Pilot, check. Project team, check. You’ve been diligently making your way down the FOAK checklist. You’re ready to build. Up next: raising the eight to nine figures, yikes!

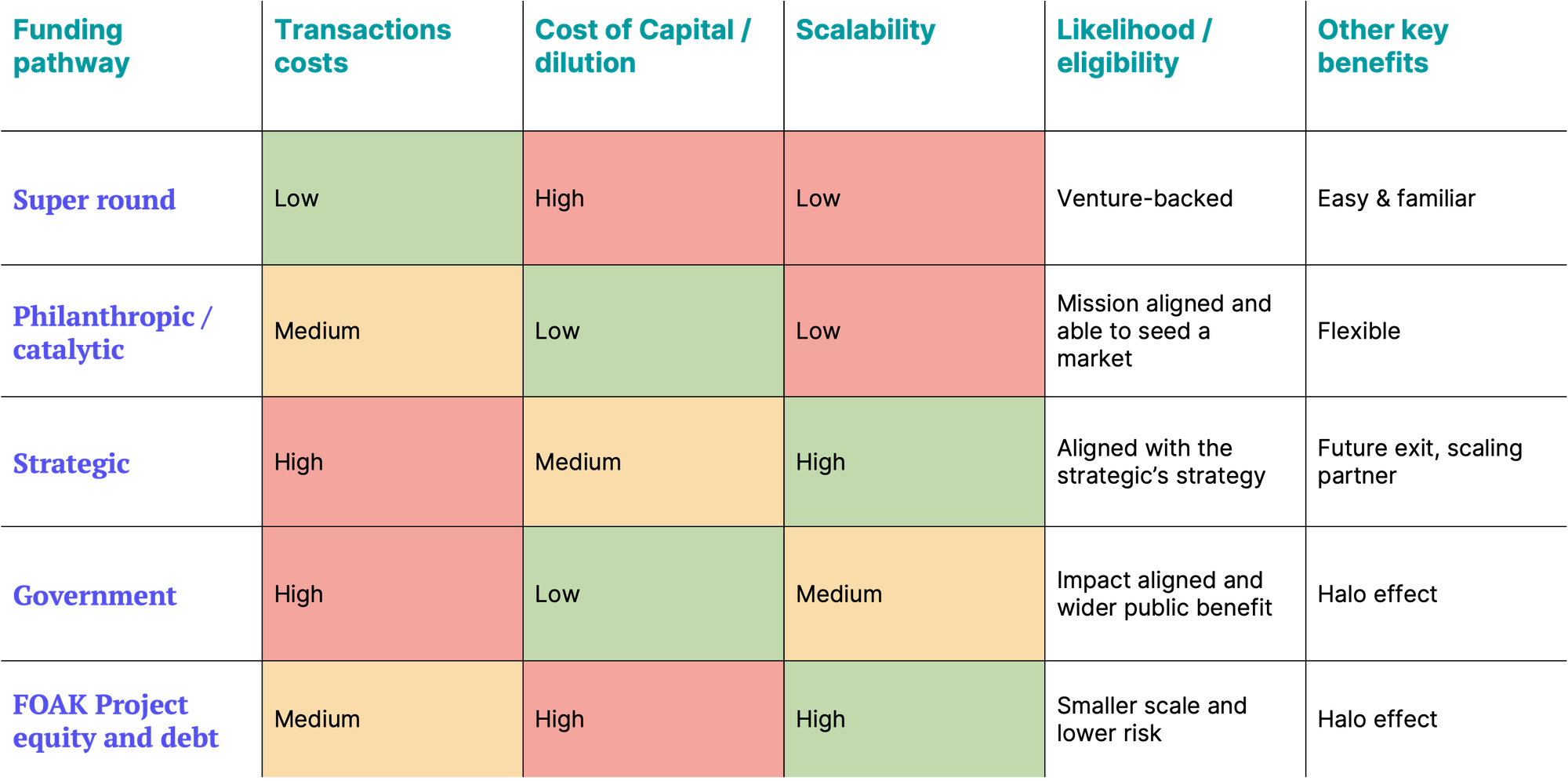

FOAK finance is finicky, to say the least. While not quite a plug-and-play formula yet, five primary financing buckets repeatedly back up FOAK with bucks: “Super Round” with Equity, Philanthropic or Catalytic Capital, Strategics, Government, and Project Investment. (For an intro to the different kinds of funding check out our Climate Capital Stack.)

In this piece we’ll look at what each investor group is looking for (The Eligible), the benefits of raising money from them (The Good), the drawbacks (The Bad), and companies that have done this before (The Exemplars).

The Eligible

What are FOAK investors looking for? Generally, it’s some combination of:

Technology readiness level (TRL). The state of your tech will determine what you can do. Start with the technology – how de-risked is the tech, how long has the pilot been running? The level of risk you’re at will dictate which investors will be open to you.

Alignment. VC and project finance (PF) may not mind what your product does so long as it makes money, but Philanthropic/Catalytic, Strategics, and Government will be led by non-financial criteria. For Strategics this might be supporting the growth of existing or even new billion dollar businesses, while for Government it might be about supporting technologies with national strategic importance, but for all three, $ alone isn't sufficient.

Capex requirements. How much do you need? If it’s nine figures, it’ll be hard, expensive, and extraordinarily dilutive to finance from the balance sheet, and it’ll be too much for most philanthropic/catalytic funders. But on the other hand it won’t be worth going to the DOE for a $20m LPO loan.

Internal Rate of Return (IRR). If your first few project equity returns are in the mid teens then you might be able to raise project capital, but anything less than that and it’s going to be tough.

The Good and the Bad

Some of the areas that may or may not go your way are:

Scalability. Ultimately you’ll want this to be the first-of-a-kind, but not the last. That means you’ll need to get onto a pathway that can support scaling up and developing lots of commercial projects. Long term for many that will mean moving to a licensing model, being acquired by an incumbent, or tapping mainstream project finance (PF) sources. Acceptance into the mature infrastructure market takes time - think project 10. But when it happens, it enables the rapid and massive scale that wind, solar, and batteries, who were FOAKs 15 years ago, experienced. Infra leaders like Brookfield or Sumitomo think in billions, not millions, will likely want to finance as many de-risked projects as you can develop, and the cost of their capital is a fraction of VC.

Cost of capital. How much is it going to cost you? Cost of capital for a FOAK is not cheap, both for debt or equity, and boards need to understand that. The appeal of PF isn’t necessarily that it’s cheaper, but rather that it’s off balance sheet which means non-dilutive and most importantly, it's the only path to gigaton scale.

Transaction costs. Your biggest cost is not often money but time. Levels and types of due diligence for FOAK will be much higher than conventional deals. So budget a year for engaging the DOE or an energy major and expect the process to be orders of magnitude more rigorous than VC diligence.

Other factors. While less significant than the points above, each financing option comes with its own quirks, for better or worse. A few key ones include:

Size of ticket. What’s their funding appetite? How much of the total they can take? Some funds are limited in their maximum ticket size, while those issuing debt may have loan to value (LTV) constraints. The LTV can have both a minimum and maximum threshold.

Credibility. Getting a well known and trusted infrastructure brand as an investor can help you raise capital from other sources, and boost your brand. In particular the DOE and global institutional investors have the halo effect. Sorry VCs.

Partnerships. Strategics can offer much more than just money. Acting as investor, offtaker, advisor, and more allows them to offer a range of benefits, albeit at the cost of a loss of control.

Term. Different asset classes measure time differently. Strategics can be patient with time horizons that can go beyond a decade, whereas institutional investors want to get their money out within a life of a 10-12 year fund. For project investment, debt terms are usually <10 years while project equity sponsors typically own assets for the life of the asset (e.g. 20 years).

The Paths Taken

1. “Super Round” (with Equity)

Who & how

Venture Capital, Growth, and Strategics – a similar group to those who may have invested in your last round – with the addition of Sovereign Wealth Funds and Pension Funds to super size the round.

Nine figure equity investment into your startup / growth company

The eligible

Actually kind of a big deal. Do you look in the mirror and see a climate unicorn? Are investors and strategics banging on your door with eight/nine figure term sheets? Most start-ups, even the ones with momentum, won’t qualify.

The good

Fast. Raises take months, not years, and once the money’s in you can get going straight away. This will likely be the fastest path.

Simple and familiar. No need to mess around with becoming a PF expert. Just raise more venture and PE money on top of the heaps you raised in the past.

The bad

Dilution. This is the most expensive and dilutive form of capital.

Low scalability. This may be how you pay for your first, but it’s unlikely you’ll be paying for your third this way. At some point you’ll need to get on the PF bus.

Pressure. You are now a unicorn and have to defend that lofty valuation going forward. Any hiccup (and if you are doing FOAK, there will be hiccups) could lead to the dreaded down round.

Examples

Climeworks (DAC), raised a whopping $650m round back in 2022 to break ground on Mammoth, their first large-scale site. Off the broad back of Mammoth, Climeworks has since begun scale-up for its megaton-scale projects, leveraging DOE’s funding in the US.

Boston Metal (green steel), raised $262m Series C last year to finance their FOAK from a who’s who of funds, strategics, and family offices.

2. Philanthropic or Catalytic Capital

Who & how

Catalytic investors (e.g. Breakthrough Energy Catalyst, Trellis Climate), NGOs (e.g. Elemental Excelerator), High net-worth individuals, Family Offices, and some Strategics (e.g. Microsoft) can also behave this way.

Debt, grant, equity or something in between/whatever you need.

The eligible

Alignment: Impact. Do you impact areas they care about? Are you catalyzing gigatons of CO2 reduction or decarbonizing the hardest industrial sectors? Don’t forget about environmental justice and issues of access and equality. Will your success support communities that have been left behind?

Catalytic. Climate-first funders have lofty goals of seeding new markets and spurring revolutionary climate solutions. Many share the goal of being the FOAK bridge that takes you from VC to PF or other kinds of scalable finance.

The good

Cheap(er) and Flexible. Catalytic funders boast of flexible capital - debt, equity, and even grants. Whatever is needed in the capital stack to get the project financed.

Credibility. Some catalytic funders, e.g. Breakthrough Catalyst, are well respected by financial investors and strategics. Their involvement has a halo effect - opening doors, adding negotiation leverage, and, most importantly, improving the chances of gaining other funding.

The bad

Not-scalable. They’re only here to FOAK, not NOAK (Nth of a kind). Your second and third projects are likely to need other funders.

Small check size. With a few exceptions, the checks are smaller. Fine if your project is millions to tens of millions, but if it's more then you’ll need to blend with other sources too.

Restrictive. Investment may come with specific impact metrics based on the funder’s priorities.

Examples

Infinium (SAF), raised $75m from Breakthrough Energy Catalyst last year. SAF’s is one of Breakthrough’s five stated priority areas. Breakthrough went on to support Infinium for their Project Roadrunner by partnering with American Airlines and Citi to fund the largest eSAF site in North America. As well as an offtake agreement with American Airlines, they arranged to transfer the associated emissions reductions to Citi to reduce their scope 3 emissions, enabling them to secure additional future revenue. In doing so they not only helped Infinum scale, but created a blueprint that other SAF producers could follow.

3. Strategics

Who and how

Strategics (e.g. corporates like ArcelorMittal, Occidental, bp, BHP, Microsoft) are typically global leaders in a category who are looking not only for financial returns but also to bring additional value through industry expertise, specialized knowledge, access to distribution channels, technology, or markets.

Equity or debt (either in the project or the company), or some combination of the two as well as in-kind services. They may likely ask for a ROFR (Right of First Refusal).

The eligible

Alignment: Business strategy. How does your startup meaningful impact a giant? Are you a disruptive tech that they need to monitor? Are you a potential new billion dollar business for them? Can your addition meaningfully grow existing operations? Sometimes it’s clear like British Airways + Shell + LanzaJet or more complex like a European energy major buying a biofuels business to grow its trading business.

The good

Silver bullet. Strategic investors can be your FOAK silver bullet. If a giant incumbent like an Oxy believes your success is his/her success (NET Power, Carbon Engineering), strategics can be not only your investor and lender but your project development partner and offtake customer.

Long term. Incumbents can take a long term view and make billion dollar commitments. Strategics like Total took LNG from FOAK to NOAK in ~10 years.

Credibility. Big strategics are well known and often trusted, having one as a partner can help unlock offtake and investment from risk-averse blue chippers.

The bad

Slow. Energy majors and other strategics may take a long time to commit. You may have to meet with their business units, their engineering teams, and then meet them again.

ROFRs (Right of First Refusal). Since most FOAK and early projects don’t have high IRRs, they may ask for ROFRs on your pipeline as the technology becomes proven and hopefully profitable. This means that the strategic would have first dibs on future projects.

Optimal for who? The gravitational pull of a strategic’s size will naturally optimize the FOAK for their business. The incumbent’s competitors (who likely may be your future customers) may start to see you as part of their competitor’s defacto subsidiary and avoid doing business with you.

Examples

Carbon Engineering (DAC), was bought by Occidental for $1.1bn last year. Occidental have stated their plan to build 100 DAC plants and see the potential to license 1,000. This commitment may have helped drive BlackRock’s decision to invest $550m in Stratos, Carbon Engineering’s FOAK. Alternatively…

NET Power (clean natural gas power), raised money from a purpose-built syndicate of strategics. This included leaders for each part of its supply chain – Baker Hughes (energy services giant), Shaw / McDermott / Lummus (EPC and process tech), Exelon (utility), and Occidental (EOR). These investors provided more than just capital and were critical for NET Power’s FOAK in 2022. NET power ultimately went public through a SPAC last year at a valuation of around $1.5bn.

4. Government

Who & how

From Gov or its entities (e.g. DOE Loans Program Office (LPO), European Investment Bank (EIB), British Business Bank, Canada Infrastructure Bank). There are hundreds of billions from hundreds of government programs to support FOAK.

Alignment: program qualification. Government dollars are earmarked for specific policy goals with defined eligibility and a set application window. For example, for the DOE’s $3.5B DAC hub funding, there is a tight definition of qualifying tech, qualifications around EOR, stipulations on cost shares, and a set application timeline. Don’t forget about community benefits that are integrated through IRA’s and BIL’s requirements.

The good

Cheap. Often the cheapest debt (e.g. 6%) for FOAK. Grants of course are even better.

Big checks. The LPO can write billion dollar checks for FOAKs. No one else will.

Credibility. Getting funding from the DOE is tough but worth it. It’s a stamp of approval that can unlock other funding pathways.

The bad

High transaction costs. Applying to the $400bn LPO is likely a year plus and will cost millions. So aim high ($250m+), or otherwise it’s not worth the fees and time. Other funding programs like the $25bn OCED and ARPA-E’s SCALEUP have lower transaction costs but write smaller checks.

Conditions. Loans and loan guarantees can come with constraints (e.g. domestic content requirements, NEPA permits, and community benefits).

Partial. Won’t be able to cover all of the ticket, think LTVs in the range of 50:50 or 60:40 depending on likelihood of repayment. This is also true of other funding sources, but not always known about government loans.

Examples

Monolith (clean hydrogen, carbon black) in 2021 received a $1bn LPO loan guarantee to expand their plant into a FOAK commercial site. The DOE stated that the project was both in line with the purpose of the fund, and would create high paying jobs, along with a strong community benefits plan.

Energy Dome (LDES), raised $25m out of a $65m funding round from the European Investment Bank for its first-of-a-kind utility-scale long duration energy storage facility in Sardinia, Italy.

5. Project Investment (equity & debt)

Who & how

While typical project investors would include large banks, sovereign wealth funds, pension funds, and other infrastructure investors, realistically they’re not going to engage at the FOAK stage. Instead it will be smaller specialist “emerging infra” firms like Spring Lane, Wollemi, Grok, Wavelength or larger funds like Antin who can do THOAK (third-of-a-kind).

Can be either debt and/or equity at the project level often coupled with investment at the TopCo.

The eligible

Lower risk. These investors in sustainable small(er) scale projects are looking for technologies to be as de-risked as possible, think EV charging for buses where similar tech and business models have already been proven with passenger EVs.

Racing for the Bronze. In the world of emerging infrastructure, most investors would rather win the Bronze medal. A THOAK should have two operating plants that can demonstrate the tech and commercial model has been derisked.

Worth the (lower) risk. The risk reward calculus will need to be compelling, one way of doing this might be having an IRR commensurate to the risk (e.g. above 15%).

The good

Highly scalable. If all goes well, your NOAK projects can graduate to mainstream investors and lenders who can write big checks and keep writing them. It’ll take a while to get there, it won't be the second, nor probably the third.

Show me the money. Infra investors’ job is to generate returns for their LPs. While they might also care about climate impact, it’s secondary.

The bad

Expensive. You can get cheaper capital but it won’t be for ambitious stuff.

Small checks. While their mainstream siblings can write the biggest checks, at the FOAK stage typically they’ll only occur in small deals, think $10ms not $100ms, although their portfolio of deals might cross the $100ms threshold.

Not easy. Even if you do meet the eligibility criteria it can still be a lengthy process to raise PF, especially if it’s a novel technology. Your funding universe is smaller and due diligence will be more rigorous. If you’re wondering how to talk project finance, check out our duolingo.

Examples

Aries Clean Energy - Spring Lane wrote a $25 million equity check to Aries for the next iteration of their operating tech to gasify biosolids and create a self powered virtual landfill. One facility soon to be up and running!

SOLARCYCLE raised asset-level equity finance from Fifth Wall for their FOAK in Texas and NOAKs for solar panel recycling. Their goal is to recycle millions of panels per year.

Blend – Everything everywhere all at once

Ultimately, how you finance your FOAK will be a blend. But each layer can help unlock the next; the credibility from a philanthropic/catalytic funder or government funding can help de-risk a project enough to unlock project finance.

As you move from FOAK to the second and third, that financing mix will change, that philanthropic/catalytic funding and Government backing will likely drop away potentially to be replaced with project finance. If that leaves you with more questions, don’t worry, moving from FOAK to NOAK will be the topic for the fourth (and final) piece in this series.

This is Part III in our FOAK playbook series. We'll be switching it up over the next few weeks, then return to your regular FOAK programming for the Part IV (and final) installation on moving from FOAK to NOAK.

Newsletter

Newsletter