🌍 Rise of the robots, NY Tech Week edition

What happens when climate tech meets robotics

Broader, deeper curated support for climate tech capitalization

This climate tech moment is different from Cleantech 1.0 for a whole blog’s worth of reasons—from procurement and customer demand to aggressive policy to cheaper clean electrons. But perhaps the biggest departure from Cleantech 1.0’s days, when VCs alone pumped expensive equity into energy commodities businesses, is the depth and breadth of specialized climate tech capital support. Heck, the climate capital stack is different now from when we first named this newsletter.

For the past three years, we’ve tracked every dollar flowing from VC funds into climate tech companies. We’ve always acknowledged that venture is just one segment of the climate capital stack, and noted in previous posts that as startups scale toward building commercial facilities and physical infrastructure, VC backing becomes less and less feasible to fund the next steps of growth.

The best outcomes in climate tech happen when companies can align their development milestones with their capital strategy. While we're proud that our Running List of Climate VCs has supported founders in their fundraising, we’ve long been preaching that VC is a tiny part of the overall climate capital stack.

The last three years have included plenty of exciting announcements from both funds (see: our fresh dry power report) and startups about the resources earmarked for climate and the tech advancements that can help lower emissions and create more circular economies. But the valleys of death remain.

Fortunately, investors with deep pockets for growth and physical assets are starting to raise and deploy investment vehicles earmarked for climate:

As climate tech becomes more fully baked, so do the layers of capital sources. Think of pulling together these sources of capital as building a multi-layered cake—stacking VC rounds on top of government grants, then piling growth, debt, or project finance on top of that, to satisfy the capital requirements necessary for scale.

Case studies: Redwood Materials, a battery recycling company, started with early venture dollars in 2017, then layered on a strategic investment from Ford, a $2B conditional loan from DOE, and now a $1B Series D round with Goldman Sachs as the lead, culminating in ~$4B to help finance construction of a battery materials recycling plant in Nevada and a larger facility in South Carolina.

Across the Atlantic, H2 Green Steel has raised more than $5B in combined debt and equity since 2021 as it works toward building the world’s first large-scale green steel plant in Sweden. The ambitious hydrogen steelmaker recently closed a $1.5B round co-led by Altor, GIC, Hy24, and Just Climate—an example of new climate funds translating into real deployment capital.

The bridge to bankability won’t be built overnight, but it’s starting to take form as climate tech announcements from both companies and investors transition into action. Climate tech companies are entering a capital-intensive maturation period, and large funds announced over the last three years are beginning to cut big checks in climate tech.

This shift marks the capital stack moving later, and as such, we’re focusing not just on VC, but across the maturing layers of the climate capital stack necessary to scale climate tech projects and businesses. For more info on the early foundational slices of the climate capital layer cake, check out our steps for winning government grants, founder’s guide to DOE funding, and the pre-seed section of our climate capital stack breakdown.

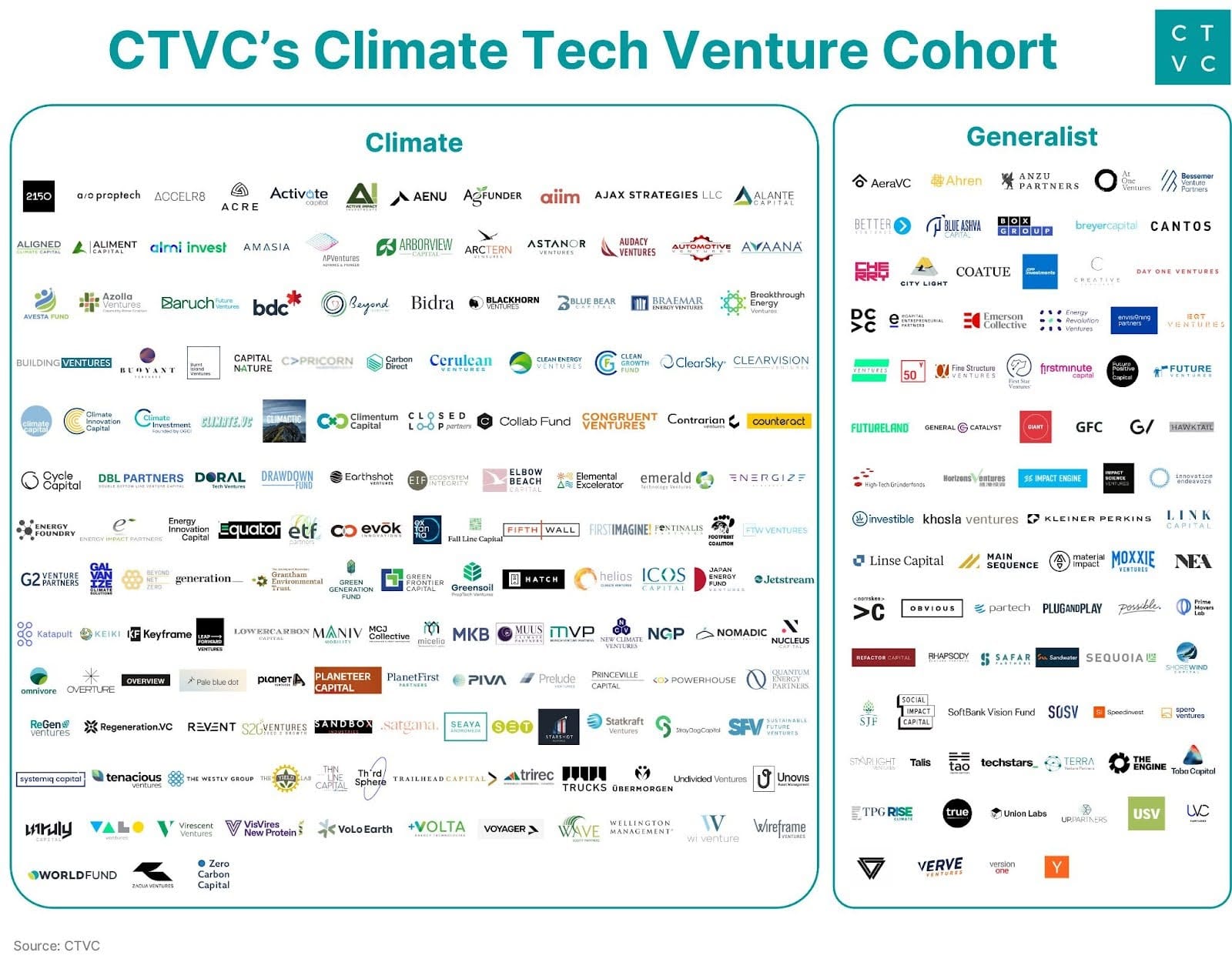

📢 We’ve given our existing climate investors list a big refresh! This is one of the most substantial updates since we first published our list of climate tech VCs in 2020. This revised list includes the latest climate investors from:

Venture Capital: Investing in early-stage companies

Corporate VCs: Venture arm or fund associated with a corporation

The list of climate investors that lives on our website here was created and maintained with the intention of being an open-source tool for climate-first founders and developers. We’ve updated it to included more categories of investors, sourcing funds through deal-by-deal tracking, as well as review of inbound submissions (which can be shared directly via this form). Transparently, our methodology is as follows:

Climate-specific: 75% (Note: we’ve consolidated legacy “vertical-specific climate funds” into this category)

General: 20% (Note: we’ve consolidated legacy “deeptech funds” into this category. Likewise, 20% is an increase up from 10% concentration in prior methodologies.)

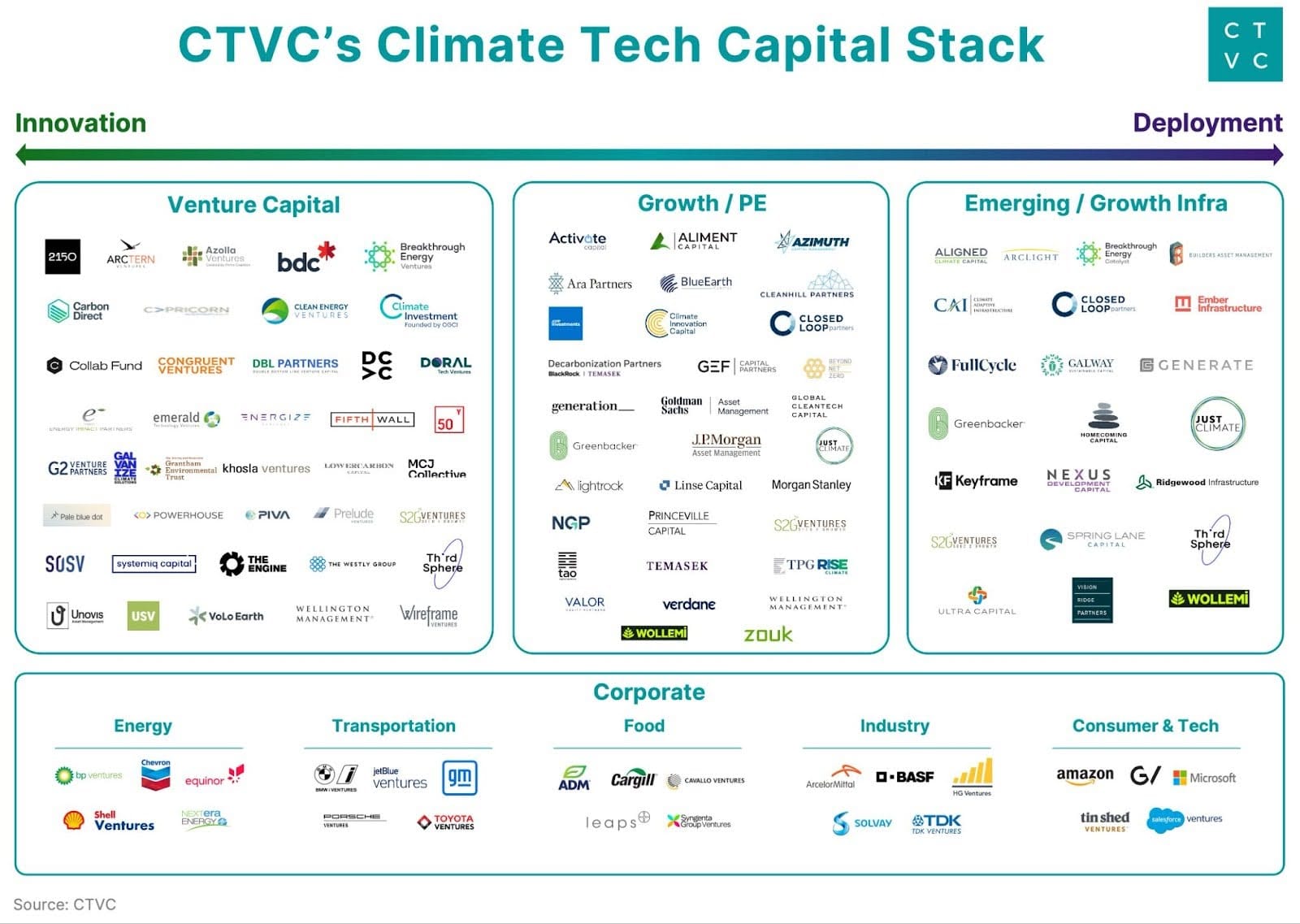

Translating ideas from the VC-funded innovation phase into capital-intensive, real-world undertakings, like building commercial facilities and energy infrastructure, requires a more creative and complex capital stack with bigger checks. This moves the conversation from VC-only into Growth, PE, and eventually Infra investors who can offer larger cash infusions and more intricate financing structures.

The investors in this section have varied priorities and preferences, but the labels and lines used to differentiate them are often blurry between categories. If the capital stack is a layered cake, investors can slice down vertically through the whole thing. We aimed to delineate them as clearly as possible here to give climate tech builders an understanding of capital allocators without splitting too many hairs on definitions.

The bottom line: What firms call themselves is less important than the types of investments they’re willing to make, and a few key questions can help founders and operators determine which investors could be a good match.

Growth: Capricorn Investment Group, Decarbonization Partners, General Atlantic BnZ, Generation, Global Cleantech Capital, Greenbacker Capital, Goldman Horizon Asset Management, JPMorgan Sustainable Growth Equity, Just Climate, Lightrock, Linse Capital, Morgan Stanley 1GT Fund, NGP Energy Capital, Princeville Climate, S2G Ventures, TPG Rise Climate, Verdane, Valor Equity Partners, Wellington Management, Wollemi Capital

PE: Ara Partners, Cleanhill Partners, GEF Capital Partners, Azimuth

Here’s a handy framework to break this out:

Investors: Aligned Climate Capital, Breakthrough Catalyst, Full Cycle, Greenbacker Capital, Homecoming Capital, Keyframe, S2G Ventures Special Opportunities, Spring Lane, Third Sphere, Ultra Capital, Wollemi Capital

Investors: Apollo Infrastructure, Builders Asset Management, CarVal, Climate Adaptive Infrastructure, Ember Infrastructure, Galway Sustainable Capital, Generate Capital, Just Climate, KKR Infrastructure, LS Power, Nexus Development Capital, Vision Ridge, Ridgewood Infrastructure, Riverstone, Stonepeak, Temasek, Zouk

Investors: Arclight, Hannon Armstrong, Brookfield Energy Transition, Global Infrastructure Partners, Macquarie, Copenhagen Infra, I Squared, EnCap, First Reserve, Equitix, EQT, JP Morgan Sustainable Infra, Antin, Energy Capital Partners, Ares Sustainable Infrastructure, Blackstone, OMERS, GIC, Starwood, Blackrock

Government: Financing climate tech projects through equity or debt with government funding or allocated capital.

Philanthropy / Catalytic Capital: Financing or enabling early climate tech projects with philanthropic dollars that seek a lower return on investment or concessionary capital.

Key players: Early Climate Infrastructure (Prime Coalition), Elemental Excelerator

Pension / Sovereign wealth funds: Asset owners managing billions of dollars (each!) that have already put some money into climate investment funds and are now beginning to enter the market as direct investors, often via climate-specific vehicles alongside their existing LP positions.

Key Players: Temasek, Canada Pension Plan Investment Board (CPPIB), Nysno, GIC, CalSTRS, NBIM

Corporates: Big players that can help finance or acquire facilities or projects from their own balance sheets (rather than through a Corporate VC). Oil and gas majors, real estate developers, and other incumbents in emissions-intensive industries are circling in on climate investments.

Key Players: Companies like Exor (a Dutch/Italian conglomerate/holding company), and strategics like Engie, Aramco, Shell, BP, Schneider, Enbridge, Borg Warner, Next Era and Kinder Morgan

There are a host of other players helping capital allocators to assess and de-risk climate tech projects, along with traditional lenders. (NOTE: We’ve purposefully put debt on hold for this feature, but keep an eye out for more soon on how debt fits into the climate capital stack.)

Banks: Provide debt and loans for climate tech companies and projects as well as advisory and syndication services to help companies raise capital and facilitate relationships with investors or acquirers.

Key Players: Bank of America, HSBC, JPMorgan, Citibank, SVB, Wells Fargo, Goldman Sachs

Insurance: Insurance providers lead the way for lenders in de-risking climate tech projects.

Key Players: MunichRE, Climate Risk Partners, New Energy Risk, Energetic Insurance, CAC Specialty, Resurety, kWH Analytics

We’ve endeavored to be comprehensive and transparent in open-sourcing this list as a public good, but please share your feedback about what may still need to be added. Send us a note at [email protected] with your take on the most useful ways to think about climate tech capital and use the button below to submit any investors we might have missed.

Stacking up the thanks to Natalie Volpe from Wollemi, Jason Scott from Spring Lane, Tim Latimer from Fervo, Ben Birnbaum and John Rapaport from Keyframe, Amanda Li from Banyan, and Janice Tran from Kanin Energy for sharing insights about how to categorize these new climate capital allocators. And shout out to John Tan for data support.

What happens when climate tech meets robotics

$90bn in climate dry powder in Q1 2026, after record fundraising in 2025

A breakdown of China’s new FYP and what it means for the next decade of the energy transition

Newsletter

Newsletter