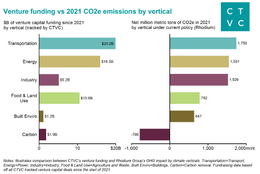

Rhodium: Taking stock of Paris targets

Late breaking ‘Inflation Reduction Act’ changes odds for the better w/ Rhodium’s Ben King

This past week, we Zoomed with Andy Karsner, Senior Strategist and Space Cowboy at X, the moonshot factory of Alphabet.

This past week, we Zoomed with Andy Karsner, Senior Strategist and Space Cowboy at X, the moonshot factory of Alphabet. Karsner has been a leader in energy financing for 30 years and is also founder and Executive Chairman of Elemental Labs and a Precourt Energy Scholar at Stanford University. He was most recently Managing Partner at Emerson Collective and leader of Elemental, its environmental practice. Karsner has been involved as an investor with numerous successful technology startups over the last 10 years, including Nest (Internet of Things), Tesla (mobility), Recurrent (solar), and Codexis (biotech). From 2005 to 2008, he served as Assistant Secretary of Energy for Efficiency and Renewable Energy of the United States, managing the approximately $2 billion annual federal applied science, research and development portfolio.

The question sounds simpler than it is. Neither funding source is uniform. Within private capital, project finance differs significantly from venture capital. It’s the same with public money. Public loan guarantees differ from ARPA-E (government funding for early-stage moonshot projects).

It is more useful to focus on the merits of a project instead of its funding source. If an effort is worthwhile and the public has a stake in its success, public policy instruments can be marshalled to support it. However, public money is usually limited and slow-moving (excluding during crisis situations like the pandemic), so public capital often lacks the scale and agility to solve problems alone.

The question becomes how to get private markets moving in the right direction. Private capital, philanthropic capital, and market-based solutions do remarkably well when properly incentivized and deployed for longer, more patient cycles. Private markets in the U.S. can be highly effective, but they are usually constrained by having a singular goal of maximizing profitability. These markets do not inherently promote national strategic priorities or humanitarian values. We need leaders with foresight to encourage investment in areas where there is a pressing need for a public good. Unfortunately, politics today often consists of polarized coalitions that impede making decisions that advance our interests. Too much political dysfunction yields too little policy efficacy or consistency to achieve predictable market signals.

I like and dislike the term “climate tech.” On the positive side, the “tech” label encourages dialogue by providing a platform for people to exchange ideas. “Tech” is also a priority for investors, so the term alone can help spur capital formation. That’s why investors are more likely to subscribe to a newsletter about “climate tech” than “climate solutions,” even if they address the same topics. I like the climate tech space because it galvanizes enthusiastic smart minds to develop new ideas that improve our world.

On the flip side, “climate tech” is a misnomer. It suggests a distinct category when, in reality, it has expanded to encompass innovations that are not focused on climate issues. These technologies might still address climate change indirectly by boosting energy efficiency, for example, in a way that is good for the environment. And, while some solutions deemed to fall within the climate tech space are not climate-focused, some others are not technical.

In this context, we should ask not only whether a solution is “climate tech” but also if it is “climate optimal” ̶ how much will it help the climate, and how fast will it work? This is not to say we should look for a single remedy. To the contrary, climate change will require aggregating and scaling many incremental solutions.

Some people say that we should not focus on climate change now because doing so will distract from our efforts to contain the pandemic. Of course, we cannot separate one from the other – they are interconnected. Both the pandemic and climate change are Mother Nature’s invoice that we need to pay for disrupting the environment. Both the pandemic and climate change emerged from nature’s responses to human activity. Moreover, both problems require urgent action.

The pandemic offers a glimpse of the potentially catastrophic results of ignoring climate change and should motivate us to move quickly. At the same time, the expedited global response to the pandemic offers insight into how we can slow or stop global warming. We have become united in a race for a vaccine because we generally agree that it is critical for a recovery. The climate crisis is the same in that we know what we have to do to solve the problem. The climate “vaccine” may be deep decarbonization, a reduction of the amount of CO2 in the atmosphere.

Unlike a vaccine treatment, we will not cure climate change with a single injection. Rather, we must change our behaviors (together with using better technology) as though we are managing diabetes. Placing a premium on carbon reduction efforts can unlock the race to a climate “vaccine.” Many of the technologies that can help us achieve this goal are within reach. It needs to be a race so we can bend the curve as soon as possible. Every day that we wait, the curve gets steeper, so we need to employ the same vigor to address climate change that we apply to developing a vaccine. Public funding and good regulation can mobilize private capital and help spur efforts to find and implement climate solutions.

We use an old-school monopoly model for distributing energy. The question is how to adapt legacy physical assets to enable rather than impede growth. Grid connectivity is the key to transitioning to cleaner electrons at scale. We need to think of our existing assets and grid connectivity as we do our interstate highway system ̶ like a public good. The grid and distribution system should be thought of as an accessible common market and a source of innovation. Just as internet connectivity launched a new economy, we should encourage the democratization of grid access and production, storage and use of clean electrons.

In the private sector, oil companies should think of themselves as energy companies. They need to view their most valuable asset not as reserves of thermally-pressurized, liquified dinosaur bones but as the intellectual capital of physicists, scientists, and engineers. If they continue to think of alternative energy as a threat instead of an opportunity, they could wind up like Blockbuster, which saw streaming as a challenge, instead of becoming Netflix. They are running low on time to avoid the fate of Kodak and GE – once titans thought to be indomitable.

Offset programs scaled at the federal level during Republican administrations, starting with Bush and Reagan policies to address acid rain. These programs imposed a cost on companies that lacked scrubbers on their smokestacks. They had to pay an amount equal to or greater than the price of the scrubbers for the offsets. These costs motivated them to reduce pollution, which helped ultimately address and eliminate the acid rain problem. So we have experience that offsets can work. You would think that since offset policies were successful in Republican administrations, there might be more bipartisan support for them, but today’s polarized politics still impedes their adoption. There are also technical challenges. Carbon is a much larger problem and less addressable than the gases targeted with the acid rain project. This does not mean that offsets are not valid, but the approach needs targeted reform so it can scale to address this global problem.

Offset markets and programs are still in nascent stages of development. These programs have adopted disparate approaches and verification practices. The discrepancies allow some buyers to value offsets in questionable ways that can undermine trust in the market. We should strive to standardize and validate these markets. If we had global liquidity in the market for offsets, and they were measurably consequential to things that were inelastic to their demand, like jet fuel, we could make big advances towards market design for decarbonizing the environment.

Regarding business-as-usual, an effective offset regime is not one that encourages a big company to buy offsets while continuing to use coal unabated. Rather, a properly-devised program should encourage companies to reduce emissions where possible and to purchase offsets for decarbonization projects that equate to the amount of unavoidable emissions.

The most important, empirically effective and scalable CO2 converter, by far, is trees. We are in a race to preserve (or biomimic) trees to reduce carbon, while seeking man-made solutions to sequester and recycle it.

The supply side needs to continue to work to develop credible offset products. Many offset programs are still too informal to achieve the scale needed to meaningfully offset carbon. For example, some companies determine an internal cost of carbon in their own investments or take the social cost of carbon given by DC and pay the NGO $2 or $3 per ton of CO2 for an offset. That is not a market; it is an experimental exercise in “innovative” environmental finance. To be widely adopted, offsets need to follow broadly adopted, transparent, and verifiable standards. Until carbon offsets can trade on NASDAQ or NYSE, for example, at scale, the market will be sub-optimal. If these programs are widely adopted, there are enormous carbon stores in nature that have yet to be properly authenticated for offset projects.

To increase demand for offsets, we need more credible, scalable, and reliable technologies to monitor our treatment of the natural environment, just as we do with the manmade one. Moreover, these systems need to provide information in a standardized way. I am keenly interested in synthesizing information from various technologies to achieve these goals.

Until now, offset markets have been largely in the province of academics and NGOs. As governments and businesses become more confident that offsets are properly valued and are fulfilling their intended purpose, entities are likely to purchase offsets with reliable, verifiable information platforms. And as demand for offsets increases and they become easier to monetize, participants will create more robust and transparent markets.

If purchasing offsets were required and not voluntary, they would become another compliant cost of doing business that would align markets and commerce with science and technology. Businesses would be motivated to reduce their emissions to improve their bottom lines. We will know when ESG (environment, social, and governance) has become a priority when companies boast of their non-economic achievements as much as they do of their economic performance.

Interested in more content like this? Subscribe to our weekly newsletter on Climate Tech below!

Late breaking ‘Inflation Reduction Act’ changes odds for the better w/ Rhodium’s Ben King

Out in front on carbon removal, Nan Ransohoff sets a new tier for climate leadership with Frontier

John Doerr and Ryan Panchadsaram's new book on OKRs to get to Net Zero

Experts

Experts

Investors

Investors