🌍 Rise of the robots, NY Tech Week edition

What happens when climate tech meets robotics

Was the climate tech VC frenzy a peak or is it a wave?

As venture capital funding falls across the startup landscape, the dollars flowing into climate tech companies dropped ~40% in the first half of 2023.

Investors spent a lot of money in 2021 and 2022. With zero interest rate policy (ZIRP) days in the rearview mirror, deployments of real assets suddenly look real expensive again. Yet, dollars-and-cents demand from customers for better, faster, cheaper climate technology products only continues to grow—along with the talent flows, regulatory accelerants, and evolving capital stack.

If climate tech is truly a resilient trend, what’s going on with the current funding slump?

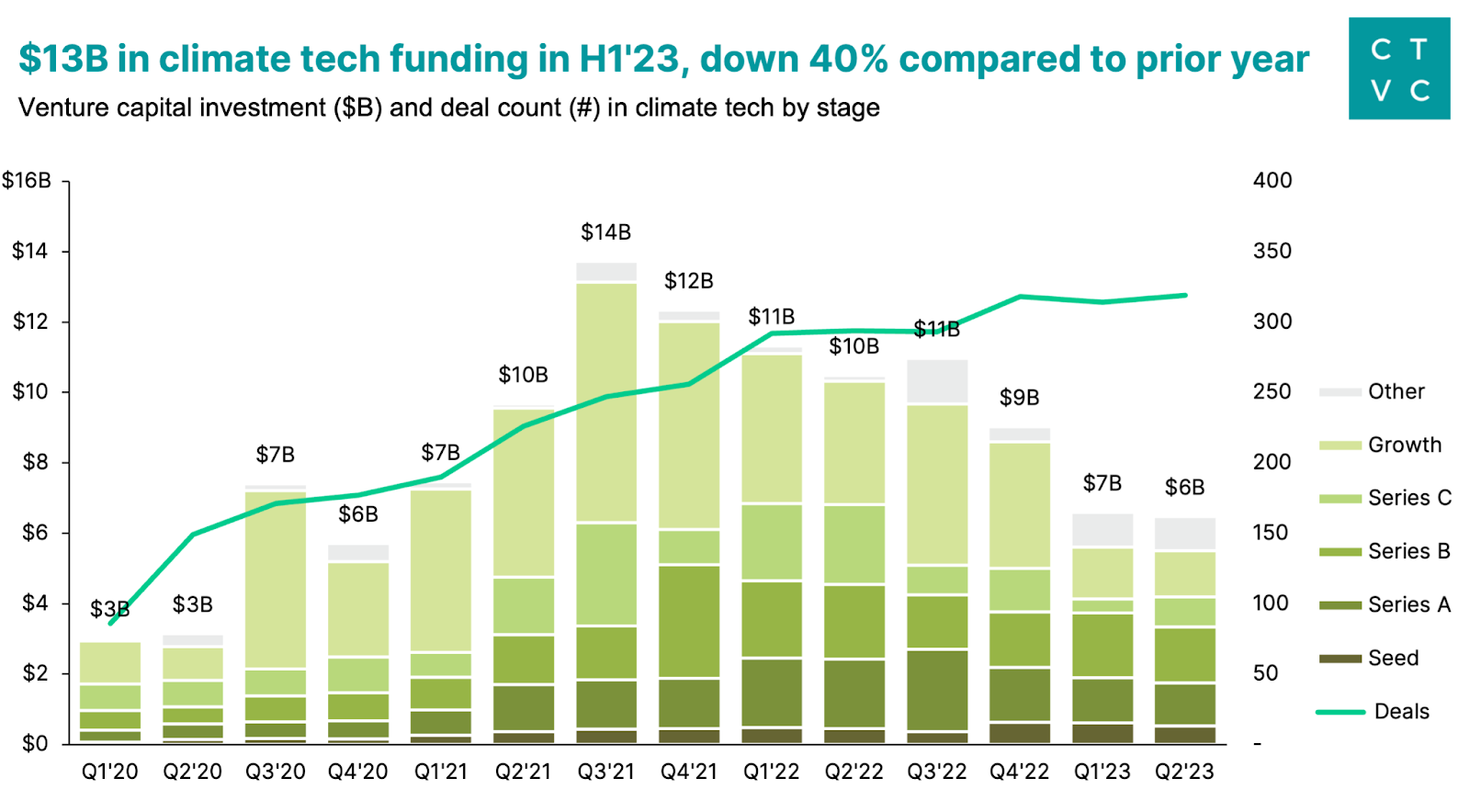

💰 H1’23 funding: Funding in the first six months of 2023 totaled $13.1B, down 40% from H1’22 and down 35% from H2’22.

🤝 Deal count: Overall deal activity increased, with deal count up 8% vs H1’ 22.

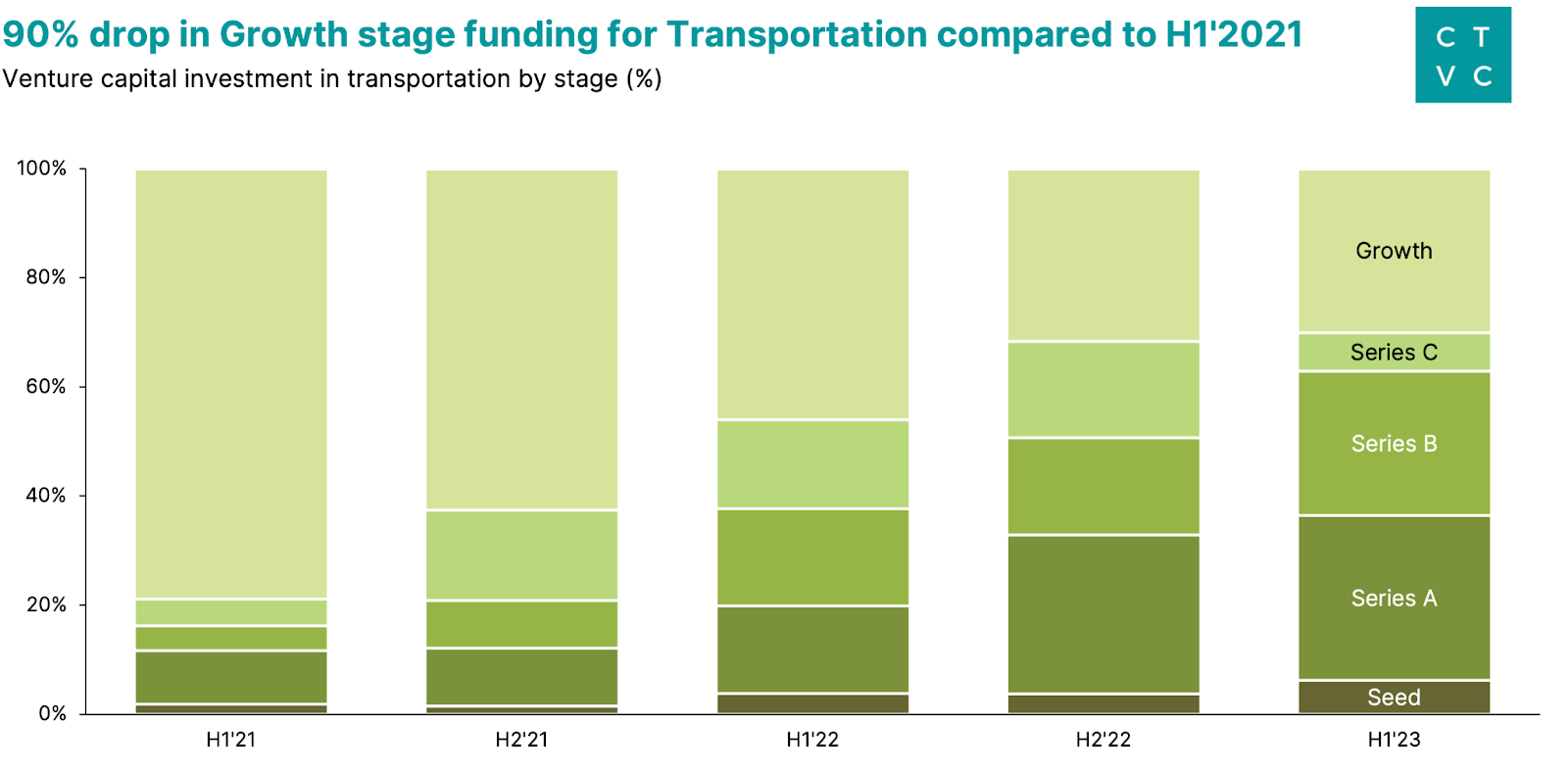

📉 Growth: Growth funding bore the brunt of the market contraction and plummeted 64%, while deal count dropped 43%.

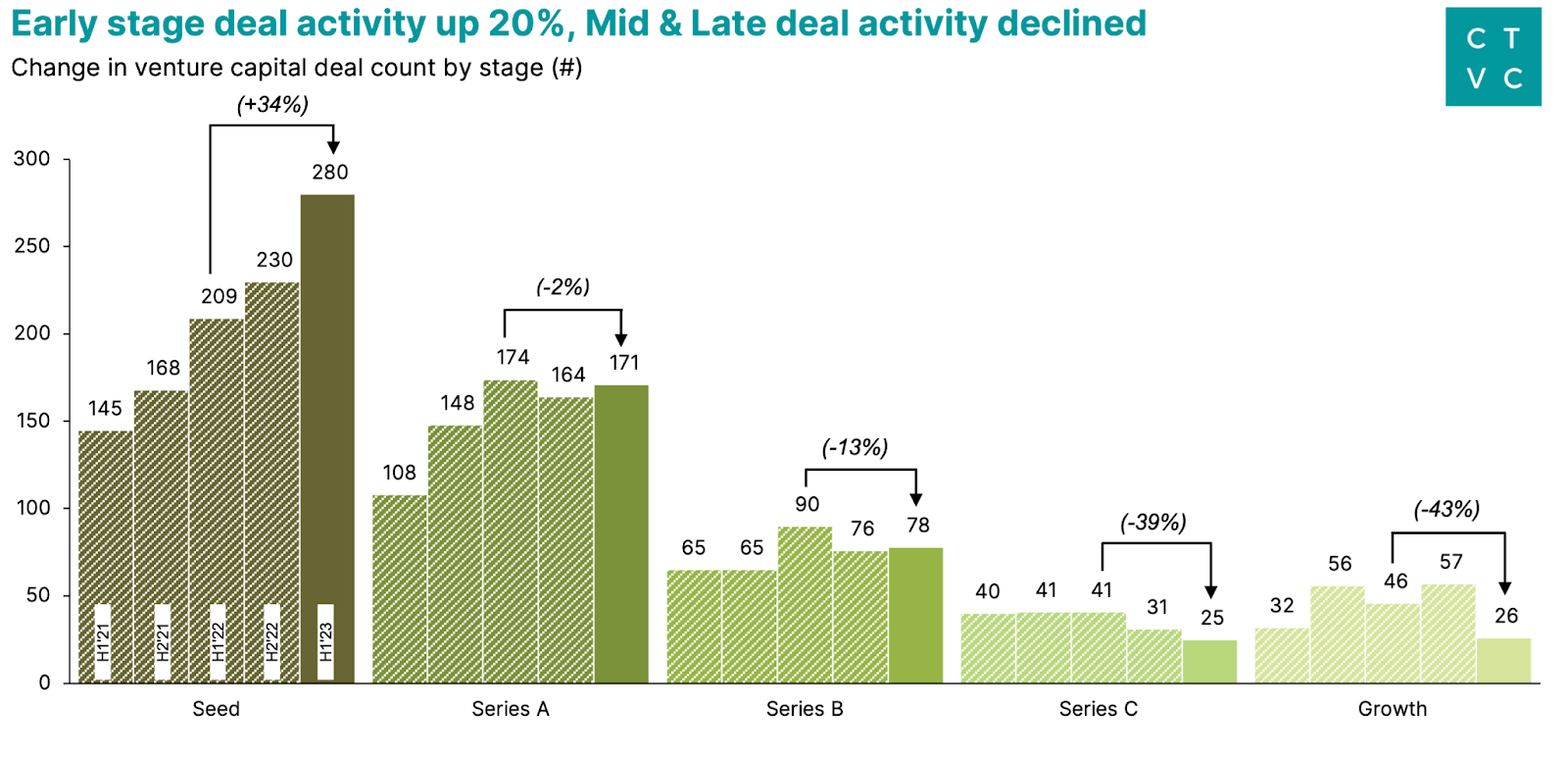

📈 Early: Breakout Seed funding grew 23% in H1’23 compared with H1’22, and Seed deal count increased 34% during the same period.

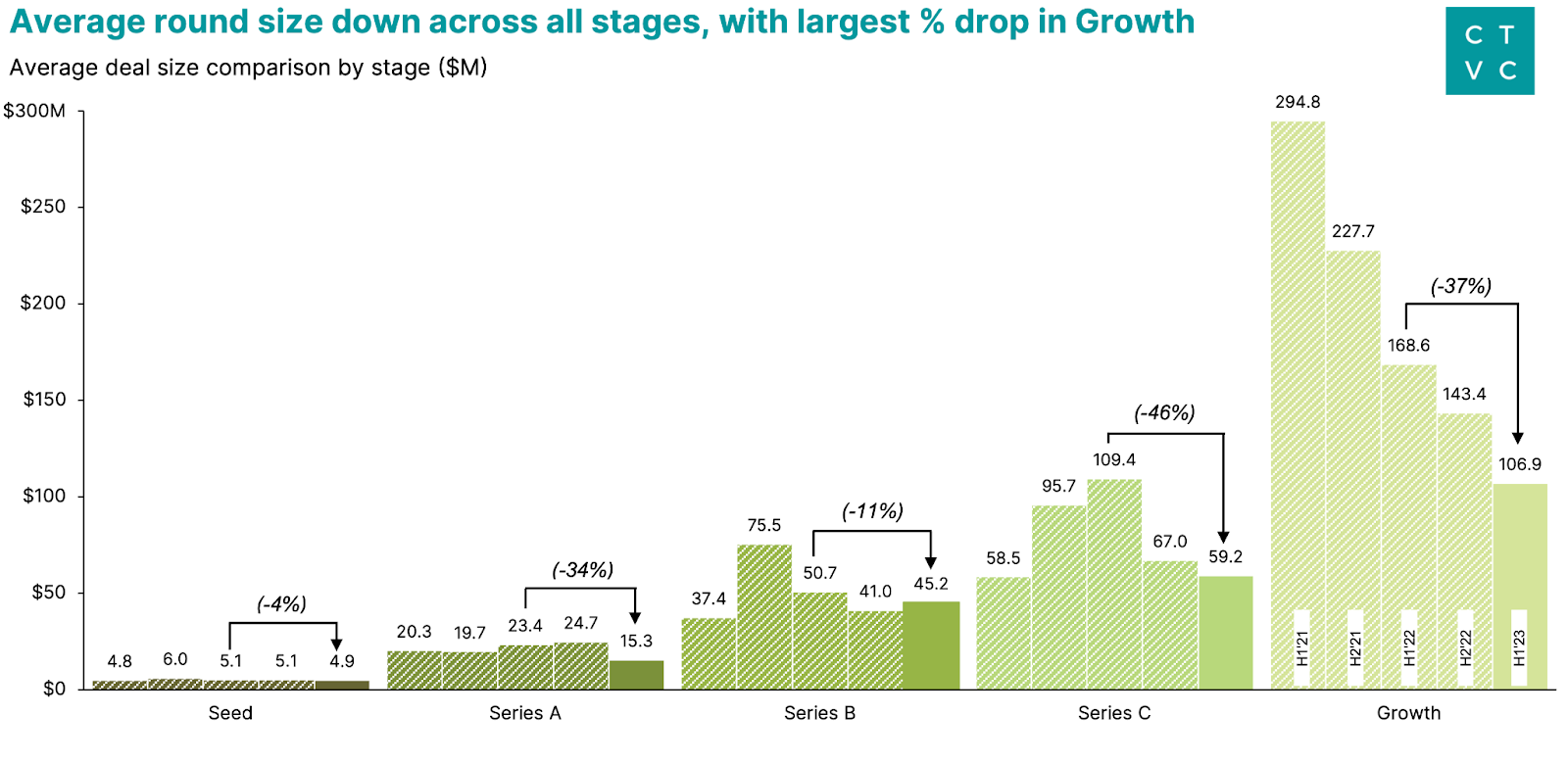

💸 Round size: Average deal size decreased 44%, with Growth rounds in particular down 37% on average. As total deal count actually rose in H1’23, all fingers point to the significant downsizing of rounds as the cause of the climate tech funding decline.

🚗 Vertical: Funding to Transport, Energy, and Food—the “Big Three” verticals—each dropped by ~50% compared to the prior year.

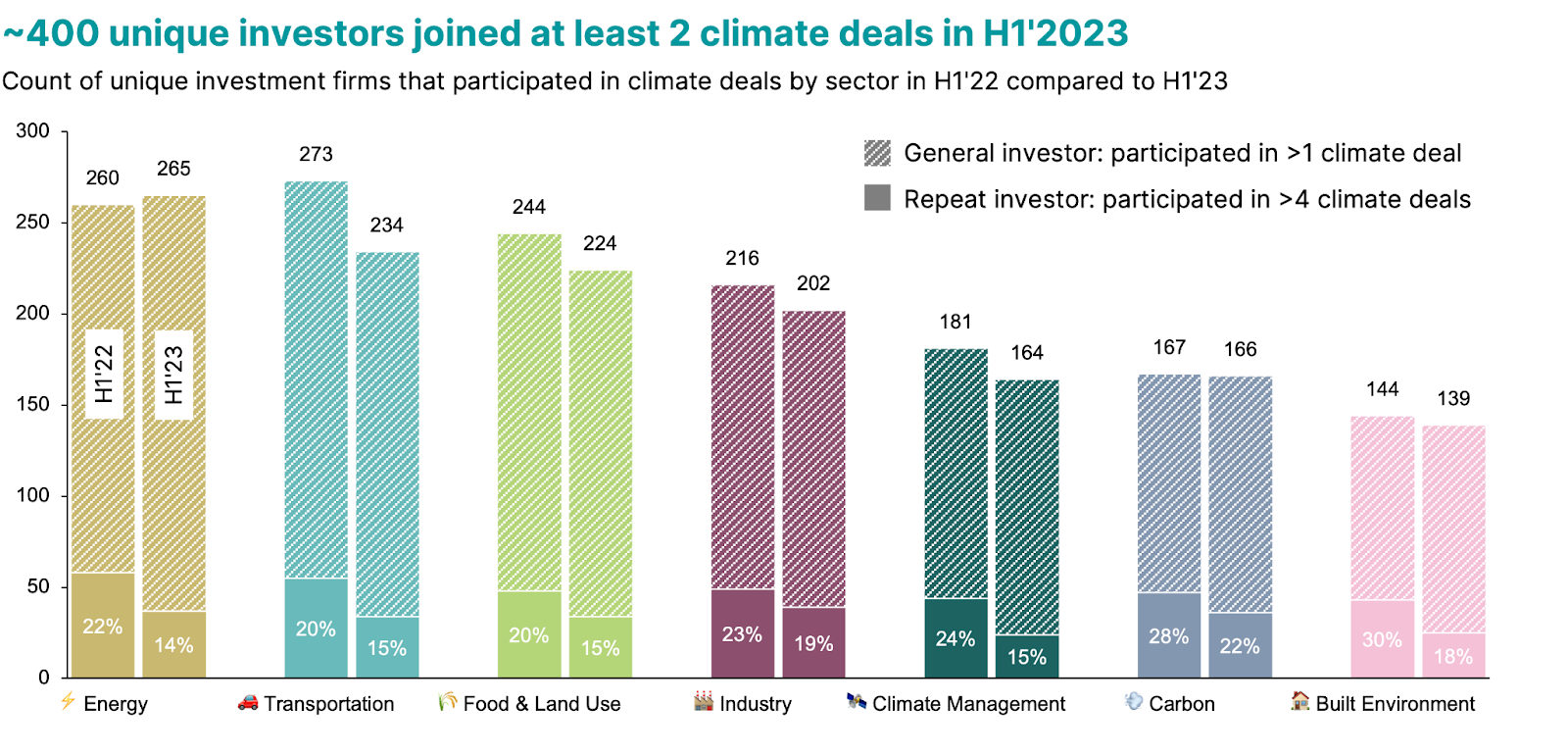

💤 Fewer repeat investors: The number of investors who have done 4+ climate deals in H1’23 slumped ~40% vs the same period last year.

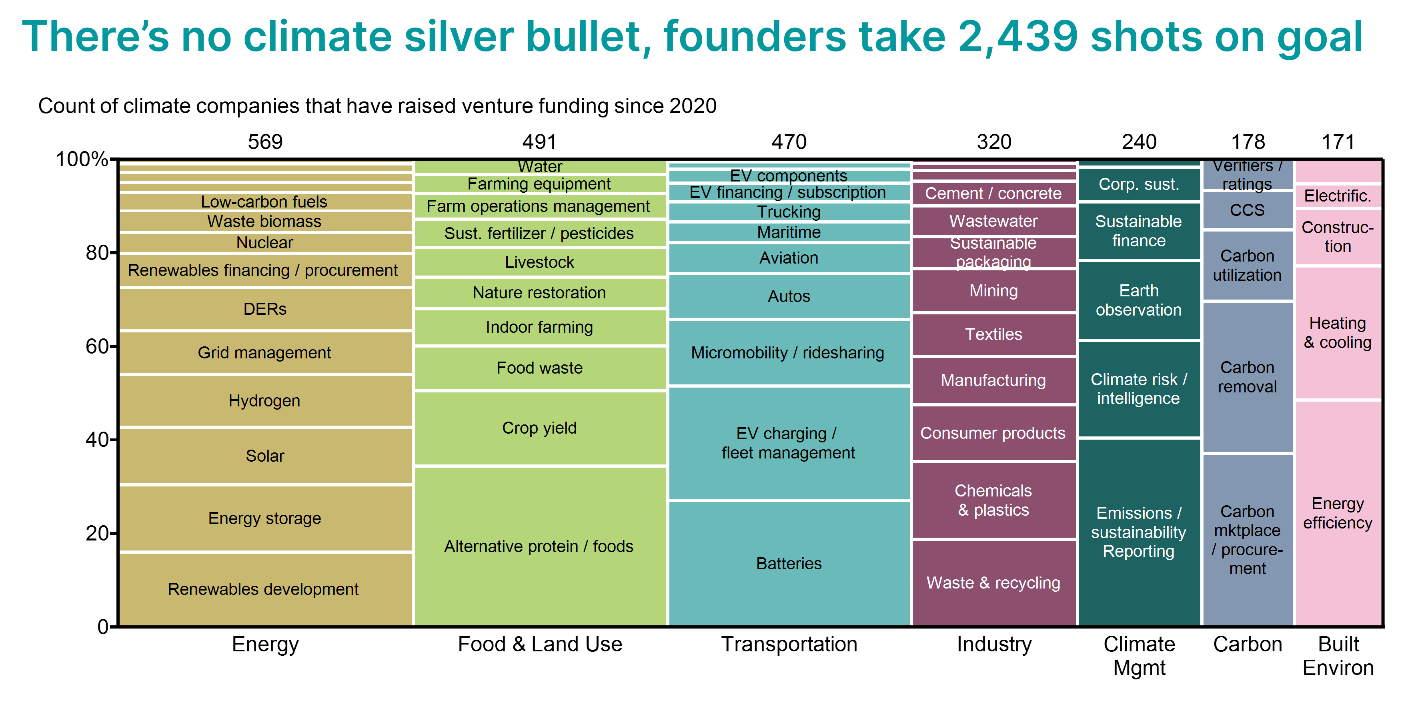

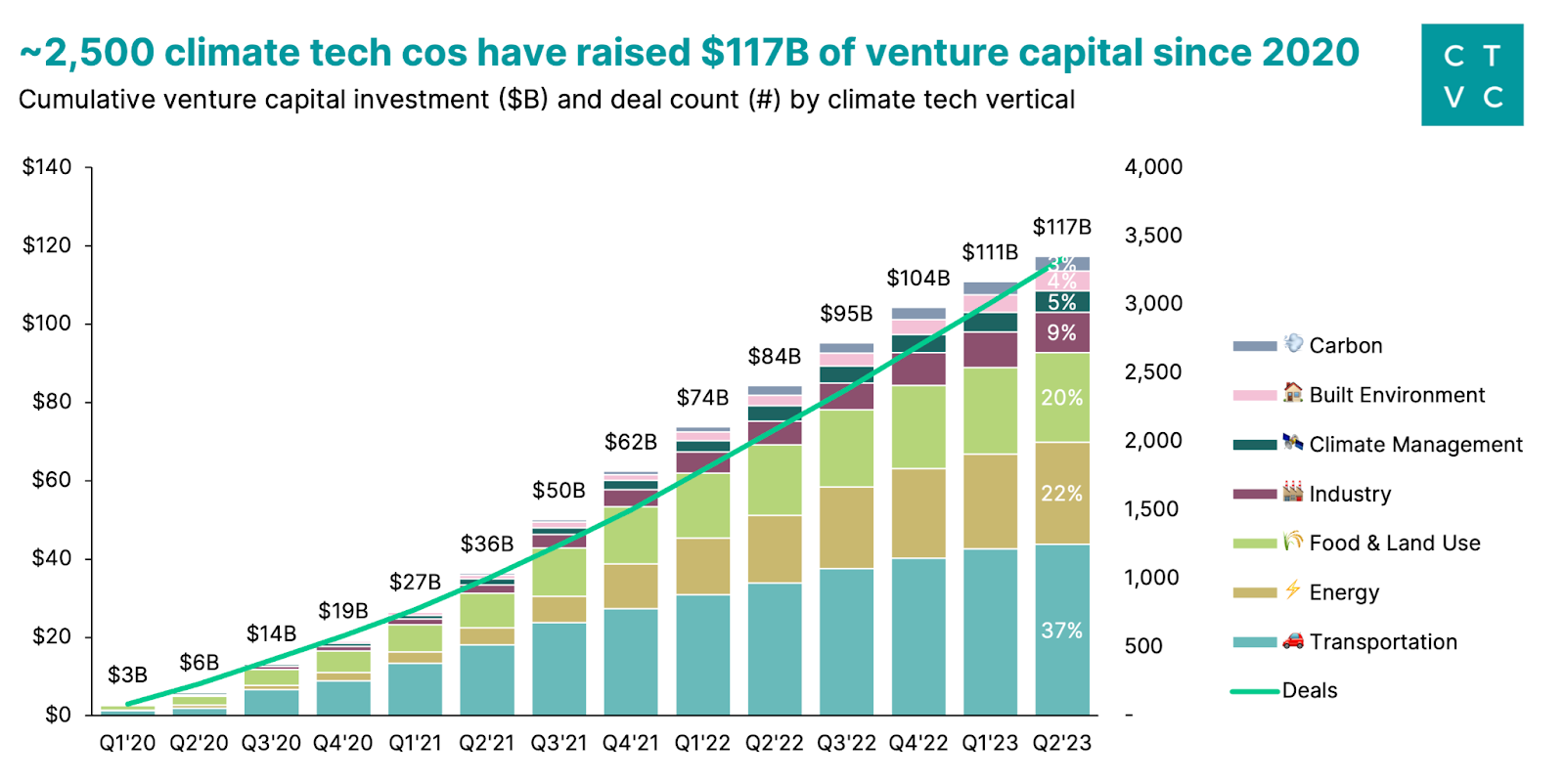

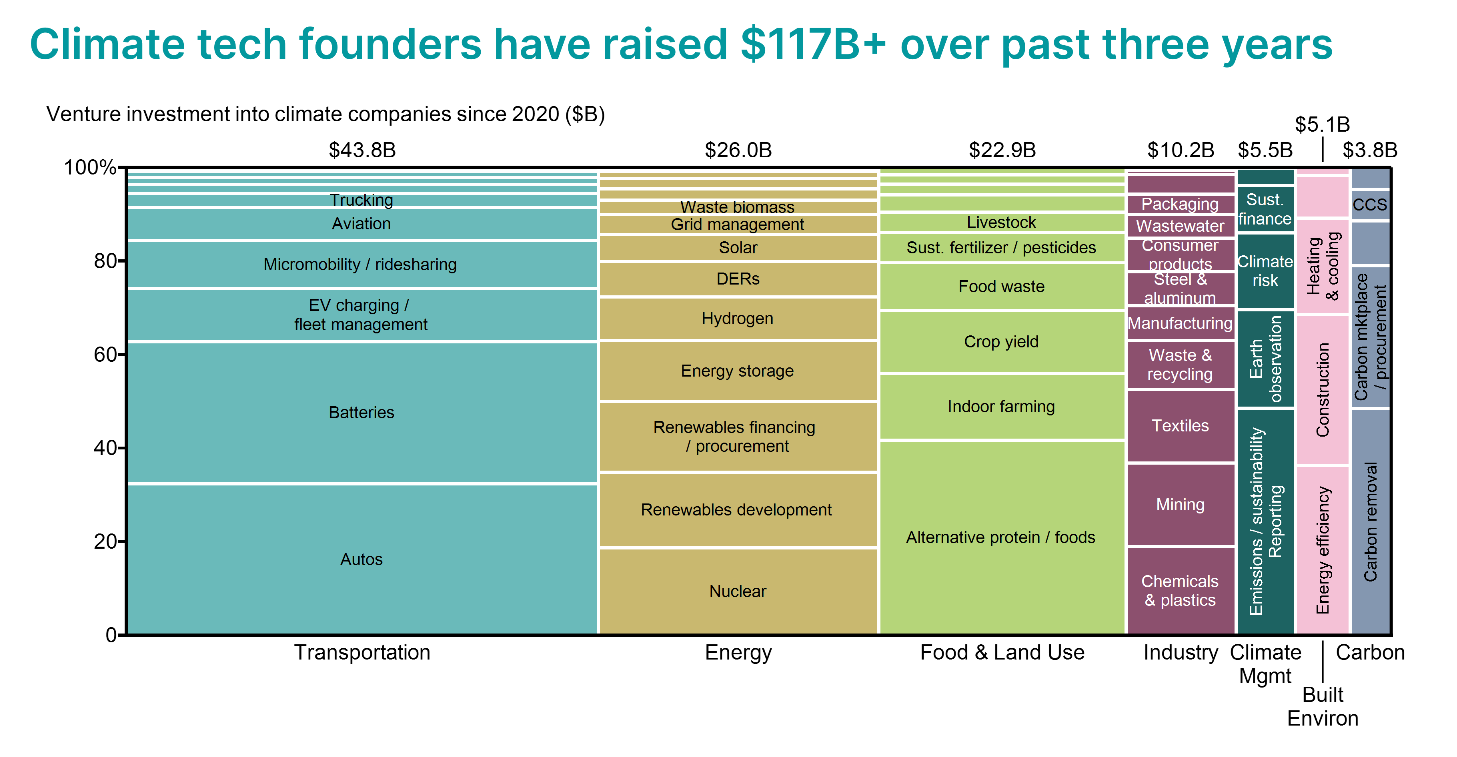

🎉 Cumulative: Since the start of 2020, ~2,500 climate tech cos have raised $117B+ of venture funding across 3,332 deals.

As the market freeze officially hits climate land, H1’23 marks the first time that quarterly funding has decreased over two consecutive quarters since the start of the climate tech boom in 2020. The decline should come as no surprise given the backdrop of the overall venture market, the telltale downtick in our 2022 funding report, and the sentiment from our investor pulse check (which astutely anticipated a 50% slowdown in deployment).

While a 40% funding drop is certainly not for the faint of heart, next quarter will tell the true story. Q3 consistently ranks as the top quarter for funding (as investors and founders return in a flurry from the summer lull).

The conventional wisdom that earlier-stage investments have been insulated from the public and growth market freezes seems even more true in climate tech. Early stages (Seed, Series A) fared better than Late stages (Series B, C) and Growth (Series D, Growth) in the first half of 2023.

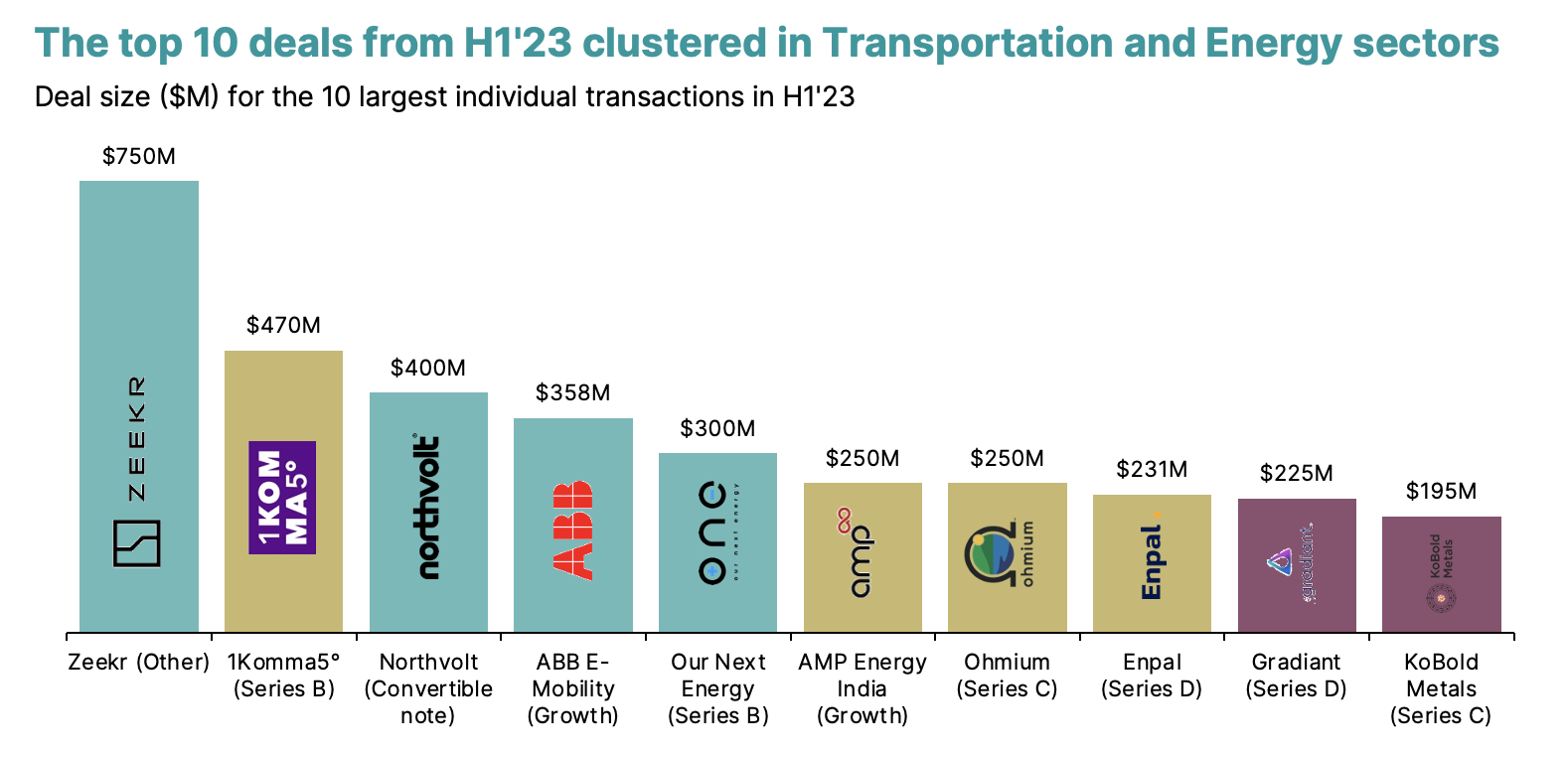

The overall funding drop owes largely to the “Big Three”: Transportation, Energy, and Food & Land Use. These have historically made up the lionshare of blockbuster rounds (e.g. Northvolt’s $2.7B, Rivian’s $2.5B, and Commonwealth’s $1.8B raises), and 80%+ of total funding for each of the previous three years.

Zooming out puts things into perspective. Since the start of 2020, ~2,500 climate tech companies have raised $117B of venture funding across 3,332 deals, with cumulative industry growth averaging ~30% each quarter. The relative slowdown brought the cumulative industry growth rate to 6% over the past two quarters—indicating a flattening of the curve rather than an all-out retreat.

The uptick in early-stage activity amid the larger downturn could be a sign of a wave of recalibrated investor interest, focused less on direct emissions-reduction tech and more on the enabling tech necessary to make those transitions work. Take Transportation as an example.

Autos alone account for 12% of total climate tech VC dollars tracked since 2020. Now that large automakers have started making big bets in EVs and battery manufacturing (just look at Ford/SK On), it’s unlikely that an upstart startup could outmaneuver their resources. In other words, the opportunity for the next Tesla has mostly played out. In response, investors are scouting further up and down the value chain for the next bottlenecks to unlock decarbonized transport. Backers of previous transportation mega-darlings, like Rivian and Quantumscape, have matured their sub-sector preferences from EVs and battery tech towards emerging tech enablers like mining efficiency, EV charging optimization, and fleet management—supported by policy tailwinds.

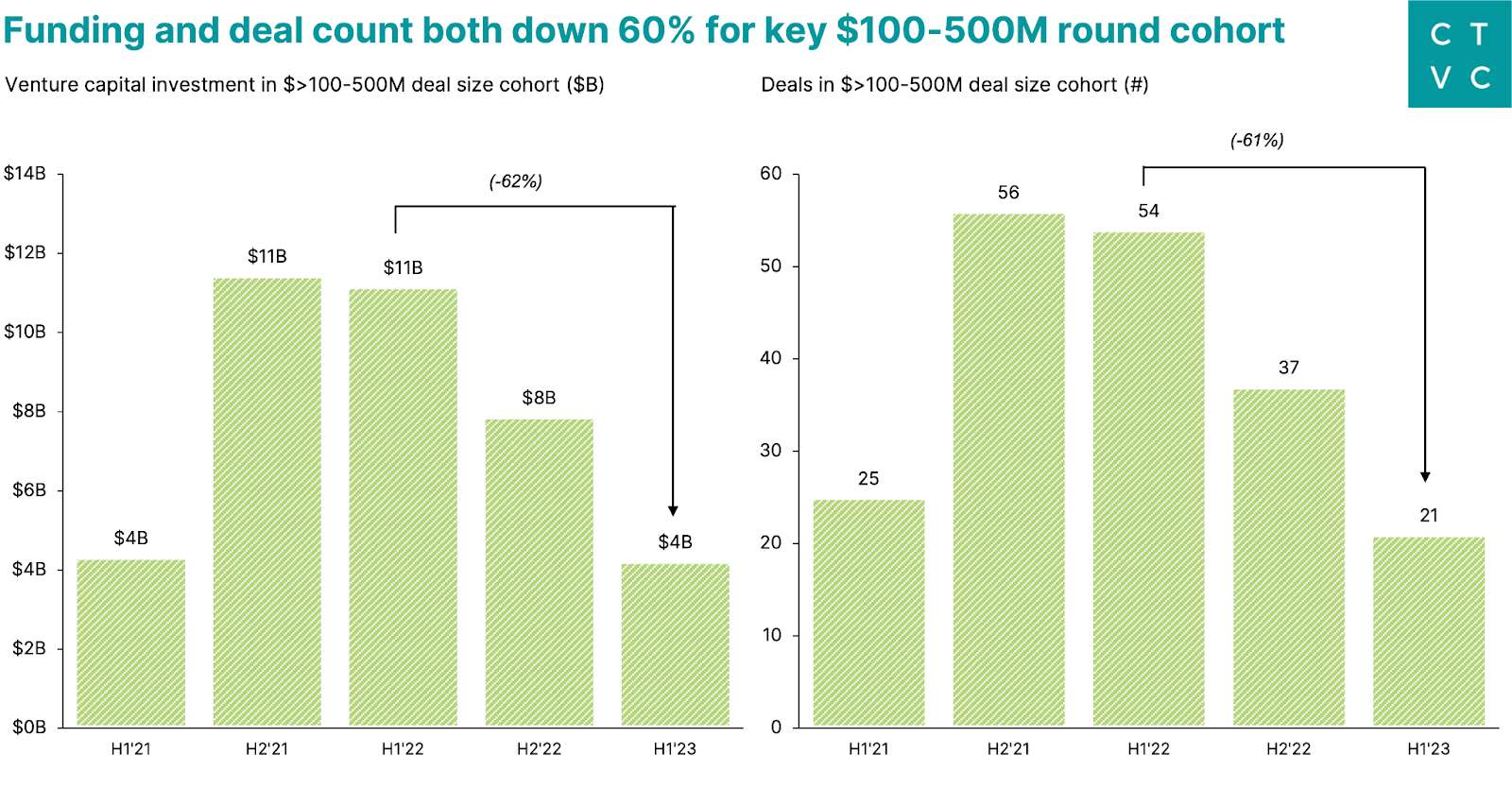

These $100-500M deals at the Series B+ stage typically happen when companies raise venture capital or growth funding for their first of a kind (FOAK) or demonstration scale facilities. This is the key valley of death for climate hardtech where tech readiness level (TRL) isn’t mature enough to raise non-dilutive project finance or debt but companies still need a significant pool of capital to prove their tech at scale. Often the riskiest stage for climate tech investors and startups alike, the market downturn appears to be steepening the valley in the near-term.

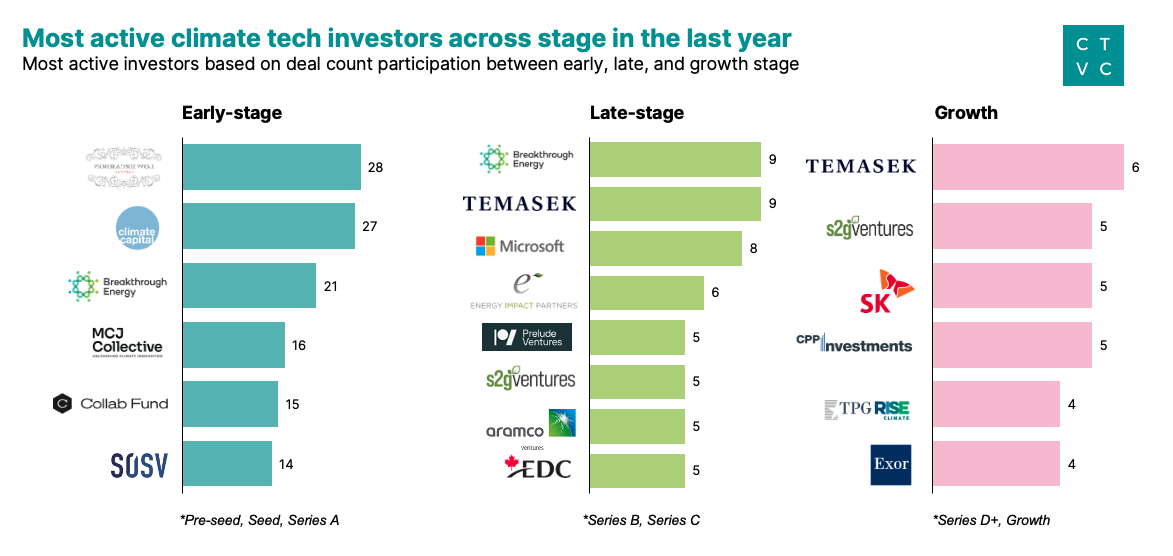

As the rate of capital deployment has slowed, many previously high-velocity investors are sitting it out and not doing as many climate deals. In H1’23 the most active investors included Breakthrough Energy Ventures, Lowercarbon Capital, Climate Capital, Temasek Holdings, Collaborative Fund, MCJ Collective, Energy Impact Partners, SOSV, Fifth Wall, and S2G Ventures.

Corporate participation in later-stage rounds sends a positive signal—a strong strategic partner committing to collaborate on a pilot project or act as a future supplier or offtaker can help lower the perceived risk profile for other investors, and catalyze the fundraising round. Anecdotally, strategics are increasingly being pulled into deals to “lead” for relatively small check sizes and attract additional investor interest. For example: Amogy’s $150M Series B funding led by SK Innovation, Boston Metal’s $120M Series C round led by ArcelorMittal, and EnergyX’s $40M Series B led by GM.

Asset class: This funding report captures only Venture Capital and Growth Equity deals that have been publicly announced through regulatory filings or press releases as of June 28, 2023. We also verified deals directly with the most active investors. Where other market observers may promote larger climate market sizes, we stay true to our Climate Tech VC name and carefully exclude:

We’ve long held that climate tech is a theme not an industry. Our definition of climate tech comes with two filters: 1) climate impact and 2) climate vertical. Companies must tick the box in at least one category for both filters in order to make the cut.

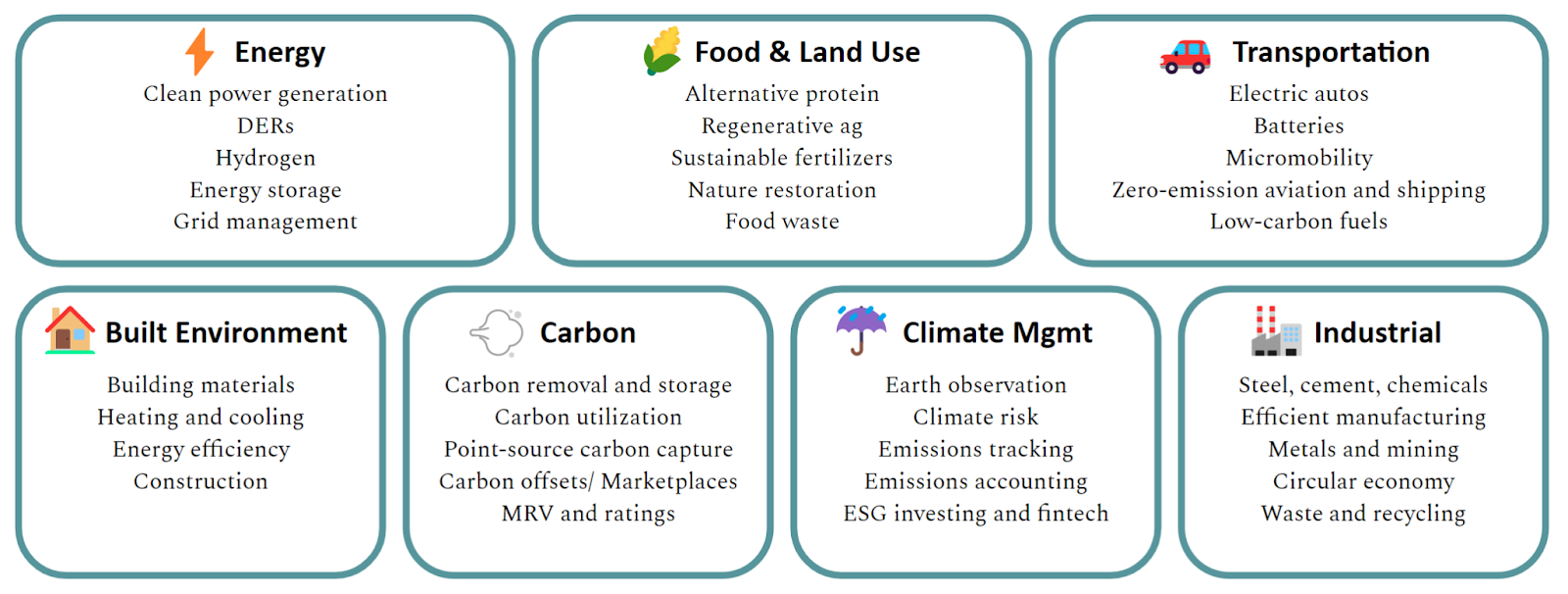

Climate Verticals: In addition to having climate impact, companies must fall into at least one of the seven broad climate verticals below. These verticals encompass 60+ sectors and 250+ technologies helping us mitigate, adapt, monitor, remove, and regenerate in our warmer and weirder world.

⚡ Energy - The electrons and fuel that power us

Sectors: new generation technologies (e.g., nuclear, solar, geothermal), energy storage, hydrogen and other low-carbon fuels, enabling renewables software, marketplace, and grid management platforms, DER and demand response tools, utility transmission and distribution services

🚗 Transportation - The movement of people and goods

Sectors: battery technologies, EV autos, EV charging and fleet management, electric micromobility and ridesharing, zero-emission planes, boats, and trains, urban public transport

🌾 Food & Land Use - The nutrients and resources that give us life

Sectors: alternative proteins, regenerative farming, vertical farming, sustainable fertilizer and animal feed, nature restoration and ecosystem services, remote sensing for crop yield optimization, autonomous farming equipment, water tech, and food waste reduction

🏭 Industry - The goods and raw materials we use every day

Sectors: low-carbon cement, chemical and plastics, steel, manufacturing, metals and mining, circular economy commerce, sustainable textiles and packaging, waste and recycling

🛰️ Climate Management - The data, intelligence, and risk associated with a changing climate

Sectors: emissions and sustainability reporting, earth observation through remote sensing, climate risk and intelligence platforms

🏠 Built Environment - The places we live and work

Sectors: sustainable building materials, low-carbon heating and cooling, prefab construction, energy efficiency, building electrification and energy optimization

💨 Carbon - The avoidance and removal of emitted carbon

Sectors: carbon offset marketplace and procurement platforms, carbon utilization, carbon removal and storage technologies, point-source CCS, verifiers and ratings enablers

***NOTE: You may notice that some of our numbers are larger in this update than previous editions. We constantly update the dataset to have the most accurate data possible, including adding post-dated deals.

Have a different take on what’s driving these climate tech investment trends? Or questions about our analysis? Drop us a note at [email protected] if you’re looking to dig deeper into the H1 2023 funding numbers.

What happens when climate tech meets robotics

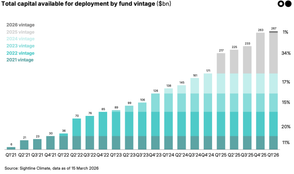

$90bn in climate dry powder in Q1 2026, after record fundraising in 2025

A breakdown of China’s new FYP and what it means for the next decade of the energy transition

Newsletter

Newsletter