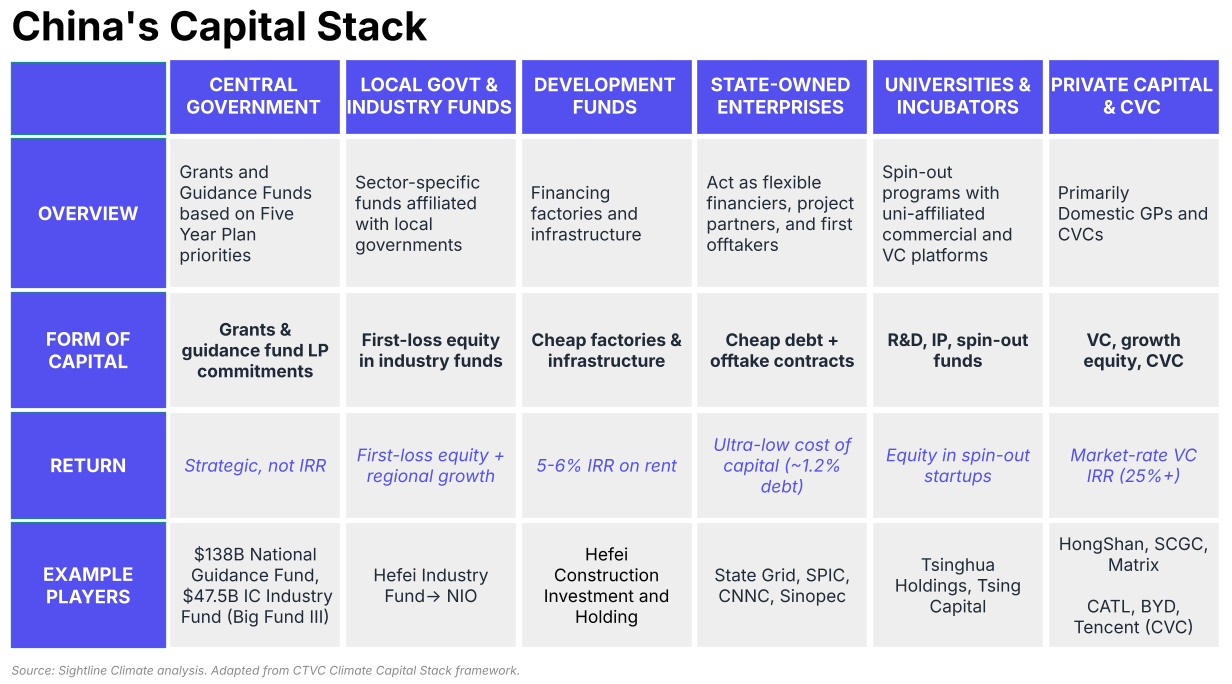

How Beijing mobilizes an entire capital stack to become the Electrostate

In the West, the Climate Capital Stack is layered with private capital, from VCs to infra funds (see Sightline’s latest dry powder report here). China’s stack is built different. State funding and direction leads, then private capital follows – call it one of the world’s best examples of public-private partnership.

And as a result, China dominates clean tech manufacturing, producing 80% of the world’s solar panels, 70% of its EVs, and 75% of batteries. In 2025, China invested $1T into clean energy, which accounts for 11% of its GDP.

That’s no accident. China has a tightly-knit capital architecture where government capital de-risks private investment at every stage. Its government is the leading investor in the venture capital/private equity market in China, investing six times more capital than private investors.

And it’s not just capital. Central policy sets the direction, local governments and industry funds provide equity and build (almost) rent-free factories, state-owned enterprises (SOEs) inject ultra-low-cost debt, and government procurement guarantees the first customer. Here's how it all works.

The central government starts at the top of the stack with grants through the Ministry of Science and Technology and “central guidance funds,” essentially venture funds run by the state. Guidance funds have become the dominant force in Chinese VC, prioritizing national goals, local economic development, and job creation, over pure IRR. In March 2025, Beijing announced a $138bn National Guidance Fund (fund of funds directing capital to GPs) to make long-term investments in cutting-edge tech like quantum computing and robotics.

Two features of the fund stand out:

Alongside this fund, Beijing also has the National Integrated Circuit Industry Investment Fund with $47.5bn raised in May 2024 targeting semiconductors, advanced materials, and AI infra.

From there, most of the action happens one layer down. Local fiscal funding flows through five levels of government – city, town, county, municipality, province.

Industry funds are government-affiliated funds that focus on specific sectors. The local government typically will contribute 20-30% as first-loss capital, with social capital from local existing companies filling in the rest. Think of it like a combo government x CVC fund. For example, in a Fujian energy storage fund, the Fujian province could provide 30%, CATL contribute another 20-30%, and other strategics or foreign partners make up the balance.

Case study: Hefei (capital of Anhui province) and NIO

In March 2020, when NIO was close to bankruptcy, the Hefei industry fund pledged ¥5 billion (~$787M) for a 17% stake in NIO’s core business. Within a year, NIO stock rallied and the city exited most of the position at a ~5.5x return. The real payoff was the city's economic growth. NIO moved its HQ to Hefei, suppliers followed, and the city became the gravitational center of an EV supply-chain cluster that today draws CATL’s investment into NIO’s battery-swapping arm and feeds downstream manufacturing across Anhui.

Hefei runs this through what local officials call a “chain leader system” (链长制): each strategic industry gets a designated political owner who spends years mapping the supply chain, identifying the critical nodes, and deploying municipal equity to anchor the company. The model requires high risk tolerance and operational sophistication, with variants now playing out in Hangzhou, Suzhou, Changzhou, and Yibin.

Where industry funds provide capital, development funds work on the infra. In order to attract companies, local governments will build factories and infrastructure – from roads, lighting, electricity, to the factory shell and floors. Governments make 5-6% IRR on these rental facilities, and if the company goes out of business, they re-rent the space. Companies can shop municipal proposals, like comparing term sheets, and can often negotiate low-cost rent, down to 1 RMB per month. This means it can go from blueprint to output in ~18 months.

Case study: Perovskite solar in Wuxi and Quzhou

UtmoLight, one of China’s leading perovskite players, began GW-scale module production at a Wuxi facility in early 2025 with local government support for land, utilities, and factory shell. It’s also standing up a second 1GW line in Quzhou. Microquanta, its competitor, set a certified 21.86% module efficiency record in February 2025 and energized an 8.6MW grid-connected perovskite farm in late 2024, the world’s largest at the time, with similar local-government co-financing.

SOEs vary. Some do research, like the Chinese Academy of Sciences, similar to the US national labs. The majority focus on developing strategic sectors: agriculture, fertilizers, construction, bridges, the grid.

Nationally, there are 97 SOEs, with the majority focusing on strategic or financial sectors. National security sectors, for instance, are majority owned by SOEs. Local SOEs are different — even at the provincial level, they could be majority-owned by local government but operate much more like private companies.

They offer several benefits:

The scale of China’s SOEs is massive. China’s 97 central SOEs sit on roughly $13T (90T RMB) in assets as of 2024. And they’re both investors and operators in China’s electrostate transformation. State Power Investment Corporation (SPIC), China Three Gorges, CNNC, Sinopec, and State Grid are among the largest utility-scale deployers of wind, solar, hydrogen, and storage globally, and they set the reference price for project finance across the rest of the stack. When CATL ran its Hong Kong secondary listing in May 2025 at $5.2bnafter greenshoe, the largest HKEX IPO in four years, Sinopec came in as the cornerstone investor. In other words, China’s national oil SOE became the biggest backer of the country’s largest battery manufacturer.

A small but growing part of the stack is Chinese universities. While China’s strength has historically come from its 10-100 scale-up muscle, Beijing is now betting big on R&D at universities to create its own domestic 0-10 innovation funnel.

Startups, governments, and universities are incredibly intertwined in China. Chan-xue-yan (产学研) means “industry, university, research institution integration”, a government-embedded collaboration model where companies, universities and the state laboratories are wired together from founding stage.

Similar to leading US universities like MIT and Stanford, China’s Tsinghua has a spin-out model leveraging tech transfer, entrepreneurship support, university-linked seed funding, and external VC. But Tsinghua can more institutionally “engineer” these spin-outs to scale-up. After a startup emerges from the university, it can stay in the university’s broader ecosystem, work with university-affiliated commercialization platforms (TusPark and Tsinghua Holdings), or “Tsinghua-themed” funds backed by a mix of alumni capital, foundations, or state-linked entities. For climate specifically, Tsinghua Holdings runs Tsing Capital, a cleantech VC arm that manages the China Environment Fund series, arguably the first dedicated cleantech fund in any country (2002).

And…finally we get to China’s private capital layer.

The Chinese VC landscape has gone through a structural shift, dominated by international dollar funds, now to state-backed capital. A lethal cocktail of China’s big tech crackdown (starting with Ant Financial’s IPO in 2020), the pandemic, and rising US-China tensions drove most international investors out of the Chinese market. The "golden era" where US dollar funds were the primary engines for early-stage Chinese tech startups effectively ended.

In June 2023, Sequoia Capital split its China operation into an independent firm, HongShan (红杉资本), which now raises capital independently. GGV Capital also split, carving $9.2bn of AUM into Notable Capital ($4.2bn US) and Granite Asia ($5bn, Asia). Tiger Global cut China from mid-teens to mid-single digits as a share of its portfolio, and Qiming Venture Partnerscut its most recent flagship fund from a $1bn target to roughly $600m.

So private investors may be down, but not quite out. The void has been filled by domestic GPs, and corporate investors:

Despite the retreat of US dollar funds, the Chinese startup ecosystem is showing signs of promise.

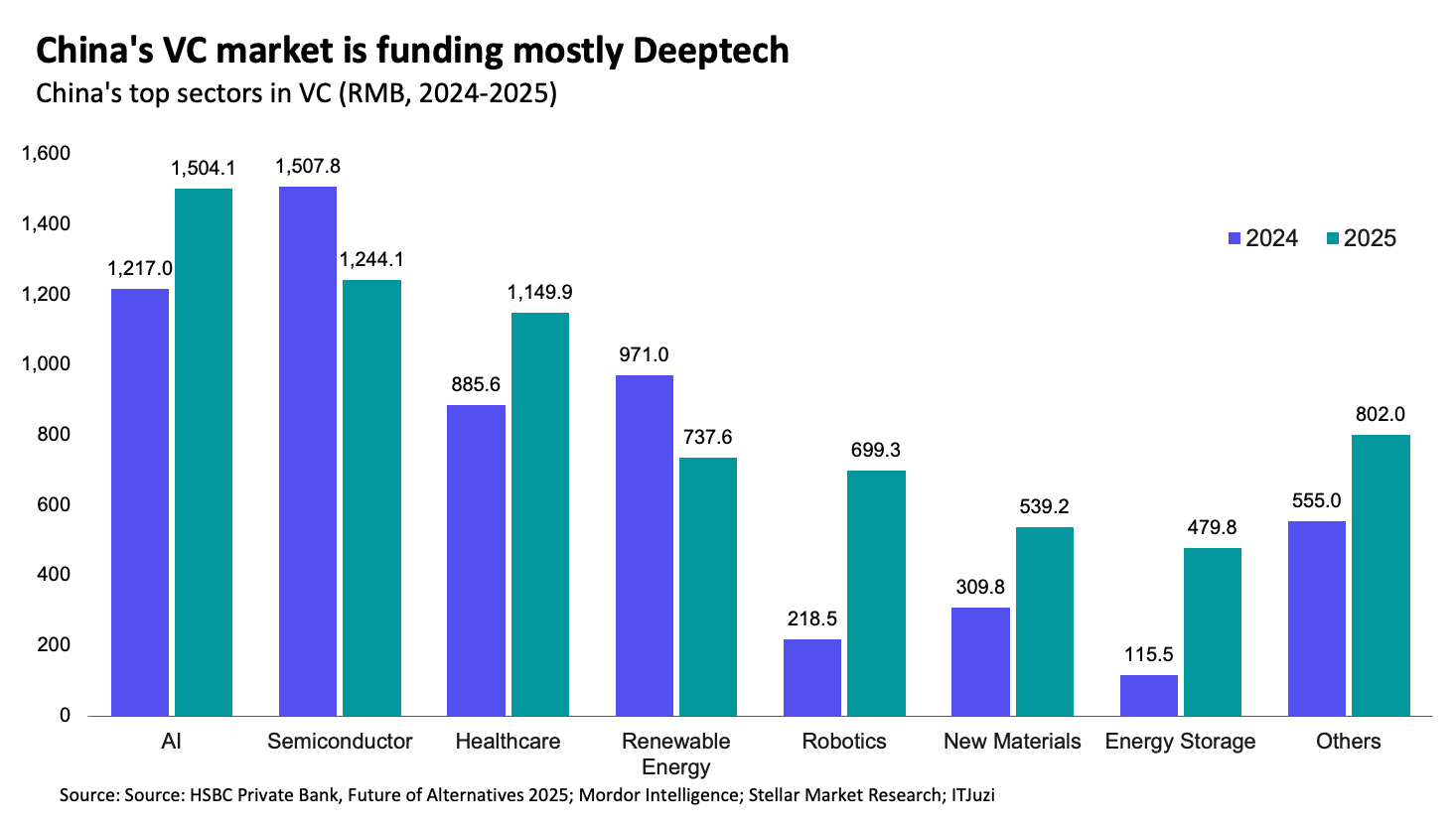

Deeptech becomes the new consensus. With the decline of consumer internet investments (which previously defined the Chinese VC boom), capital has aggressively rotated into "hard tech" or deep tech sectors. This aligns closely with Beijing's push for self-reliance and tech leadership in its 15th Five Year Plan. The most heavily invested sectors AI, semiconductors, healthcare, energy, and robotics. Robotics shot up the most in 2025, up 220% YoY.

China’s top deals in 2025:

Exits (overseas) seeing a comeback. Much like the West, China’s exit market has also been in the doldrums, especially since the traditional route of listing on US exchanges became fraught with regulatory hurdles from both US and Chinese authorities. Regulatory tightening on listening standards and pricing on Chinese exchanges (Shanghai's STAR Market, Shenzhen's ChiNext, the Beijing Stock Exchange) also slowed the pace of domestic IPOs.

2025 was the year that exits came back. VC/PE exits on the A-share market jumped 138% YoY to 109bn RMB, and 294 Chinese companies went public, up 30%. But the majority, 61% to be exact, of those IPOs happened offshore with Hong Kong and other foreign exchanges offering Chinese companies that have been hit with overcompetition overseas market access. Hong Kong Exchange (HKEX) in particular booked 106 IPOs and ~HK$280B (~$36B) in proceeds, up 218% YoY with CATL’s May 2025 secondary listing as the most notable IPO.

Speed and scale have a tradeoff: overcompetition. The same capital alignment that produced CATL, BYD, and the world's cheapest clean-energy supply chain also produced 100+ EV brands and a solar sector competing at zero margins. Involution and excellence come from the same mechanism.

The bar is higher in the East than it looks. Startups can raise VC, but traction requirements are steeper, and the government tailwind isn't evenly distributed. Budgets are tightening and strategic focus is shifting away from saturated cleantech toward AI and robotics. State support is a feature of the system, not a guarantee for any individual company.

For Western investors and builders, the structural cost gap isn't closing anytime soon. But the more useful question is where China isn't dominant yet - solid-state chemistry, perovskites, long-duration storage, grid software - and whether the West can mobilize fast enough to matter in those windows before China gets there too.

A special thanks to the experts for their help in demystifying China’s capital stack. Raymond Song is a climate policy and finance analyst with 10+ years of experience on China and the geopolitics of climate. Pengxin Dong is a VC investor and operator with an independent advisory firm supporting climate tech startups and VC funds with fundraising, international market expansion across Asia and Europe, and other operational and strategic needs.

Subscribe to CTVC, run by Sightline Climate, here:

Our new report ft. low-carbon data center megadeals, reopened public markets, and rise of adaptation

Newsletter

Newsletter