🌎 CTVC’s guide to New York Climate Week ‘26 #307

We're bringing back the NYCW climate tech event tracker!

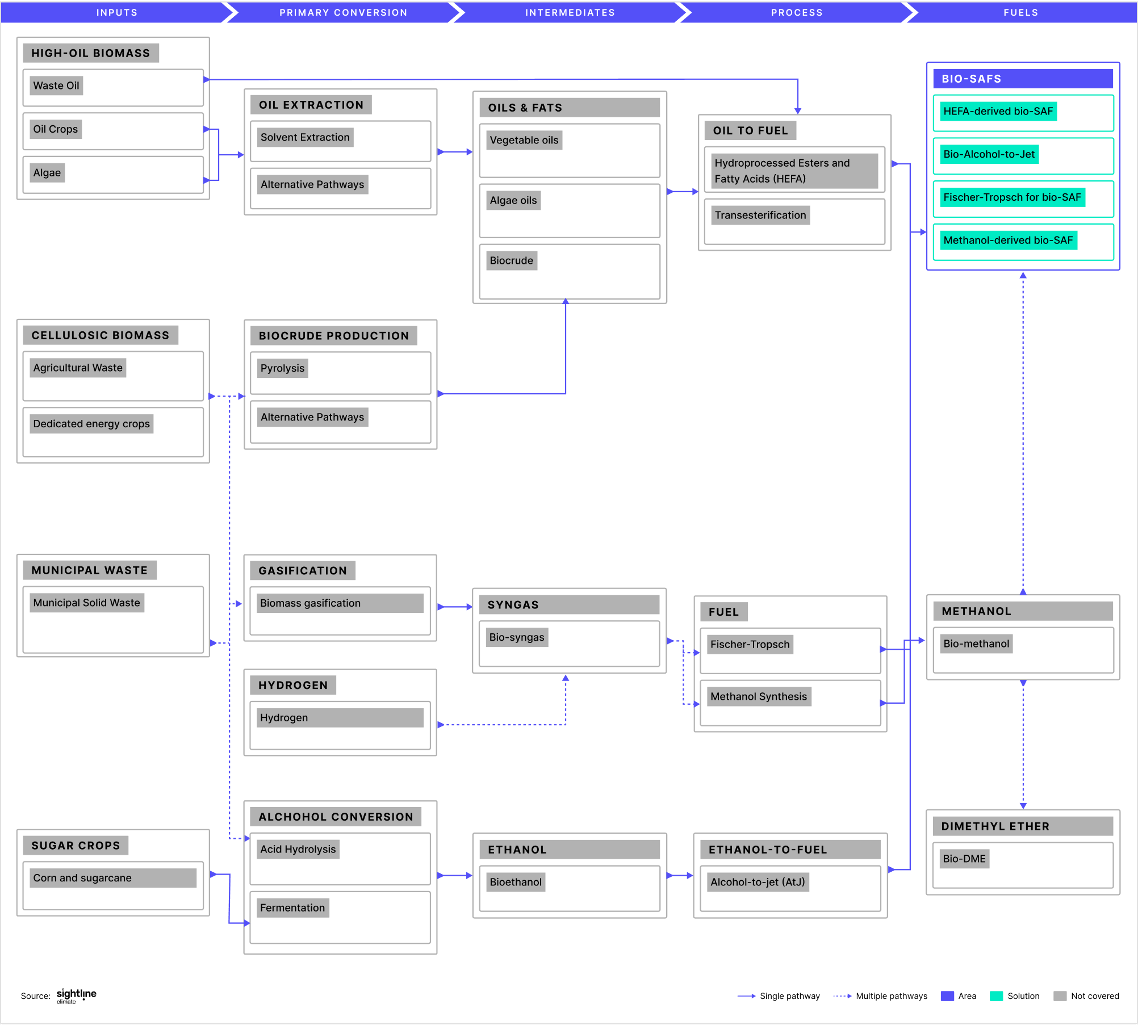

The U.S. gives new guidance on qualifying for SAF tax credits.

Happy Monday!

Hope you bet on the right horse for the Kentucky Derby this weekend. Meanwhile, the Biden administration is placing its bets in the race to scale sustainable aviation. The U.S. released specific guidance for the SAF tax credit under the IRA, allowing corn ethanol-to-jet fuel to qualify and opening up the runway for corn farmers and bio-SAF producers.

In other news, Biden cracks down on Chinese parts and materials in EV supply chains with new EV tax credit rules; carbon removal startup Vaulted signs a lucrative offtake agreement with Frontier; and Brookfield and Microsoft sign a massive PPA to develop over 10.5 GW of new renewable energy capacity.

In deals, $650m for renewable energy development, $60m for parametric insurance, and $45m for green hydrogen via alkaline electrolyzers.

And don’t forget: On May 7th, we'll be hosting a webinar, "Line of Sight: To FOAK and beyond," with special guest David Yeh. Register today.

Thanks for reading!

Not a subscriber yet?

📩 Submit deals and announcements for the newsletter at [email protected].

💼 Find or share roles on our job board here.

Last week, the U.S. unveiled its long-awaited guidance on sustainable aviation fuels, aka SAFs. The 2022 Inflation Reduction Act introduced a tax credit ranging from $1.25 and $1.75 per gallon (up to 25% of the fuel’s value) for SAFs capable of achieving a “lifecycle GHG emissions reduction of at least 50% as compared to fossil fuel-based jet fuel.” But it didn’t specify how to measure eligibility…until now.

As we previously covered, not all SAFs are created equal and neither are their emissions profiles. Bio-SAFs, derived from biomass, can have significantly different lifecycle emissions depending on their feedstocks and conversion methods. E-fuels, derived from CO2, hydrogen, and renewables, can save as much as 80-90% of emissions but are far more expensive today.

The big question has been whether corn ethanol-to-jet fuel qualifies for the SAF credit. Given the influence of the U.S. corn ethanol industry and potential decline in demand for ethanol due to rising EVs, corn farmers, ethanol producers, and SAF makers alike have been eagerly waiting for clarification. The answer they got was, “Yes, but…”

We read the new IRA guidance, aka “Notice 2024-37,” so you don’t have to. Here are all the ifs, ands, and buts:

Flying commercial

This new guidance further solidifies the role that biomass-based biofuels will play in the U.S., but helps tip the balance from the most common biomass used — hydroprocessed esters and fatty acids (HEFA) like used cooking oils or vegetable oils — to an alternative, Alcohol-to-Jet (AtJ), which uses sugar sources like sugar cane or corn.

Winners:

Losers:

What’s next?

Commercialization on the horizon. Alcohol-to-Jet (AtJ) pathways are still maturing, with FOAK facilities such as LanzaJet's Freedom Pines just coming online. Looking forward, we’d expect to see more U.S. AtJ facilities being built and oil refineries expanding their HEFA capabilities in order to hit the Biden administration’s target of meeting all domestic jet fuel demand with SAFs by 2050.

Offtake not taking off (yet). Meanwhile, the vast majority of contracted offtake for SAF has yet to be delivered, so many airlines are still waiting to use the fuel. But building up the supply chain and pipeline of FOAK (and NOAK) projects will take time.

Carrots for sustainable ag. The rules use SAF credits as the carrot to incentivize more sustainable agricultural practices, but land-use concerns persist regarding grow-to-fuel, as SAFs compete between fuel production and other agricultural uses. Fortunately, scientists are also developing alternative ways to obtain sugars for ethanol production, such as using different crops or even waste products.

International departures. The EU’s RefuelEU program prioritizes e-fuels or power-to-liquid production, which could mean that e-fuel producers may look to the EU to build FOAK facilities. Expensive e-fuels may now have more competition in the U.S., but new room to grow in the European market.

⚡ Pine Gate Renewables, an Asheville, NC-based renewable energy developer, owner, and operator, raised $650m in PE Expansion funding from Generate Capital, HESTA, and Healthcare of Ontario Pension Plan.

☂️ Arbol Insurance, a Queens, NY-based parametric insurance platform, raised $60m in Series B funding from Giant Ventures, Opera Tech Ventures, and Mubadala Capital.

⚡ Charge Zone, a Vadodara, India-based fleet electrification and retail EV charging platform, raised $19m in Growth funding from British International Investment and BlueOrchard Finance.

🚢 X Shore, a Stockholm, Sweden-based all-electric boat manufacturer, raised $9m in funding from undisclosed investors.

☂️ AIDash, a San Jose, CA-based infrastructure monitoring platform, raised an additional $8.5m in Series C funding from additional investors Lightsmith Group and Marubeni Corporation.

⚡ Stargate Hydrogen, a Tallinn, Estonia-based green hydrogen via alkaline electrolyzers developer, raised $45m in Seed funding from UG Investments.

🔋 LiNova, a Monrovia, CA-based high-energy polymer battery technology maker, raised $16m in Series A funding from Catalus Capital and Chevron Technology Ventures.

🌱 Carbonfact, a Paris, France-based life-cycle assessments for fashion platform, raised $15m in Series A funding from Alven, Headline, and Y Combinator.

👕 Xefco, a Sydney, Australia-based water-efficient textile dyeing platform, raised $7m in Seed funding from Main Sequence.

🌾 Smartbreeder, a Piracicaba, Brazil-based AI-based crop yield platform, raised $3m in funding from EcoEnterprises Fund.

🚚 Movener, a Santiago, Chile-based hybrid vehicle retrofitting company, raised $2m in Seed funding from SQM Lithium Ventures.

🥩 Maia Farms, a Vancouver, Canada-based mycelium-based protein, raised $2m in Seed funding from Joyful Ventures, PIC Investing Group, and Koan Capital.

🌾 CroBio, a Macclesfield, UK-based soil regeneration platform, raised $2m in Seed funding from The Grantham Foundation, SOSV, Ponderosa Ventures, and Catapult Ventures Group.

♻️ Kubik, a Nairobi, Kenya-based low-carbon buildings from plastic waste company, raised $1.9m in Seed funding from African Renaissance Partners, Endgame Capital, and King Philanthropies.

🔋 Pure Lithium, a Boston, MA-based lithium battery technology platform, raised an undisclosed amount in additional Series A funding from Ivanhoe Capital and WS Investment Company.

Infinity Recycling, a Rotterdam, Netherlands-based investment firm, held a final close of a $188m fund that invests in advanced plastic recycling.

Bluefront, an Oslo, Norway-based investment firm, announced the launch of a $50m fund targeting sustainable seafood companies.

Can’t get enough deals? See full listings and deal analytics on Sightline Climate

President Biden took a bold stance against Chinese influence in the electric vehicle (EV) sector by implementing stringent final EV tax credit rules. The final rules include a stipulation banning manufacturers from claiming tax credits on parts manufactured in China after a two-year grace period.

Carbon removal startup Vaulted secured its most lucrative offtake agreement to date with Frontier, a corporate buyers organization for carbon credits, highlighting the growing market for carbon removal technologies. This is the largest deal that Frontier has signed since April of 2022.

In another major deal, Brookfield and Microsoft signed an offtake agreement to develop over 10.5 gigawatts of new renewable energy capacity worldwide, setting a new standard for corporate-driven renewable energy initiatives. This is the largest corporate level PPA ever signed, and is almost eight times larger than any previous PPAs.

In more EV news, Tesla company laid off the majority of its supercharger team, creating significant concern from industry experts about the network's growth outlook. These layoffs come at the same time that the majority of automakers switched to Tesla’s NACS charging port.

The Vogtle Unit 4 Nuclear Reactor reached commercial operations this past week. Despite cost overruns and project delays, the project coming online represents a pivotal moment in the U.S. nuclear energy landscape, although experts question if this may be the last of its kind project. In the same week, The U.S. Senate passed a bill banning Russian uranium imports by 2028, as the U.S. focuses on its domestic supply and looks to add stockpiles in the near-term.

Russian energy giant Gazprom revealed a loss of $6.9bn, its worst loss in more than 20 years, due to a loss in exports. The losses are a sign that Europe is decreasing its gas demand and successfully weaning itself off of Russian natural gas, although the bloc is turning to LNG imports from the U.S. instead.

Oman’s green hydrogen producer Hydrom launched an ambitious $11bn initiative in North Africa to develop two projects. One project will power a single ammonia plant using 4.5 GW of solar and wind energy to deploy an electrolyzer with a capacity of 2.5 GW — surpassing today’s global green hydrogen capacity of 1.5 MW. It points to a Middle Eastern and North African strategy of offsetting natural gas industry declines with higher hydrogen production.

Bill Gates paves the way for a greener future, one pothole at a time.

An (actually helpful) overview of AI use cases in energy, courtesy of the DOE.

PwC reveals climate risks in nine key commodities.

Bridgewater’s take on scaling climate tech (spot the Sightline cite).

Beluga whales are talking about you through a blob of fat in their forehead.

A two-brood Cicadafest is coming to the US midwest and southeast.

New student resources for the energy transition just launched.

📅 Line of Sight: To FOAK and beyond: Register to join a live discussion with Sightline Climate and climate tech experts on May 7th on scaling climate tech solutions to FOAK (First-of-a-Kind) projects and beyond.

📅 Insurance Innovation Prize Launch: Register to join the NYCEDC Innovation Prize launch event on May 9th for an opportunity to engage with leading climate tech experts and discuss the latest innovations in insurance for the energy transition.

📅 World Hydrogen Summit: Register to join global leaders in hydrogen technology from May 13-15th to discuss the critical role of hydrogen in the global energy transition and explore partnership opportunities.

📅 Battery Conference: Register to join this leading industry event from May 13-16th to explore the latest developments in automotive battery technology and connect with experts to advance your knowledge in the evolving battery sector.

📅 Green Marine Fuels Conference: Register to attend the Green Marine Fuels conference from May 14-16th to discuss the future of sustainable marine fuels, network with industry leaders, and gain insights into innovative solutions for greener maritime operations.

📅 Stanford Sustainability Innovation Conference: Apply to attend the Stanford Graduate School of Business Scaling Sustainability Innovation Conference on May 17th to engage with ecopreneurs, scholars, and business leaders.

Research Lead; Data Operations Associate, Research Intern; Data Intern @Sightline Climate

Lead Biodiversity Scientist @EarthAcre

Project Delivery Lead @Station A

Content & Social Media Manager, Visual Storyteller @Aigen

Senior Financial Analyst, Energy and Sustainability @Google

2024 Summer Intern @Azolla Ventures

Investment Associate, Sustainable Investing @Ontario Teachers' Pension Plan

Head of Operations @Andes

Associate or Analyst @Allied Climate Partners

Chief of Staff @Fervo Energy

📩 Feel free to send us deals, announcements, or anything else at [email protected]. Have a great week ahead!

We're bringing back the NYCW climate tech event tracker!

Newsletter

Newsletter