What goes down must come back up? After the slowdown in climate tech investment for most of 2023, new data points to a potential proximate rev up: We’ve now seen a spike in climate-focused fund announcements and record deployment for the past two quarters.

Today, we’re releasing our updated Dry Powder report — for the first time since Q3’2023 — tracking the ~270 climate investment funds that have been announced since January 2021 with caches of earmarked cash. (Read more about our methodology at the bottom of this newsletter.)

Even as Pitchbook reports that venture capitalists are struggling to find LPs with risk-on appetite for funds — landing just $30.4bn in closed institutional capital in Q1 of 2024 — we’ve tracked $3.1bn of commitments to new climate funds in the same time, about 10% of that total. In fact, the amount of dry powder being added to the tank in Q1’2024 nears the heights of the ZIRP craze phase. Wondering what’s going on? Read on for the hard data and hot takes.

Want to double-click into this dataset? Drop us a note at [email protected] or request a demo here.

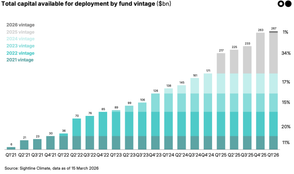

💰 Climate funds raked in $217bn of private assets under management (AUM) across 267 new VC, Corporate VC, Growth, Infra, and Private Equity funds that have announced their final close since we began tracking climate dry powder in January 2021.

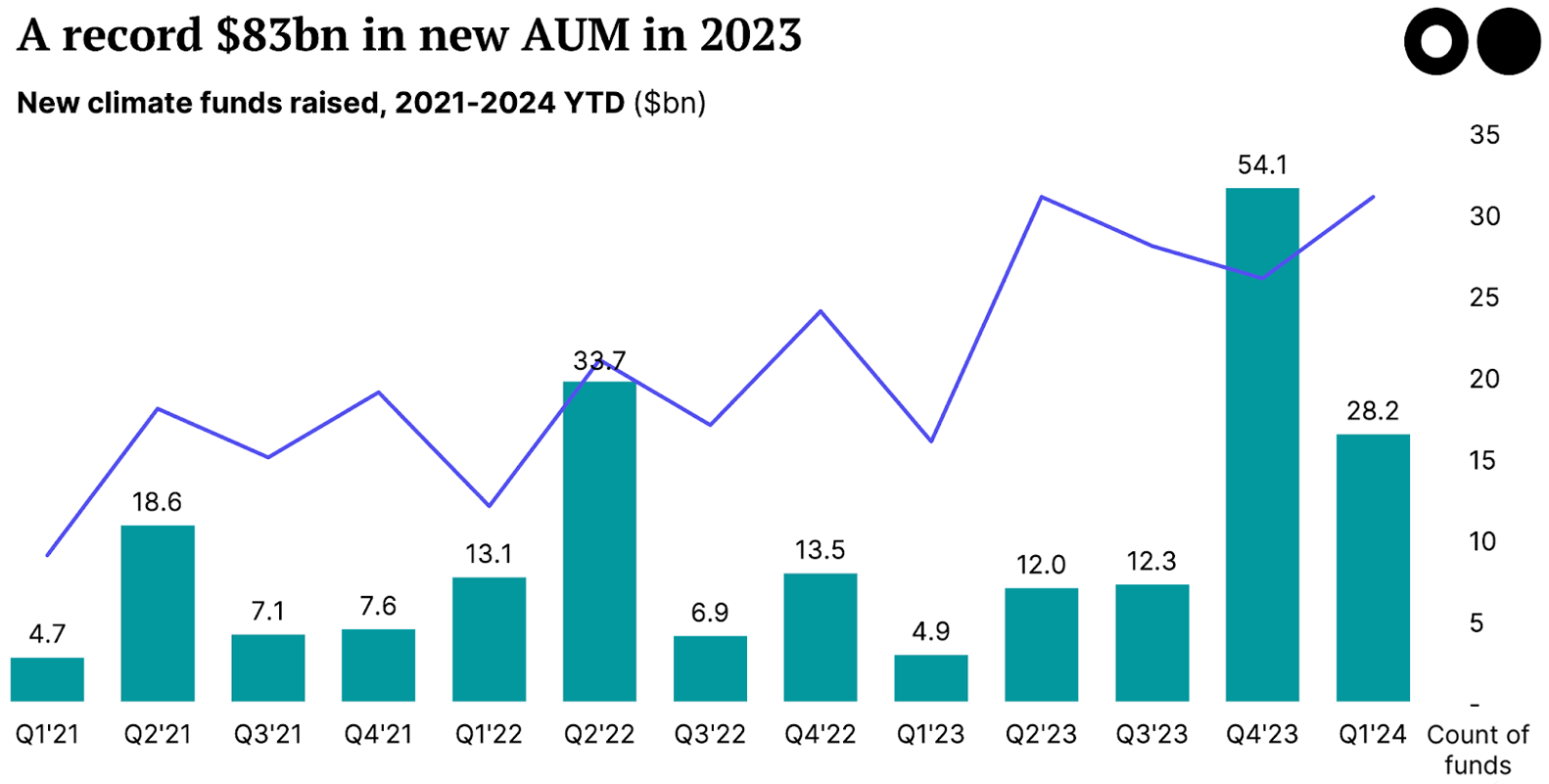

Despite today’s tough fundraising environment, climate funds have landed: 63 new funds have raised $82bn in fresh closed capital since September 2023, with $28.2bn and 31 new funds in 2024 alone.

Year-to-date 2024 is already ~75% of the way to smashing the total 2021 cumulative fund-type AUM. And the number of new funds has nearly doubled since last year, with 31 so far compared to 16 in Q1’2023.

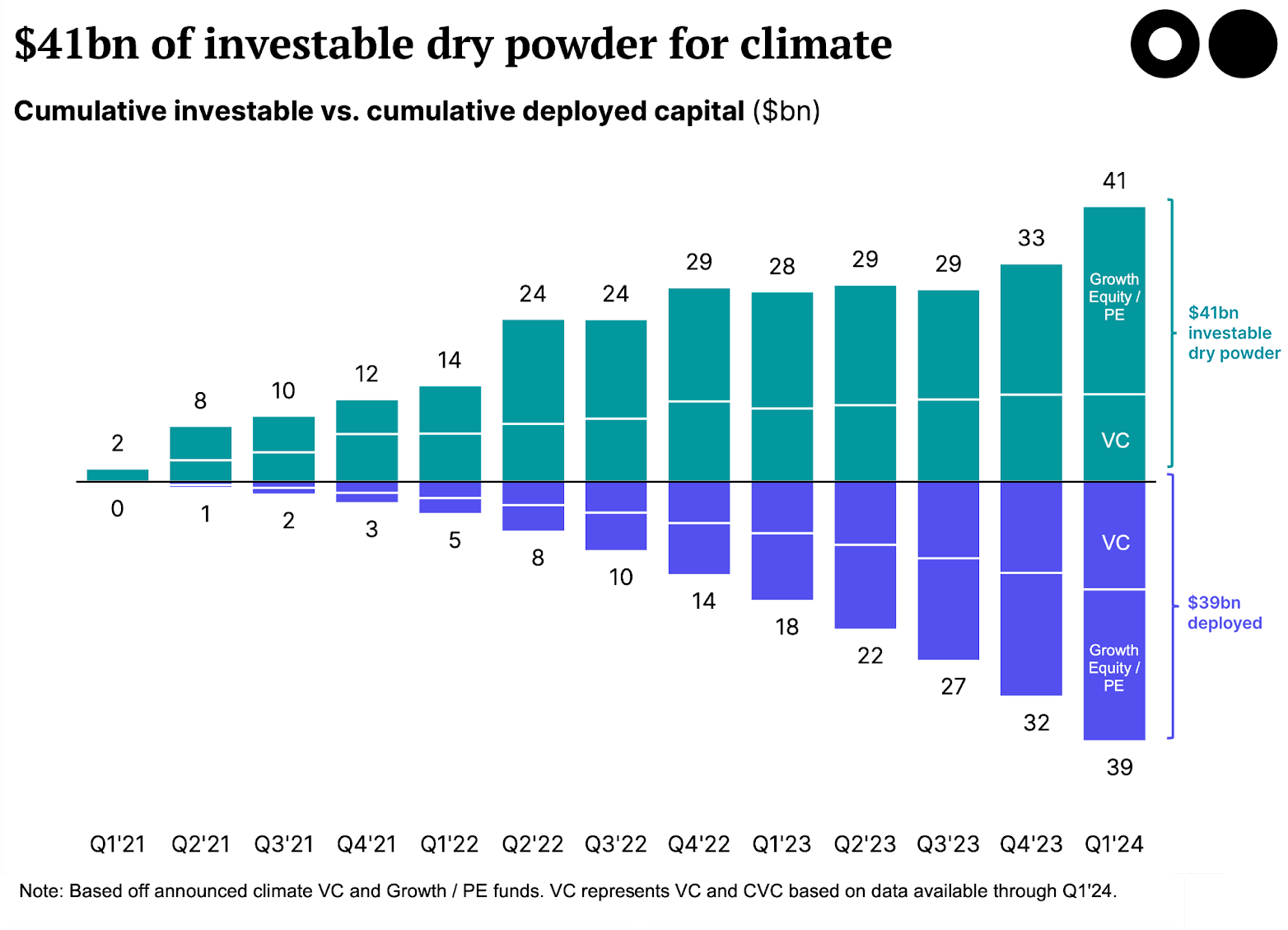

🔢 We estimate that funds have deployed $39bn into climate companies since 2021. After excluding Infra funds ($93bn) and removing management fees ($44bn), that’s $41bn of remaining investable dry powder, ready to deploy in climate, from existing closed funds.

🧾 It isn’t just VC creating climate dry powder anymore. The types of investors joining climate funds — and accordingly, the goals of these funds themselves — are diversifying, as moreGrowth Equity / PE and infrastructure firms enter the chat. VC continues to grow at a consistent pace, but a record 13 Growth Equity / PE and Infra funds were announced with an outsize $50.4bn AUM in Q4’2023. Compare that with the 8 funds with $8.4bn AUM announced in Q4’2022.

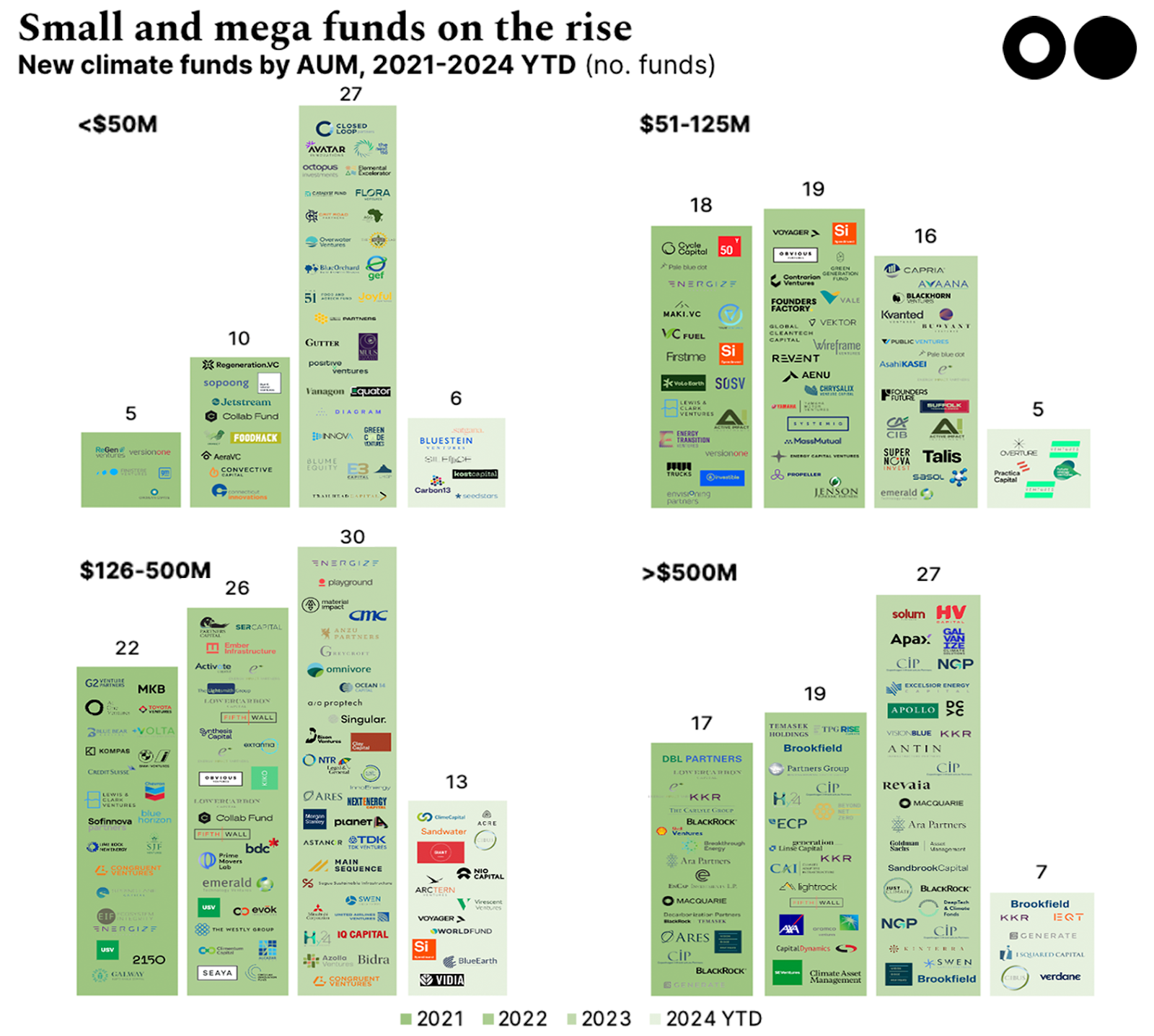

📈 The majority of new capital is concentrated in the 22 mega-funds ($500M+) announced in the past two quarters, which account for 46% of new funds by count and make up ~95% of total AUM. That’s a step up from the same time period a year ago (Q4’2022 - Q1’2023), in which 15 mega-funds were announced — 38% of all new funds — with 83% of all AUM.

Inside the dry powder keg

With all of the data in for the end of 2023 and the start of 2024, here’s the shape of new capital ready to deploy in climate tech.

Since our last analysis in September 2023, climate fund managers have closed $7.5bn in VC (including CVC) and $24.9bn in Growth Equity / PE.

In 2023, climate funds deployed $18.2bn of dry powder — comprising 56% of all tracked 2023 investment.

New money in the game

At the end of 2023, a record number of funds announced — particularly Growth Equity / PE funds, which tend to have higher AUM than VC. Of course, fund announcements are a lagging indicator of interest in the market, because rallying LPs to raise a new fund takes time (even more so in today’s risk-off LP environment). We tracked funds based on the date of their most recent close announcement, when we have confirmed information on total fund size. In reality, these funds are likely actively investing a year (or a few!!) before announcing their final close.

The final numbers for 2023 reveal the highest annual count of fund announcements yet: 100 funds, far above 2021’s 62 and 2022's 74.

2023 also smashed new annual AUM records: $83bn fresh capital, far exceeding 2021’s $38.2 and 2022’s $67.3.

2024 year-to-date is already on track to top the trend, with 31 new funds YTD and $28.2 new AUM.

Who’s got money in the bank?

In the last two quarters, the greatest growth in count of funds (22, compared to 15 the year before) came from the largest fund size, the mega-fund >$500m category. Bias to scale mirrors LP’s preference for platform vehicles, where they can park large single slugs of cash, for their underwriting work.

Naturally, the mega-fund category, which makes up 46% of new AUM in the last two quarters, is dominated by Growth Equity / PE and Infra funds. Some of the biggest money drops were Infra funds (Brookfield’s eye-popping $28bn fifth flagship infra fund, Brookfield’s $10bn second Global Transition Fund, and Macquarie Group’s $8.7bn European infra fund), which can finance mature infra assets from climate solutions, like renewables, all the way to traditional infrastructure, like roads or telecom.

The maturing climate capital stack

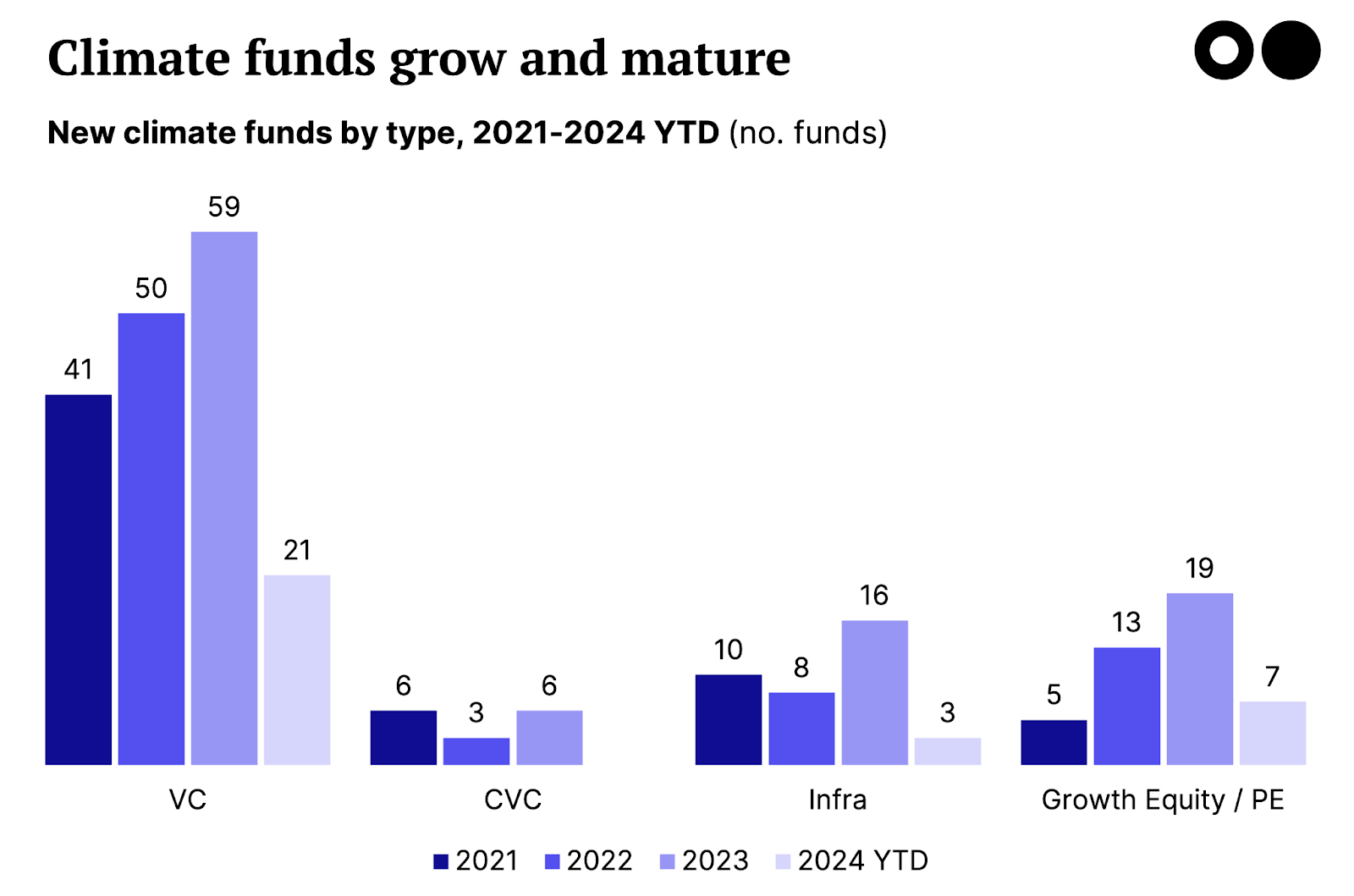

Climate VC funds top the list of new fund announcements, continuing the trend from early 2023. There were 21 new VCs announced in the first quarter of 2024, more than 2X the amount compared to the same period in the prior year.

Still, more and more funds from non-VCs are being announced as the climate capital stack evolves: a whopping $51.6bn in infrastructure funds announced since our last analysis in September 2023. The number of Infra investors came in at 8 in Q4’2023, a 2x of the 4 announced in Q3’2023.

Key Takeaways

New VC capital for sunnier deployment days. VC deployment had slowed in 2022, compared to its fast pace during the rapid-fire, ZIRP days of 2021. However, VC funds continue to stack the dry powder, with a smattering of small newcomers and proven veterans coming back for their second and third funds.

Infrastructure funds locked and loaded. The biggest pickup has been in infrastructure fund announcements, many with massive reserves and a partial mandate (or at least callout) for financing sustainable assets.

Missing middle. Despite all the capital being raised for early VC and mature infra, investors still hesitate to fund FOAKs. Simultaneously, even for non-hardtech, there’s a gap in late-stage venture bridging to true growth at the Series B+ stage.

Wait-and-see for deployment. Dry powder and deployment rates are not linearly correlated. Total climate tech funding outlays dropped 30% last year, as investors played wait-and-see for valuations to risk-adjust, the IPO window to reopen, and interest rate hikes to stabilize. In the interim, last year, many managers re-focused inwards on cushioning their own portfolio companies to bridge market uncertainty, and likely also on their own proactive fundraising.

The final rally. While climate dry powder remains robust, there’s a caveat: Fund announcements are lagging indicators of the market. It takes years (even more so today) to convert the first LP pitch to the final close and press release. The recent spurt in closed fund announcements and AUM might represent a last delayed marketing signal from the hyperboom 2021/22 market heydays.

What to watch

Blended capital to bridge the gap. Don’t expect to see any plays soon into FOAKs from Infra funds, despite the hype. Instead, expect to see more blended approaches to getting FOAK off the ground with non-institutional and catalytic forms of capital, namely philanthropy, corporate balance sheets, or government grants and loans. If companies (or technologies) could cross the gap to the Nth-of-a-kind (NOAK) project stage, then they would access the pile of infra dry powder earmarked for sustainable assets. While some infra investors are starting to explore expanding into emerging sectors that could follow a similar path to solar and wind (i.e., SAF, CCS, battery recycling), de-risked, investable companies and/or projects are still lacking.

Enter the asset owners. Keep eyes onasset owners, like sovereign wealth or pension funds, which have the patience and balance sheets to bridge the missing middle and match the capital intensity and longer commercialization timelines of climate tech companies. Some are either starting to spin up their own direct growth vehicles or bolster overall dry powder as LPs directly in the brand name PE funds they know best. Consider, for instance, the UAE’S $30b Alterra fund, announced at COP28. It’s already funneling $6.5B towards Blackrock, TPG, and Brookfield.

Bull vs Bear: We said this last time, and we’ll say it again: It’s a glass half-full or half-empty market, depending on your perspective. A lot of this capital could end up sitting due to a lack of investable companies or projects. If investor return requirements or risk profiles won’t match what companies need to scale, that yet again leaves companies stuck in the Series B range, unable to go further. On the other hand, it could be that we’re just getting started and you ain’t seen nothin’ yet. With all this capital raised (and relatively little deployed to date) we could see a lot more of it start to flow toward creating winning sectors and companies.

Flight to quality. Just like with startups, there will be a flight to quality fund managers with the best track records (and new managers with emerging structural and network advantages). It’s too early to make bets on climate tech liquidity, since the market and exit outcomes for this true “climate tech cohort” are still green, but LPs are sharply watching exits results. And it's not just in climate — it’s across the board. After the last decade of private market frenzy, LPs seem to be waiting for existing investments to return capital before making new commitments.

Behind the numbers: our dry powder math

Post-close: This analysis conservatively includes only funds that have announced the exact size of (at least their first) close - and excludes fickle announced targets.

Deployment period: We’ve assumed a 3 year deployment period, and also made the big assumption that funds deploy 100% of their capital during the deployment period. Realistically, deployment follows a wider bell curve as funds “reserve” capital to follow on to original investments.

Management fees: We subtract a full 20% of the fund size upfront to cover management fees, and assume that just the remaining 80% of AUM is used for investments. (2% annual management fee over a ten year fund lifetime). **Note this is a new assumption in our methodology compared to our previous analysis.

No recycling: We don’t include any assumptions for “recycling,” or taking initial returns from the fund performance and deploying it back into the fund (often to make up for management fees cutting into the investable AUM).

Fund type: We’re purposefully just representing dry powder for climate-specific venture, corporate venture, growth / PE asset classes (**excludes infrastructure).

Climate-specific: As with our definition for climate investors, we only include funds that meet our “impact” and “vertical” thresholds of a certain percentage of climate investment, by fund type. Our analysis isn’t accounting for dry powder from non-climate-specific funds that may cross over to invest into climate companies.

Are you seeing the glass half-full or half-empty in these findings? Want to double-click into this dataset? Drop us a note at [email protected] or request a demo here.

Newsletter

Newsletter