🌎 H1 2025 Climate Tech Investment: Capital stacking up for energy security & resilience

Get Sightline’s signature H1’25 investment trends report inside

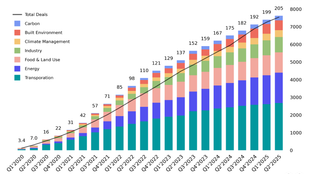

More deals, fewer dollars in the first half of 2022

Since we last tracked climate tech’s funding peak of $40B in 2021, the free-flowing venture market has started to retreat for the first time since 2019. The venture market was hit with a -23% drop in funding in the last quarter, and an even steeper -31% in crypto.

As overall funding declines, climate tech investment returns to pre-boom time levels with a good amount of dry powder left to go. Of note, venture funding announcements are lagging indicators of real-time market shifts. We’ll continue to keep a finger on the pulse on the coming months, and whether the new spate of climate dry powder is enough to weather the macro funding fallout.

The majority of the funding we’ve seen remains in the US across Transportation, Energy and Food & Land Use. Fewer mega deals (>$500m) this year account for the drop in total climate dollars while the actual volume of climate deals has increased with the amount of climate-curious investors joining in.

Tl;dr, climate tech investment activity - particularly earlier stage - is still on track to increase YoY, even if funding dollars may decrease from the $40B funding peak in 2021.

In our report, we break that down by vertical, sector, stage, and geography to offer a full market map across ~$70B in climate funding in 1,312 deals over the past two years.

As always, we’ve sourced deals from reader submissions, web scraping, paid databases, and other networks and evaluated each company to assign it a climate tech subsector and deal stage.

Whenever you’ve got climate funding news to share with our community, drop those deets at this link 👉

🧹 Other housekeeping: we’ve launched a new website! If you’re on Gmail, add [email protected] to your contacts and move any emails from the promotions tab to make sure we’re landing in your inbox.

💰Climate tech startups raised $19B across ~500 venture deals in the first half of 2022

📉 H1’22 total funding dropped 21% compared to the white-hot back half of 2021 ($23B) - consistent with the broader market slowdown, particularly in later-stage deals

📈 Up and to the right! Meanwhile, deal count maintained ~15% growth Q over Q, buoyed by double the deal activity at early-stages

💨 Carbon vertical funding jumped 8x (!) compared to the same period in 2021

⚡ Energy, Transport, and Food maintained 70% share of dollars raised, with early signs of diversification into less mature verticals

🌎 US and Europe dominate ~80% of climate cos’ HQs

💼 ~2,500 climate-curious investors joined at least 1 climate tech deal over the last two years

As the climate tech market continues to evolve, we’ve accordingly updated our methodology to capture the 7 broad climate verticals and subsequent 60+ critical sectors helping us monitor, mitigate, remove, and adapt to our warmer and weirder world. (You better believe that we’ve got another 250+ technology subsectors behind that, but we’ll spare you the details.)

Finally! A market map of climate tech! Over the past 2 years, we’ve tracked $70B of venture capital deployed in 1,140 companies across the 7 major climate verticals and 60+ critical sectors. Transportation, Energy, and Food verticals still reign supreme accounting for 60%+ of climate company count and a whopping 80%+ of dollars deployed.

The “Impossible, Tesla Effect” has led to a disproportionate share of activity in Alternative proteins (8% of company count) and investment into Electric Autos (17% of dollars deployed).

[What’s this weird rectangle chart, you ask? 😕 As recovering bankers and consultants, we love a good Marimekko - which helps us understand the bigger market picture and spy outliers. Best read left to right spot the relative width of verticals, and then bottom to top to spot the relative height of sectors. Thanks for indulging us.]

Climate tech startups raised $18.6B in the first half of 2022. Funding declined 21% compared to the white-hot back half of 2021 ($23B), though H1’22 investment still outpaced H1’21 ($16B).

Where Transportation, Energy, and Food verticals pulled in ~90% of total climate funding in 2021, the start of 2022 shows signs of vertical diversification with 30% of deal activity dedicated to Industry, Climate Management, Carbon, and Built Environment as climate-curious investors start to explore new territories.

Carbon has been the breakout star of the year so far, scoring 8% of funding compared to a <2% trickle in 2021 - said another way, a whopping 8x growth from H1’21. (Much more on Carbon in the vertical breakout below!) Not to be outmatched, funding in Climate Management and Industry also steadily climbed to 8% and 11% of total 2022 dollars.

Transport funding trended downwards 40% compared to H1’21, driven by fewer mega Electric Auto and Battery deals as the air has been let out of the EV SPAC frenzy. Energy funding also rebalanced to normalized levels sans $B+ fusion deals like Helion and CFS which momentarily buoyed Q4’21 Energy funding.

Deal activity count tells another, steadier story. Market slowdown aside, the number of climate deals sizably increased to 477 rounds so far this year. Midyear deal count grew 76% and 36% compared to the first and second half of 2021, respectively.

The relative ratio of vertical splits held steady from prior quarters, with deal count momentum ticking up in Carbon and Industry segments in particular.

The impact of the broader market slowdown hit late-stage deals the hardest with a 39% decline in Growth (Series D+) funding between H1’22 (32%) vs H1’21 (57%).

Market slowdown, market shmo-down for early-stage deal activity! Seed and Series A funding and deal count more than doubled compared to the first half of 2021. Early-stage deals are likely insulated from broader macroeconomics for the time being given the ~$20B of climate dry powder in the coffers of climate investment funds.

Deal stage distribution reveals the difference in maturity between verticals (mature on the left, emerging on the right). Cleantech 1.0 Era verticals like Transportation, Energy, Food & Land Use lean towards later-stage deals with 40%+ of activity in Series B and later. Meanwhile, emerging markets like Carbon and Climate Management skew towards early-stage activity (~80% Seed and Series A).

Average deal sizes by stage shows an even starker view of the dropoff in Growth round sizes, and some resilient upwards momentum in Series C-stage round sizes over time.

Stage naming conventions can be quite subjective, so we assigned late-stage funding ($>50m) into cohorts by deal size range. The dropoff in mega-sized rounds is best spotlighted by the absence of $>500m deals from 10% in 2021 to 2% in 2022 companies so far.

2022 might just be the Year Of The Carbon Vertical. H1’22 Carbon deal activity doubled (92%+) compared to the same timeframe last year, while funding 8Xed (740%+)! Funding was buoyed by a few large deals including Climeworks’ $650m and $100m+ rounds from Carbon Clean and Twelve. Verdox’s $80m and Flow Carbon’s $70m likewise set the benchmark high for Series A deal sizes. Prior to 2022, Svante’s took the cake for largest Carbon round size with their $75m Growth round.

While CDR is the star of the show with 32% of deal and 57% funding action, Marketplace & Procurement software startups score the greatest number of deals (36%) but require much less capital each (14% of total funding).

2,424 unique investment firms participated in at least 1 climate deal over the last 2 years. Food & Land Use companies attracted the greatest number of investors - a comfortable place to start wrapping one’s head (mouth?) around climate investing. Built Environment and Carbon attracted the fewest investors, perhaps because these verticals are among the most technically complex and insular.

To isolate the non-tourist investors whose fund theses focus on climate specifically, we assigned a tag to funds that participated in at least 5 climate deals over the past 2 years. (Imperfect, we know - check our Running List of Climate Tech VCs for much more detail on climate-first funds.) Interestingly, those tagged ‘Climate Investors’ tend to participate equally actively across the 7 climate verticals. Sensibly, the concentration of ‘Climate Investors’ in technically complex emerging verticals like Built Environment and Carbon is notably higher.

Of CTVC’s tracked climate tech companies, 54% are based in the US with California alone making up 24% of the total count. Together, the US and Europe represent 81% of climate headquarters with Asia Pacific accounting for a growing 10%. Of note, India and Australia make up 36% and 24% of APAC, respectively.

Further detail on CTVC’s 7 verticals and 63 sectors:

⚡ Energy - The electrons and fuel that power us

Sectors: new generation technologies (e.g., nuclear, solar, geothermal), energy storage, hydrogen and other low-carbon fuels, enabling renewables software, marketplace, and grid management platforms, DER and demand response tools, utility transmission and distribution services

🚗 Transportation - The movement of people and goods

Sectors: battery technologies, EV autos, EV charging and fleet management, electric micromobility and ridesharing, zero-emission planes, boats, and trains, urban public transport

🌾 Food & Land Use - The nutrients and resources that give us life

Sectors: alternative proteins, regenerative farming, vertical farming, sustainable fertilizer and animal feed, nature restoration and ecosystem services, remote sensing for crop yield optimization, autonomous farming equipment, water tech, and food waste reduction

🏭 Industry - The goods and raw materials we use every day

Sectors: low-carbon cement, chemical and plastics, steel, manufacturing, metals and mining, circular economy commerce, sustainable textiles and packaging, waste and recycling

🛰️ Climate Management - The data, intelligence, and risk associated with a changing climate

Sectors: emissions and sustainability reporting, ESG investing and fintech, earth observation through remote sensing, climate risk and intelligence platforms

🏠 Built Environment - The places we live and work

Sectors: sustainable building materials, low-carbon heating and cooling, prefab construction, energy efficiency, building electrification and energy optimization

💨 Carbon - The avoidance and removal of emitted carbon

Sectors: carbon offset marketplace and procurement platforms, carbon utilization, carbon removal and storage technologies, point-source CCS, verifiers and ratings enablers

We’re officially Climate Tech VC obsessed and are contributing to the market’s understanding through our deal-by-deal company and investor tracking. Massive thanks to the entire CTVC team for their contributions to this issue, and always.

We continue to build out our insights like this one to inform investors, operators, and those interested in getting into climate tech - so send us a note 📩 if you want to take a magnifying glass to the charts, or have thoughts, insights, and questions.

Get Sightline’s signature H1’25 investment trends report inside

Survey results: what’s working, what’s stalled, and what’s missing

A sneak preview from Sightline’s exclusive client-only webinar