From “FOAK fatigue” to funding flux, climate tech investors are navigating a trickier, more tactical market in 2025.

A few months ago, we fielded an investor market sentiment survey, in partnership with Elemental Impact, across the CTVC ecosystem to dig into where capital is flowing, where it’s jammed up, and generally what the vibes are like. Now, we're excited to bring you the results. (And founders, be on the lookout for a similar survey for you dropping this summer.)

The results show a market that’s maturing, but not mellowing. Investors are still betting big on clean energy, but actively avoiding the treacherous middle ground between venture-scale risk and infrastructure-scale certainty. And as the policy landscape shifts post-election, portfolios are bracing for turbulence. Below, the most revealing signals from across the stack.

Key takeaways

🔻 FOAK remains the cliff. 69% expect funding for first-of-a-kind projects to shrink, spotlighting the persistent gap between promising pilots and commercially viable deployments.

⚡ Clean energy holds its lead. Investors still back renewables, grid, and storage as core to the energy transition — even as funding for the broader sector cools.

🧱 The scale gap is still wide — and deepening. The $45m–$100m range is the “missing middle within the missing middle,” stuck between venture and infra capital.

📉 Policy whiplash is the #1 fear. Uncertainty around IRA incentives, tariffs, and credit transferability is shifting strategies and modeling worst-case scenarios.

🏗️ Philanthropy ≠ charity. Investors want catalytic dollars to de-risk FOAK — and they see real leverage: small awards unlocking 100x in follow-on funding.

🧠 What’s missing? Labor. One of the most overlooked constraints in scaling climate solutions isn’t capital — it’s workforce.

Market sentiment & landscape

What is your outlook on climate tech valuations for the remainder of 2025?

With the market in a chill, the biggest cohort (42%) anticipate more bankruptcies. This pessimism isn’t just about weak businesses getting weeded out; it's a signal that capital constraints are biting across the board, especially for companies without near-term profitability or flashy returns. Capital access isn’t just a matter of business model clarity but market liquidity.

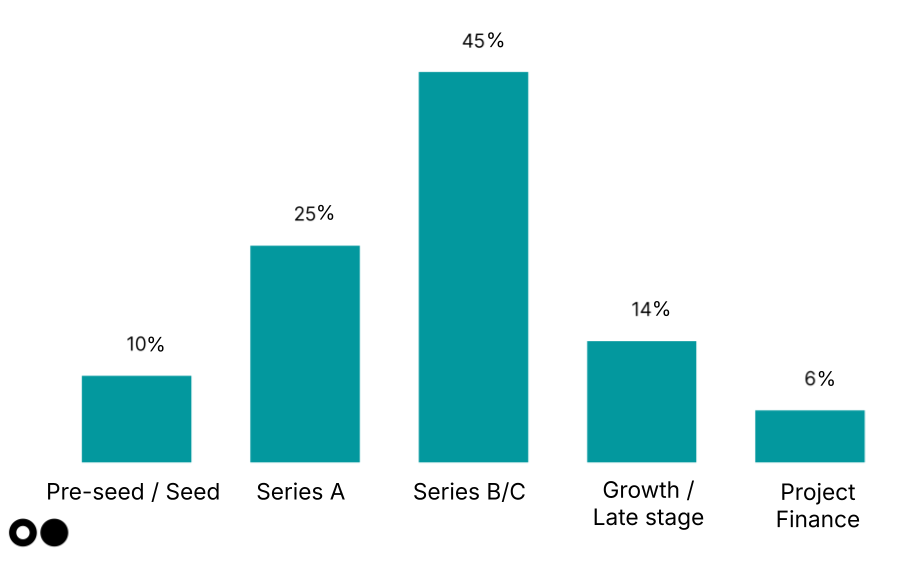

Which stage of climate tech funding do you see as facing the biggest challenges in the next 12 months?

The Valley of Death looms large. Series B and C stages are expected to face the biggest funding challenges, as many climate tech startups have reached this scale-up phase, just as the funding environment is recovering from the 2021–2022 surge.

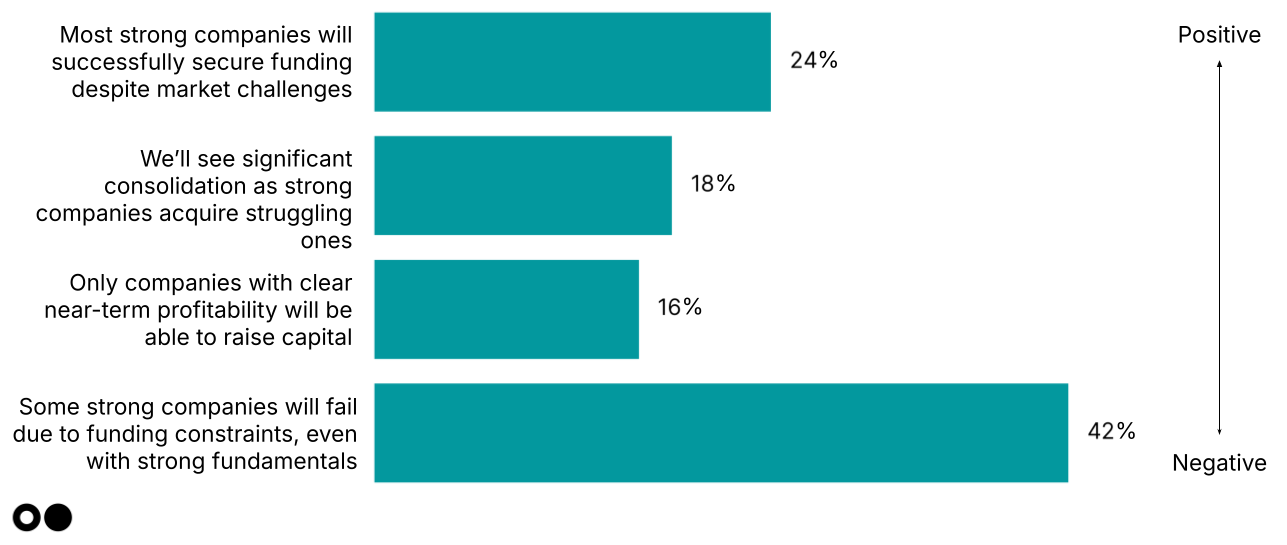

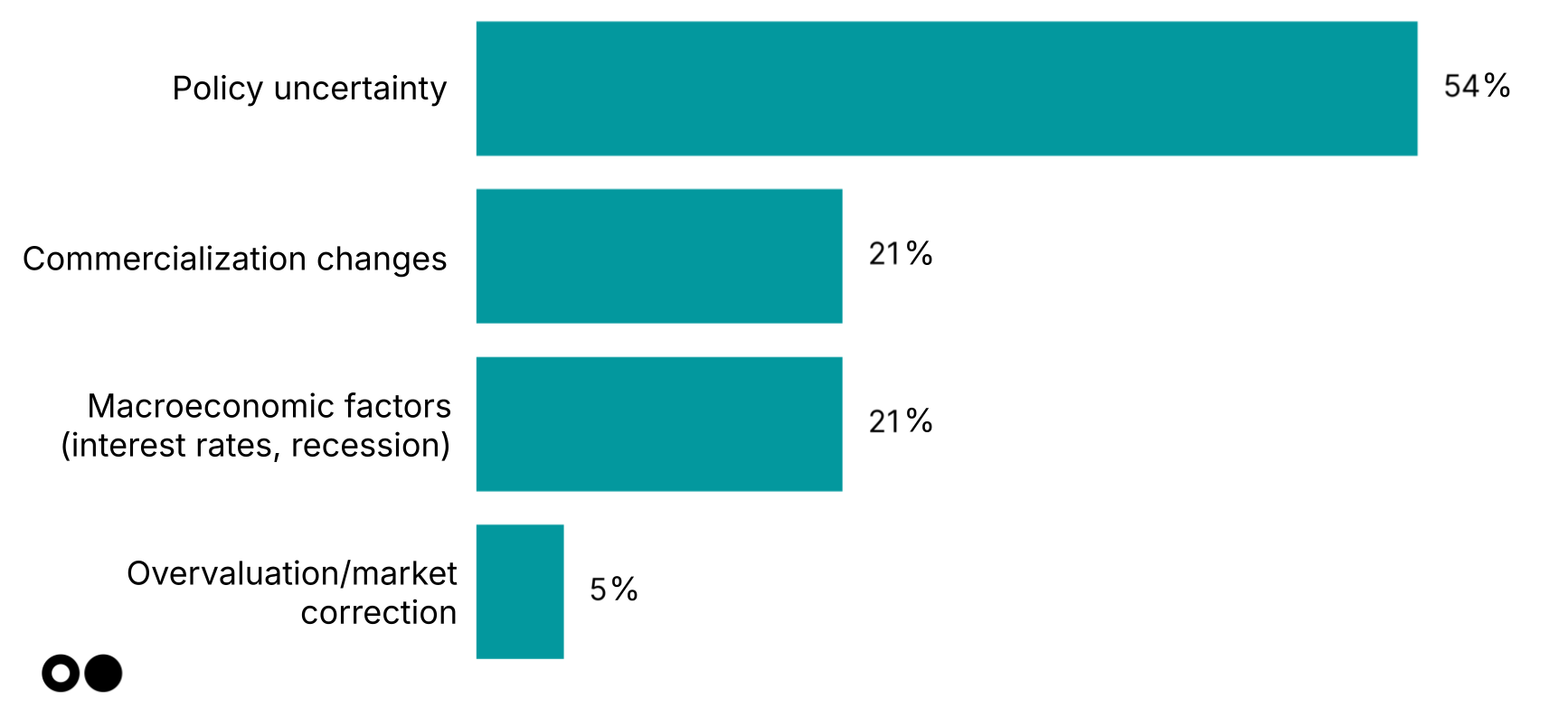

What is your biggest concern for the climate tech ecosystem in 2025-2026?

Policy whiplash looms largest. Over half of respondents flagged policy uncertainty as the top concern for climate tech in 2025–2026, outweighing worries about commercialization shifts (21%), macroeconomic conditions (21%), or lingering overvaluation hangovers (5%). We’ve said it before and we’ll say it again, but investors are allergic to uncertainty.

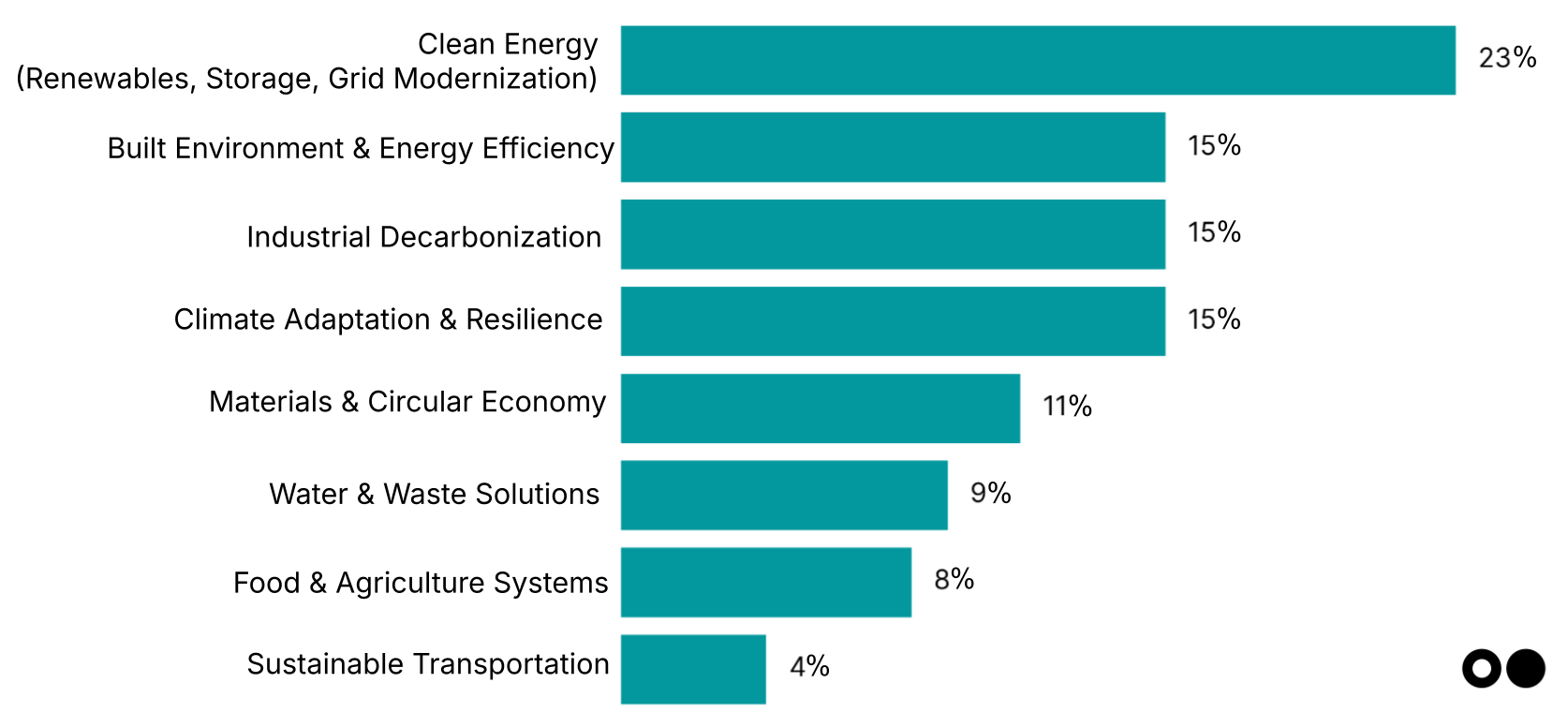

What climate tech sectors do you believe are most ripe for investment in 2025?

Clean energy still tops investor interest (23%), holding its lead even as overall climate funding cooled — a signal of continued conviction in the sector’s central role in the energy transition. The sector’s lead isn’t just hype — clean energy funding rose 12% in 2024 to $9.4bn, signaling continued momentum as capital flocks to (relatively) de-risked climate plays.

Still, “clean energy” can mean many things. Renewables remain a cornerstone of the energy transition — and a safer bet for more mature or infra-focused investors. But storage and grid innovations are increasingly essential in an era of rising power demand, driven by AI-hungry data centers and the growing need for clean, firm load.

Scale gap & financing mechanisms

At which development stages do you anticipate companies will face the greatest financing challenge in 2025-2026?

FOAK remains the steepest financing cliff. A resounding 51% of respondents pointed to first commercial-stage facilities as the toughest development stage to finance in 2025–2026 — highlighting that the “first-of-a-kind” gap hasn’t budged. While early-stage R&D and pilots draw grant and VC support, and scaled deployment finds infra capital, the leap to commercial-scale remains the riskiest, least funded frontier, especially with the threat of the elimination of DOE funding under Trump 2.0.

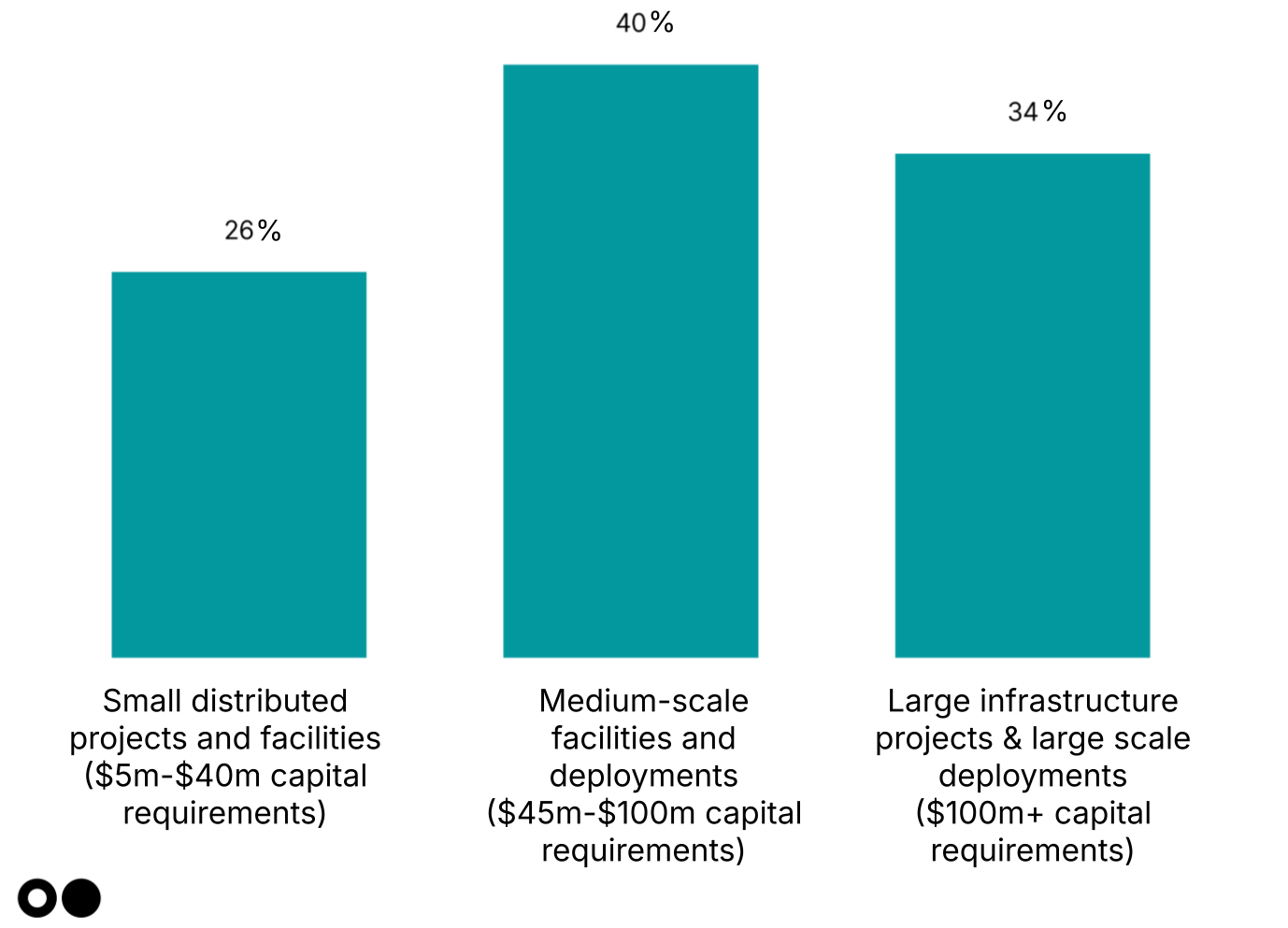

Which projects do you anticipate will face the greatest financing challenge in 2025-2026?

There’s a missing middle within the missing middle. 40% of respondents flagged $45m–$100m deployments as the hardest to fund — too large for venture, too small for infra. This specific midsize slice of the broader scale gap continues to challenge project developers and financiers alike.

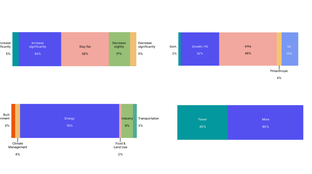

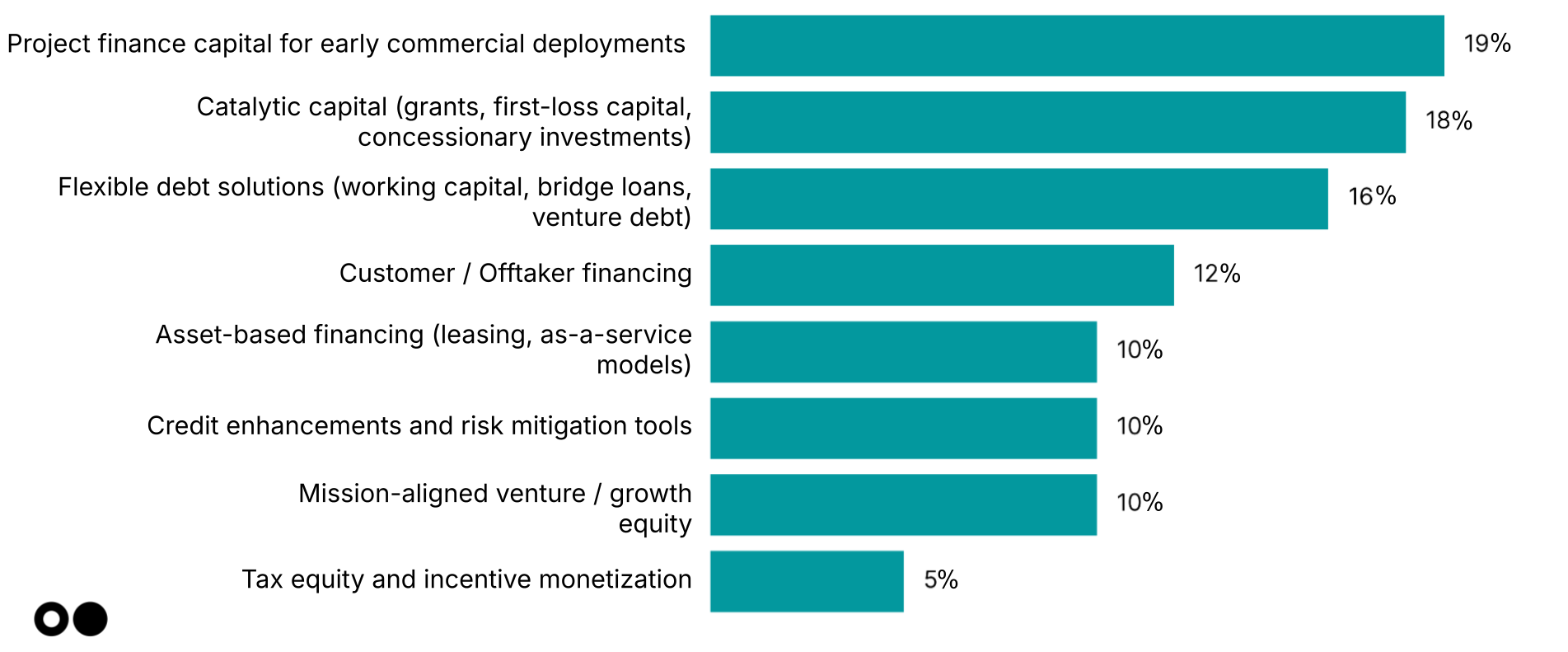

Which financing mechanisms show the most promise for bridging the scale gap?

Project finance (19%) and catalytic capital (18%) top the scale-gap toolkit, signaling a shift away from pure venture toward structure-heavy stacks for early commercial deployments. Flexible debt and offtaker financing aren’t far behind.

Tax equity and incentive monetization trail at just 5%, suggesting a tougher road ahead. With US budget proposals phasing out tax credit transferability — a major engine of the IRA — developers are potentially facing a return to traditional tax equity markets, which reintroduces some friction.

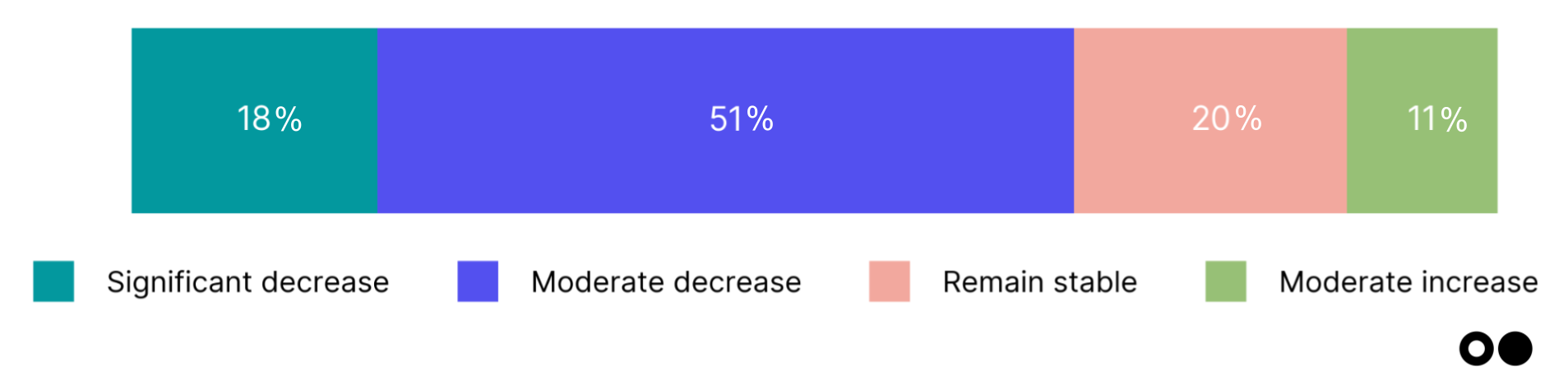

What’s your expectation for capital availability for FOAK facilities across all sectors in 2025-2026?

FOAK funding outlook remains bleak: 69% of respondents expect capital for FOAK facilities to shrink through 2026, signaling sustained investor hesitation at the scale-up edge. With much of the low-hanging fruit already picked, it’s the hard-to-abate sectors — high-capex, high-emissions, low-competition verticals — that now need patient capital to get FOAK projects off the ground and unlock the next wave of commercially viable climate tech.

Policy & political environment

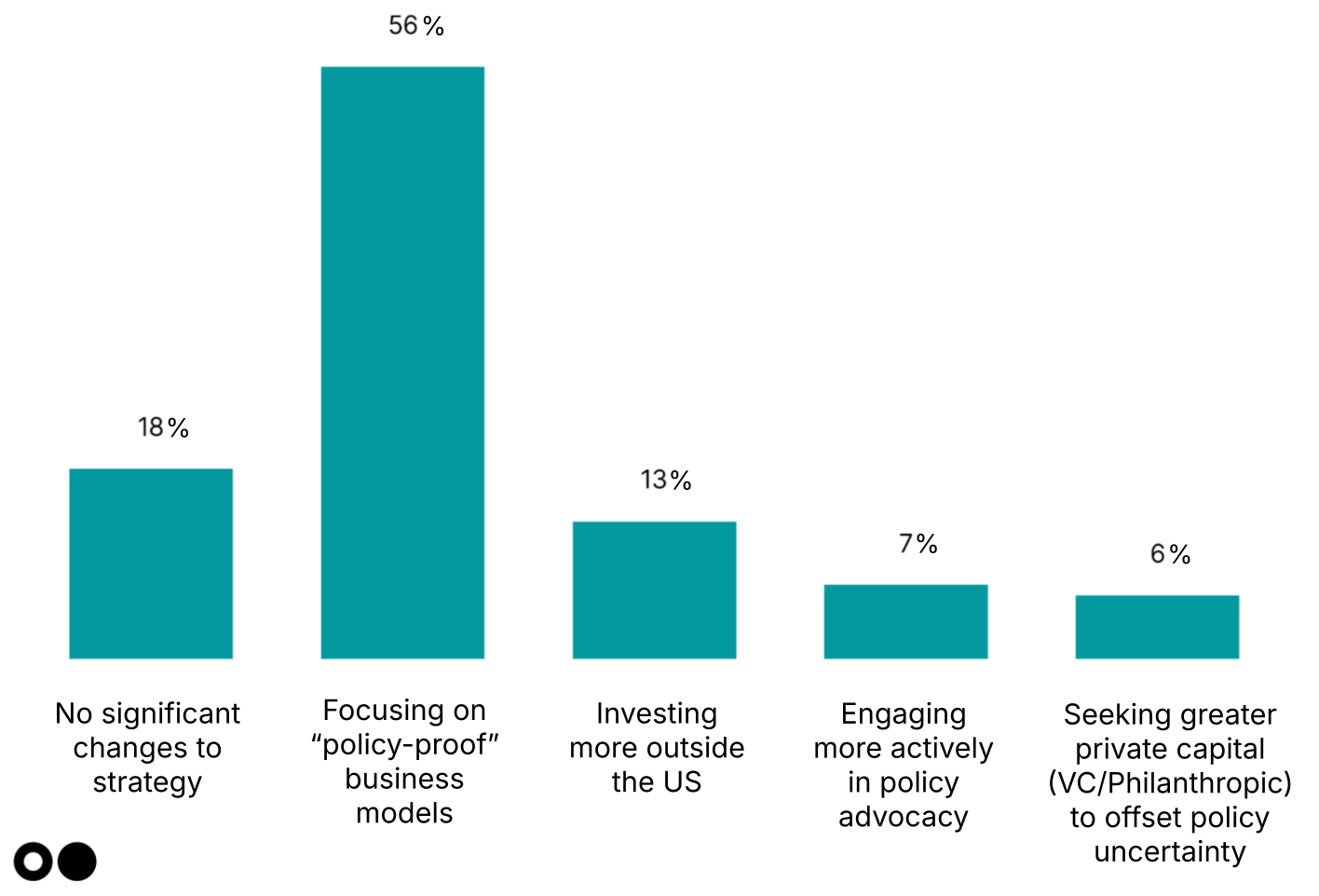

How are you adapting your investment strategy to the current political environment?

Investors are hedging against policy whiplash by backing climate tech that doesn’t depend on government tailwinds. “Policy-proof” business models, like behind-the-meter solutions, SaaS tools for decarbonization, waste heat recovery, or energy efficiency retrofits could pencil out on cost savings alone. With uncertainty around IRA implementation, tariffs, and permitting reform, investors are steering toward companies that can scale on pure market economics, no subsidy required. We do expect more to look overseas, as well.

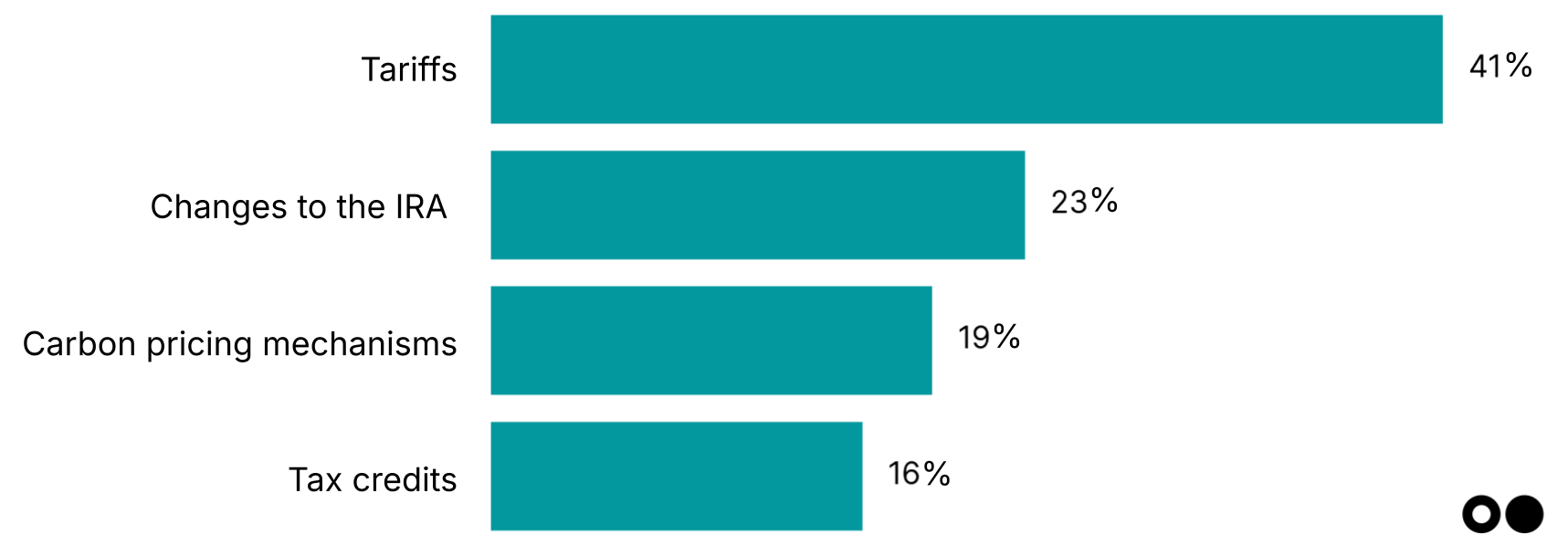

Which policy development would most significantly impact your investment thesis or portfolio companies?

Tariffs take center stage in investor risk calculus: 41% of respondents cited tariffs as the most impactful policy lever for their portfolio. With US industrial policy leaning protectionist and global trade tensions rising — and physical products made up the majority of deals (54%) in 2024 for the first time since 2021 — supply chain risk could hit hard for tech like solar panels, batteries, and heat pumps. Investors are bracing for cost volatility and supply chain reshuffling that could reshape manufacturing strategies and delay deployments, especially with tax credit and FEOC rule changes potentially on the horizon.

Investment trends & activity

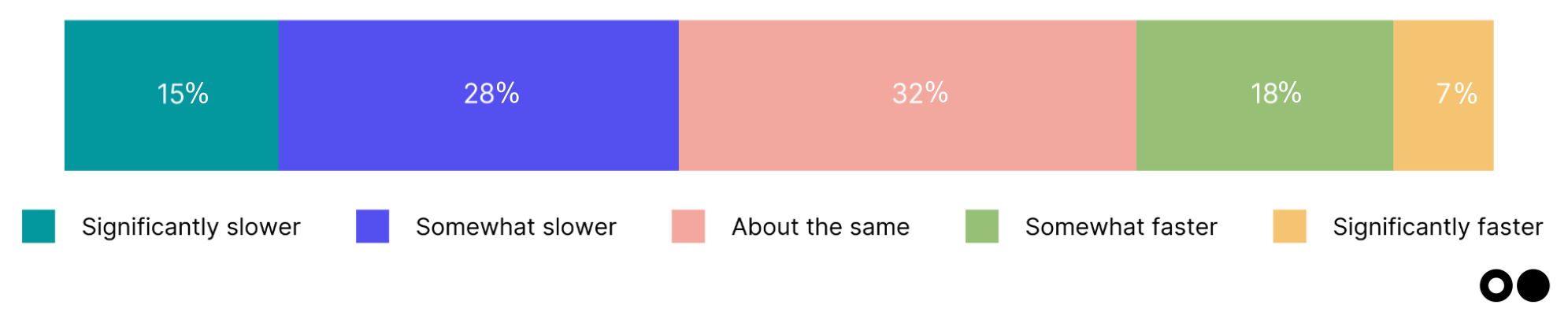

How would you characterize your investment pace over the past 6 months (Nov - Apr) compared to the 6 months prior?

To no one’s surprise, the mood is mixed. 32% say their investment tempo remained steady over the past six months, while 25% reported moving faster, hinting at growing confidence in certain subsectors or geographies. Still, 43% dialed things back, with many likely holding out for macro clarity, clearer policy signals, or improved capital efficiency from startups. The split signals a market in flux: not frozen, not frenzied.

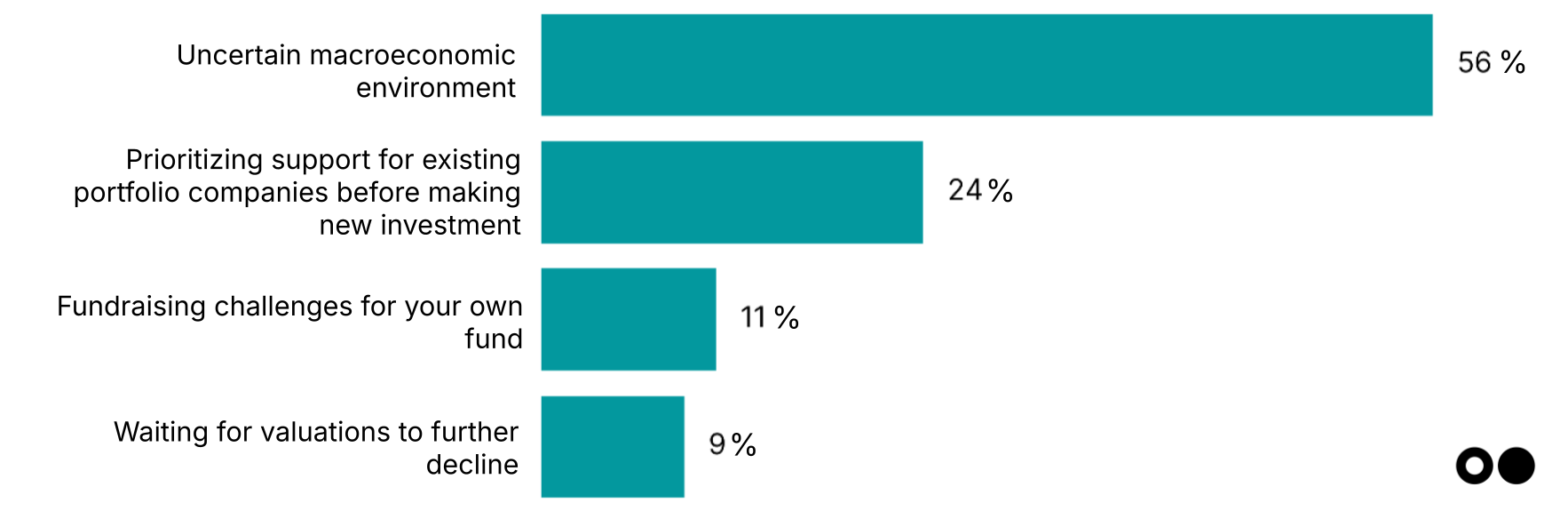

If you’ve delayed or slowed investment pace, what is the primary reason?

Macro clouds dominate the slowdown narrative. 56% of investors who’ve hit pause cite the uncertain macro environment, like high interest rates, sticky inflation, and geopolitical risk, as the top reason for dialing back. Another 24% are retrenching to support existing portfolios, signaling triage mode as runway extensions and inside rounds take priority. This fits with other trends in the investment space, like more bridge rounds among startups that can’t raise larger graduating rounds.

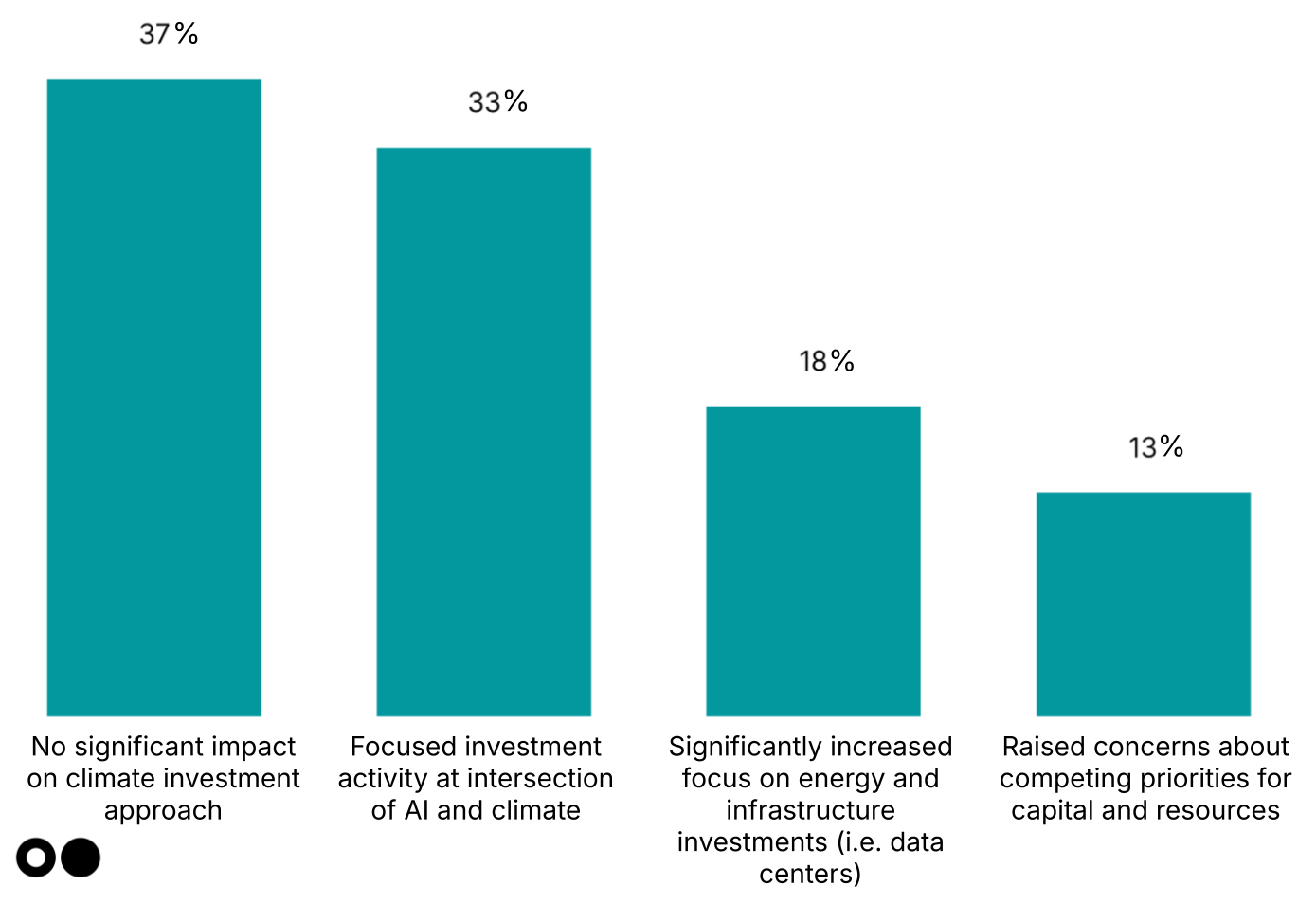

How has the emergence of AI influenced your climate tech investment thesis?

AI is reshaping investment patterns. The majority (33% and 18% together) are considering AI in decisions. Of course, AI power demand is creating new opportunities for startups in the energy space. We’ve even heard that some investors are backing earlier-stage startups with leaner teams, who can leverage AI to increase productivity.

Portfolio performance & fundraising

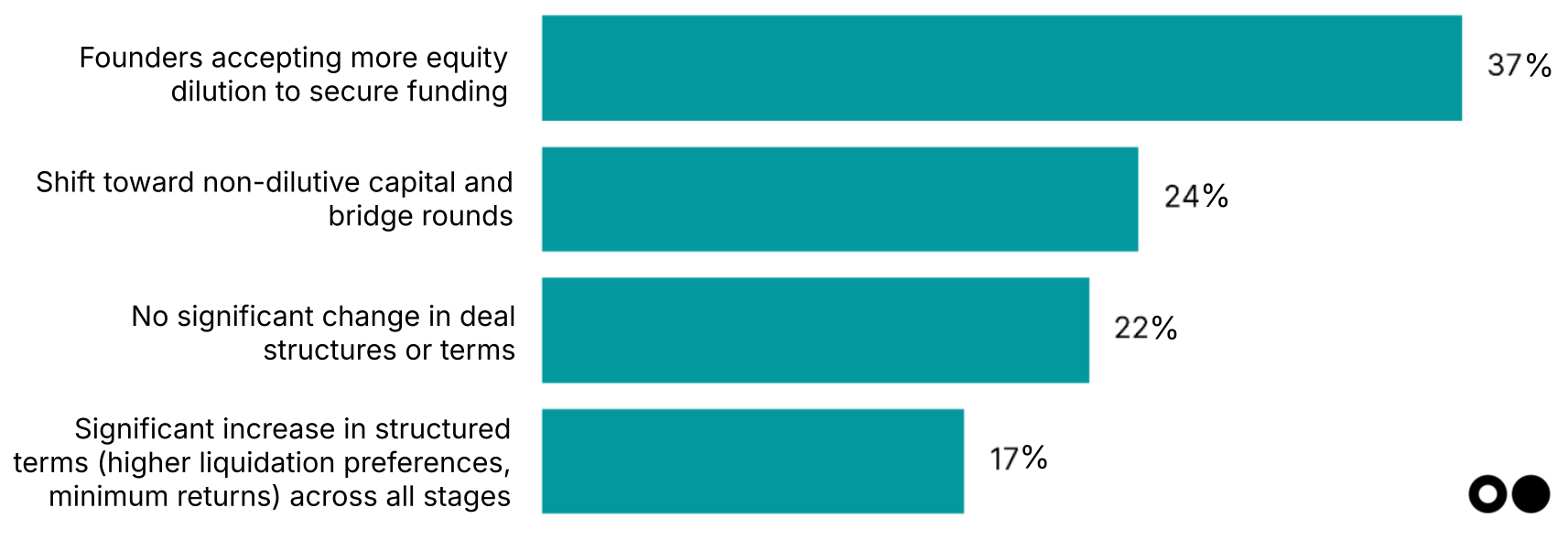

How have terms and structures in climate tech deals evolved over the past 6 months?

The capital stack is getting more creative, and more expensive for founders. In a colder market, 37% of respondents report founders accepting greater dilution to get deals done, while 24% highlight a turn toward non-dilutive capital or bridge rounds to stretch runway. But creativity comes with cost: structured terms like liquidation preferences and return minimums are rising (17%), meaning capital may be flowing, but on tougher terms. Founders are blending sources to close gaps, but often at the expense of ownership and flexibility.

Approximately what percentage of your climate tech portfolio is currently fundraising or expects to fundraise in the next 6 months?

Still raising. Most portfolios have 50%+ of companies heading into a raise. Companies need more cash, if they can get it. And that's not only full rounds, but we've heard from investors that many portfolio companies raised extensions in the past year, as startups stretch runway and investors prioritize supporting existing bets.

Role of Philanthropy

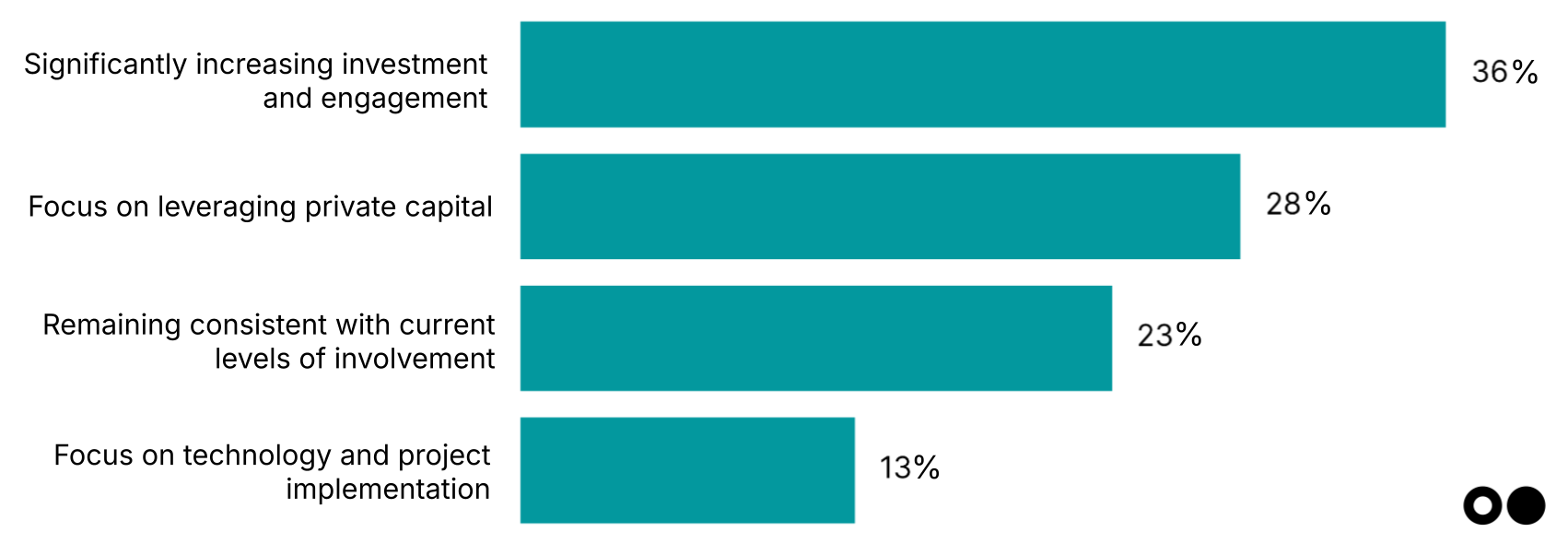

What role do you hope philanthropy will play in climate over the next 12 months?

Philanthropy is expected to play a catalytic, not charity, role in climate tech. Combined, 56% of investors want philanthropy to either significantly expand engagement (32%) or focus on leveraging private capital (24%) — a clear mandate for active deployment that unlocks commercial investment rather than passive grantmaking.

Recognition that philanthropic capital's highest value lies in de-risking opportunities for follow-on investors, not replacing them. Investors see philanthropy as uniquely positioned to bridge financing gaps through patient capital structures that commercial investors cannot provide.

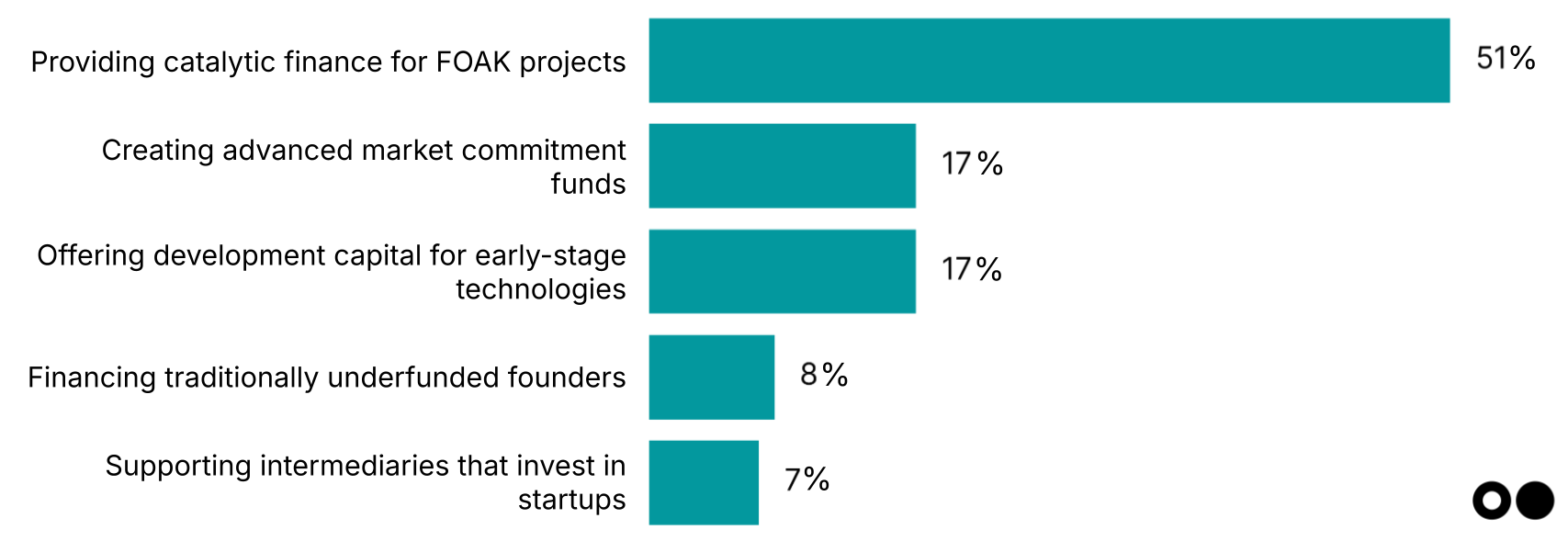

What’s the most catalytic role philanthropy can play in climate technology commercialization in the next 12 months?

Philanthropy has the opportunity to bridge the critical “valley of death” between technical proof and commercial viability. FOAK remains the critical bottleneck in climate tech scaling, and traditional capital consistently fails to bridge this gap. Half of respondents identify FOAK project financing as philanthropy’s most catalytic role over the next 12 months — more than double any other response. This confirms what Elemental has experienced firsthand: patient, risk-tolerant capital can transform promising climate technologies from pilot projects to bankable commercial assets. Case in point: Elemental's $500k-$2.25m investments have unlocked $13.5m-$384m in follow-on capital.

Final reflections

What’s one climate tech trend that you believe isn’t getting enough attention but will be significant in the next 12 months?

The top hits are there, but of note: workforce is a notably overlooked factor in climate tech scaling. Despite the capital-intensive focus of most climate discussions, one investor highlighted a critical blind spot: "If you don't pay attention to labor as a cleantech company, you will fail." Land use change projects — essential for agriculture and renewable energy development — cannot scale without addressing workforce realities. As climate technologies move from pilots to commercial scale, the availability of skilled and legally authorized workers may prove as constraining as capital availability — a reality that could derail even well-funded projects if not proactively addressed.

What’s your one-word or -phrase description of the climate tech investment landscape for 2025?

A massive thank you to Elemental Impact for their partnership in launching this survey, as well as analyzing the data and drawing insights. Follow Elemental Impact on LinkedIn here.

Note: Based on ~100 responses, most survey participants identified as VC / Early-stage Investors (45%), followed by Founders / Startups (16%) and Private Equity / Growth Investors (10%). The rest represented a mix of corporate, impact, infrastructure, philanthropic, and other investor types.

Newsletter

Newsletter