Sightline Climate has just published an update to our most comprehensive analysis of climate fundraising. We've tracked every fund close, vintage, and LP commitment across the market since 2021, and can show you where the capital stands today. We’ve got some highlights below, but there’s a lot more you can find if you download the report.

Want the deeper cut? The full report on the Sightline platform includes most investors by fund type, the most active LPs, granular fund-level data, geographical trends, close-rate analyses, and even more. Clients can get the full version on the platform here.

Not a client yet? Talk to our team to learn how to get access.

But don't worry - we'll be breaking it down live in a webinar on May 1 at 11AM ET. Join us to learn about the data and the trends behind it from the Sightline team, and ask anything in a Q&A. Register here.

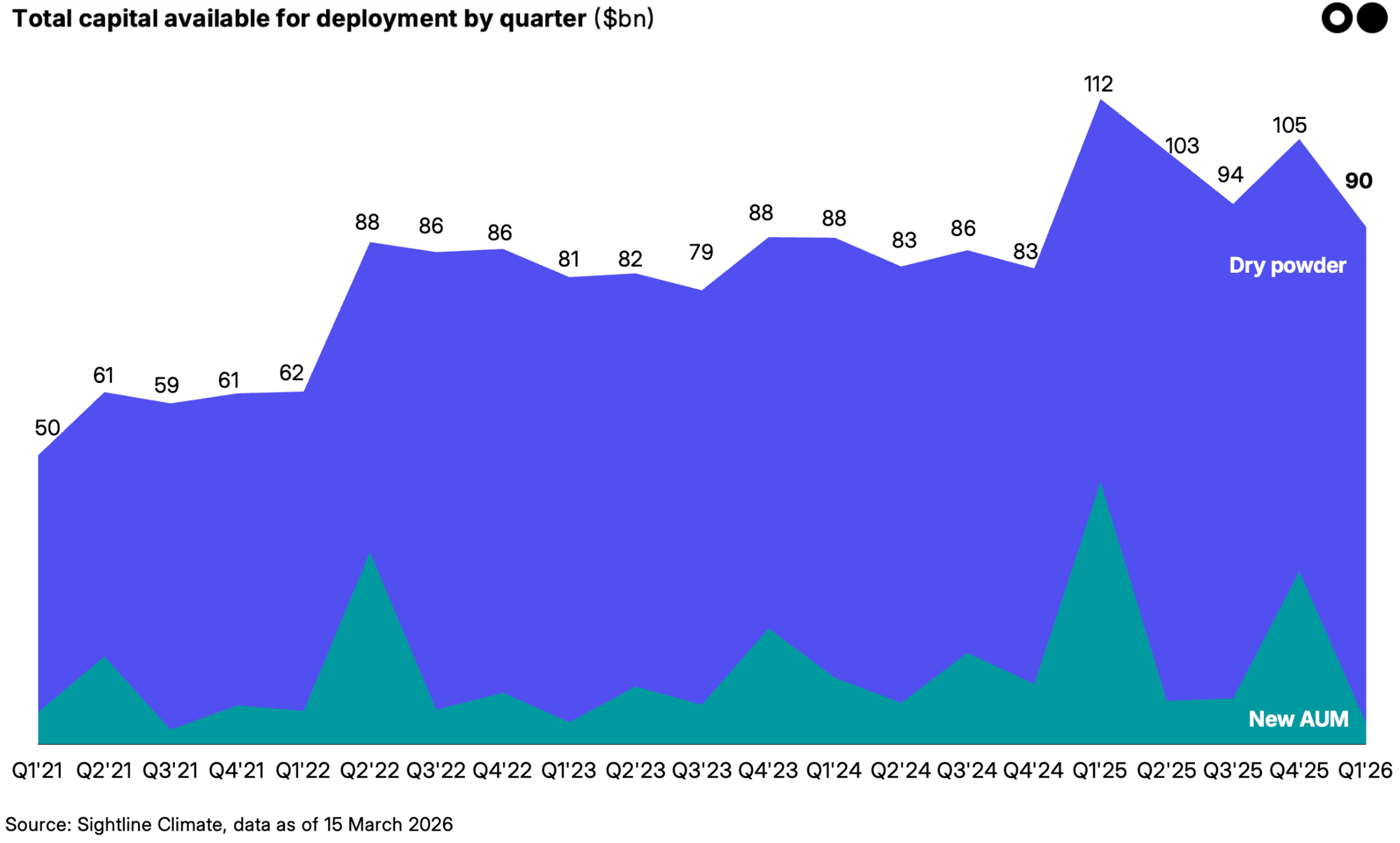

$90bn in climate dry powder as of Q1 2026. 2025 was a record year for climate fund closes, with $92bn in new capital raised across 179 funds. The $90bn in dry powder is down from a peak of $112bn in Q1 2025, as deployment has outpaced fundraising.

Infrastructure wins. The focus has shifted from early-stage riskier bets to established players with track records in mature tech. VCs focused on tackling hard-to-abate sectors, or investors operating in volatile climate policy markets like the US, are struggling to raise. LPs waiting on exits are hesitant to top up here. But infra is playing a different game: yields from mature tech deployment are slow but steady.

75% of all capital in just 58 mega-funds. $193bn is concentrated in just 58 mega-funds from the top ten most active investors. Brookfield alone accounts for $51bn in climate closes, with ECP, CIP, and EQT each north of $24bn. The biggest checks are going to the biggest platforms.

VC dry powder is drying out with climate venture funds unable to raise net new capital to refill their coffers. The average VC fund is shrinking, total venture share has compressed from 20% in 2021 to under 8%, and close rates for VC have cratered to 39%, the lowest of any fund type.

Fund close rate drops to 57% in 2025. This has left $205bn in targeted capital sitting in the pipeline. The US has been the worst hit at just 35%, while Europe has been less volatile at 71%. Europe overtakes US with $61bn in 2025 The US closed just $37bn. It’s a striking reversal from 2022, when the US led. Development finance institution (DFI) anchoring and policy stability have made Europe the most reliable region for climate capital formation, while US fundraising falters under uncertainty surrounding the One Big Beautiful Bill Act (OBBBA).

Our methodology: We track climate funds in VC/Growth, Private Equity, Infrastructure, and Other (e.g. Government, Fund-of-funds). For generalist funds with a focus on renewable energy or climate, we apply weighting factors to estimate the portion allocated to climate. For the full methodology behind the dry powder and funds analysis, see the report.

Investable dry powder for climate stands at $90bn

Investable dry powder for climate stands at $90bn, as of Q1 2026. This figure represents the total capital committed to climate-focused funds that has not yet been deployed into companies or projects, encompassing venture capital, growth equity, private equity, and infrastructure vehicles.

Dry powder growth has slowed dramatically since 2022. The linear increase of the past few years is a far cry from the steep ascent of 2021 when the stockpile nearly doubled from $50bn to $88bn in a single year. The net zero commitments that drove the boom are no longer the main driving force of climate investment. New funds instead have oriented around energy and infrastructure, instead of just climate.

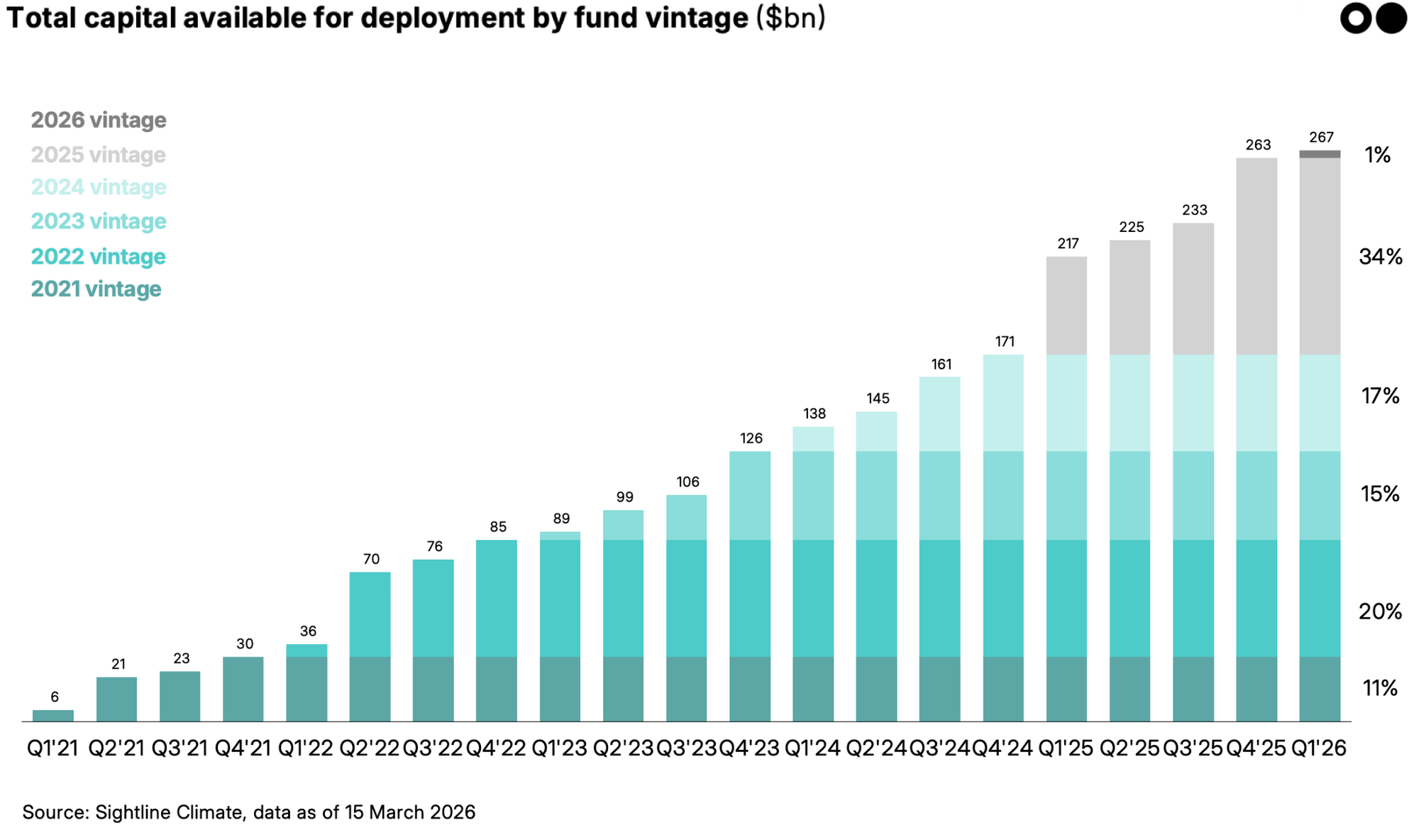

2025 was a record year for climate fund closes

2025 broke records after two years of slower fundraising and growing uncertainty about climate tech. Mega-funds drove the rebound: 179 funds closed $92bn led by energy infra giants like EQT, Brookfield, and Copenhagen Infra. That was double 2024’s raise, and 85% more than the $50bn raised in 2022. The count of funds was also up from 163 in 2024 and 123 in 2023. Financing the booming energy and AI infra wave requires bigger check sizes and larger funds.

The 2025 vintage now accounts for 34% of total dry powder, the largest single vintage. By contrast, the 2023 vintage represents 15%, and the pre-2021 vintages have largely been deployed. 2025 investment was 10% higher than in 2024, proving there are enough targets for those funds to deploy into new technologies.

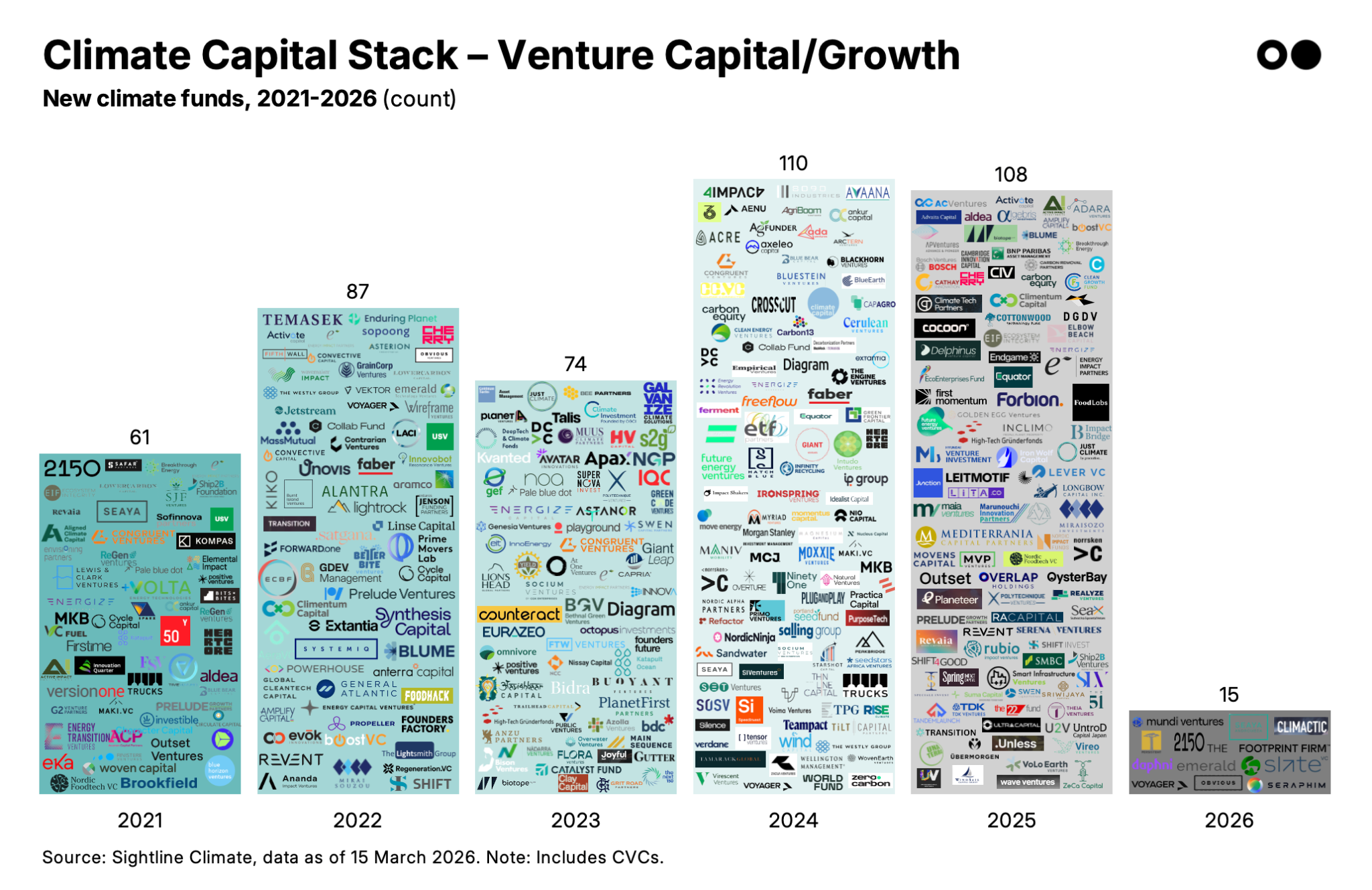

Climate Capital Stack — Venture Capital/Growth

VC and growth funds are still the largest segment of the capital stack by count. The number grew from 61 in 2021 to a peak of 110 in 2024, before dipping slightly to 108 in 2025. With only 15 new VC/growth funds in the 2026 YTD data, the segment is continuing its downward trajectory. But high fund counts are masking dropping fund sizes. VC and growth funds collectively raised $6.5bn in 2025, roughly the same as in 2022, but this capital is now spread across nearly 25% more funds. The average climate VC fund is getting smaller, from $174m in 2024 to $160m in 2025, and the total share of capital flowing through venture channels has shrunk from roughly 20% in 2021 to under 8% in 2025.

The free-for-all of the 2021–22 boom is over. When it looked like both corporates and governments were ready to put serious money behind climate, first-time fund managers found it relatively easy to raise capital. LPs are now demanding much higher standards, prioritizing return numbers, deal track record, and sector expertise. The drop in VC close rates to 39%, the lowest of any fund type, reflects this tougher environment. Many of the VC funds launched in 2023–24 are still fundraising, and a growing number may never reach their targets. The risk is a generation of “zombie VCs”: funds that raised enough for a first close but lack the capital to follow on, leaving portfolio companies stranded in the Series A-to-B gap.

There's a lot more in the full report.

We break down exactly where within infrastructure the capital is going (mature vs. growth vs. emerging), profile the PE players quietly raising follow-on funds, and name the top 10 investors accounting for the bulk of climate AUM.

Newsletter

Newsletter