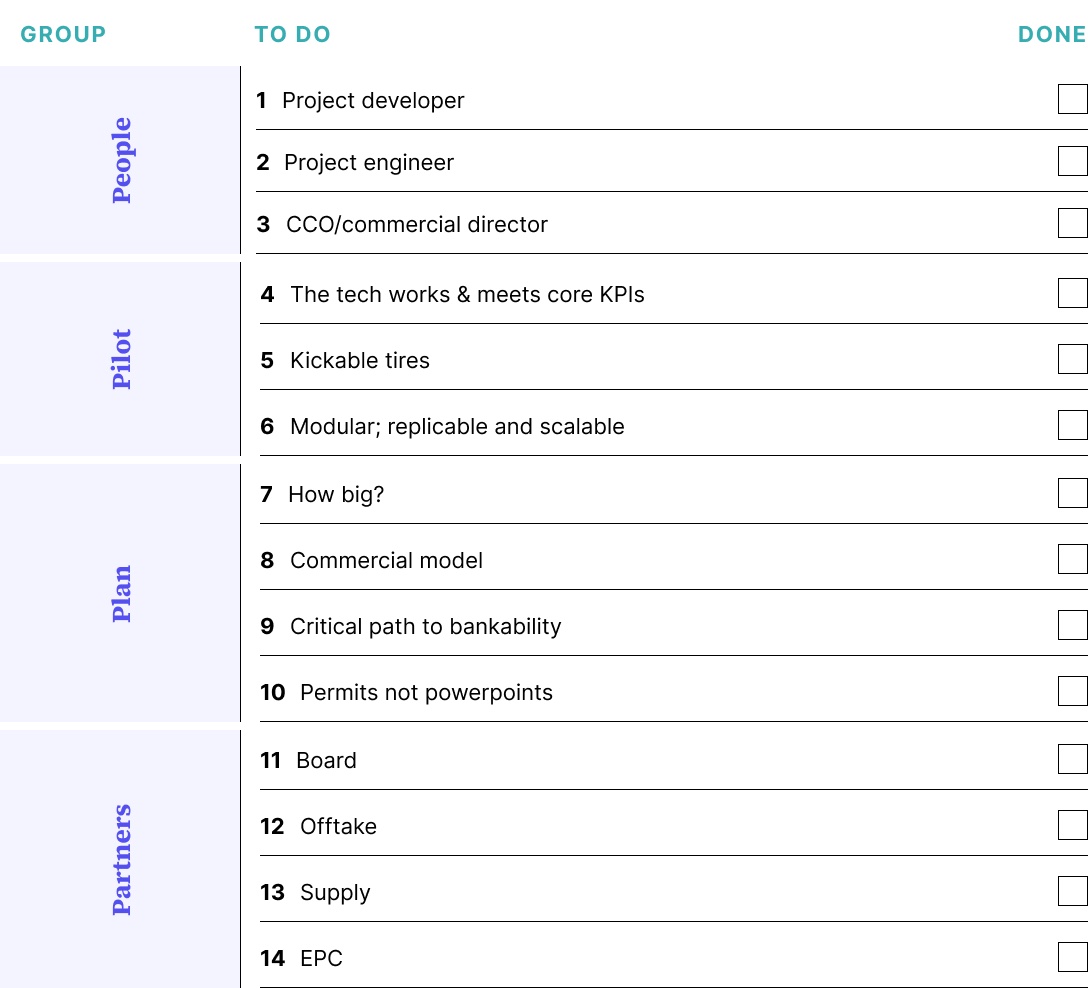

In this second feature in our First-of-a-kind (FOAK) series we’ve gone completely and unabashedly full framework to bring some structure to this adventure wonderland of finicky first projects. Porters Five Forces stand down, the FOAK Five Ps have arrived! As everyone will tell you, FOAK is hard. But rather than wax cynical about the chasm ahead, we’ll review what actions help aspiring Teslas put one foot in front of the next on the path to the promised land of bankability; people, pilots, plan, and partners, all tied together with a lot of persistence.

People – Meet the FOAKers

Planning and delivering a FOAK requires recruiting a purpose-built FOAK team. This team will have years of track record in developing, engineering, financing, and constructing projects that are often outside of venture’s and tech’s wheelhouse. While ideally new recruits would have already worked on a FOAK, that may be too much to ask. Instead ideal candidates will have completed several projects at name brand infrastructure firms like Avangrid, SunPower, Bechtel, or Macquarie. Ideally their prior experience will be in an area with similar dynamics, e.g. a Tellurian LNG alum if you’re in hydrogen, or a Baker Hughes O&G engineer if you’re in geothermal where skills translate well. And don’t be shy about recruiting from energy majors or SpaceX, Tesla, and other FOAK success stories. Leading FOAK growth companies like Fervo are stocked with ex-oil and gas veterans lending their skills to the energy transition. Recruiting your FOAK dream team not only brings in the necessary skills but also demonstrates that expertise to potential investors to build confidence. Key roles are:

Project manager / developer. They’ll be your internal founder and project CEO; they’ll find the site, and manage everything from permitting to key stakeholder relationships to locking down the offtake agreement. Their background is business not technical. They’re responsible for the project's strategy, fundraising and finances, development milestones, managing engineers, etc. They may have an MBA and spent some time in finance or at an investment bank.

Project engineer. They’ll be responsible for the engineering from design to construction. They’ll manage the FEED process, liaise with your OE (Owner's Engineer), EPC (Engineering, Procurement, and Construction), and someone else’s IE (Independent Engineer), and make sure your roadmap from the pilot to FOAK to full commercial is investment-grade. Background includes being an engineer building projects at blue chips like Fluor, Power Engineering, and Kiewit as well as operating companies too.

Commercial director/CCO. While initially it may be the project manager building commercial relationships, later on when it comes to negotiating the supply and offtake contracts it's important to have someone who’s been through relevant large long term contracting cycles before. They’ll be the one making sure the terms will meet PF investors expectations and checking the assumptions in your models pass the sniff test.

Pilots – Pre-flight training

Before taking on your FOAK you’ll likely have run a pilot if not pilots. Climeworks started with a lab project in 2012 capturing kgs of CO2, moving to tons in their 2017 pilot, then onto hundreds of tons in 2017, then up to thousands of tons with their Orca project in 2021, and are due to step up to the tens of thousands of tons with Mammoth this year. Ideally from your pilot/s you’ll be able to show:

The tech works. The three scariest words in project finance are “binary technology risk.” Does tech work or does it not? If there is a whiff that your tech is not ready, infra finance will flee. So your pilot/s’ job #1, 2, 3, and 4 is to demonstrate the de-risking of your tech in the field, not just in the lab. You may have specific KPIs that show you’re ready, these could be operational KPIs like running for x many hundred hours without issues, commercial KPIs like producing units at a certain rate and cost, or impact metrics like being able to show that your product leads to tangible emissions reductions, something that may be a prerequisite for some investors.

Kickable tires. The explicit role of your pilot is to demonstrate an operating project - your climate solution works in the real world under real world conditions. The expression, “you have to see it to believe it” applies doubly in infrastructure. Having a concrete project outside the lab at “clearly beyond lab scale” where your investors, strategics, and other partners can “kick the tires” and diligence is paramount. Climework’s $600M+ round was not won with powerpoint, white paper, or techno-economic model (though we are sure that they were great). Their series of working pilots won them their FOAK street cred. By the way, all investors like to play Bob the Builder and wear hard hats around construction sites :)

Modular. Startups often base their FOAK projects on the principle of modularity, but claiming scalability akin to "solar" isn't enough. True modularity, as deemed by project finance, implies that the engineering and design used in pilots will be replicated exactly in the FOAK. For example, a billion-dollar energy storage plant may use their pilot to test a single manufacturing line, then scale 50+ identical lines for the gigafactory FOAK. The startup mindset of “move fast and break things” doesn't apply here. If you have to iterate, you’ll need a bulletproof story for your investor’s engineers to explain your rationale for the change, how risks will be mitigated and managed, and what aspects of pilot performance are comparable to the FOAK, vs. where you're asking FOAK financiers to take a leap.

Plan – Looking for Goldilocks

Not only is FOAK planning a bigger exercise than earlier projects, but it’ll need to be written in a different language for a different audience. Check out our Venture to Project Finance Duolingo to learn more about code switching.

How big? The scale of your project should be ambitious yet realistic, striking a balance in the “Goldilocks zone”. Your project shouldn't be too big where there’s a “billion dollar capex” sticker shock or scale too fast to be probable (100x might be excessive). It should be substantial enough to validate your technology at a commercial level and provide a credible reference for larger commercial scale projects to follow.

Commercial model. What is the source of your cash flow? You need an offtake contract that uses realistic assumptions about supply chain and the offtake market and prices that shows a path to price parity or an acceptable green premium. It should give a PF a credible basis for believing your unit economics. What is the IRR (internal rate of return), MOIC (Multiple on Invested Capital), and DSCR (debt service coverage ratio)? They may expect a higher risk premium for being early in the asset class, so to make the numbers work you may need to get creative. Infinium, a SAF producer, managed to attract investment for their Project Roadrunner by partnering with American Airlines and Citi to fund the largest eSAF site in North America. As well as an offtake agreement with American Airlines, they arranged to transfer the associated emissions reductions to Citi to reduce their scope 3 emissions, enabling them to secure additional future revenue.

Critical path to bankability. From FOAK to nth. As well as outlining how you get to FOAK, you’ll also need to map out how you expect tech and engineering learning curves to affect your future commercials and unlock the path to bankability.

Permits not powerpoints. Do you know where you're going to build it? Have you engaged with the local community, started work on your FEED study, got the team in place and operational? You may not have been through permitting yet but you’ll know everything that needs to happen to break ground on your project - every permitting milestone and the associated level of spend and risk with each. When it comes to pitching for FOAK financing just ambitious ideas in a deck = a short meeting.

Partners – Anyone I’d know?

Investors are more comfortable coming to a party when they recognize and know the other guests (i.e. partners). Supply and offtake are the name of the game, but so is the creditworthiness of those partners so investors can have confidence that the project can meet its commitments ten years from now. Don’t underestimate the importance of your offtake partner’s financial strength, as well as the reputation of your EPC partner, even in early project stages like engineering design and feasibility studies.

Board. You’re going to need a bigger board. While your venture investors may be the biggest names in Silicon Valley, you’re not just playing in the valley anymore. Having names on your project sponsor list, cap table or advisory board that other infra investors recognize will not only give you a useful advisor but also breed confidence. Some names like Singapore’s GIC and Temasek, and strategics in general, can be well-regarded on both sides of the aisle.

Offtake. Securing a 20-year PPA (Power Purchase Agreement) with a Microsoft or SK Group might be ideal but not always feasible. Energy contracts are often long-term, unlike other decarbonization sectors like concrete or jet fuel. The key to success in offtake is securing long-term contracts with creditworthy buyers. But in sectors like concrete or jet fuel, there's a need for innovation in moving buyers from short-term merchant markets to longer-term contracts, and potentially leveraging newer financial mechanisms like Low Carbon Fuel Standards (LCFS), tax credits (e.g. 45X or Q), or carbon credits.

Supply. The yin to the offtake yang. Like you need a reliable buyer you need a reliable source too. Even if a feedstock is commoditized and easily purchasable on the market, the absence of a formal supply contract can still cause investors to be skittish. And, like with offtake, it needs to be with someone who can be trusted to still be around to fulfill the contract.

EPC. Working with an experienced EPC can also mitigate FOAK risk. The ideal scenario would be to secure a fixed-price full-wrap agreement with an EPC like Bechtel, who would guarantee the total cost of the project. But these are harder to come by, especially for FOAK projects. What’s more likely is a partial wrap, where the EPC assumes ownership for specific elements of the project. The more that’s covered, the lower the risk for investors and the more attractive the project opportunity.

Persistence - One does not simply walk into FOAK

Nothing to tick off here, other than the inevitable passage of time as weeks turn to months and on into years. Critical FOAK steps of project development, offtake negotiations, and government funding don't happen overnight. The course from path to pilot is a marathon, not a sprint, and will require patience, resilience, and persistence. But you’re not alone! There are many experts willing to advise and lament with you, and their first call might even be free.

This is Part II in our FOAK playbook series. In Part III we’ll be looking at the FOAK financing roadmap and the different routes for blending capital for FOAK funding.

David Yeh is a veteran climate investor with 20+ years in infra and VC and former White House and DOE official. He’s a climate OG focused on catalyzing FOAK financings for gigaton scale climate solutions.

Special thank you to Caroline McGeough, co-founder of Wavelength Infrastructure, for her preparation and partnership building this FOAK checklist.

Newsletter

Newsletter