With the US off for the Fourth of July, this week has felt a bit like halftime for 2024. But watching from courtside seats for the game so far, we’re ready to get into the highlights.

The big theme is the continued constriction of the climate tech market these past six months, but at the same time, some interesting new signals have emerged. At the top of the year, we noted that investors played “wait-and-see” for most of last year, and rather than bounce back, that trend has persisted: H1’24 saw the continued gradual downtick in climate tech deal count and funding. And this time, the decline finally reached early-stage, with Seed and Series A taking a hit alongside later-stage. This trend mirrored the general slump in the broader VC market over the same time, according to Pitchbook, with sticky inflation, high interest rates, and geopolitical turmoil to blame.

But it’s not all doom and gloom. While climate tech investors are keeping a tight grip on the purse strings — due both in part to the tough macroeconomic climate and uncertainty ahead of the US election — deals and even mega-deals are still getting done. At the earlier stages — Seed, Series A, Series B — round sizes are actually healthier compared to post-2021-2022’s market mania.

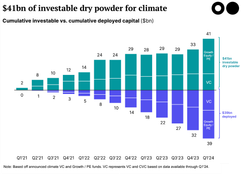

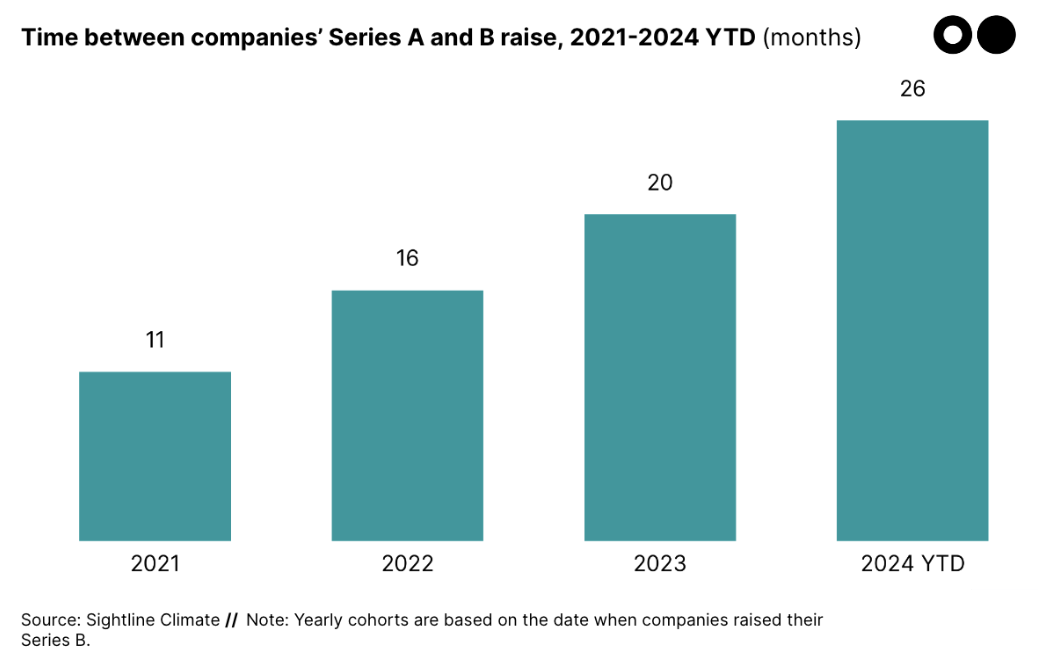

Still, the Valley of Death between Series A and Series B has become more precarious, as a large cohort of climate tech companies approaches the milestone. The average time it takes a company to raise a Series B in 2024 is more than double the time it took three years ago, jumping from 11 months to 26 months between rounds. Meanwhile, late-stage and growth investment and deals have also dropped precipitously. These investors are holding on to record levels of dry powder, but they’re raising their expectations and looking for more concrete proof of commercialization and ARR goals.

So, with the funding frenzy of 2021-2022 firmly in the rearview mirror, these shifts could represent a flight to quality, as investors conduct more due diligence before writing checks. But we’re also seeing signs that many companies and projects aren’t solely relying on VC funding anymore, as they’re starting to graduate from equity to project finance and debt in the race to deploy, deploy, deploy.

We’ve got the charts, trends, and analysis tracking investment, deal activity, FOAK deals, bankruptcies, time between rounds, and investor activity of the past half-year below. (You can read about our full methodology for capturing and categorizing deals at the bottom of this post.)

💰 H1’24 funding: Funding in the first six months of 2024 totaled $11.3bn, down 20% from H1’23 and down 41% from H2’23.

🤝 Deal count: Overall deal activity decreased — H1’24 deal count totaled 553, down 26% from H1’23’s 749 deals.

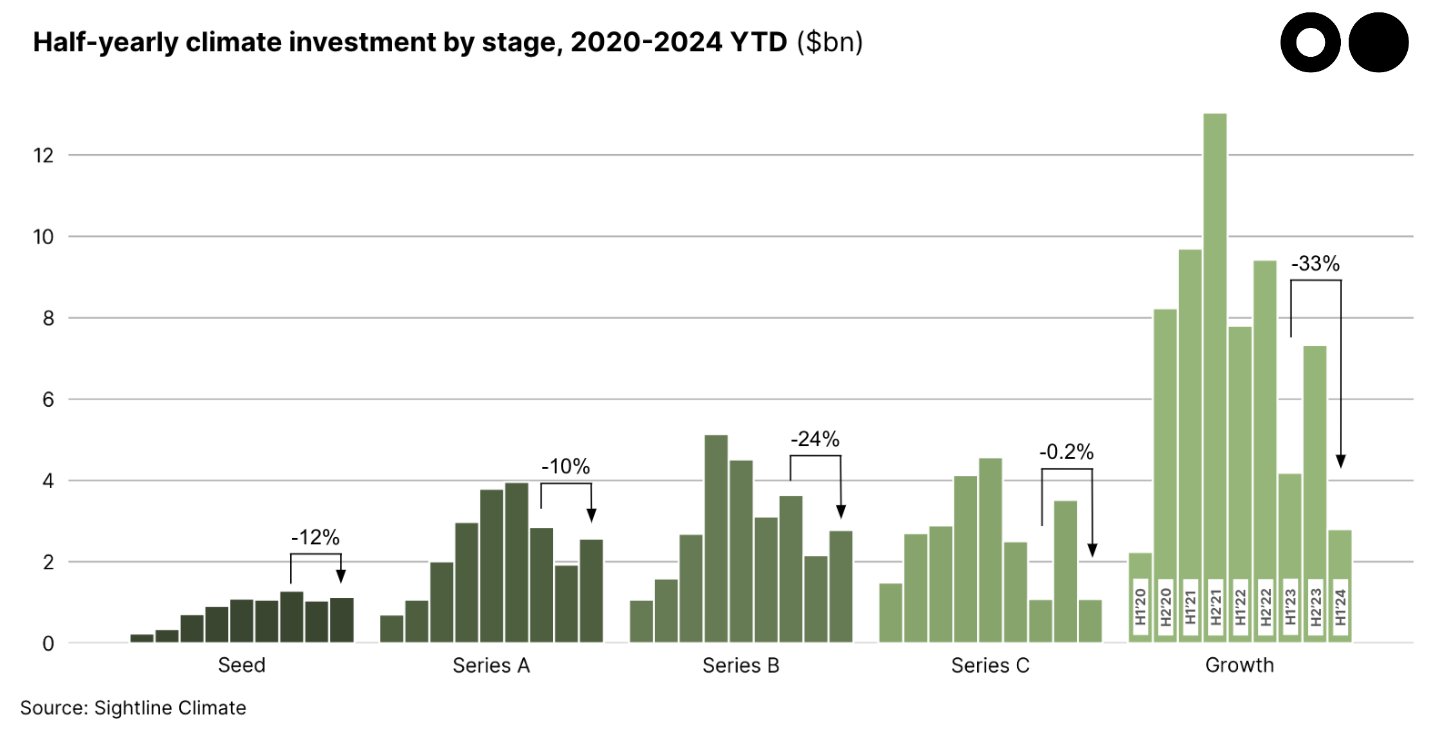

📉 Growth: Growth funding dropped 33%, while the number of growth deals dropped 13%, compared to H1’23.

📈 Early: Seed funding declined 12% in H1’24 vs. H1’23, and Seed deal count decreased 30% for the same period.

💸 Round size: Average deal size between Seed and Series A actually increased by 19%, but decreased by 13% from Series C to Growth, compared to H1’23.

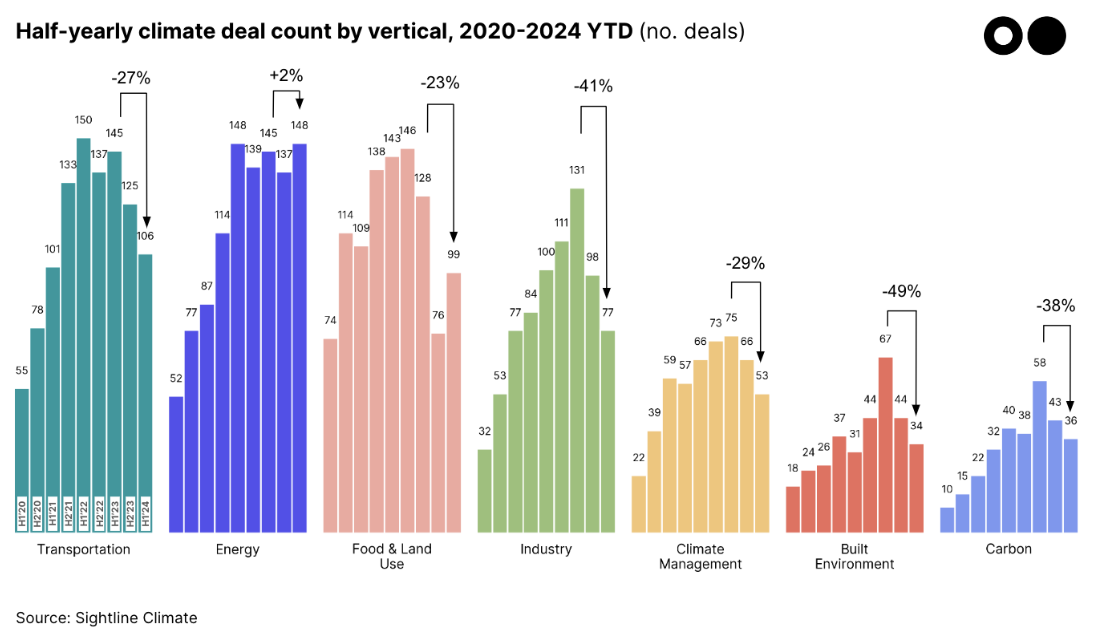

⚡ Vertical: Funding in Built Environment and Carbon Management fell by ~40%, but Energy remained somewhat resilient, with only a single-digit 7% drop.

💥 Notable deals: The companies that were able to get funding this half-year represented many of this year’s emerging trends in climate tech: hype-y AI and the clean firm power it requires, high-flying Sustainable Aviation Fuels, and batteries leading the charge. Advanced geo developer Fervo, thermal energy storage (TES) provider Antora Energy, and textile-to-textile recycler Syre raised massive rounds for hardware buildouts. Plus, steelmaker H2 Green Steel, lithium extractor Lilac Solutions, and Liquid Air Energy Storage (LAES) developer Highview Power all raised “FOAK” rounds to support commercial-scale project development.

H1 2024 Update

The big picture: $11.3bn in H1’24, down 20% from H1’23

H1’24 investment was down compared to H1’23. Investment in the first six months of 2024 totaled $11.3bn, down 20% from H1’23 and 41% from H2’23.

Quarterly investment stabilizes around the $5bn mark. Quarterly totals dropped to $6.5bn and $4.8bn in Q1’24 and Q2’24, respectively.

The notable quarterly exception was Q3’23, which saw mega-deals in the batteries sector driving a bumper quarter.

The drop this Q2 continues the trend of investors taking a “wait-and-see” approach, possibly ahead of the US election.

Overall deal count continues its slide. H1’24 was the second consecutive half-year where deal count decreased, with 26% fewer deals compared to the peak in H1'23.

Climate tech investment begins to plateau

Total funding from H1’20 to H1’24 reached $156bn. H1’24 added an 8% increase to the cumulative climate tech investment total.

But a new investment ceiling may be looming. Quarterly growth continues to slow down, with Q2’24 only growing by 2%, compared to 3% in Q2’23 and 5% in Q2’22. Looks like the cooldown that some bear investors predicted at the end of 2023.

Energy and transportation split the top deals scoreboard

Hot rocks and geologic hydrogen reach the funding surface. Significant mega-deals in Energy include EGS geothermal project developer Fervo Energy raising $244m in new funding led by Devon Energy, and Koloma racking up $246m in its Series B to locate reservoirs of naturally occurring hydrogen.

Rivian raise dwarfs all mega deals. While Rivian has graduated from the private markets (and off this chart), the EV automaker notably raised a $1bn unsecured convertible note from Volkswagen (reminiscent of the Tesla Daimler deal back in 2010). With an additional $4bn coming by 2026, the partnership between legacy automaker and EV challenger aims to pave the way for the next generation of software-defined vehicle (SDV) platforms.

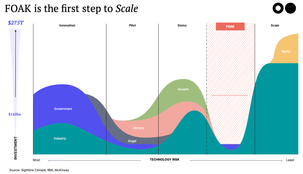

FOAK-level finance drives mega-deals. H1’24 saw a flurry of investment towards companies at the FOAK stage, such as H2 Green Steel, Fervo, and Rondo. Note: We define FOAK deals as funding rounds directly supporting first commercial-scale projects utilizing novel technologies or processes.

The five funders for FOAK in action. As we’ve said before, there’s no tried-and-true recipe for funding FOAK, a “no man’s land” that straddles two adjacent asset classes with contrasting risk and return profiles. Companies are getting creative to fill this gap with equity, philanthropic or catalytic capital, strategics, government lending, and project finance.

Stage

Series B and Growth see sharpest declines in investment

Series B and Growth stages see the most dramatic scalebacks. Overall funding for Series B dropped 24%, while Growth was down 33%, in H1’24, compared to the same time last year.

Companies looking for Series B funding are facing a growing funding gap, and getting stuck. They either must conserve capital or, increasingly commonly, raise a bridge round with unfavorable terms.

Downswing reaches Seed and Series A. Investment at the Seed and Series A stage decreased 12% and 10% respectively in H1’24 compared to H1’23, signaling the end of early-stage resilience to the downturn.

Deal count continues to drop, hitting early stages the hardest

Seed and Series A tumble from their H1’23 peak. Deal activity for Seed and Series A has fallen sharply since the H1’23 peak, by 30% and 23%, respectively.

Series B deals drop reveals steep Valley of Death. The decline in Series B deals — a 28% dropoff — also shows how fewer climate tech startups are crossing the post-Series A “Valley of Death” (more on that below).

The caveat is, H1s are usually quieter than H2s. However, investors might still play wait-and-see in 2024 H2, given the US presidential election, tougher macroeconomic fundraising environment, and investor heads’ turning to AI.

Raising Series B takes ~2.5x longer than it did in 2021

Raising a Series B isn’t as easy as it used to be. The amount of time to go from Series A to Series B has crept over the two-year mark. We’ve heard from investors and founders that a large cohort of climate tech companies are stuck at the pre-Series B stage, unable to raise their next round from later-stage investors, as they face increasing expectations about their ARR (often >$10m) and proof of commercialization.

Seed, Series A, and Series average deal size all rise

Seed deal size went up, despite the decline in total deal count. The average Seed deal size rose 21% from H1’23 to H1’24, indicating healthier rounds. Deeptech startups that often are more capex-intensive successfully raised larger rounds — like Stargate Hydrogen’s $45m Seed round for its ceramic-based electrolysis technology development, and Blue Laser Fusion’s $30m Seed funding for a first prototype for their novel laser fusion technology. CuspAI, as well, raised a notable $30m seed round.

Series B deal size shows a flight to quality. Companies that did get to the Series B stage were rewarded with larger deal sizes — a sign that growth capital continues to recognize performing companies who can make it past the Series A. H1’24 saw a flurry of mega-deals at the Series B stage, from EV-charging company Electra raising a $330m round to expand operations to TES developer Antora Energy raising $150m.

Growth deal size decreases, but that may not be the full picture. Deal size at the Growth stage declined 21% from H1’23 — but as the climate capital stack sophisticates, we’re seeing more than just venture funding coming into the growth picture. H2 Green Steel paired a $372m Equity raise with a $4.5bn Debt raise, and Sunfire’s Series E equity raise was followed by a $108m loan from EIB.

Vertical

Energy steals the top spot from Transportation in H1’24

Transportation’s sharp decline from H2’23 puts Energy on top. Investment in transport was down 22% from H1’23, and a whopping 60% from a high in H2’23, although that was primarily driven by several mega-deals (such as battery recycler Redwood Materials’ $1bn Series D raise, battery makers Verkor and Hithium’s Series C raises of $905m and $605m, respectively, among others). Energy only declined 7% in H1’24 compared to H1’23, remaining the most resilient vertical.

Last year, Energy beat Transportation for the first time in attracting the highest number of investors — and we predicted that 2024 would be the “year of Energy”.

Across-the-board drop in H1’24 compared to H1’23. The average drop across all verticals was 24%, compared to H1’23. Funding to Transport, Energy, and Food — the “Big Three” verticals — dropped by an average of 15%, compared to the prior year. However, Food & Land Use had some green shoots, increasing 20% from H2’23.

Transportation and Energy cumulative total unswayed

Transportation and Energy domination still persists. These two sectors still account for ~60% of all total investment.

Batteries lead the charge. The share of investment towards Batteries is still larger than three least funded verticals (Climate Management, Built Environment, Carbon) each.

Exits (or lack thereof)

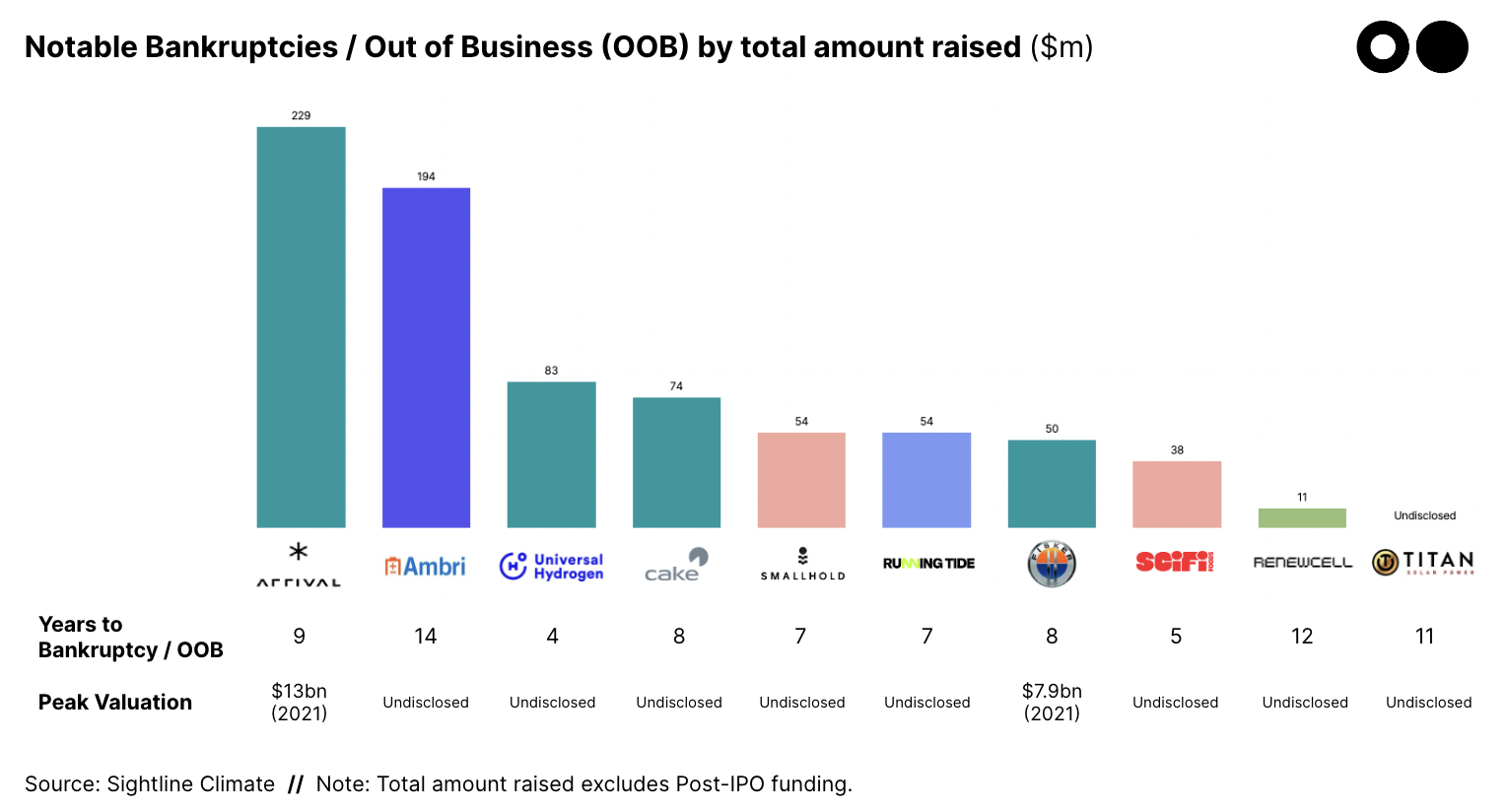

Bankruptcies hit high-profile climate tech cos

Challenges are vertical-specific. Bankruptcies / out of businesses this half of the year were plagued by scaling challenges, from cost of production to regulation risk to consumer skepticism.

Transportation: Arrival, Fisker, and Cake failed to meet production targets and suffered from product quality issues, leading to costly recalls. Arrival and Fisker, who both went public via SPAC merger, joins the growing list of EV companies that have crashed from all-time peak valuations of $13bn (2021) and $7.9bn (2021).

Food & Land Use: H1’24 brought about the bankruptcy of Smallhold, a mushroom vertical farming company, and SciFi Foods, a cultivated meat company, shut down operations. Smallhold cited lack of demand due to a spore-adic mushroom market, while SciFi Foods faced regulatory hurdles preventing them from even entering the market.

Energy: Ambri, backed by Breakthrough, filed for bankruptcy after failing to find financing for their manufacturing facility in Milford. Even though they had signed multiple MoUs to deploy their liquid-metal battery, investors were unconvinced about their path to commercialization, despite being founded 14 years ago.

Show me demand. Many of these bankruptcies / OOBs failed to attract new financing due to the lack of demand. Universal Hydrogen had successfully piloted their hydrogen-fueled regional plane but failed to attract customers, especially as SAFs took center-stage in the aviation industry. Running Tide closed down, publicly citing lack of demand in the voluntary carbon market. Titan Solar Power also shut down, due in part to high interest rates and struggling residential solar demand.

Decade milestones are hard to reach. The median time tobankruptcy of the H1’24 Bankrupt/OOB companies cohort was 8 years. Only three companies made it above the decade mark (Ambri, Renewcell, Titan Solar Power), but the likes of Universal Hydrogen and SciFi Foods flamed out faster.

Investors

Sharp decline in repeat investors H1’23 vs. H1’24

Total unique investors takes a hit. The number of total unique investors has declined on average 44% across all verticals.

Repeat investors (5+ deals in one year) also plummets across all verticals. In H1’23, repeat investors accounted for 30% of all investors (2+ deals in one year) but this has declined to 14% as of H1’24. This means that there are more non-repeat, “tourist” investors taking trips, but fewer investors staying long-term.

Energy continues to attract the most investors. Total investment into Energy not only overtook Transportation this half-year, but the vertical has also attracted the most investors, with 173 investors making deals in H1’24.

Climate generalists top early and late-stage

Climate generalists take the lead in earlier stages. Investors like Lowercarbon, SOSV, Breakthrough, Climate Capital, and MCJ Collective have become known names in the early-stage climate investing ballpark, with more early-stage deals under their belts since 2020.

Breakthrough center-stage at late-stage. Breakthrough continues to top the late-stage leaderboard, with Temasek and Energy Impact Partners following closely behind.

Institutional investors top Growth stage. Temasek, Goldman, and Canada Pension Plan Investment Board (CPP Investments) have participated in notable Growth rounds, separately and together, since 2020. For instance, CPP and Temasek were lead investors in Perfect Day’s $350m Growth round in 2021.

Methodology

Asset class: This funding report captures only Venture Capital and Growth Equity deals that have been publicly announced through regulatory filings or press releases as of June 30th. We also verified deals directly with the most active investors. Where other market observers may promote larger climate market sizes, we stay true to our Climate Tech VC name and carefully exclude:

We’ve long held that climate tech is a theme not an industry. Our definition of climate tech comes with two filters: 1) climate impact and 2) climate vertical. Companies must tick the box in at least one category for both filters in order to make the cut.

Climate Verticals: In addition to having climate impact, companies must fall into at least one of the seven broad climate verticals below. These verticals encompass 60+ sectors and 250+ technologies helping us mitigate, adapt, monitor, remove, and regenerate in our warmer and weirder world.

⚡ Energy - The electrons and fuel that power us

Sectors: new generation technologies (e.g., nuclear, solar, geothermal), energy storage, hydrogen and other low-carbon fuels, enabling renewables software, marketplace, and grid management platforms, DER and demand response tools, utility transmission and distribution services

🚗 Transportation - The movement of people and goods

Sectors: battery technologies, EV autos, EV charging and fleet management, electric micromobility and ridesharing, zero-emission planes, boats, and trains, urban public transport

🌾 Food & Land Use - The nutrients and resources that give us life

Sectors: alternative proteins, regenerative farming, vertical farming, sustainable fertilizer and animal feed, nature restoration and ecosystem services, remote sensing for crop yield optimization, autonomous farming equipment, water tech, and food waste reduction

🏭 Industry - The goods and raw materials we use every day

Sectors: low-carbon cement, chemical and plastics, steel, manufacturing, metals and mining, circular economy commerce, sustainable textiles and packaging, waste and recycling

🛰️ Climate Management - The data, intelligence, and risk associated with a changing climate

Sectors: emissions and sustainability reporting, earth observation through remote sensing, climate risk and intelligence platforms

🏠 Built Environment - The places we live and work

Sectors: sustainable building materials, low-carbon heating and cooling, prefab construction, energy efficiency, building electrification and energy optimization

💨 Carbon - The avoidance and removal of emitted carbon

Sectors: carbon offset marketplace and procurement platforms, carbon utilization, carbon removal and storage technologies, point-source CCS, verifiers and ratings enablers

NOTE: You may notice that some of our numbers are larger in this update than previous editions. We constantly update the dataset to have the most accurate data possible, including adding post-dated deals.

Have a different take on what’s driving these climate tech investment trends? Or questions about our analysis? Drop us a note at [email protected] if you’re looking to dig deeper into the H1 2024 funding numbers.