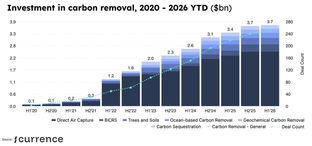

🌎 Pushing the Frontier for carbon removal #301

Inside the $915m bet on carbon removal's next phase

We read the S-1s so you don't have to

Happy Monday!

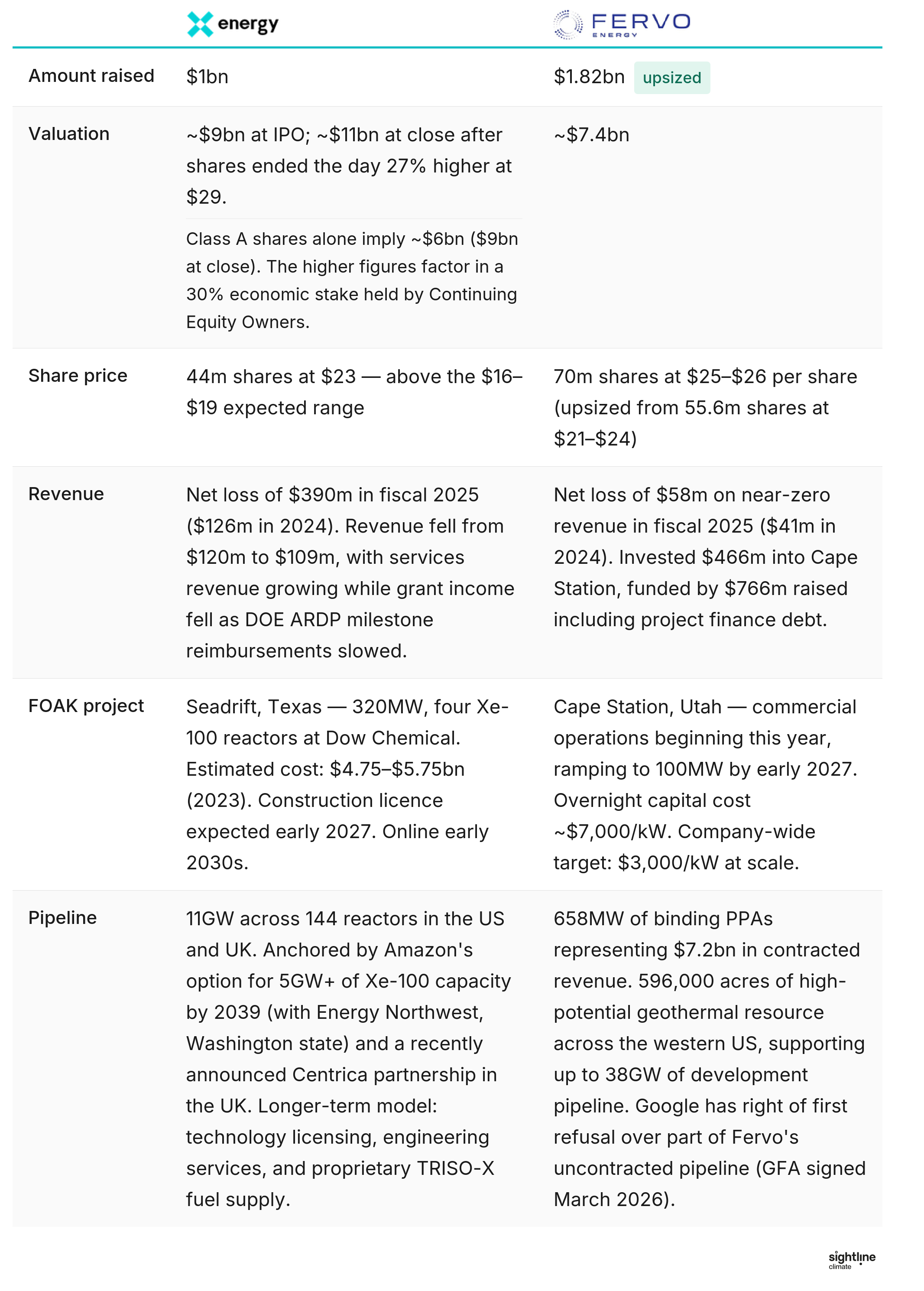

We went through Fervo and X-energy's S-1 filings so you don't have to. The numbers are the clearest window yet into what clean firm actually costs.

In deals, $140m for wave power, $60m for ultra-fast charging, and $40m for EV battery repurposing.

In other news, regulatory tailwinds for microreactors, Blue Energy gas-to-nuclear hits new milestone, and European batterymaker Morrow goes out of business.

Thanks for reading!

Not a subscriber yet?

📩 Submit deals and announcements for the newsletter at [email protected].

💼 Find or share roles on our job board here.

CTVC is powered by Sightline Climate, the tactical market intelligence platform for energy and investment decision-makers.

It’s a big moment for our sector. Two darlings are making their debut: advanced nuclear reactor company X-energy has officially IPOed, and enhanced geothermal systems developer Fervo Energy has filed to.

Luckily for us, these IPO and SPAC filings bring more disclosure on costs, timelines, and project economics. So we took a peek at the S-1s, and they give us the clearest window yet into what clean firm actually costs to build.

Fervo and Google's deal stands out. Google is the first to lock down the first real shot at scalable clean firm in a while. Fervo has better economics, earlier revenue, and cheaper capital than any comparable startup, and Google wants to get a piece of that pie. The GFA signed in March gives Google right of first refusal over part of Fervo's uncontracted pipeline and downside cost protections. Given Fervo is the only developer likely to bring hundreds of megawatts online in the coming years, it's a solid bet.

Fervo doesn't need to hit its cost targets to build a big business. Even at $5,000/kW — short of the $3,000/kW goal — its LCOE would be around $100/MWh, a price point with massive demand. With low operating losses, project finance capability, and $7.2bn in contracted revenue not far off, Fervo is in great shape.

X-energy, meanwhile, is a bet on nuclear licensing — notoriously tough, lengthy, and expensive. The company is burning cash before the hard part starts: a $390m net loss before FOAK construction has begun, a construction licence not expected until 2027, and an analogue project that took 11 years to reach commercial operation. It will need billions more in equity before it generates meaningful power revenue.

🌊 Panthalassa, a Portland, OR-based wave-powered renewable energy technology developer, raised $140m in Series B funding from Peter Thiel, Anthony Pratt, Dylan Field, Fortescue Ventures, Founders Fund and other investors.

⚡ Nyobolt, a Cambridge, England-based ultra-fast charging battery developer, raised $60m in Series C funding from Symbotic, CBMM, IQ Capital, Latitude, and Scania Invest.

♻️ Moment Energy, a Coquitlam, Canada-based EV battery repurposer, raised $40m in Series B funding from Evok Innovations, Acario Innovation, Amazon Climate Pledge Fund, In-Q-Tel (IQT), Liberty Mutual Investments, and other investors.

🪨 Lithosquare, a Paris, France-based AI-driven critical mineral explorer, raised $25m in Seed funding from Kindred Capital, World Fund, Daphni, OVNI Capital, and Omnes Capital.

🏗️ Terra CO2 Technology, a Golden, CO-based supplementary cementitious materials maker, raised $22m in Series B funding from All Aboard Coalition.

⚡ Reel, a Copenhagen, Denmark-based renewable energy procurement platform, raised $18m in Series A funding from Future Energy Ventures, The Footprint Firm, Transition VC, and UVC Partners.

🥩 Meatly, a London, England-based cultivated meat for pets company, raised $14m in Series A funding from Clean Growth Fund, JamJar Investments, and Oyster Bay Ventures.

🌿 Trillium Renewable Chemicals, a Knoxville, TN-based bio-based chemical manufacturer, raised $13m in Series B funding from HS Hyosung Advanced Materials and Capricorn Partners.

❄️ Barocal, a Cambridge, England-based solid-state cooling systems producer, raised $10m in Seed funding from Breakthrough Energy Discovery, Cambridge Enterprise Ventures, IP Group, and World Fund.

🔥 Reduciner, a Helsinki, Finland-based industrial CO2-to-fuels developer, raised $4.2m in Seed funding from Lifeline Ventures, Mikko Kodisoja Foundation, and Voima Ventures.

🌾 vGreens, an Essen, Germany-based precision agriculture software platform, raised $2.3m in Seed funding from Christ Capital, Dürr Group, Frutania, Guido Kerkhoff, Ulrich Wolters, and other investors.

🪨 Alkemio, a Berkeley, CA-based modular rare earth refiner, raised $2.0m in Pre-seed funding from Amplifica Capital, Dalus Capital, Epic Angels, VU Venture Partners, and VX Ventures.

♻️ Humara, an Ourense, Spain-based software platform that optimizes waste and recycling, raised $1.4m in Seed funding from Impact Shakers, Inclimo, Ship2B Ventures, and Zubi Capital.

💡 ENVIOTECH, a Frankfurt am Main, Germany-based smart streetlight retrofit kits maker, raised $1.2m in Pre-seed funding from Jürgen Fitschen and Joachim Drees.

🌍 Geothermal Engineering, a Cornwall, England-based geothermal energy developer, raised $14m in Debt funding from ABN AMRO.

🌋 Fervo Energy, a Houston, TX-based enhanced geothermal systems developer, announced an IPO filing targeting $1.3bn, at a valuation of up to $6.5bn.

⚡ ENGIE Impact, a NY-based utility expense management, energy procurement, and sustainability advisory, was acquired by Arcadia for an undisclosed amount.

⚡ Bluedot, a San Francisco, CA-based EV charging payments platform, was acquired by Epic Charging for an undisclosed amount.

♻️ General Equipment Acceptance Corporation, a West Chester, PA-based waste handling equipment leasing company, was acquired by BP Environmental Services for an undisclosed amount.

🌱 CEMAsys, an Oslo, Norway-based ESG software and consultancy, was acquired by Energi.AI for an undisclosed amount.

🏭 KOMPAS VC, a Copenhagen, Denmark-based venture capital firm focused on industrial technology and decarbonisation, closed $188m for its Fund II, to invest in early-stage startups across manufacturing, energy, logistics, the built environment, and advanced materials in Europe and North America.

⚡IKAV i-BESS Co-Investment Fund, a Hamburg, Germany-based utility-scale battery energy storage fund managed by IKAV, completed a first close of $88m to invest in utility-scale BESS projects in Germany.

🔬 Surround Ventures, a New York, NY-based venture capital firm focused on deep tech for defense, biotech, quantum computing, and AI for energy and infrastructure, completed a first close of an undisclosed amount for its second fund.

This is a sample of deals available for Sightline clients. Can’t get enough deals?

☢️ The NRC proposed Part 57, a new regulatory framework that would actually make microreactors viable. It removes barriers around shipping fuel loaded reactors, eases site security requirements, and introduces fleet licensing instead of individual approvals. [Link, Link]

This is the unlock the microreactor space has been waiting for and Radiant looks like the biggest winner here. Pair this with DIU's recent Advanced Nuclear Power for Installations selections and you have an emerging procurement + regulatory tailwind for the category.

☢️ Blue Energy announced GE Hitachi as its nuclear partner for its 2.5GW Texas FOAK, with 1GW of gas power potentially online by 2030 and nuclear coming in 2032 at the earliest. [Link]

GE Hitachi is arguably the best partner Blue Energy could have landed, aligned with its heavy deployment and financial risk mitigation focus. The gas bridge to nuclear sequencing also leapfrogs many advanced nuclear FOAKs that are still pre-construction.

🔋 Morrow files for bankruptcy, the latest European battery maker that can't compete with China on price. [Link]

European battery startups are stuck between two impossible options: compete on price against vertically integrated Chinese giants (CATL, BYD have cost advantages at every stage of production), or differentiate on sustainability/supply chain security and hope premium buyers show up. So far, the premium and state-level support haven't been enough.

💨 Fertiberia signed a deal to supply PepsiCo with up to 150,000 tonnes of green hydrogen-based fertilizer annually. [Link]

It’s a significant offtake agreement for green hydrogen, which has been struggling. But big F&B investments could help unlock this use case for hydrogen, and the scale here alone is meaningful for one of the toughest hydrogen offtake categories.

📊 SEC is scrapping climate risk reporting requirements, but also moving away from quarterly reporting. [Link]

Killing the public company climate disclosure rule is the headline - but Republicans have long been fighting against this rule. Meanwhile, the shift away from quarterly reporting could have potential benefits, as quarterly cycles are capital intensive and punish long-payback climate investments. Less short-term focus could benefit to long-term climate projects.

⛽ Gulf state sovereign wealth funds may be exploring war related force majeure to exit binding climate finance commitments. With ~40% of global sovereign wealth coming out of the Gulf, this could put trillions in pledged climate project finance at risk. [Link]

The projects in the region mostly include data centers, alt fuels, SAF, and CCS. Force majeure clauses don't apply selectively, but if possible, the ones most likely to be abandoned are the ones whose economics have soured.

⛏️ USGS finds eastern US hard rock lithium reserves could replace imports for "a century or more." [Link]

Permitting, infrastructure, and processing capacity timelines for developing these resources mean minimal short-term impact on critical mineral security or domestic battery supply chains.

🚢 US mounts another new bid to block international shipping carbon tax. [Link]

🌎 Ted Turner: a media mogul who tried to repair the land. A profile of the largest individual landowner in the US and his decades-long bet on bison, conservation, and ecological restoration. [Link]

⚡ New IRENA report: solar + BESS is now eating clean firm power's lunch on economics. [Link]

🛢 Meanwhile, Fermi's gas-to-nuclear strategy unraveled, CEO ousted after stock slid. [Link]

💡 Hannah Ritchie's latest take on AI electricity demand, with a more measured read of the data than most. [Link]

🚗 EVs in Europe going gangbusters, with sales accelerating despite the broader auto market crunch.

📅 Tailoring Your Pitch: Storytelling for Early-Stage Fundraising in Climate: On May 28, from 11am to 12:30 pm PT, join Enduring Planet and Friends for a 90-minute session on building a compelling fundraising narrative — covering financial storytelling, communicating impact, and breaking through the AI hype cycle to capture investor attention.

📅 Renewable Energy & Climate Tech @ National MSC Conference & Expo 2026: On May 27-28 in Dublin, from 9am to 4pm, join Premier Publishing & Events for two days of talks, networking, and expo floor exploration covering the latest in renewable energy and climate technology.

📅 Carbon to Value Initiative Year 5 Showcase: On June 3 in NYC, from 4:30 to 7:30pm, join us for an evening of engaging connections and celebration of the C2V and wider carbontech ecosystem with large industrials and 10 up-and-coming carbontech startups.

📅 Trellis Impact 26: From Jun 23-25 in Moscone West, San Francisco, Trellis Impact brings together 3,500+ leaders powering the future of sustainable business, from AI-enabled solutions to emerging technologies reshaping decarbonization, energy, circularity, and beyond. Get practical insights and hard-won examples of the technologies and strategies that are influencing sustainable business transformation. Register by May 15 before prices go up, and you can get 20% off with our partner code: TI26SCP.

Head of Finance, Investor @Gigascale

Analyst Trainee, Program Specialist Trainee, Bureau Chief of Budget & Procurement, Deputy Director of Grid Scale Resources, Deputy Director of Virtual Power Plants, Director of Clean Energy Planning & Analytics, Bureau Chief of Grid Scale Resources - Division of Clean Energy, @New Jersey Board of Public Utilities

Marketing Lead, @Glimpse

📩 Feel free to send us deals, announcements, or anything else at [email protected]. Have a great week ahead!

Inside the $915m bet on carbon removal's next phase

A letter from the co-founders, Kim Zou and Mark Taylor

Newsletter

Newsletter