By 2016 it was official: cleantech was dead. The venture capital funding model had failed to grow the promising clean energy companies of the early 2000s and everybody lost… or so declared the canonical report from MIT. The title alone—Venture Capital and Cleantech: The Wrong Model for Clean Energy Innovation—pounded the final nail in the coffin of cleantech 1.0.

Ultimately, less than 10% of cleantech companies founded after 2007 generated returns to cover even the initial capital. While some investors tried to squint at Tesla's long-term stock performance long enough to see a favorable outcome for cleantech 1.0 as a whole, it took until 2020 for enthusiasm to bounce back in earnest.

Even as more money flows to thousands of climate founders playing venture with their careers and renewable energy company IPOs such as Nextracker and Enlight Renewable Energy are among the largest so far in 2023, we haven’t seen much analysis on climate exit trends since the 2016 MIT postmortem. Climate tech is not cleantech, so we rolled up our sleeves and built the dataset ourselves! Our analysis of the 289 climate tech exits from January 2020 to February 2023 reveals a clearer picture of the trajectory of the modern climate tech industry so far.

Highlights

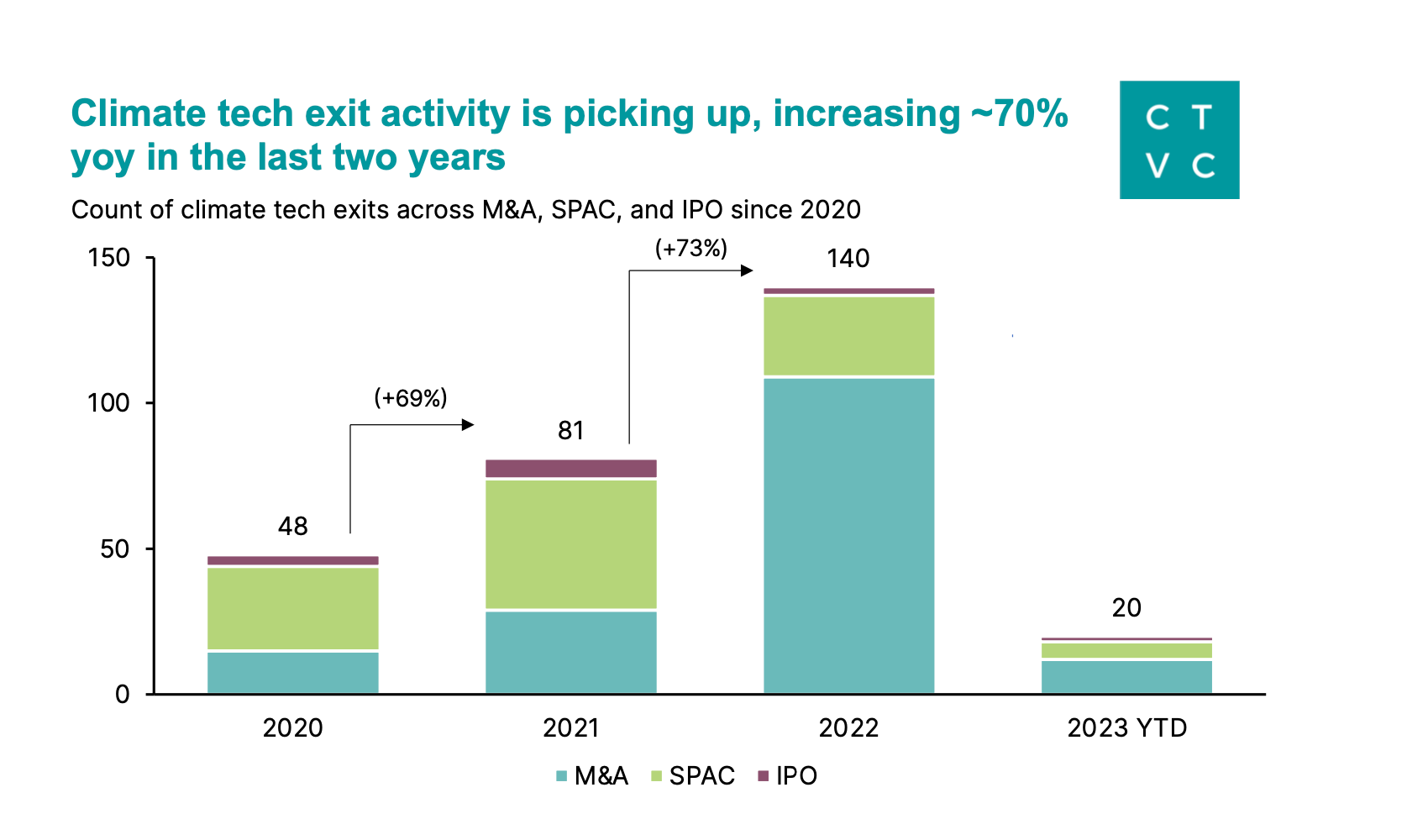

289 climate tech companies have exited via M&A, SPAC, and IPO since 2020.

Climate tech exit activity has increased 70% YoY in the last two years

$400B in total enterprise value from the last three years’ 150 disclosed exits

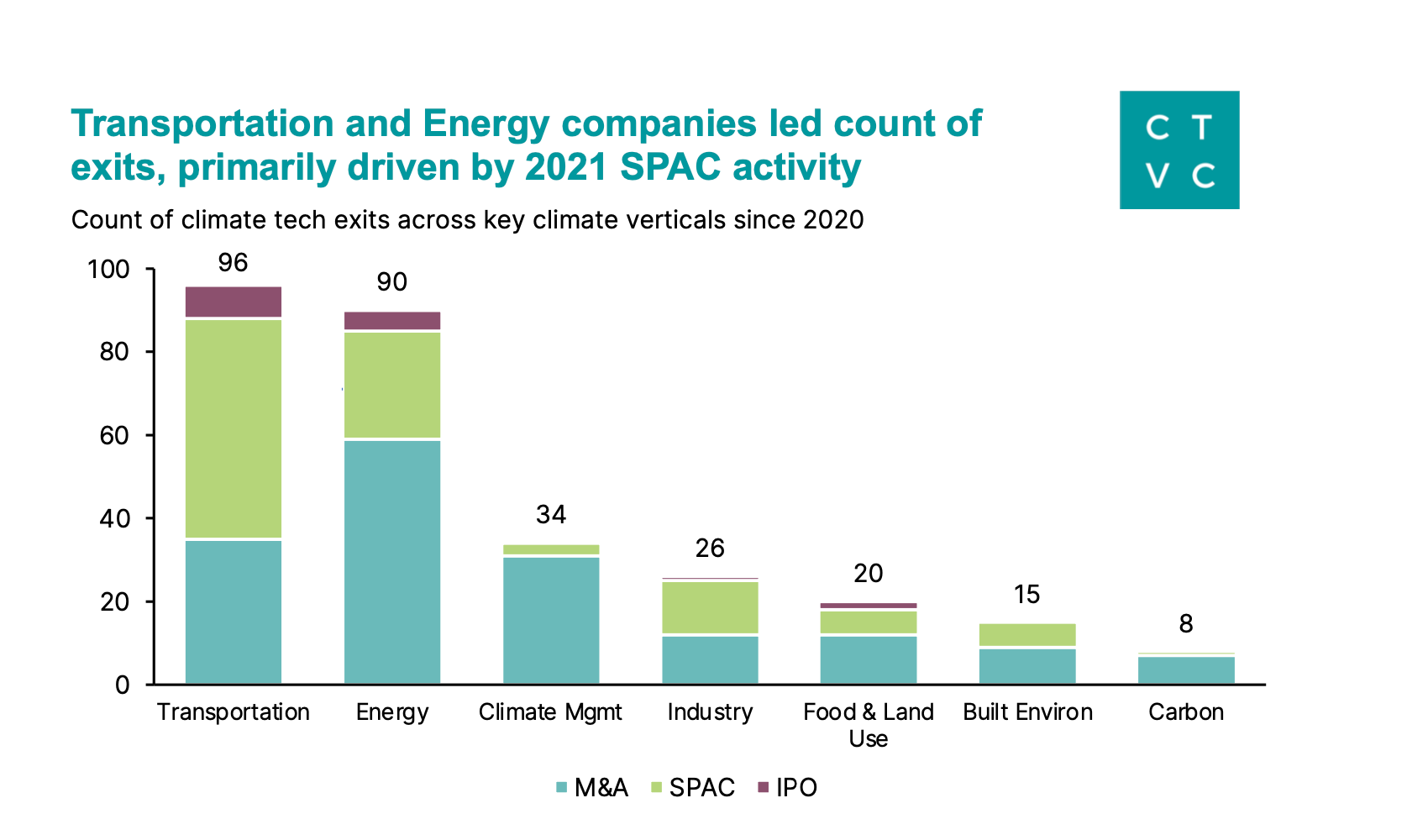

Transportation and Energy companies led the exit count at 186, making up 64% of exits.

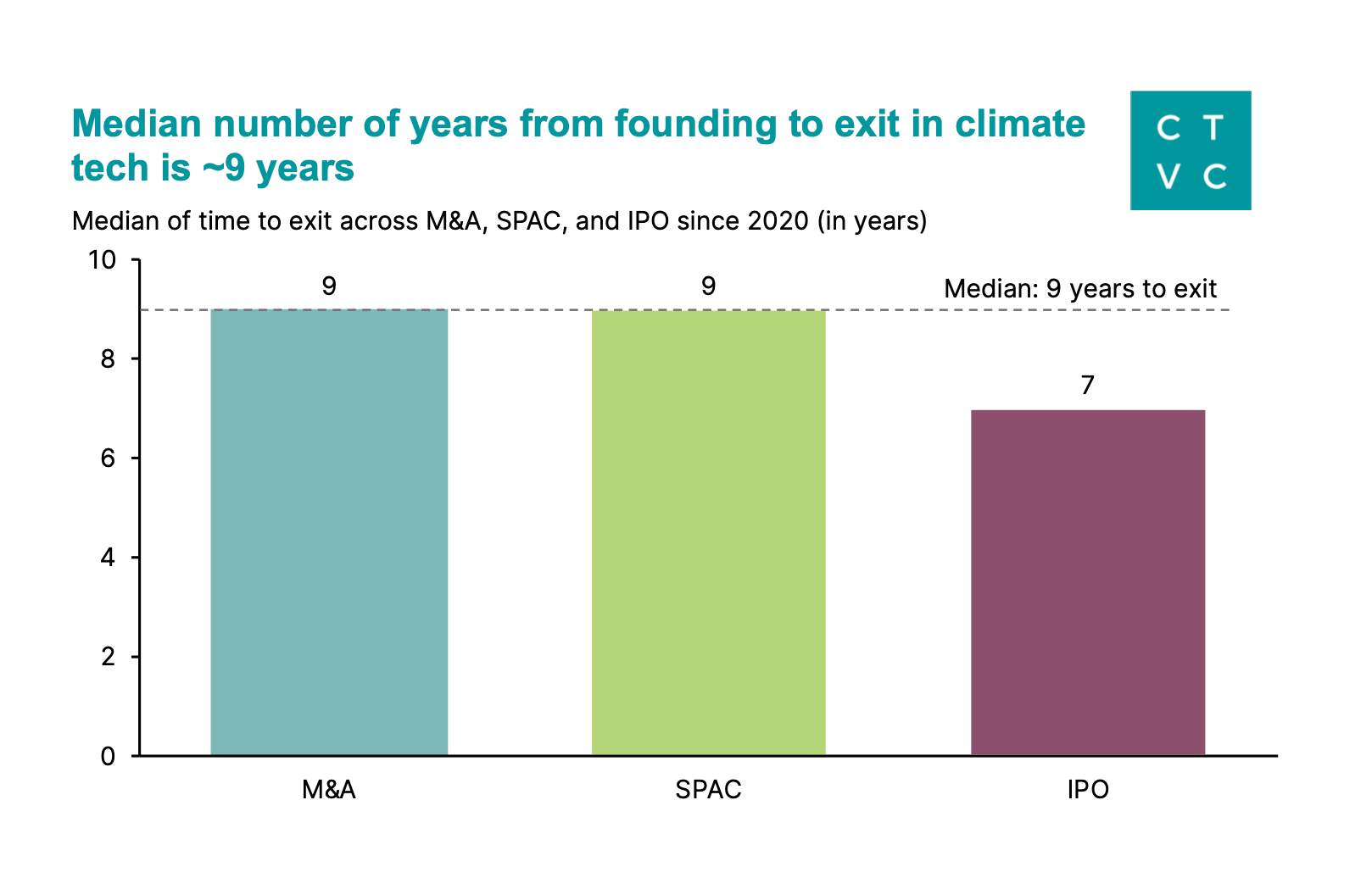

The median time from founding to exit is ~9 years.

The top acquirers were primarily large energy companies and private equity firms.

Exit methodology

Exits come in many shapes and sizes, and climate tech is no exception. Our methodology for defining an “exit” is outlined below:

Deals must have been announced between 2020 and 2023 YTD

Tracked exits are based on M&A, IPOs, and SPAC activity

Only included majority ownership exits at the corporate level (excluded divestitures/spinouts, project or asset sales, or minority buyouts)

Important note: Not all exits were climate tech venture-backed startups under our methodology—only 21% were previously tracked in our VC dataset. Many exits came in the form of renewables developers trading between private equity firms, industrial “climate tech” businesses (think: electric motors, RNG fuel production) getting scooped up for their sustainability merits, or quick-flip companies that hadn’t previously raised venture but jumped on the SPAC frenzy.

Zooming out on climate tech exits since 2020

Climate tech exits have been steadily moving up and to the right along with funding and dry powder. The total number of IPOs, SPACs, and M&A transactions increased by ~70% YoY in 2021, then again in 2022.

With the SPAC market cooling down post 2021-boom, climate tech saw a significant uptick in exit activity as early climate companies matured and got picked up by larger legacy players.

M&A became the largest segment of exits last year—the number of these deals more than tripled compared with 2021. From 2020 to February 2023, M&A accounted for 57% of all exits, with SPACs following close behind in second at 37%.

Only a handful of climate tech companies reached the public markets through the traditional IPO route each year, peaking at seven in 2021 with Rivian’s $66B debut leading the pack. Despite a steady rise of exit count, the tiny 6% proportion of IPOs indicate a still-nascent exit market, especially with IPOs representing the gold standard of exit outcomes for VCs.

It’s no surprise that the most mature climate tech verticals—transportation and energy—saw the largest number of companies go public or get acquired. Those verticals alone account for nearly 65% of total exits.

Exit activity across verticals parallels the proportionate amount of venture & growth funding by vertical. As with VC funding, the biggest exits were primarily EV and battery companies.

Within transportation, more than half of the companies to exit were in the auto industry or EV charging/fleet management space. This SPAC-heavy vertical includes automakers who made splashy exits since 2020 but are already struggling to keep their engine going (and share price above $10), like Arrival, Nikola, Lucid, and Lordstown.

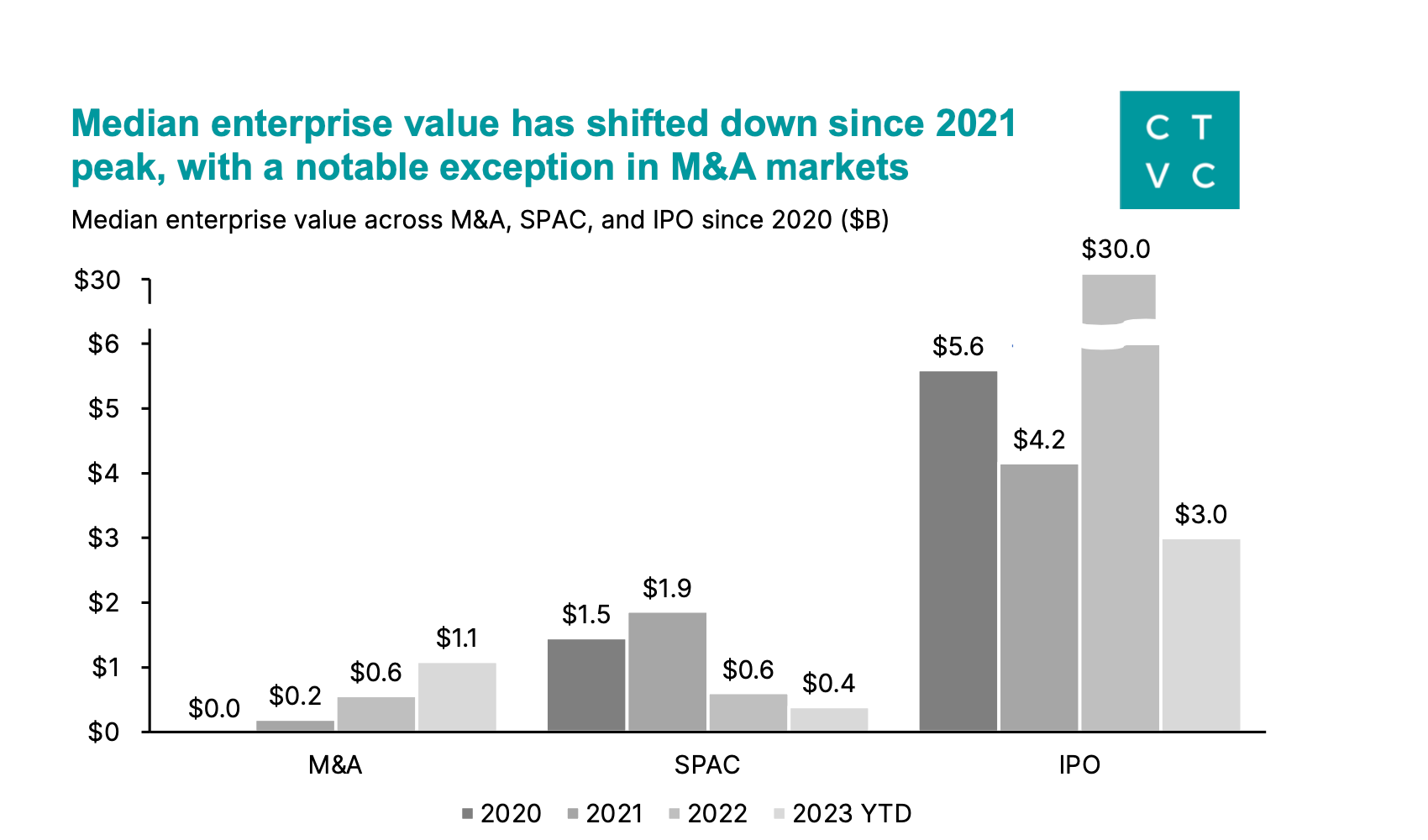

Median enterprise values trended down for SPAC and IPO exits as public markets faced rising uncertainty. Meanwhile, M&A enterprise values have increased each year since 2020.

The total number of IPOs is much smaller—just 16 across all three years—and the $60B LG Energy Solutions IPO drove the spike in median enterprise value for those exits in 2022.

While M&A deals made up the majority of exits, sample size for those median enterprise values is also much smaller, since most M&A deals didn’t disclose the transaction value.

A climate tech acquisition spree

With the 275% increase in M&A activity over the last year, we zoomed in on the most acquisitive companies and the motivations for their spending sprees.

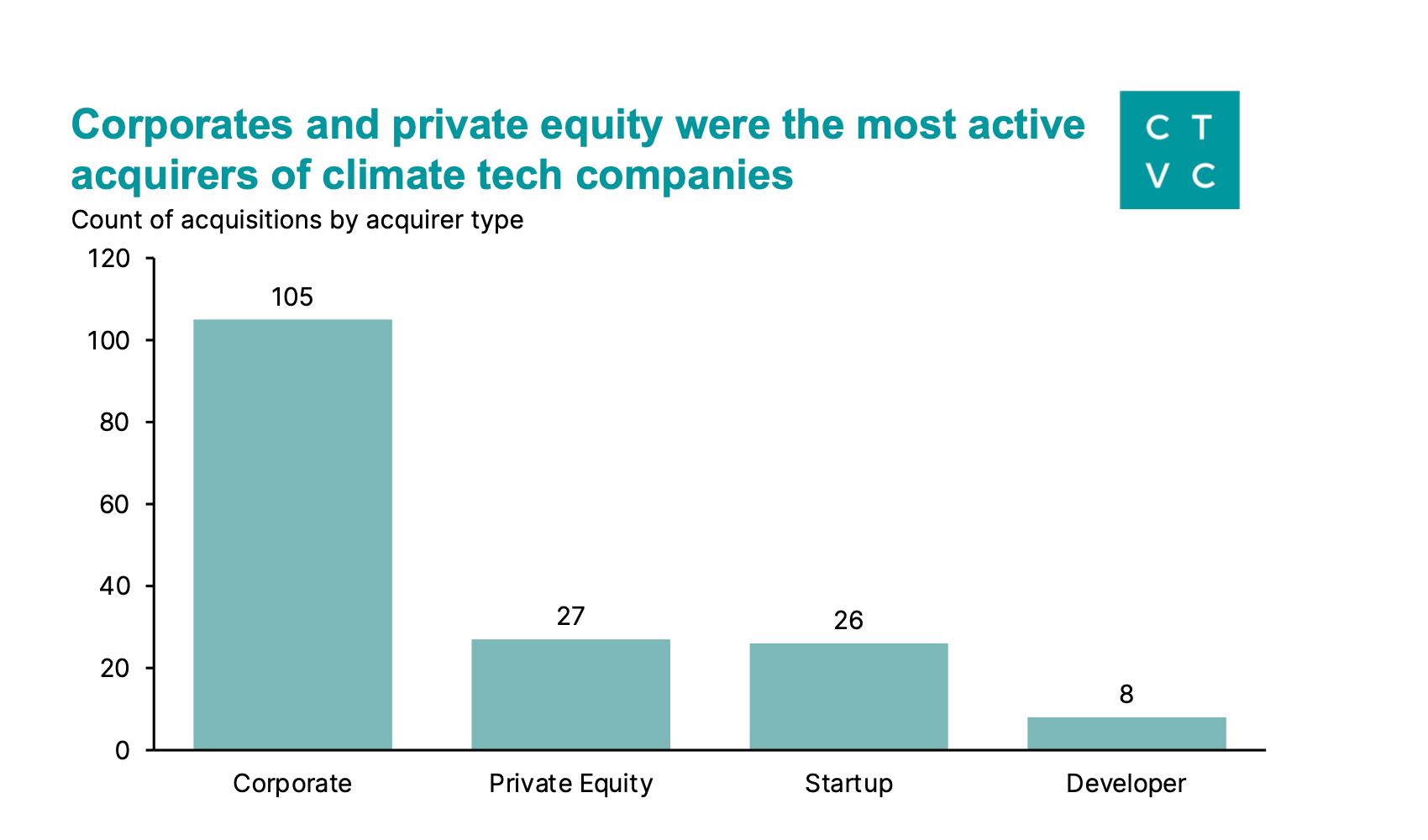

The activity was spread out—more than 120 different acquirers across 165 deals. Corporate buyers were by far the most common, participating in 63% of all acquisitions.

PE firms and startups tied closely for 2nd and 3rd place, with investors scooping up sustainable assets for new ESG mandates and maturing startups buying up earlier players to gain market share/tech.

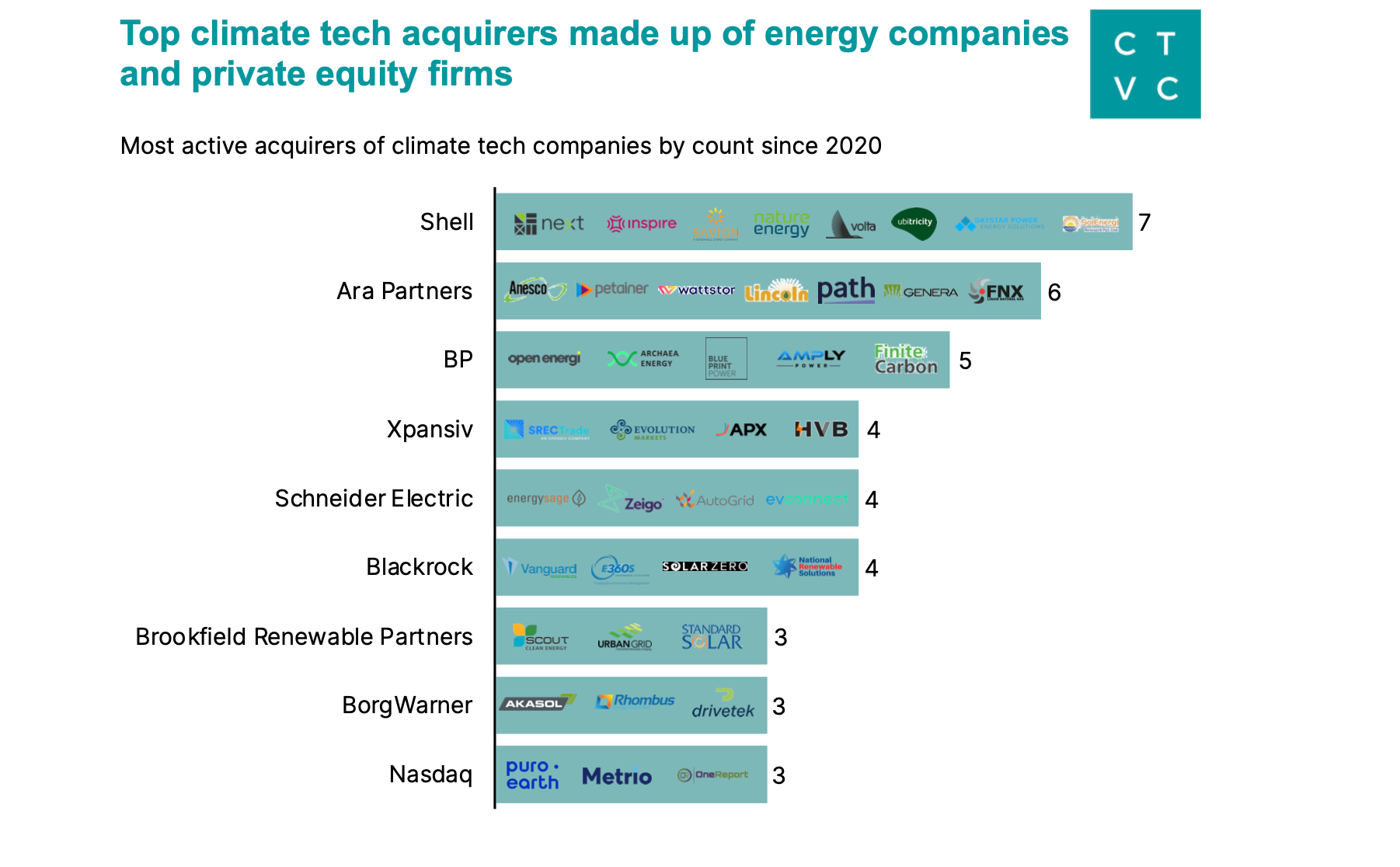

Top acquirers

Fossil-fueled purchasing power: Big O&G companies are inching into the energy transition game through acquisitions. Last year, M&A activity in the O&G industry actually dropped to its lowest levels since 2008, according to analysis from Deloitte. But purchases of “clean” energy assets (“wind, solar, biofuels, hydrogen, battery, advanced mobility, carbon capture, ammonia, etc.”) totaled $32B—more than 2X any previous year and a record 15% of overall M&A deal value in the sector.

Shell has bought seven climate tech companies since January 2021—the most of any acquirer in our analysis. The O&G giant began pushing into the renewables market with Savion, Daystar Power, and Inspire Clean Energy. BP bought five climate tech companies between December 2020 and October of last year.

So far, much of the activity has been focused on technologies that overlap with what O&G companies already know well, like swapping fueling for EV charging and natural gas for RNG.

EV Charging: In January 2021, Shell acquired on-street charging company Ubitricity for an undisclosed amount. Two years later, Shell picked up EV charging network Volta in an acquisition that highlighted SPAC burnout—Shell paid just $169M, less than 9% of the company’s $2B value when it went public via SPAC in early 2021. Expect to see more SPAC’d high-flyers come back down to earth in the next year.

A landgrab for RNG: Low-carbon mandates have fueled a spate of renewable natural gas (RNG) acquisitions as well. RNG is a biogas that’s interchangeable with natural gas extracted from underground but made from waste feedstocks like food scraps, plant-based materials, wood, and paper products. It can also be used to make hydrogen fuels.

Bottom line: While RNG has yet to displace a significant share of natural gas use and its potential to reduce emissions may be considerably less than previous estimates suggested, these deals show that large energy companies are betting on biogas as a pathway to “cleaner” fuels.

The velocity of startup fundraising has slowed over the last six months and fewer private companies are venturing into uncertain public markets. The combination of capital drying up and high O&G share prices creates an opportunity for industry giants to swoop in on discounted climate tech deals. Those are beneficial conditions for the fossil fuel acquirers, but early acquisitions now could hinder the healthy maturation of climate tech as fewer companies make it to large IPOs down the road.

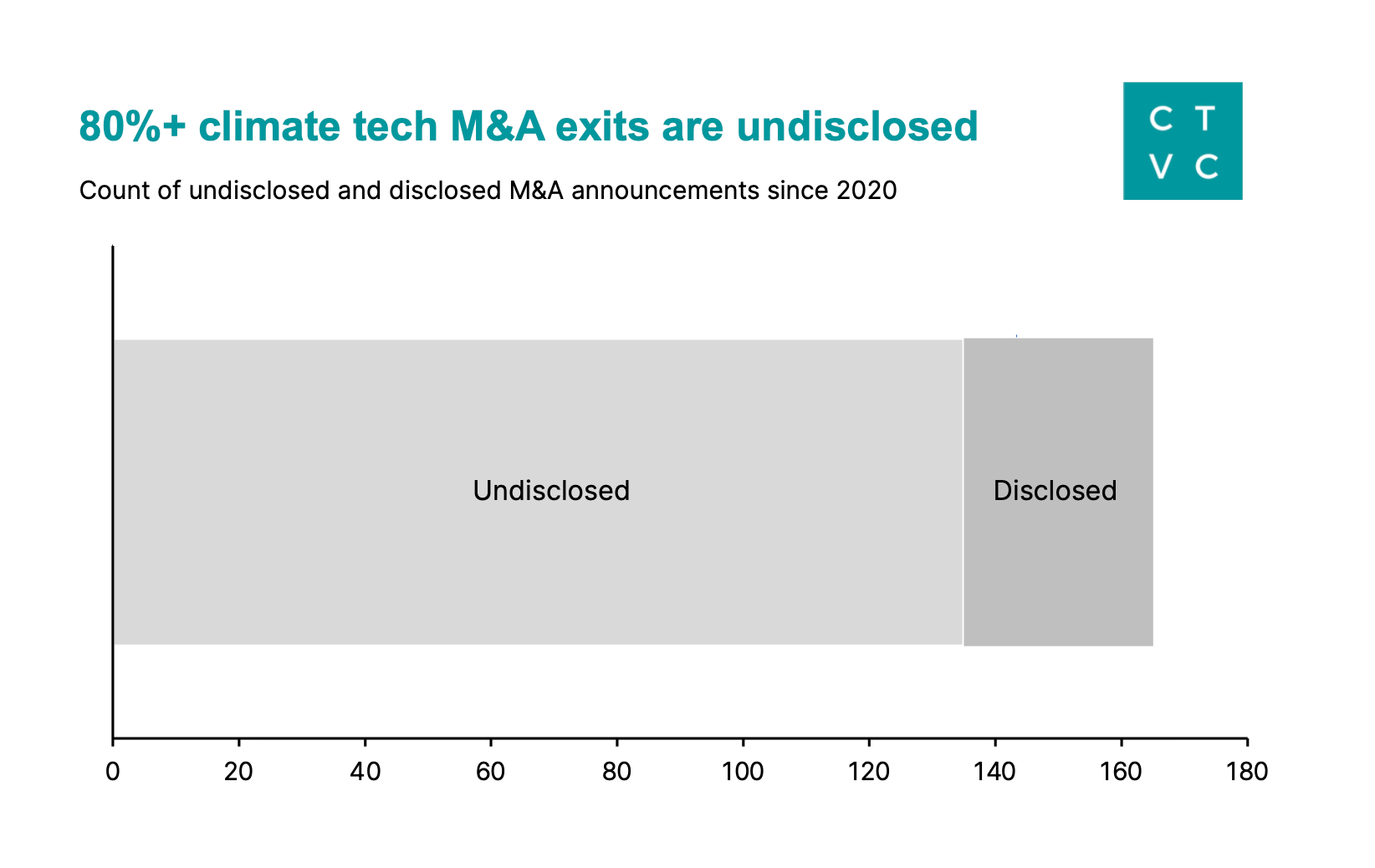

While M&A transactions make up the majority of climate tech exits, more than 80% flew under the radar with smaller, tuck-in acquisitions.

Although not a hard and fast rule, undisclosed acquisitions—with no dollar amount listed for the deal—can often signal mediocre outcomes for the target. Given the early status of the climate tech market, many of these transactions may have been bargains for the buyers rather than successes for the sellers.

Most of the disclosed deals were for large renewables or industrial acquisitions, such as Westinghouse (Nuclear), Archaea (RNG), and Meritor (electric drivetrains). But only six of the 26 startups in our analysis shared their M&A transaction value: Volta, WM Motor, BreezoMeter, SenseHawk, Root AI, and Rhombus.

The (almost) decade-long journey to exit

The median time to exit is 9 years. That means even if a company was founded at the start of this current climate tech wave in 2019, it would still be 5+ years from exit, on average.

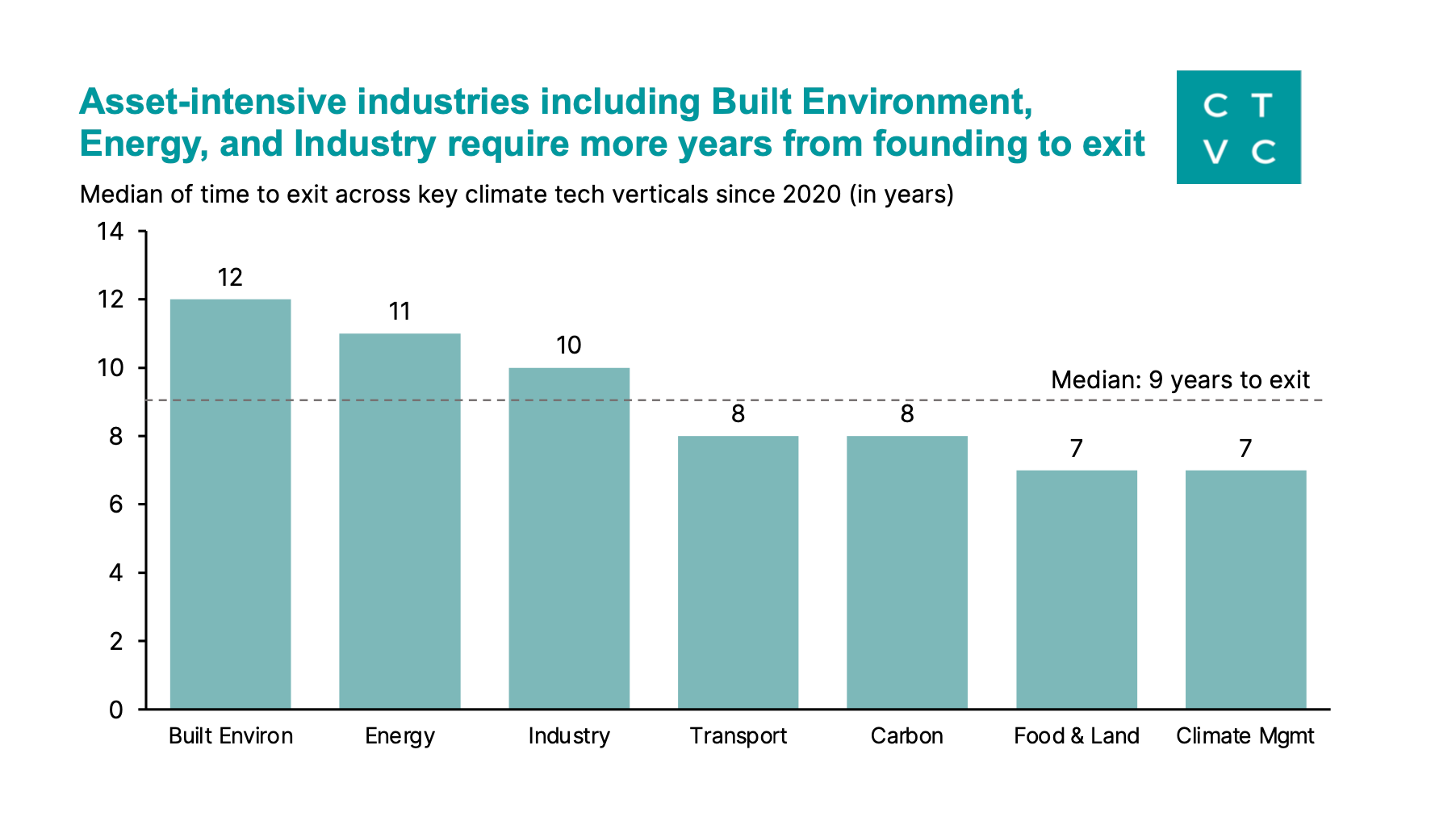

Time from founding to exit in climate tech also spans a vast range. The longest time to exit was Westinghouse, which was founded in 1884 and changed hands multiple times before Brookfield acquired it last year. One of the quickest exits captured was the acquisition of BetterClimate, which Watershed bought in 2022—less than a year after it was founded.

More asset-intensive sectors like Industry, Energy, and Built Environment fall above the median in terms of years from founding to exit. Software- or consumer-focused verticals like Food & Ag and Climate Management have a slightly speedier time through exit.

While the count of climate exits has increased YoY, quality is questionable. Quick SPACs and M&A account for 94% of exit activity, with “gold standard” IPOs still too small of a cohort to call any definitive success yet.

We’re early in the climate tech market maturation. Specifically, we’re ~4 years into the median 9-10 year cycle to exit (even longer in hardtech). Expect the rash of climate exit activity to occur in 2026+ once the current large cohort of Series B cos cross over to the other side.

Regulation and O&G tailwinds continue to accelerate demand. The past six months of data signals increased public market and acquirer demand for climate tech assets, especially fueled by IRA. Likewise, corporate buyer interest is higher than it was during cleantech 1.0. We anticipate more near-term “energy co” corporate buyer activity as fossil fuel stock prices soar, coinciding with frozen growth-stage private markets.

More comparison data is good for climate tech. Exits provide reference points for where startups are going and incentive for founders and investors to enter the space. Robust exit results are the missing puzzle piece in proving climate investing is not concessionary.

Newsletter

Newsletter