Venture capital investment in climate tech may have dropped ~40% in the first half of this year amid the broader market slackening, but climate-focused funds have still been steadily stacking the green.

We’ve tracked more than 200 new climate investment funds since January 2021 that are creating fresh stockpiles of capital to deploy into growing companies and projects. Our count excludes investment vehicles announced prior to 2021 as well as generalist funds that are backing companies in this space. As such, our analysis of the available climate dry powder offers insight into the resources of climate-specific funds raised over the last ~3 years, rather than a comprehensive estimate of the total dollars ready to be put toward decarbonization.

Rallying LPs to raise a new fund takes time, and that means fund announcements are a lagging indicator of interest in the market. The 2023 dry powder numbers illustrate a cool-off from the height of the zero interest rate policy (ZIRP) craze, but there’s still a lot of new money headed toward climate investments.

Highlights

There's $121B of total private climate assets under management (AUM) across 207 new VC, Corporate VC, Growth, Infra, and Private Equity funds since Jan 2021.

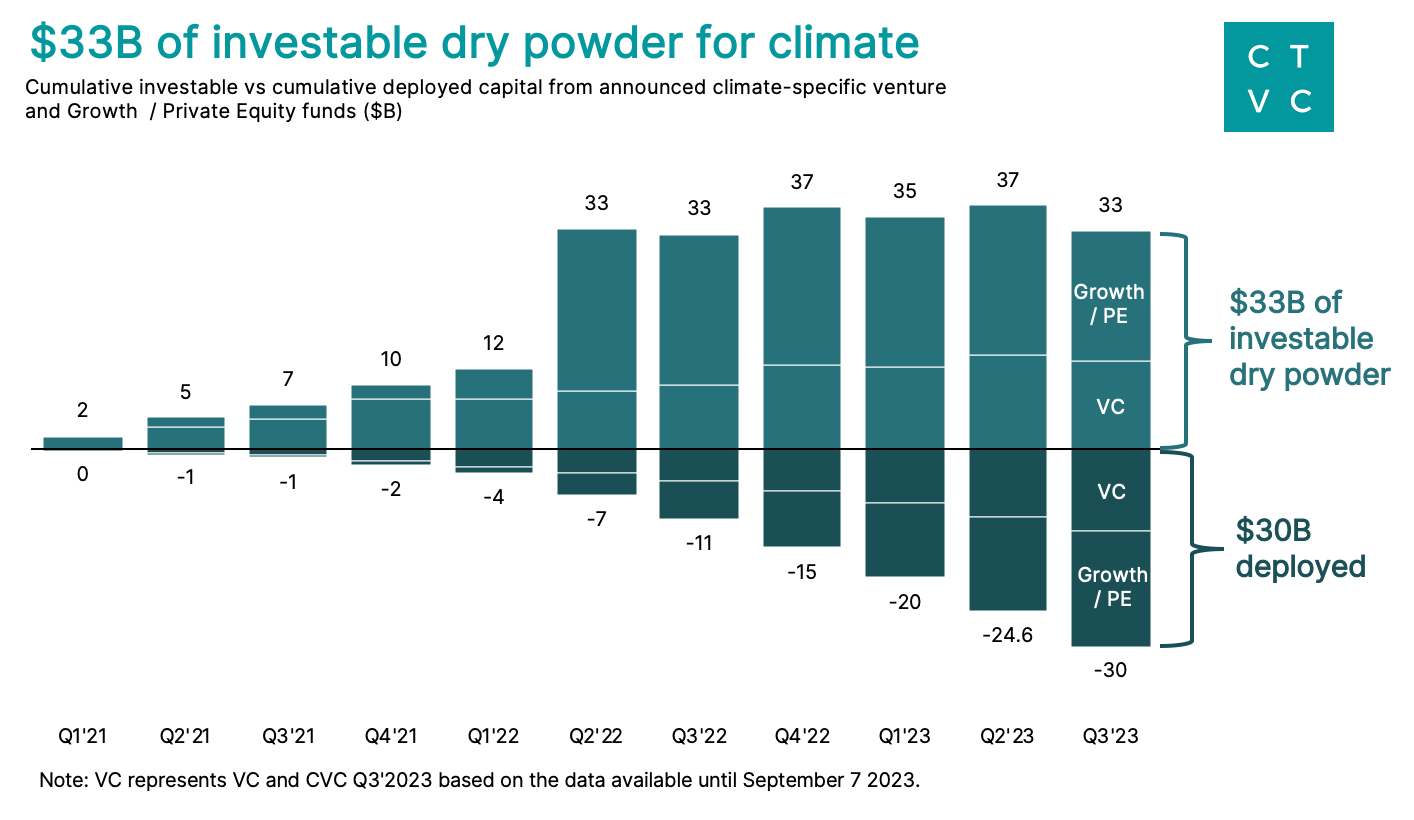

Following some standard deployment assumptions, we expect that $30B from these VC and Growth / PE funds has been plowed into climate companies already. After excluding Infra funds ($34B) and removing management fees ($24B), that means there’s $33B of investable dry powder ready to deploy in climate.

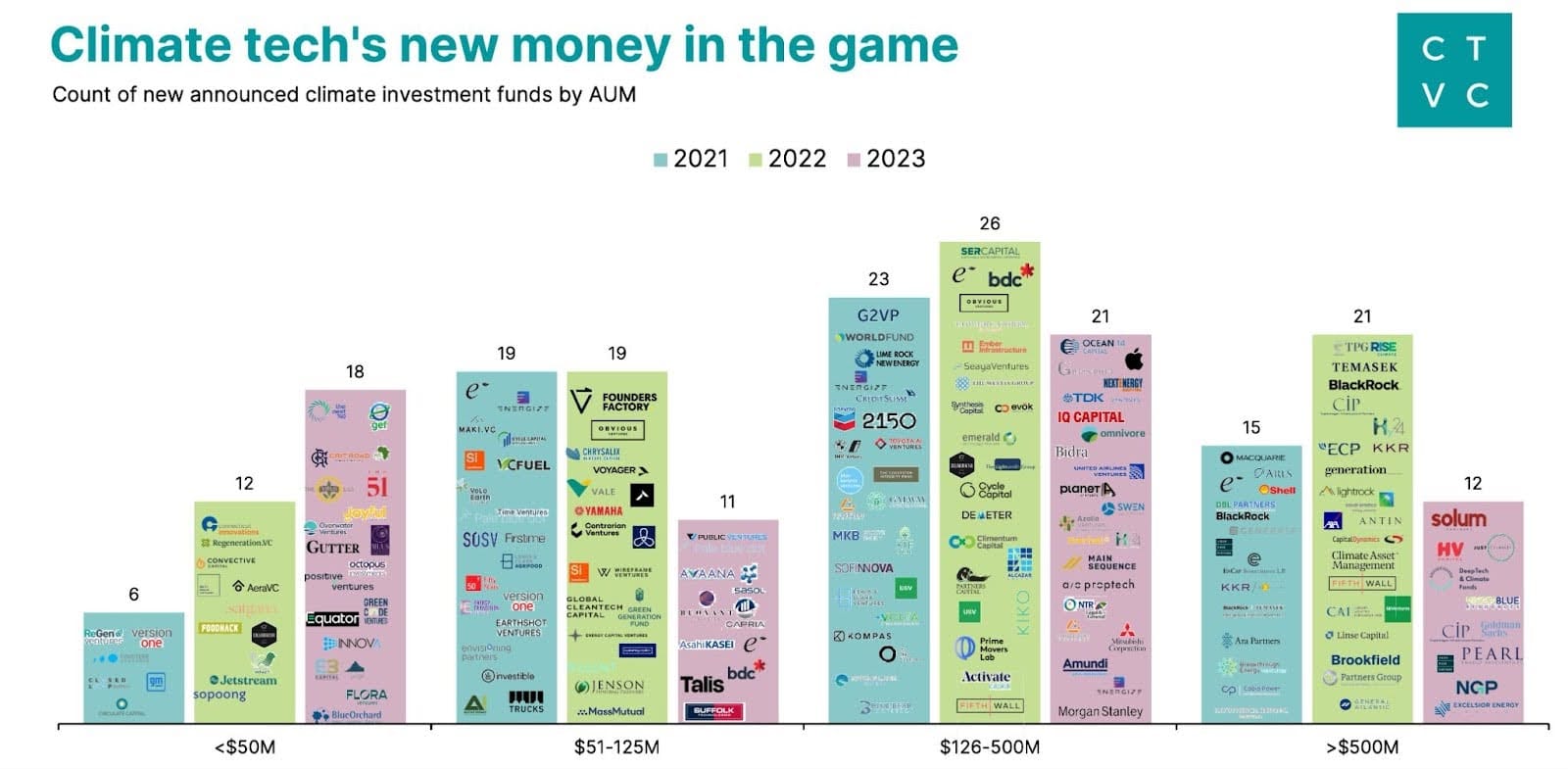

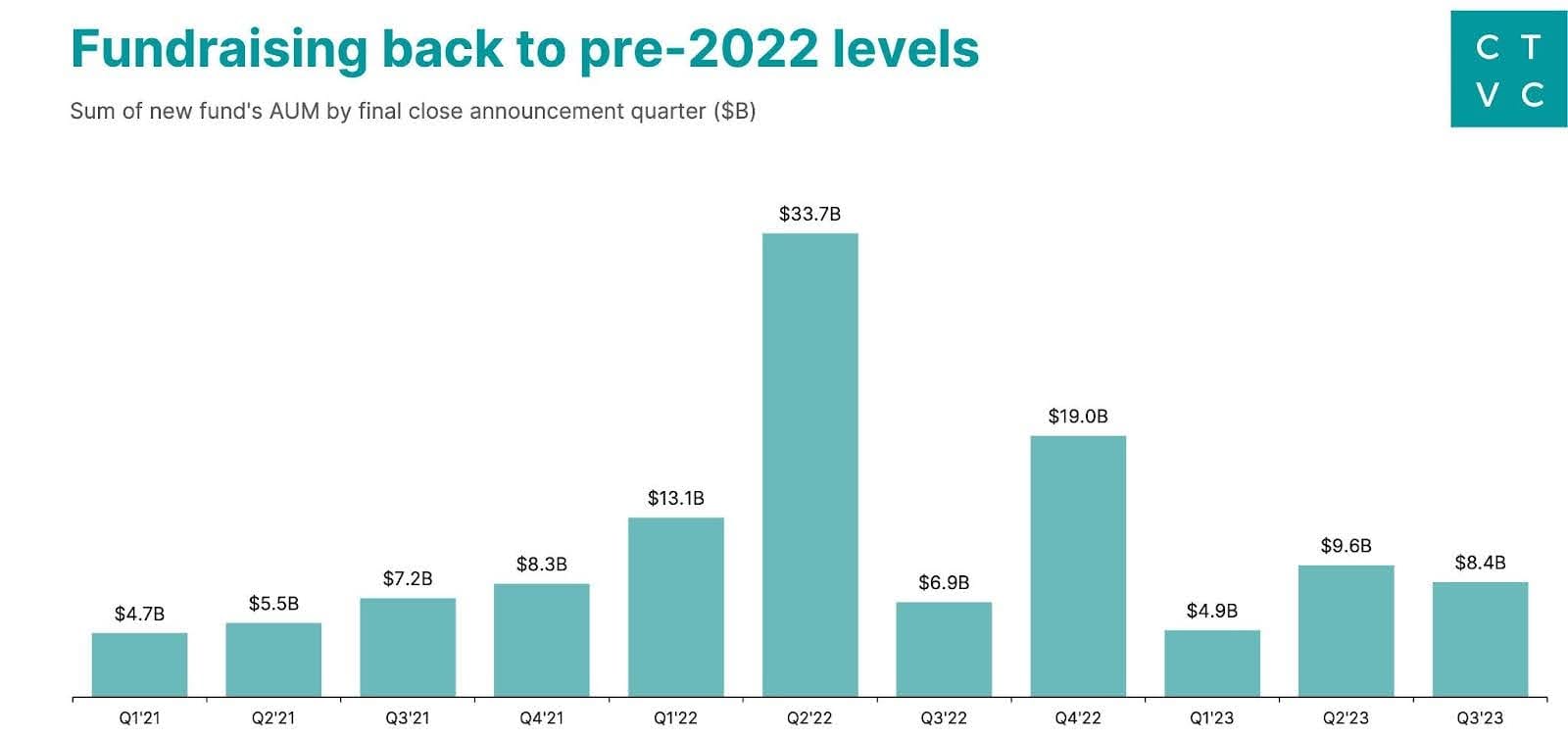

The number of new funds is slightly lower in 2023 YTD compared to 2021, and fund sizes are marginally smaller, with announced AUM down 69% compared to 2022 and 10% compared to 2021 (though we’ve still got Q4 to go).

The majority of the capital is concentrated in mega-funds ($500M+), which account for just 19% of funds in 2023 by count but make up ~70% of total AUM.

The Dry Math

If we were back in our consulting and banking days, we’d start this presentation with some big “directional” and “illustrative” stickers caveating that this analysis is very much imprecise. Ultimately, we’re trying to put a number on a number that doesn’t exist. Of course, when a fund makes a “final close” announcement that they’ve completed raising capital, that AUM isn’t literally stacked high in that VC’s bank account. For all sorts of reasons (not to mention IRR drag), funds “call” percentages of their LPs’ commitments over their investment time period. The pace of calls varies, so it’s hard from the outside to know exactly how much a fund has deployed, and, sometimes, that announced final fund size actually never gets fully invested at all.

All to say, we’ve skewed conservative in our assumptions to estimate the (directional! illustrative!) amount of dry powder available for climate tech.

🔎

Methodology

- Post-close: This analysis conservatively includes only funds that have announced the exact size of (at least their first) close and excludes announced targets. - Deployment period: We’ve assumed a 3 year deployment period, and also made the big assumption that funds deploy 100% of their capital during the deployment period. Realistically, deployment follows a wider bell curve as funds “reserve” capital to follow on to original investments. **Note that this is an increase from 2.5 years in our 2022 analysis. - Management fees: We subtract a full 20% of the fund size upfront to cover management fees, and assume that just the remaining 80% of AUM is used for investments. (2% annual management fee over a ten year fund lifetime). **Note this is a new assumption in our methodology compared to our previous analysis. - No recycling: We don’t include any assumptions for “recycling,” or taking initial returns from the fund performance and deploying it back into the fund (often to make up for management fees cutting into the investable AUM). - Fund type: We’re purposefully just representing dry powder for climate-specific venture, corporate venture, growth / PE asset classes (excludes infrastructure). - Climate-specific: As with our definition for climate investors, we only include funds that meet our “ impact” and “ vertical” thresholds of a certain percentage of climate investment, by fund type. Our analysis isn’t accounting for dry powder from non-climate-specific funds that may invest into climate companies.

For those of you that have eagle eyes, there are two big changes that make this year’s numbers lower than our previous dry powder analysis:

Slower rate of deployment: We increased the deployment timeline by an extra 6 months from our 2022 analysis to represent the proportionally slower investing environment. By extending the timeline of investments, less capital is available each quarter.

Including management fees: This is the first time we’ve accounted for management fees. Subtracting the 20% of funding that goes toward fund operating costs makes the overall AUM available to deploy smaller.

Some further caveats:

Starting the clock: We tracked funds based on the date of their most recent close announcement, when we have confirmed information on total fund size. In reality, these funds are likely actively investing a year (or more!) before announcing their final close—meaning that the actual available dry powder in the market was higher than our totals reflect. For example, the first close of the TPG Rise Climate Fund was reported as $5.4B in July 2021, but grew to $7.3B at the final close in April 2022.

YOY trends: 2023 isn't over yet, and we’ve shared this analysis earlier in the year than our 2022 numbers. We’ve used YTD figures when possible for more accurate comparisons, but the 2023 totals in the charts below still have some time to grow.

The size of the prize

With all that in mind, here’s the shape of new capital ready to deploy in climate tech.

There’s $13B of VC and $20B of Growth / PE dry powder from closed, climate-specialized funds in 2023 so far.

These funds have invested a cumulative $30B since the start of 2021, alongside earlier vintage funds and general investors for a total injection of nearly $100B into climate tech during that period.

Who’s got money in the bank?

With 62 new funds, the YTD count for 2023 is down from the 78 new funds raised in 2022, but on track for a tie with 2021 by the end of Q4’23.

The greatest growth in count of funds came from the smallest <$50m fund size category. More specialized and first-time GPs are joining the climate charge, and getting a new investment firm off the ground for new GPs takes time.

Naturally, a few of the largest funds contributed the majority of new AUM in 2023. These mega-funds tend to be focused on clean energy and infrastructure investments, such as NGP’s final closing of their $700M energy transition fund, Copenhagen Infrastructure Partners’ $6.1B first closing of their renewables investment fund, and Just Climate’s final closing of their $1.5B fund focused on growth-stage, asset-heavy companies.

Tallying new funds

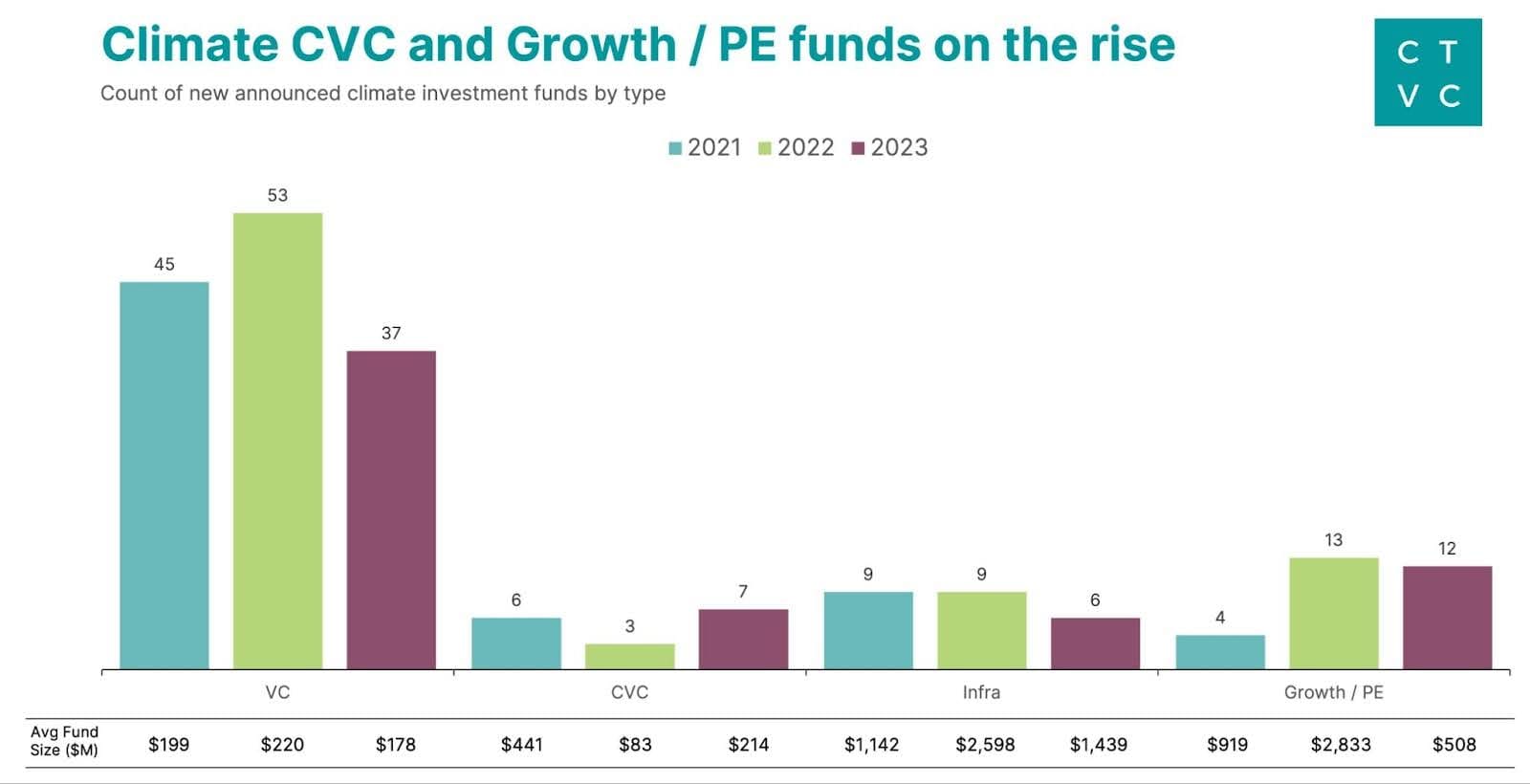

The majority of new raises have been for climate tech VC funds, which have fallen 34% compared to 2022. But the climate capital stack is sophisticated beyond just venture across a diversity of asset classes.

Corporate VCs (CVC), venture funds associated with a corporation, have more than doubled since last year. Corporate players are increasingly allocating capital to verticals within climate tech, including United’s Sustainable Flight Fund and Coca-Cola’s Sustainability Fund.

Growth and PE funds, which acquire minority or controlling stakes in growth and mature companies, are up from 2021, with 12 new funds so far this year. Notable mentions include: Goldman Sachs Asset Management announced a final close of $1.6B for their Horizon Environment & Climate Solutions fund; Morgan Stanley’s 1GT Climate PE strategy, which announced a first close of $500M; Vision Blue Resource announced a $650M final close for their new fund; Energize Capital announced a final close of $300M for their second growth fund.

Infra funds that invest in climate or clean energy projects and assets (rather than companies) continued to broaden the aperture beyond renewables, including Vision Ridge’s $700M sustainable real assets fund.

Market swing

2022’s spike in closed AUM lags 2021’s investing frenzy. Last year, a slew of mega mega funds (e.g., Brookfield's $15B fund, TPG’s $7.3B fund) boosted totals. New fund AUM has since returned to pre-2022 levels.

There are ~20 funds that have made launch or target announcements (including a friendly face in Planeteer!) but have not yet announced how much they’ve closed, so expect to see a flurry of announced AUM heading into Q3 and Q4.

Key Takeaways

VCs slow the roll: Compared with the rapid-fire, ZIRP days of 2021, investors are operating with a “fewer, better” dealmaking strategy, even as active climate funds are kicking off or closing repeat raises. This is especially true for larger, later-stage checks and means we’re back to a reasonable initial investment period of ~3 years—or even longer for mature investors who don't want to back-stop slow revenue ramps during tech development.

CVCs up the ante: Sometimes it’s not all about returns. As more corporates and CVCs enter this space, we’re seeing more investments that could have financial benefit, but even more, provide strategic benefit to the company by building up a capability or shoring up a position in the value chain. For example, Oxy buying Carbon Engineering, or Shell’s continued purchases of public EV charging solutions.

Waiting for liquidity. LPs are making fewer commitments—not just in climate, but across the board. After the last decade of private market frenzy, LPs are waiting for existing investments to return capital before making new commitments. On top of the need for more liquidity, there’s also a continued “wait-and-see” posture from LPs when it comes to understanding outcomes of climate tech exits, emerging headwinds (like rising interest rates), and political certainty on federal climate policy (e.g., the IRA).

Mismatch in the middle: There’s a lot of capital being raised but activity has been concentrated in the smallest, earliest early funds and biggest, latest funds. That leaves a gap in the Series B+ stage as companies get bigger than early funds can support, but haven’t reached the size that mega funds can write mega checks for yet.

What to watch

Moving to maturity: Expect to see more funds seeking to plug the gap in the late-stage venture (Series B+), growth, private equity, or infra investments as the early cohort of climate tech companies—and the technologies themselves—mature toward deployment and scale. As some of these venture-backed companies become real cash-flowing businesses, more PE-type investors (targeting 20-25% returns) could begin taking a climate-focused approach.

Vertical integration: Existing investment firms are growing their AUM with additional fund vehicles abutting their core fund’s stage. Various late-stage funds are moving earlier into pre-seed or are launching incubation programs, while early-stage funds are raising later-stage “opportunity” vehicles to follow on with existing, maturing portfolio companies.

Infra beyond energy: Infra funds are also beginning to dip earlier into emerging sectors that could follow a similar path to solar and wind (i.e., hydrogen, CCS, battery recycling), potentially increasing climate AUM from infra. Case in point: KKR Global Climate Fund, which is intentionally targeting “climate,” rather than just energy, to encompass decarbonization of sectors like transportation, food, and industry.

Climate-curious: Institutional LPs are becoming more climate-curious and starting to put in the work to formulate a climate strategy (...or at least using summer interns to map the market). Meanwhile, bigger pension funds and sovereign wealth funds have taken matters into their hands to build their own climate funds and theses to target later-stage investments directly (i.e., Temasek, Nysno).

Bull vs Bear: It’s a glass half-full or half-empty market, depending on your perspective. A lot of this capital could end up sitting due to a lack of investable companies or projects. If investor return requirements or risk profiles won’t match what companies need to scale, that yet again leaves companies stuck in the Series B range, unable to go further. On the other hand, it could be that we’re just getting started and you ain’t seen nothin’ yet. With all this capital raised (and relatively little deployed to date) we could see a lot more of it start to flow toward creating winning sectors and companies.

Thank you to John Tan for the first-rate data analysis and visualization. Are you seeing the glass half-full or half-empty in these findings? Want to double-click into this dataset? Drop us a note at [email protected] with your predictions, comments, or questions.

Newsletter

Newsletter