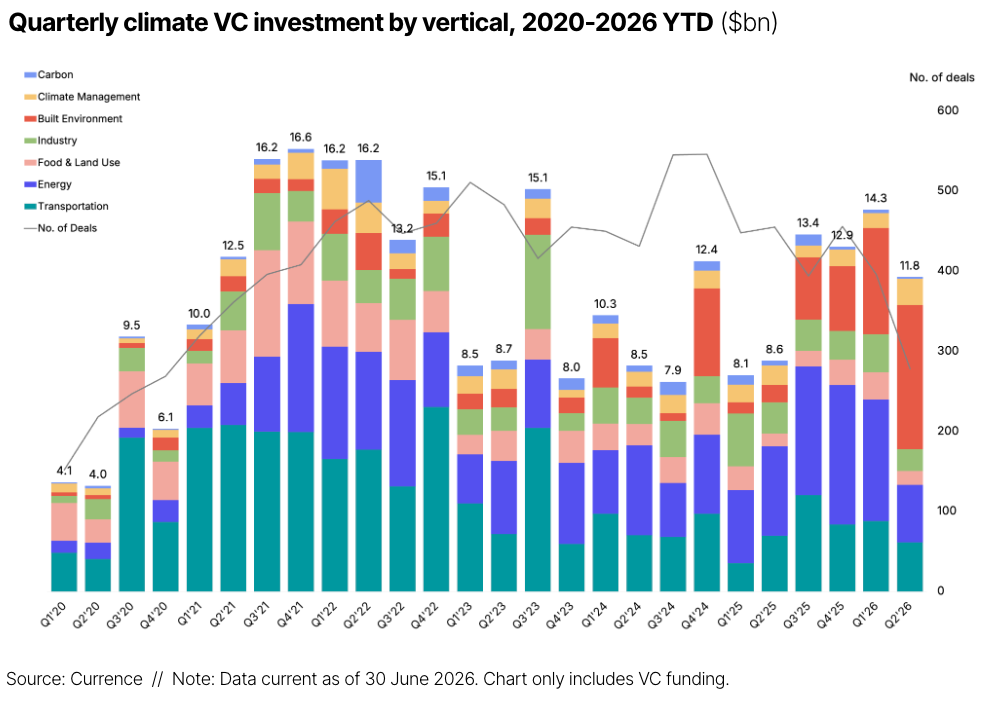

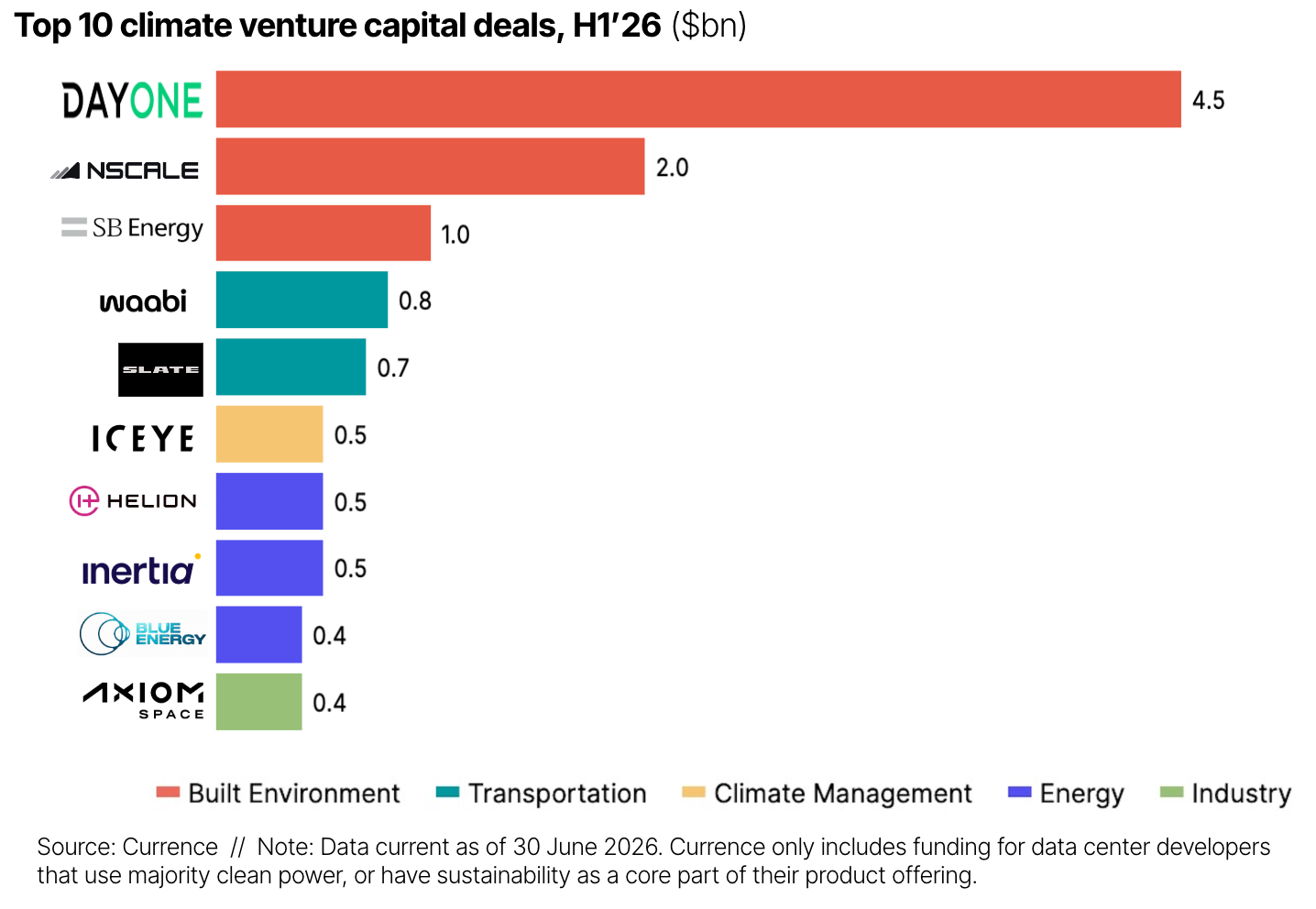

⚽ The best H1 since 2022, thanks to data centers, but fewer players on the field. H1'26 VC investment was 55% higher than H1'25, but the concentration in deals continues. Low-carbon data centers made up 34% of the half's investment, with a large portion coming from just two deals: DayOne ($4.5bn) and NScale ($2bn).

⚽ Clean firm power is breaking out. Energy IPOs and SPACs are beating expectations. Fervo ($1.9bn, up 35% on debut) and X-Energy ($1bn, up 27%) broke records for clean firm power IPOs.

⚽ Carbon and low-carbon fuels got subbed off early. Carbon is down 61% to its weakest half since 2020 - but capital is also taking the form of offtake instead of equity. Low-carbon fuels are also down 56% as US subsidies sunset and European buyers wait for 2027 policy reviews.

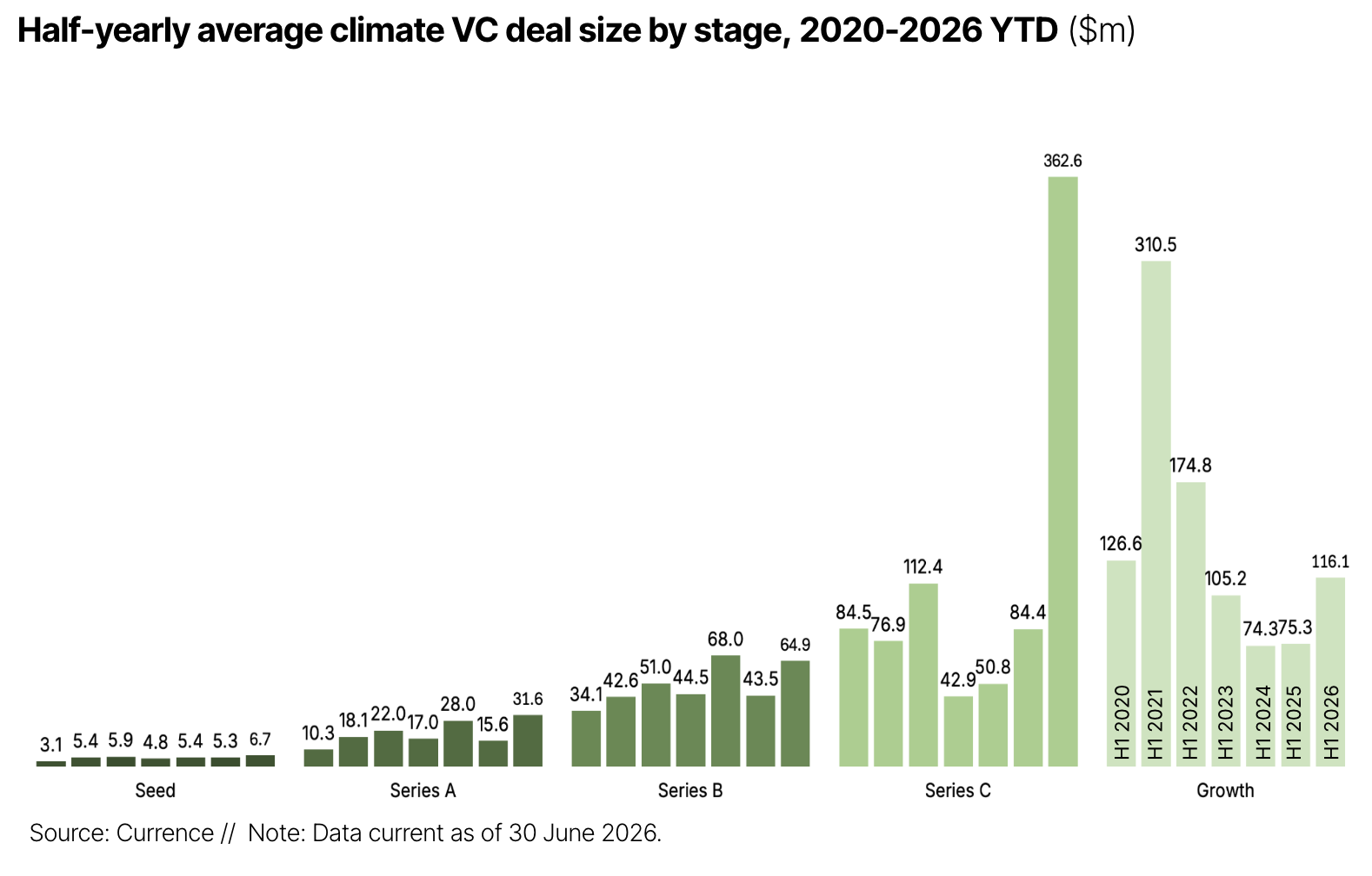

⚽ The rules of the game are changing at Series C. This typically lower count category had its biggest half on record, up nearly fourfold to $10.5bn, with VC starting to look a lot like infrastructure-level project finance.

⚽ Physical AI called a hydration break. AI models for use in the real world need real-world data, and investment has flooded into the startups collecting it. Earth Observation funding tripled as a route to real-time geospatial and historical data (also as physical climate risk increases). Additionally, training startups within robotics, including foundational models and data and simulations, have raised almost 4x the next largest sector.

And that's just the highlight reel! The full report has the complete breakdown on fundraising, stages, verticals, exits, and investor activity.

Currence clients can dig into the play-by-play commentary, including innovation trends, regional fundraising, notable exit breakdowns, and all the data directly on the platform here.

⚡ Proxima Fusion, a Munich, Germany-based developer of stellarator fusion energy systems, raised $470m in Series A funding from East X Ventures, XTX Ventures, Balderton Capital, Bayern Kapital, Brevan Howard, and other investors.

⚡ Quaise Energy, a Houston, TX-based developer of geothermal drilling technology, raised $134m in Series B funding from Prelude Ventures, Idemitsu Kosan, JERA, and Safar Partners.

🌾 Hippo Harvest, a Half Moon Bay, CA-based indoor farming operations and robotics developer, raised $30m in Series C funding from Cox Farms, Collaborative Fund, Congruent Ventures, Fresh Investment Club, and Hawthorne Food Ventures.

📦 Fleek, a London, England-based secondhand fashion platform, raised $25m in Series B funding from Burda Principal Investments, Andreessen Horowitz (a16z), ebay, FJ Labs, H14, and other investors.

⚡ Axle Energy, a London, England-based energy flexibility optimization platform, raised $25m in Series A funding from Energize Capital, Accel, Eka Ventures, and Picus Capital.

🏠 e-peas, a Mont-Saint-Guibert, Belgium-based developer of fabless semiconductors for low-power energy harvesting, raised $22m in Series A funding from Crédit Mutuel Innovation, SFPIM, European Innovation Council (EIC), Invest BW, KBC Focus Fund, and other investors.

⚡ Hephae Energy Technology, a Spring, TX-based geothermal drilling technology developer, raised $18m in Series A funding from Susquehanna Sustainable Investments (SSI), Underground Ventures, alfa8, Baruch Future Ventures, Centaurus Capital, and other investors.

⚡ Bohr Energie, a Toulouse, France-based renewable and storage asset aggregation and optimization platform, raised $11m in Series A funding from Suma Capital, AFI Ventures, Crédit Agricole, Founders Future, Grand Sud Ouest Capital (GSO Capital), and other investors.

🏠 Fuchs & Eule, a Potsdam, Germany-based energy efficiency consultancy, raised $11m in Series A funding from GET Fund, PI Impact, Picus Capital, Realyze Ventures, SET Ventures, and other investors.

🍎 Polysense, a Gent, Belgium-based AI-powered food quality control developer, raised $11m in Seed funding from Felix Capital, 100IN, Fortino Ventures, and Syndicate One.

🍓 Dogtooth Technologies, a Cambridge, England-based developer of autonomous robots for harvesting soft fruits, raised $6.2m in Seed funding from 24 Haymarket, ACF Investors, and EMV Capital.

🌾 Aardaia, a Wageningen, Netherlands-based developer of new protein crops from wild-species domestication, raised $5.7m in Seed funding from Point Nine, Astanor Ventures, FoodLabs, and Grey Silo Ventures.

💧 Porelio, a Berlin, Germany-based developer of materials for metal recovery and water treatment, raised $2.7m in Pre-seed funding from Faber, Better Ventures, Grupo Technologica, and Polytechnique Ventures.

🛵 Milo Drive, a Gurgaon, India-based EV mobility platform, raised $2.4m in Seed funding from Antler, Caret Capital, Alteria Capital, Aureolis Ventures, Climate Angels, and other investors.

⚡ Wildfire Energy, a Brisbane, Australia-based waste-to-energy technology developer, raised $1.4m in Seed funding from Climate Tech Partners, Airbus, and Qantas Group.

⚡ GIGA Storage, an Amsterdam, Netherlands-based large-scale energy storage operator, raised $513m in PF Debt from ABN AMRO, asr, Belfius, HCOB, ING, and other investors.

☀️ Avantus, a San Diego, CA-based solar IPP and battery storage developer, raised $263m in PF Debt from BBVA, CIBC, and Santander.

⚡ Opdenergy, a Madrid, Spain-based independent renewable energy producer, raised $57m in PF Debt funding from BNP Paribas, Instituto de Crédito Oficial (ICO), and Sumitomo Mitsui Banking Corporation (SMBC).

⚡ General Fusion, a Richmond, Canada-based magnetized target fusion developer, completed a SPAC merger with Spring Valley Acquisition Corp. at an implied valuation of $1.0bn.

🌱 IPoint, a Reutlingen, Germany-based product compliance and sustainability software platform, was acquired by Assent for an undisclosed amount.

⚡ 🔋 Harmony Energy, a Knaresborough, England-based BESS developer and operator, was acquired by Alpiq for an undisclosed amount.

⚡ Lemvig Biogas, a Lemvig, Denmark-based producer of biogas from agricultural and industrial waste, was acquired by BioticNRG for an undisclosed amount.

B Capital, a Manhattan Beach, CA-based multi-stage global investment firm, closed $500m at hard cap for Ascent Fund III, to back early-stage technology, healthcare, and energy companies across North America and Asia.

Climentum Capital, a Copenhagen, Denmark-based venture capital firm focused on European climate hard tech, closed $68m in a first close for Fund II.

This is a sample of deals available for Currence clients. Can’t get enough deals?

⚡ The UK government has extended the life of nuclear reactor Sizewell C, guaranteeing its electricity price at £70.50/MWh from 2035 to 2055 in final CfD terms. [Link]

With energy security and affordability top of mind, it makes sense to keep Sizewell B, which started in 1995 and supplies about 3% of UK electricity, around. And at £70/MWh, it’s below UK average day-ahead wholesale prices, which are currently high, around £81–105/MWh, after the Russia and Iran crises spiked gas prices.

🔌 Governors of 11 Western states formed the Western Transmission Expansion Coalition to coordinate permitting across the West. [Link]

The region has been the most exposed to the transmission bottleneck as solar and geothermal buildouts race grid capacity. Multi-state coordination on permitting is the piece that's been missing, bipartisan governor buy-in across 11 states is a rare political alignment.

☢️ Aalo Atomics became the fourth US microreactor startup to reach criticality under Trump's DOE pilot program. [Link]

Four criticalities in a year is a meaningful pace for a category that was regulatory-blocked six months ago. However, China is already finishing full commercial builds.

🌳 Amazon signed a 2m-ton nature-based carbon deal, one of the largest corporate NBS offtakes to date. [Link]

At ~$40m for 2m afforestation credits, the deal costs roughly the same as buying 80k tonnes of DAC at $500/ton - but that supply doesn’t exist yet. Still, it’s a low price anchor, and afforestation credits have a long track record of underdelivering on permanence.

📊 A new MIT/Columbia study found 74% of expected IRA-era clean energy capacity survives Trump-era rollbacks through 2035. [Link]

A nice reality check against the "IRA is dead" narrative. Solar, storage, and geothermal economics are strong enough that most projects are profitable without full tax credit stacks. The 26% that don’t survive are concentrated in offshore wind, green hydrogen, and some EV manufacturing.

☀️ Oman's United Solar closed a $1.6bn IFC financing package for what will be the largest polysilicon plant outside China. [Link]

🌬 The Netherlands connected its 760MW Hollandse Kust West VI offshore wind farm to the grid across 52 turbines. [Link]

⛽ Energy security concerns are driving a global biofuels boom. [Link]

💡 Generate Capital, CalSTRS, and the Rhodium Group published a "transition acceleration framework" offering a fresh lens for measuring energy transition progress beyond emissions alone. [Link]

📅 RE+ Mid-Atlantic 2026: Join industry professionals in the solar and energy storage industries from August 12th-13th in Philadelphia to explore business solutions, new technologies, and policy initiatives.

💡 Carbon to Value (C2V) Initiative: Apply by August 28th to be considered for Columbia's C2V climate venture program. Now on its sixth cohort, the program supports carbontech and connects them with corporates, governments, nonprofits, investors, and technical experts to explore how to move from promising technology to real-world commercialization.

💡 Exelon $20M Climate Initiative (2c2i): 2c2i supports innovative start-ups that catalyze solutions to climate change challenges while advancing social equality and economic prosperity. Selected Startups realize a number of benefits including; a $100,000+ equity investment from Exelon Foundation. Apply by September 28th.

📅 Yotta 2026: From September 28th–30th, at Caesars Forum in Las Vegas, network and learn at the biggest AI infrastructure conference of the year. With 6,000+ leaders across data centers, energy, compute, and capital, the conference is bringing industry leaders together to solve the cross-stack challenge of sustainable, scalable growth in the age of AI. Use code SIGHTLINE20 for 20% off passes

Senior Business Development Manager B2B Carbon Markets @Carbonfuture

Lead Data Analyst, Commercial Analytics @Octopus Energy UK

VP, Communications @XPrize

Finance & Ops AI Lead – Associate @Keyframe

Energy & Climate Policy Engagement Lead @Coreweave

📩 Feel free to send us deals, announcements, or anything else at [email protected]. Have a great week ahead!

Get our new report on offtake, with HSBC

Inside the $915m bet on carbon removal's next phase

Inside the $915m bet on carbon removal's next phase

Newsletter

Newsletter