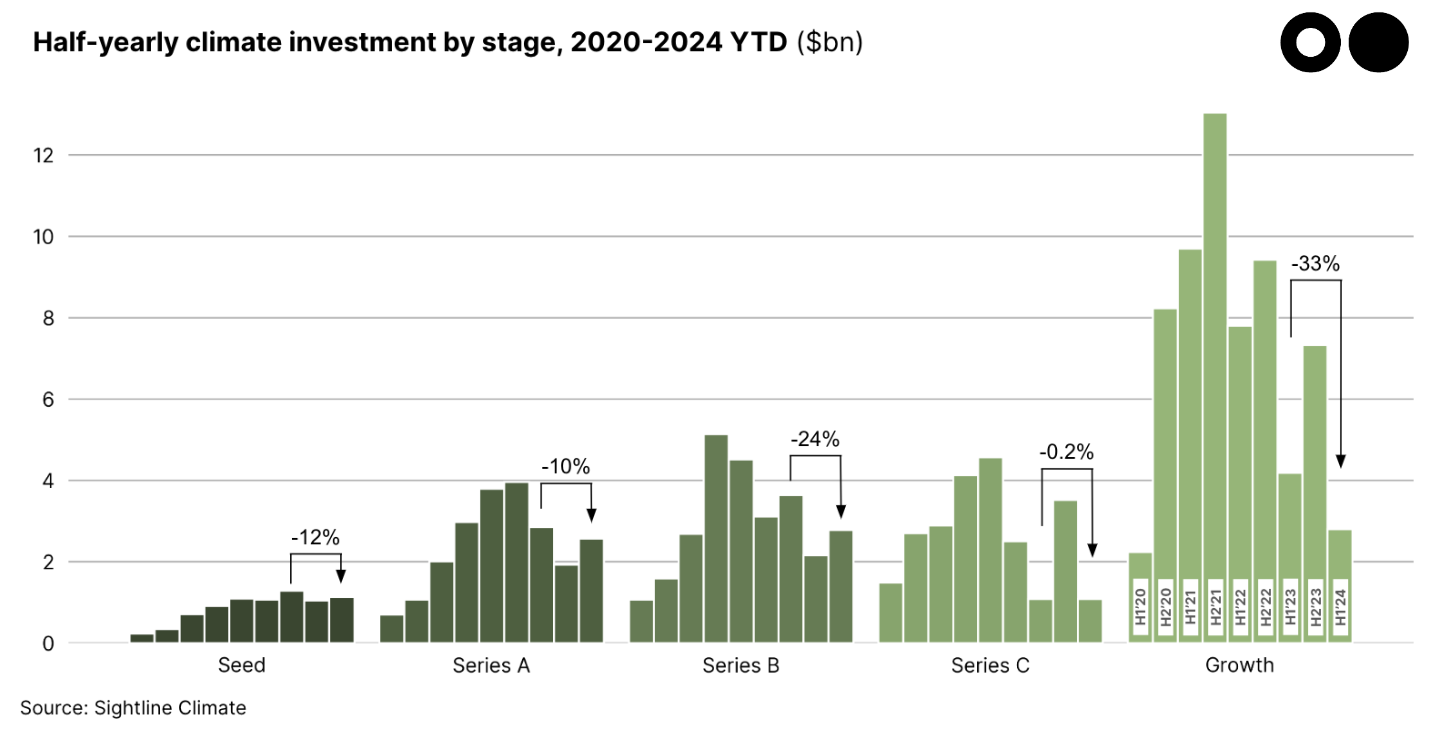

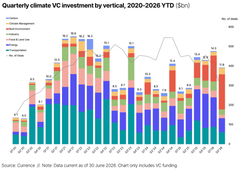

H1'24 funding totaled $11.3 billion, down 20% from H1 2023.

Happy Monday!

Hope you got to enjoy some fireworks and barbecues over this Fourth of July weekend. At CTVC, we were cooking up our report on H1’24 climate tech funding, and we’ve got some takeaways for you below.

In deals, $541m in four newly announced funds, $183m for 3D metal printing, and $149m for electric aircraft across two deals.

In other news, new AI use leads to surge in Google’s emissions; leading nonprofit SBTi CEO resigns; and Shell pauses construction on one of the biggest biofuels projects planned.

Thanks for reading!

Not a subscriber yet?

📩 Submit deals and announcements for the newsletter at [email protected].

💼 Find or share roles on our job board here.

Last Friday, we released our midyear report on climate tech investment trends. Here’s a recap of the play-by-play for 2024 so far.

The climate tech market has been on defense for the first half of the year. Investors, who spent most of 2023 on the bench “waiting-and-see,” have continued to play it safe. The result? A drop in both deal count and funding, with the usually resilient early-stage investments finally feeling the pinch.

Highlight reel

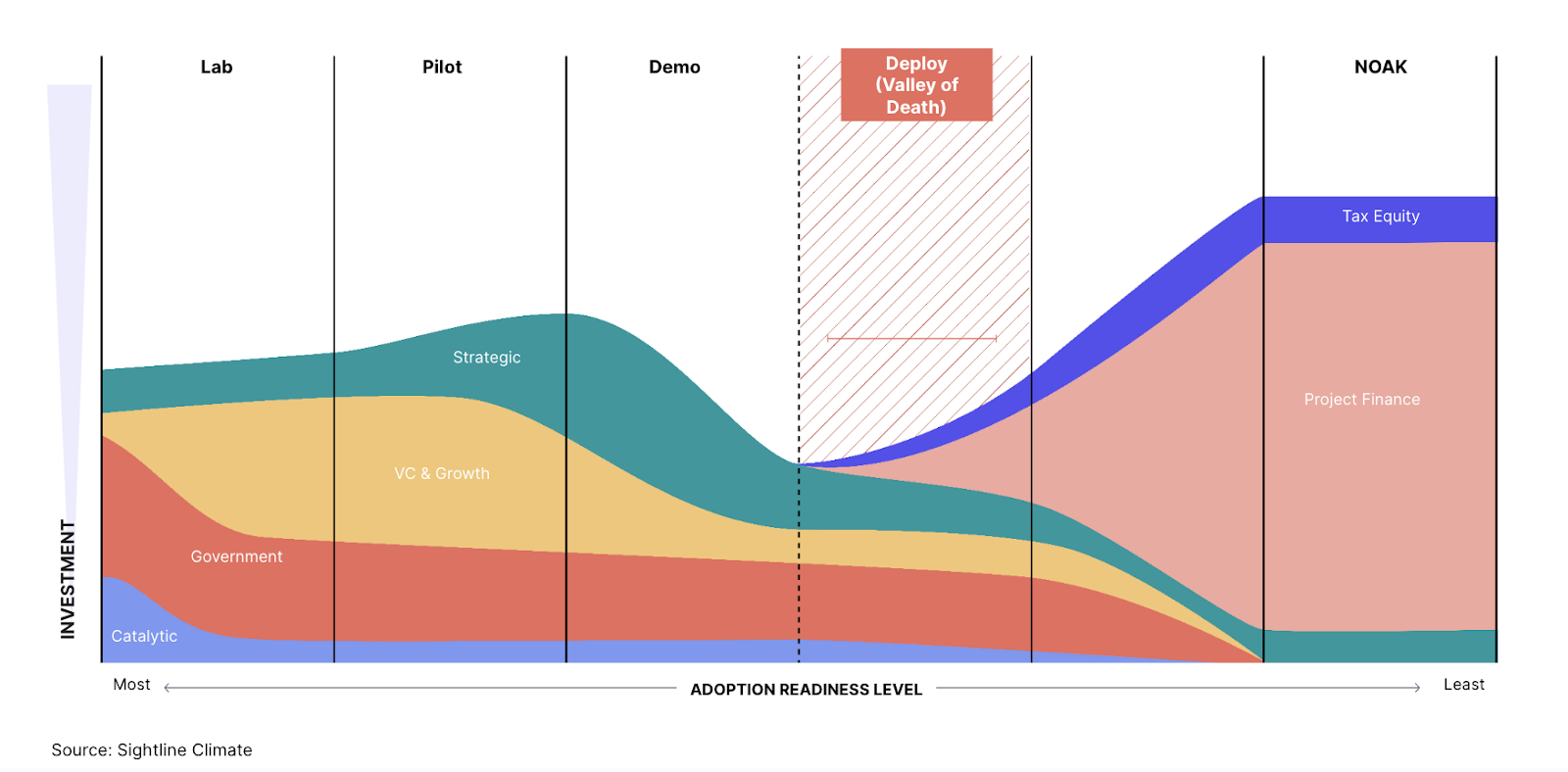

Zooming in on the climate tech Valleys of Death

As Tim Latimer discussed at the Breakthrough Energy Summit at London Climate Action Week last month, the founding of Breakthrough Energy around 2015 marked one of the biggest financing signals for the start of climate tech.

Now, there’s a sizable cohort of climate tech startups approaching their FOAK deployment scale — which requires hundreds of millions, if not billions, for their next round. But high interest rates, sticky inflation, and uncertainty around global geopolitics have made growth investors more cautious.(Bloomberg highlighted this trend in an article about our report.)

As the funding frenzy of 2021-2022 fades in the rearview mirror, we’re seeing dropoffs in investment. (The caveat is, this is all VC funding — some later stage companies are starting to pivot from equity to project finance and debt to get their projects off the ground.)

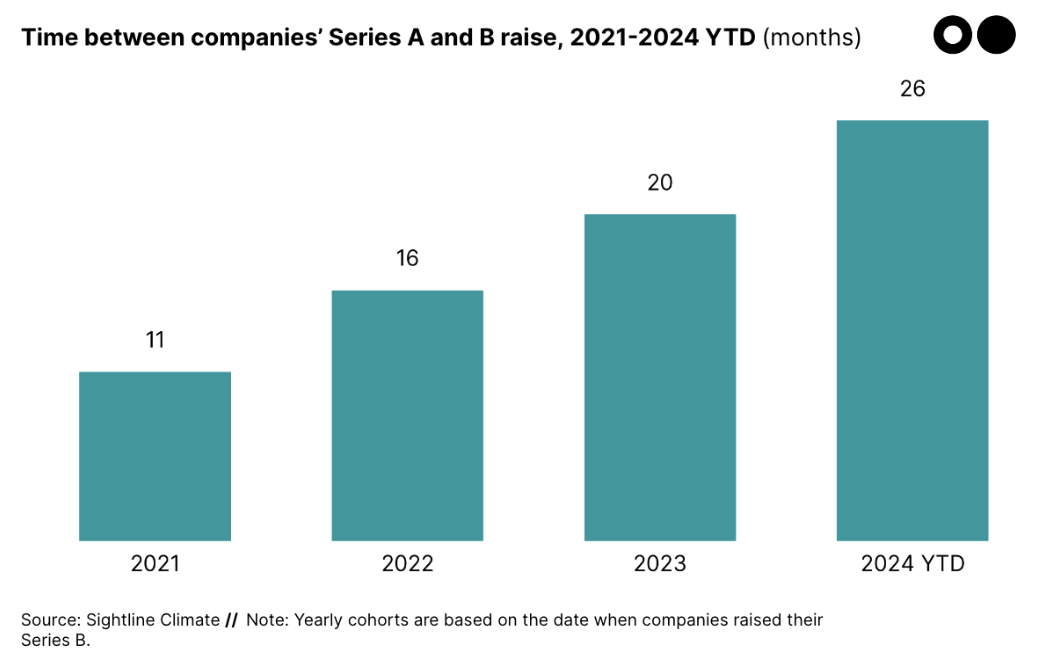

Meanwhile, raising a Series B isn’t as easy as it used to be. Raising a Series B takes ~2.5x longer than it did in 2021, leaving these companies stuck as they face increasing expectations about their ARR (often >$10m) and proof of commercialization from later-stage investors.

Key takeaways

Don’t blow the final whistle yet. The first half of 2024 has been a mix of defensive and offensive plays for the climate tech market. Investors are cautious, funding is shifting, and the focus is on quality and due diligence.

Despite the tough economic climate and jitters ahead of the US election, deals — including some big plays — are still happening. Round sizes at the early stages (Seed to Series B) are looking healthier compared to the 2021-2022 funding frenzy, reflecting the investor flight to quality. So those that do cross the Series B Valley of Death are rewarded.

We’re also seeing signs that many companies and projects aren’t solely relying on VC funding anymore, as they’re starting to graduate from equity to project finance and debt for the ultimate game plan: deploy, deploy, deploy. For instance, H2 Green Steel paired a $372m Equity raise with a $4.5bn Debt raise, and Sunfire’s Series E equity raise was followed by a $108m loan from EIB.

Check out more charts, trends, and analysis in our report here. And for Sightline clients, you can access the full report and underlying data here.

🛵 Matter Motors, an Ahmedabad, India-based electric bikes manufacturer, raised $35m in Series B funding from Capital 2B, Helena, Japan Airlines & Translink Innovation Fund, and Saad Bahwan Investment Management Company (SB Invest).

📦 Vytal, a Köln, Germany-based reusable packaging-as-a-service platform, raised $7m in Growth funding from Grazia Equity, Kiko Ventures, Rubio Impact Ventures, and Ventis.

📦 Cartken, an Oakland, CA-based AI-powered autonomous robots maker, raised $23m in Series A funding from 468 Capital, Incubate Fund,Magna International, Mitsubishi Electric and Shell.

🏭 Phaidra, a Seattle, WA-based industrial AI control system for energy efficiency platform, raised $12m in Series A funding from Index Ventures, Ahren Innovation Capital, Character, Flying Fish Partners, Helena, and other investors.

🌾 eAgronom, a Tartu, Estonia-based online farm management system, raised $11m in Series A funding from Swedbank, Icos Capital, Soulmates Ventures, and SmartCap Green Fund.

🧱 alcemy, a Berlin, Germany-based predictive analytics platform for cement and concrete, raised $10m in Series A funding from Norrsken VC, AENU, and Galvanize Climate Solutions.

☔ Natcap, a London, England-based nature risk management solutions platform, raised $10m in Series A funding from Neon Capital Partners, Yeo Ventures, and angel investors.

🌾 Travertine Technologies, a Boulder, CO-based electrochemical platform for sustainable fertilizer, raised $9m in Series A bridge funding from Holcim MAQER Ventures, the Grantham Foundation, Clean Energy Ventures, and Bidra Innovation Ventures.

📦 Uncaged Innovations, a Troy, NY-based sustainable leather alternatives producer, raised $6m in Seed funding from Green Circle Foodtech Ventures, Fall Line Capital, Golden Seeds, InMotion Ventures, Ponderosa Ventures, and VegInvest.

📦 Zedify, a Cambridge, England-based low-carbon delivery services, raised $5m in Series A funding from Barclays (Sustainable Impact Capital), Green Angel Syndicate, Mercia Ventures, and Midlands Engine Investment Fund.

🏭 Altrove, a Paris, France-based AI platform for sustainable materials, raised $4m in Pre-Seed funding from Contrarian Ventures, Emblem, and angel investors.

♻️ Sensorita, an Oslo, Norway-based waste management analytics company, raised $3m in Seed funding from Brick & Mortar Ventures and Telenor.

⚡Orus Energy, a Paris, France-based electrical flexibility platform, raised $3m in Pre-Seed funding from Asterion Ventures, Myriam Maestroni, Pierre Trémolières, Ring Capital, and b2venture.

🧱 Cambridge Electrical Cement, a Cambridge, England-based low-carbon cement producer, raised $2.3m in Seed funding from Zero Carbon Capital, Almanac Insights, Cambridge Enterprise Ventures, Delph25, and other investors.

🥩 MATR Foods, a Copenhagen, Denmark-based plant-based food producer, raised an undisclosed amount in Seed funding from Novo Holdings.

✈️ Eve Air Mobility, a São Paulo, Brazil-based electric vertical take-off and landing (eVTOL) aircraft developer, raised $94m in funding from Embraer and Nidec Motor Corporation.

✈️ Archer, a San Francisco, CA-based eVTOL developer, raised $55m in Corporate Strategic funding from Stellantis.

☀️ New Green Power, a Taipei, Taiwan-based solar developer, raised an undisclosed amount in Corporate Strategic funding from Google.

🏭 H2 Green Steel, a Stockholm, Sweden-based decarbonized steel production manufacturer, raised an undisclosed amount in funding from Demeter.

🏭 Desktop Metal, a Burlington, WA-based 3D metal printing developer, was acquired by NanoDimension for $183m.

✈️ Universal Hydrogen, a Hawthorne, CA-based hydrogen fueled aircraft, filed for bankruptcy.

🛵 Cyclobility, a Provincie Oost-Vlaanderen, Belgium-based electric bikes leasing provider, was acquired by Down 2 Earth Capital for an undisclosed amount.

Seaya, a Madrid, a Spain-based investment firm, held a final close of its $326m climate fund that will invest in companies working on reducing waste and cutting greenhouse gas emissions.

The Westly Group, a Menlo Park, CA-based investment firm, held a final close of its $100m fund that will invest in seed companies across energy, mobility, buildings, and industrial sectors.

Carbon Equity, an Amsterdam, Netherlands-based investment firm, held a $65m first close of its third fund that invests in companies working on climate technologies.

Freeflow Ventures, a Kolkota, India-based investment firm, raised $50m to invest in deeptech opportunities to solve human and planetary challenges.

Can’t get enough deals? See full listings and deal analytics on Sightline Climate

Google said last week that its emissions have climbed 48% over the past five years, due in part to surging energy-hungry data centers and AI use. The uptick is in line with other big tech companies — Microsoft’s disclosed emissions increased by around 40% from 2020-23, and Meta’s Scope 3 emissions rose by over 65% from 2020-22.

The CEO of the Science Based Targets initiative (SBTi) has resigned after controversy over changes to the leading verification group’s guidance on carbon offsets. This past spring, the group changed its guidance to allow companies to use carbon credits to offset emissions along their entire supply chain, leading staff to call on him to resign.

Shell has paused construction at one of Europe’s largest biofuels plants in Rotterdam, Netherlands. This is the latest blow to the European biofuels industry, which has been held back by slow demand growth.

The US approved its ninth offshore wind project, the New Jersey-based Atlantic Shores. The 2.8GW project will power nearly 5m homes when complete, and is part of the Biden administration’s plans to deploy 30GW of offshore wind by 2030.

Europe’s largest renewable energy producer StatKraft said it was slowing down development plans for new solar and wind capacity. They join other European utilities such as Orsted and EDP in cutting growth plans, due to a challenging macroeconomic environment marked by lower electricity prices and higher capital costs.

Russia is moving ahead with the world’s first exported SMR plant, after signing the construction contract for a 330MW plant in Uzbekistan, a big step for international advanced nuclear. In other geopolitical energy news, the US is using foreign policy to secure critical minerals access, seeking to facilitate a mining deal in the Congo.

Big names Yara Clean Ammonia, Scatec, ECHEM and MOPCO have signed a deal for renewable ammonia offtake in Egypt. The sponsors intend to build up to 480MW of renewables, to power a 240MW electrolyzer, almost on par with the world’s largest, 260MW Sinopec electrolyze.

In its latest round of funding for decarbonization projects, the DOE has awarded up to $270m for a Texas CCUS plant, with awards worth up to $620m in negotiation for other plants in North Dakota and California. The agency also announced a $100m funding call for LDES projects, and a second round of funding for enhanced geothermal pilot projects.

A Louisiana judge has ruled that the Biden administration cannot delay consideration of liquefied natural gas (LNG) export projects. States had challenged the federal decision to ban LNG export to countries without a free trade agreement was challenged by the states in March.

Fusion powers ahead with new 2024 industry report.

Building the foundation for low-carbon cement.

New report on EU energy shows 74% of the bloc’s electricity in January-June was from emissions-free sources.

An out-of-this-world solution to the data center problem: putting them in space.

Big, if true: a new EV prototype that could charge in five minutes with a full 155-mile range.

The EU gives go-ahead to new $3.3bn CCS project in Sweden.

A prime cut: Bezos Earth Fun launches new Center for Sustainable Protein at Imperial with $30m.

Carbon removal verifier launches new reporting structure.

📅 Solar Visibility Prize: Apply to the Data-Driven Distributed (3D) Solar Visibility Prize by July 10th for your software solution to win a $50,000 prize and mentorship from the DOE.

💡 Stripe Climate Fellows: Apply to be a Stripe Climate Fellow by July 15th and receive grant funding to work on ambitious yet feasible proposals to catalyze voluntary or policy actions, aiming to increase carbon removal demand.

💡 Google Climate Accelerator: Apply to the Google for Startups Climate Change Accelerator by July 21st for a 10-week, equity-free hybrid program for Seed to Series A climate startups providing technical support, and workshops focused on product design and business growth.

💡 DOE Methane FOA: Apply to the Methane Emissions Mitigation and Quantification Program under the IRA by August 26th to access $850m in grants for projects that minimize methane emissions from oil and natural gas production, processing and transportation.

Research Lead; Product Designer @Sightline Climate

Head of Installation Ops; Home Electrification Advisor; Operations Manager @Zero

Director of Media & Content @Elemental Excelerator

Senior Associate - Climate Aligned Industries, CDR @RMI

Sustainability Data Analyst/ Specialist @Ethic

Strategy Associate @Fervo Energy

Chief of Staff @David Energy

Chief of Staff @Optiwatt

Director of Partnerships; Head of Government Relations @Breakthrough Energy

📩 Feel free to send us deals, announcements, or anything else at [email protected]. Have a great week ahead!

Our new report ft. low-carbon data center megadeals, reopened public markets, and rise of adaptation

Newsletter

Newsletter