🌎 CTVC’s guide to New York Climate Week ‘26 #307

We're bringing back the NYCW climate tech event tracker!

Inside the $915m bet on carbon removal's next phase

Happy Monday!

The corporate carbon removal market got a $915m vote of confidence, a new AI buyer, and a strategy refresh. We dive into Frontier’s new advance market commitment below.

In deals, $54m for AI-driven clean energy procurement and optimization in the US; $53m for residential rooftop solar installation in India; and $40m for AI-powered industrial certification in the UK.

In other news, DOE grants get reinstated, massive new geothermal lease sales, and a big CO2 battery project.

ICYMI, Sightline Climate, the market intelligence platform behind CTVC, is now Currence. Read the letter from our founders here. Nothing changes on your end — CTVC will keep landing in your inbox every week, in the same format, free as always.

Thanks for reading!

Not a subscriber yet?

📩 Submit deals and announcements for the newsletter at [email protected].

💼 Find or share roles on our job board here.

CTVC is powered by Currence, market intelligence to power the AI era.

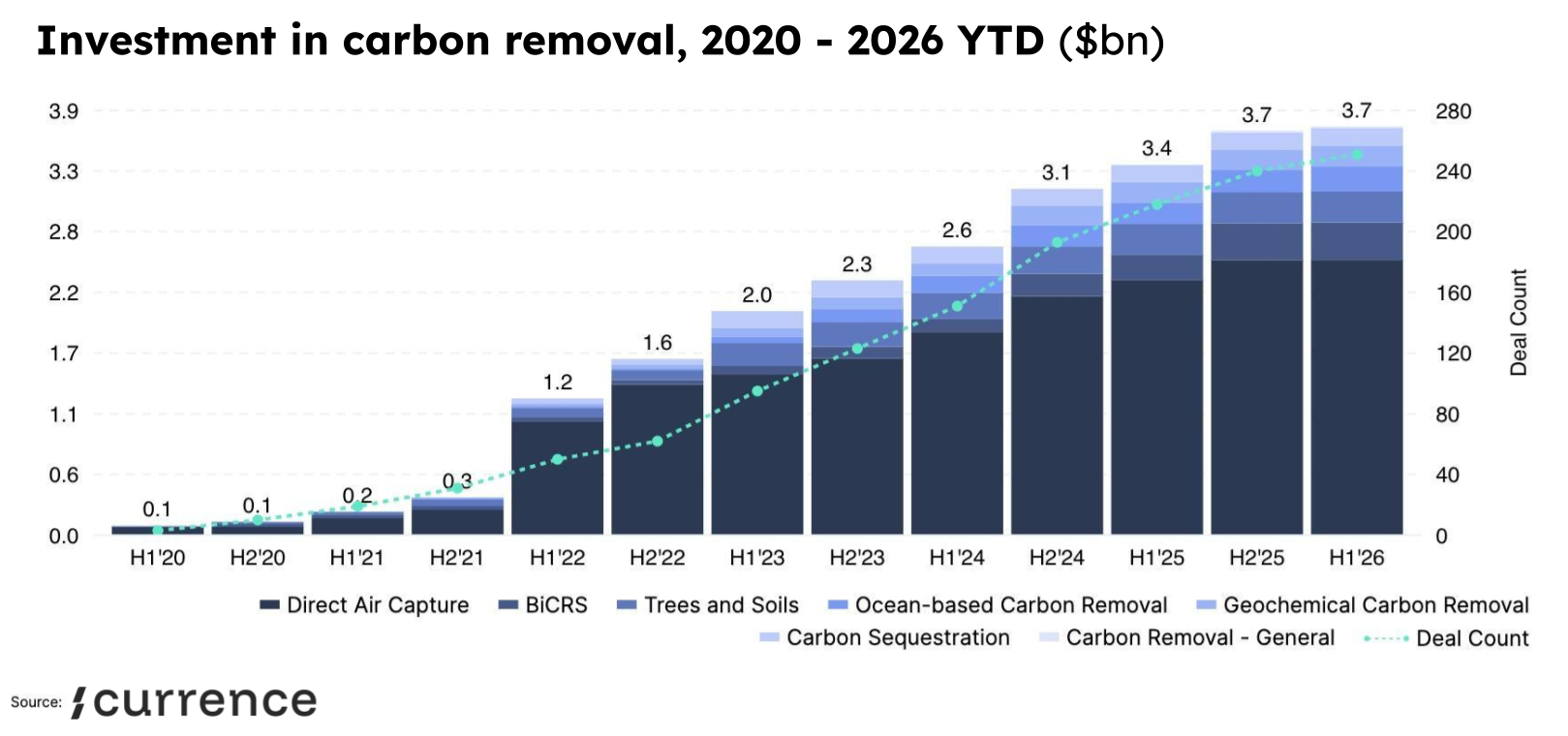

The buyers' club that kicked off the corporate carbon removal era just doubled down. Frontier, the advance market commitment that launched in 2022, announced $915m in new funds through a "Growth AMC" that shifts the coalition from seeding a wide field of startups to scaling a concentrated set of more mature ones.

Carbon removal could be back from the dead. It’s a crucial technology lever that can undo historic CO2 emissions rather than just mitigate new ones, pulling back toward pre-industrial levels, necessary for serious climate action. For corporates and governments, it's how net zero targets get met once the easy fixes are made, how hard-to-abate sectors offset emissions they can't yet eliminate, and how buyers answer growing skepticism of avoidance-based credits with something permanent and verifiable. It hinges on durability: storage that keeps carbon out of the system for good, and it's still proving it can deliver at scale and price.

The sector has faced some recent roadblocks, like reports that Microsoft, by far the largest buyer to date, at roughly 37m credits and about three-quarters of the market, was slowing its purchasing. Now, this fresh funding signals there's still appetite.

Frontier's original goal was to drum up demand in a market that didn't exist yet, getting corporates to pool their purchasing power to scale the nascent, still-expensive solutions faster. The sector has indeed grown since its launch; Currence’s tracking of investment in startups in the carbon removal space shows massive jumps right around 2022, and continued growth since. Still, the strategy shift is also an admission that to fully scale, government support is needed, whether from compliance markets, industrial regulation, or government procurement.

Frontier will favor jurisdictions where carbon removal policy has already passed or looks likely, read: the EU ETS. The EU's binding net 90% 2040 target took effect on 7 April, handing permanent removals a role in the ETS to offset hard-to-abate emissions. The rules won't be set until the ETS revision due in July, and removals likely won't count in the system until after 2030. It’s a welcome source of policy-mandated demand, especially as other corporate net-zero alliances have winded down (e.g. NZBI).

At the same time, other positive signals have emerged. SBTi just said companies will need to use removals to cover a small, rising share of residual emissions from 2035. JPMorgan and Charm Industrial struck a deal in which JPMorgan will buy 61,500 tons of removal credits and provide debt financing to support future production capacity, a structure that hands developers capital while locking in future buyer supply. Norway is consulting on a €1.7bn CDR fund. And Isometric, now the largest removal certifier by contracted volume at 16m+ tons, raised a $40m Series A to scale the AI-based verification that makes these credits bankable in the first place.

⚡ Verse, a San Francisco, CA-based AI-driven energy infrastructure platform for clean energy procurement and optimization, raised $54m in Series B funding from Bessemer Venture Partners, GV (Google Ventures), NVIDIA, and Norrsken VC.

☀️ SolarSquare Energy, a Mumbai, India-based residential rooftop solar installation platform, raised $53min Series C funding from B Capital Group, Elevation Capital, Good Capital, Lightspeed Venture Partners, Lowercarbon Capital, and Rainmatter Capital.

🌿 Isometric, a London, England-based AI-powered industrial certification platform, raised $40m in Series A funding from AVP, Lowercarbon Capital and Plural.

🏠 TAR, a Texas City, TX-based modular energy infrastructure developer for data centers, raised $27m in Seed funding from an undisclosed investor.

🏭 Foundation Alloy, a Cambridge, MA-based advanced alloys platform developer, raised $22m in Series A funding from Voyager Ventures, America's Frontier Fund (AFF), El Cap Holdings, Engine Ventures, Kanematsu Corporation, and other investors.

⚡ Critical Energy, a Hawthorne, CA-based low-cost geothermal power solutions developer, raised $19m in Seed funding from Susa Ventures, Upfront Ventures, Humba Ventures, MaC Venture Capital, Scribble Ventures, and other investors.

⚡ Kvasir Technologies, a Gladsaxe Municipality, Denmark-based marine e-fuel developer, raised $12m in Series A funding from European Energy, Export and Investment Fund of Denmark (EIFO), Maersk Growth, and The Footprint Firm.

🌾 Rainbow Crops, a Gent, Belgium-based advanced crop genetics developer, raised $11m in Seed funding from LIFTT, Agri Investment Fund (AIF), Corteva Catalyst,, Maia Ventures, PINC, and VIB.

⚡ Cypress Creek Energy, a Durham, NC-based solar and storage project developer, raised $1.8bn in PF Debt funding from Barclays, BNP Paribas, Santander, and Wells Fargo Bank.

🚗 Zenobe Energy, a London-based EV fleet and battery storage financing platform, raised $1.3bn in Debt funding from ABN AMRO, Aviva, Barclays, Bayerische Landesbank, Canadian Imperial Bank of Commerce (CIBC), and other investors.

⚡ DRI, an Amsterdam, Netherlands-based renewable energy developer, raised $127m in PF Debt funding from Erste Bank, PKO Bank Polski, and UniCredit Group.

🚗 JBM Ecolife, a Delhi, India-based electric mobility and bus deployment platform, raised $40m in Debt funding from Motilal Oswal Alternates (MO Alternates).

⚡ Axian Energy, an Andovoranto, Madagascar-based rural electrification solutions developer, raised $40m in Debt funding from Mauritius Commercial Bank Ltd.

⚡ Critical Energy, a Hawthorne, CA-based low-cost geothermal power solutions developer, raised $3m in Debt funding from Silicon Valley Bank.

💨 Seqana, a Berlin, Germany-based soil carbon MRV company, raised $1.8m in Debt funding from Rentenbank.

🔋 eMabler, a Helsinki, Finland-based open EV charging platform, raised $1.2m in Debt funding from Finnvera.

🥩 Nukoko, a Guildford, England-based cocoa-free chocolate alternative developer, was acquired by Dohler Group for an undisclosed amount.

☀️ SOL Components, a West Sacramento, CA-based solar mounting systems provider, was acquired by Create Energy for an undisclosed amount..

👕 Keel Labs, a Morrisville, NC-based seaweed-based materials developer, filed for Bankruptcy / Out of Business.

🥩 Swap Food, a Paris, France-based plant-based meat company, filed for Bankruptcy / Out of Business.

🌍 Desai Ventures, an Ahmedabad, India-based climate technology venture fund, launched an undisclosed amount for its Climate Fund II, targeting early-stage climate tech startups across the US, UK, and India.

This is a sample of deals available for Currence clients. Can’t get enough deals?

🏛️ A judge reinstated 11 DOE grants that the Trump administration cut over blue-state politics. [Link]

It reversed the October termination of 11 EERE awards in Connecticut, New York and Colorado, covering efficiency, critical-minerals reclamation, and solar and hydrogen, after recipients argued the cancellations were partisan retribution tied to states that backed Harris. There are still more than 300 other project grants that were terminated.

🔋 Energy Dome is building its second US project, a 19-MW, 10-hour CO2 battery in Arizona, on a 20-year tolling deal with Google cost-sharing the build. [Link]

It’s a meaningful step up in operational scale for long duration energy storage, and points to the future of the sector. Energy Dome's first US project in Wisconsin leaned on an OCED demonstration grant, while this one rides hyperscaler capital. Form Energy is on the same arc, OCED-backed then hyperscaler-pulled, as federal money dries up.

🌡️ The Bureau of Land Management held a massive geothermal lease sale in New Mexico, with winning bids for $16.6m for 158,000 acres. Pricing hit $108.82/ac on average (but winning bids varied by parcel), matching Utah's 2025 record. [Link]

All BLM sales since 2014 total at ~$38m, so this was close to half of all previous spend in one auction. Six brand-new LLCs took 60% of the acres (Novo Mesa, Rock Canyon, EDM Geothermal, Magdalena Energy, Entrada Energy, and EGX Energy, none of which have web presences nor prior BLM history). Established players like Ormat, Invenergy, and Zanskar also all showed up, indicating demand is growing.

💸 The Department of Interior will pay Invenergy $765m to surrender four more offshore wind leases. That brings the buyout total to more than $2.5bn, after earlier payouts to TotalEnergies and others. [Link]

The administration keeps its campaign against offshore wind going, despite losing appeals in court against projects and having a stated “all of the above” approach to energy. But it’s found more success going directly to the developers. Invenergy, a power developer, has agreed to steer funds into at least five new gas plants across Indiana, Wisconsin, Iowa, Kansas, and Missouri, plus geothermal out West for the first time. RWE, which paid $1.1bn for its NY/NJ lease, could be the next deal.

🏭 Australia opened its first carbon refinery to turn captured CO2 into concrete, paper, and glass. MCi Carbon's demonstration plant in Newcastle uses mineral carbonation to process CO2 from Orica's ammonia operations on Kooragang Island for 2,500 tons/year. [Link]

💡 NY Climate Exchange Climate Tech Fellowship: Applications are open for early-stage innovators at the intersection of energy and urban resilience. Join a six-month hybrid program that combines expert-led curriculum, 1:1 mentorship, non-dilutive funding, and access to The Exchange's global partner ecosystem. Deadline is August 1.

💡 Electrify Nevada, gener8tor's energy accelerator: Apply for the program for advanced energy, critical minerals, lithium loop, physical AI, and related deep tech startups to help with GTM for Nevada, one of the top energy states in the US. First review is June 30.

Senior Manager / Director, Communications @Carbon Removal Canada

Finance & Ops AI Lead – Associate @Keyframe

Software Engineer @Althea

📩 Feel free to send us deals, announcements, or anything else at [email protected]. Have a great week ahead!

We're bringing back the NYCW climate tech event tracker!

Newsletter

Newsletter