🌎 H1'26 climate tech funding up 55% to $26bn, thanks to data centers

Our new report ft. low-carbon data center megadeals, reopened public markets, and rise of adaptation

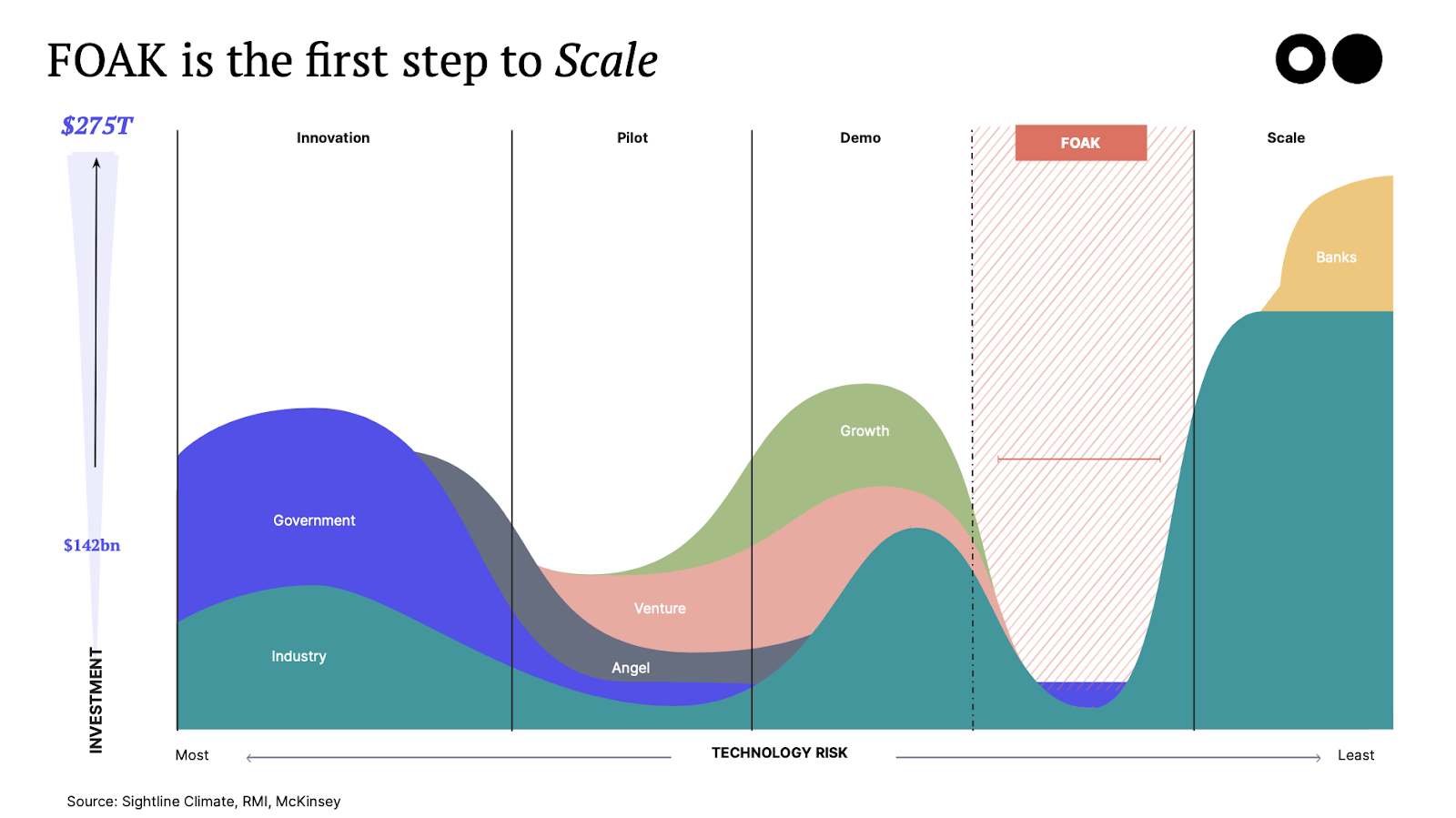

“Deploy, deploy, deploy” starts with building the first project or factory, or the first-of-a-kind (FOAK). Only after the launch of its first factory plant in Fremont (thanks to the DOE Loan Programs Office) did Tesla grow into the success story of Cleantech 1.0 and drive the shift towards full-electric transportation. But the first of anything is always the hardest, and a true net zero future will depend on a “Tesla” arising in every industry – from new clean ways of flying, generating power, or producing steel.

A FOAK project is the first step on the bridge to bankability, and getting to FOAK is as Darwinian as it is ambitious. Companies ready to cross the bridge will have already traversed several valleys of death, first proving their tech works in a lab, then progressing to pilots to demonstrate their technology can work in the real world. They’ll have raised tens, if not hundreds, of millions of venture, won customers and deals, and hired top talent. But it’s only at FOAK where the rubber really meets the road – where they’ll demonstrate the solution scales effectively and de-risk all of the commercial, operating, technical and even manufacturing risks that make them attractive to project financiers - before moving to second-of-a-kind projects then third, and eventually “Nth” where projects become repeatable and derisked (boring for VCs and entrepreneurs : ) which means bankable for project finance (PF).

We’ve written about the FOAK challenges companies face when scaling beyond the world of venture:

Today, more climate technologies are maturing, and we’re starting to see FOAKs in a variety of sectors, from sustainable aviation fuel to green steel (e.g. H2Green Steel’s $5B deal, Lanzajet’s Freedom Pines sustainable jet fuel plant, DOE’s DAC and green hydrogen hubs).

The problem is that while venture capital funds the lab and pilot stages, and project finance is available for commercial projects, FOAK falls in between, requiring infrastructure-scale sums of money with risk comparable to venture capital. This leaves these potentially pioneering projects in a finance “no man’s land”, straddling two adjacent asset classes with contrasting risk and return profiles.

Venture investors swing to hit home runs, where a few investments can return multiples of a fund. Project finance investors look for a high batting average –– no strikeouts in investments characterized by long-term stable cash flows from projects with de-risked technology and creditworthy commercial agreements, secured by assets. Financing FOAK is a brave new world, requiring a blend of VC and infra expertise, as well as philanthropic capital, grant funders, customers, and strategics.

Learning project finance lingo as companies plan the first commercial-scale, $100m+ facility is already too late. Talking the talk and walking the walk to get to FOAK takes years of putting steel in the ground, operating performing projects, and raising capital in a markedly different world than VC. Project financiers have their own distinct pattern recognition for what “good” looks like. Due diligence requires detailed review of long-term commercial agreements, credit quality of off takers, market studies, and EPC contracts to start. Debt-service coverage ratios (DSCRs) are more important than return multiples. VCs’ ears may perk up at “innovative” and “disruptive”, but “off-the-shelf” and “vanilla” are the preferred adjectives for PF.

Fluency in project finance takes years. But we’ve built a VC-to-PF Duolingo to get you started.

(Note: Both venture and project finance are incredibly nuanced in their own right, and the information below is for illustrative purposes only. For simplicity here we’re only addressing project finance debt, and ignoring project equity. Typically debt-equity ratio for project finance will be around 80% debt and 20% equity. FOAK terms will not be that generous in debt.

Looking for a dynamic project finance model to get you started? Check out Extantia’s FOAK Financing Toolbox here.

David Yeh is a veteran climate investor with 20+ years in infra and VC; and former White House and DOE official. He’s a climate OG focused on catalyzing FOAK financings for gigaton scale climate solutions.

And special shoutout to Guy Cohen for acting as lead venture to PF translator.

Our new report ft. low-carbon data center megadeals, reopened public markets, and rise of adaptation

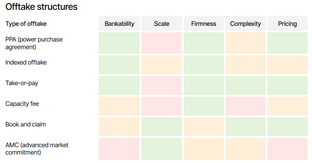

Get our new report on offtake, with HSBC

What happens when climate tech meets robotics

Newsletter

Newsletter