The missing link to net zero

Closing the loop on decarbonized & resilient supply chains with Energy Impact Partners' Nina Litman

When Larry Fink pens a letter, people read it. From his January 2021 letter to CEOs, he puts it simply as “climate risk is investment risk” and warns that “no issue ranks higher than climate change on our clients’ list of priorities.”

When Larry Fink pens a letter, people read it. As the head of Blackrock, the world’s largest asset manager, his prose signals a State of the Union for institutional investors. From his January 2021 letter to CEOs, he puts it simply as “climate risk is investment risk” and warns that “no issue ranks higher than climate change on our clients’ list of priorities.”

Indeed, Blackrock is “asking companies to disclose a plan for how their business model will be compatible with a net zero economy” while, at the same time, the pace picks up on federal climate finance appointees. The US Fed tapped Kevin Stiroh to lead the Supervision Climate Committee to study climate’s impacts on banks and financial markets, while Janet Yellen vows to set up a climate team at the Treasury. New Zealand and the UK have already mandated climate disclosures by 2025, and – for the first time ever – the US Fed biannual stability report notes climate change as a material risk.

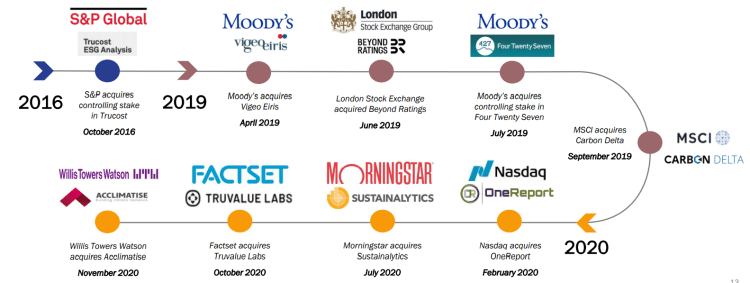

Fundamentally, finance is a balance of pricing risk versus return. Climate change’s epochal disruption of scientific and societal systems seriously threatens to disturb this balance. Despite work by early movers like sustainability data companies and some insurance players, the financial industry doesn’t yet have a solid handle on incorporating this climate risk (and opportunity!) into their models. Of course, climate change isn’t slowing down; climate poses material risk to both short- and long-term portfolios. Banks and asset managers have a fiduciary duty to incorporate this risk, especially as access to insurance and credit starts to feel the squeeze. The market is hungry for climate risk scores and ratings, and acquirers have certainly already made their appetite clear with a frenzy of acquisitions.

For an industry that is no stranger to regulation, structure, and standardization, the financial sector has so far lacked rigor around measurement of climate risks. National regulation will enforce adoption, likely through existing leading standards such as The Task Force on Climate Related Financial Disclosure (TCFD) and the Sustainability Accounting Standards Board (SASB), which is sending corporates scrambling for technology and resources to meet anticipated disclosure standards. “The TCFD provides a framework for understanding climate risk. In the TCFD, risks are broadly categorized into ‘physical’ and ‘transition.’ Physical are risks to assets (facilities, supply chains, etc.), from hazards like extreme temperature, drought, wildfire, flooding, and more. Transition risk refers to the changing legal, regulatory, and market conditions that can impact a business,” James McMahon CEO of The Climate Service explains.

Supported by expansion of earth science data collection methods such as satellites, drones, and sensors superpowered by ML and AI, a number of companies have emerged which can harness climate data, in combination with physical and financial asset data, to measure and manage the varied impacts of climate change. OS-Climate, hosted by the Linux Foundation, is one such effort to promote open-source data and analytics around climate risk, and recently announced Goldman Sachs joining its ranks. As Amy Francetic, co-founder of Buoyant Ventures, a VC fund focused exclusively on “digital solutions for climate risk” notes, “we see a tremendous opportunity for new companies to build on, and improve, the work of pioneers in the climate risk intelligence sector to assess physical risk. We are excited to see new entrants developing solutions that can be used to manage risk – both physical and transitional – as we drive towards a decarbonized economy.”

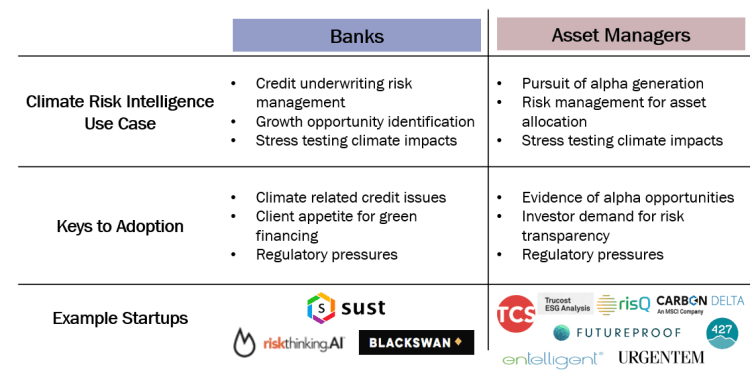

Below we’ve highlighted several innovative startups solving the different pain points within the financial sector faced by banks and asset managers:

Climate Disclosures and Reporting (TCFD): Voluntary set of recommendations for companies to offer disclosure around governance, strategy, risk management, metrics and targets.

Sust Global addresses the inconsistency, low resolution, and complexity of today’s physical climate risk data with the aim to improve that data so it can integrate into day-to-day operations and financial decision-making. They fuse frontier climate models, satellite based observations and geospatial data streams with proprietary machine learning techniques to improve the spatial and temporal resolution of climate data. They transform these data sources to enable predictive analytics on monthly, annual, decadal and multi-decadal time horizons to create transparent and meaningful financial indicators.

Sust Global provides asset-level geospatial insights on chronic and acute climate hazards. Each specific asset has a different exposure to physical hazards, and a unique financial and operational vulnerability to these perils. Sust Global provides insights and indicators to partners and customers to estimate, quantify and model forward-looking losses. They help their clients to comply with – but also go beyond – climate disclosure and reporting practices (e.g. TCFD and SASB compliance), to embed climate risk indicators across operational workflows in financial institutions, corporates and supply chains.

The Climate Service built the Climanomics® platform, a SaaS technology which enables climate risk reporting and disclosure aligned with the TCFD framework. Based on principles similar to catastrophe risk models, but driven by climate and socioeconomic data, their methodology employs peer-reviewed climate projections—merged with customer asset data and econometric impact/hazard functions—to model vulnerabilities. Inputs, including terabytes from public (IPCC, NASA, NOAA), academic and commercial sources, and proprietary TCS models, are updated as new sources become available or desirable. Their rapidly growing proprietary library of impact functions, modeling the vulnerability of individual assets to individual climate-related risks, is a key differentiator.

In financial services, the Climanomics® platform is used to assess the physical and transition risks and opportunities from climate change in equities, commercial mortgage-backed securities, real estate, agricultural assets, sovereign and corporate bonds. It can also be used to assess the climate risk in the lending portfolios of global banks. The company plans to launch a new set of products on the platform giving investors even deeper insights into financial instruments.

Climate Risk Modeling/ Stress Testing: Data to generate scenarios and measure the financial risk under extreme conditions (stress test).

RiskThinking.AI has developed a data and analytics platform to compute the climate financial risk of portfolios and physical assets for large asset managers, custodians, as well as corporations, and governments. They are releasing a Climate Risk Data Exchange that will be regulatory ready and standards-driven. Their database covers the entire world, bringing together in a consistent manner a variety of different types of climate, economic, financial data from 1850 to forward-looking scenarios to 2100. The system offers a unique functions to compute forward looking risk using Structured Expert Judgement and Machine Learning, which also draws on scientific knowledge from latest literature . They’ve also created a standard, not unlike GICS for Equities[G3] , for climate change, based purely on climate science and understanding of key climate drivers These offerings allow clients to rate their activities in a consistent manner and their CaR (Climate-risk Adjusted Return) rating can even be aligned with bonuses to reward “good” climate behavior.

Riskthinking.AI has developed patented algorithms for generating forward looking multifactor scenarios. They are the only company offering this unique and necessary feature. Multifactor scenarios are important for stressing climate events which mainly occur through interlinkages of risk factors. They calculate the full frequency distribution of gains and losses in portfolios under different transition scenarios and the physical risk of assets. This gives them the unique ability to create climate risk ratings for portfolios, funds, physical assets and entire business units.

Climate-Related Property and Physical Risks: Assessment of sectors which directly face climate-related risks (e.g. mortgage backed securities, municipal bonds)

risQ models a mixture of geospatial catastrophe, climate change, economic and social scenarios. They’re laser focused on the US Fixed Income market – both municipal bonds and mortgage backed securities – because (a) these real-asset backed markets are existentially threatened by climate change and (b) they also have the financial tools, incentives, and structures in place to actually start funding climate action and investments at scale. risQ works with all of the key stakeholders of the municipal bond market: i) investors to understand climate risk and manage it in their portfolios; ii) ratings agencies to understand and incorporate into their methodology and business; iii) muni bond insurers to inform what bonds they will insure; iv) sell-side firms and advisors to position climate risk as issuers come to market, and v) issuers to quantify the economic and social cost-benefit tradeoffs for climate adaptation projects.

Beyond just climate risk, risQ also adds rigorous analytics on socioeconomic dimensions to the growing ESG market, with a focus on historically marginalized and disenfranchised communities.

Special thanks to the team at Buoyant Ventures, a venture firm focusing on digital solutions for climate change, and Sophie Logan for their thought leadership and expertise.

Interested in more content like this? Subscribe to our weekly newsletter on Climate Tech below!

Closing the loop on decarbonized & resilient supply chains with Energy Impact Partners' Nina Litman

The new business of seeing climate from space

Carbon

Carbon

Climate Risk

Climate Risk

Founders

Founders