🌎 Two climate investors on raising in today's tough market

Q&As with Sophie Purdom, who just closed first-time Planeteer Fund I, and John Tough, who recently closed Energize Capital's mega-fund Ventures Fund III

How the US DFC is financing climate across the capital stack and around the world

Financing the climate crisis takes on multiple shapes and sizes across the capital stack - venture capital towards innovation, project finance and debt for building clean infrastructure, government aid and grants for adapting to new climate realities.

To avoid a climate catastrophe, we must invest an estimated $6T annually into climate by 2030. In 2022, we invested $1T - and a mere $40B in venture capital. While we’re not on track just yet, the past decade saw growing momentum, with public and private climate finance almost doubling between 2011 and 2020. But reaching the Paris Agreement target by 2050 will require climate investment to increase 6X by the end of this decade.

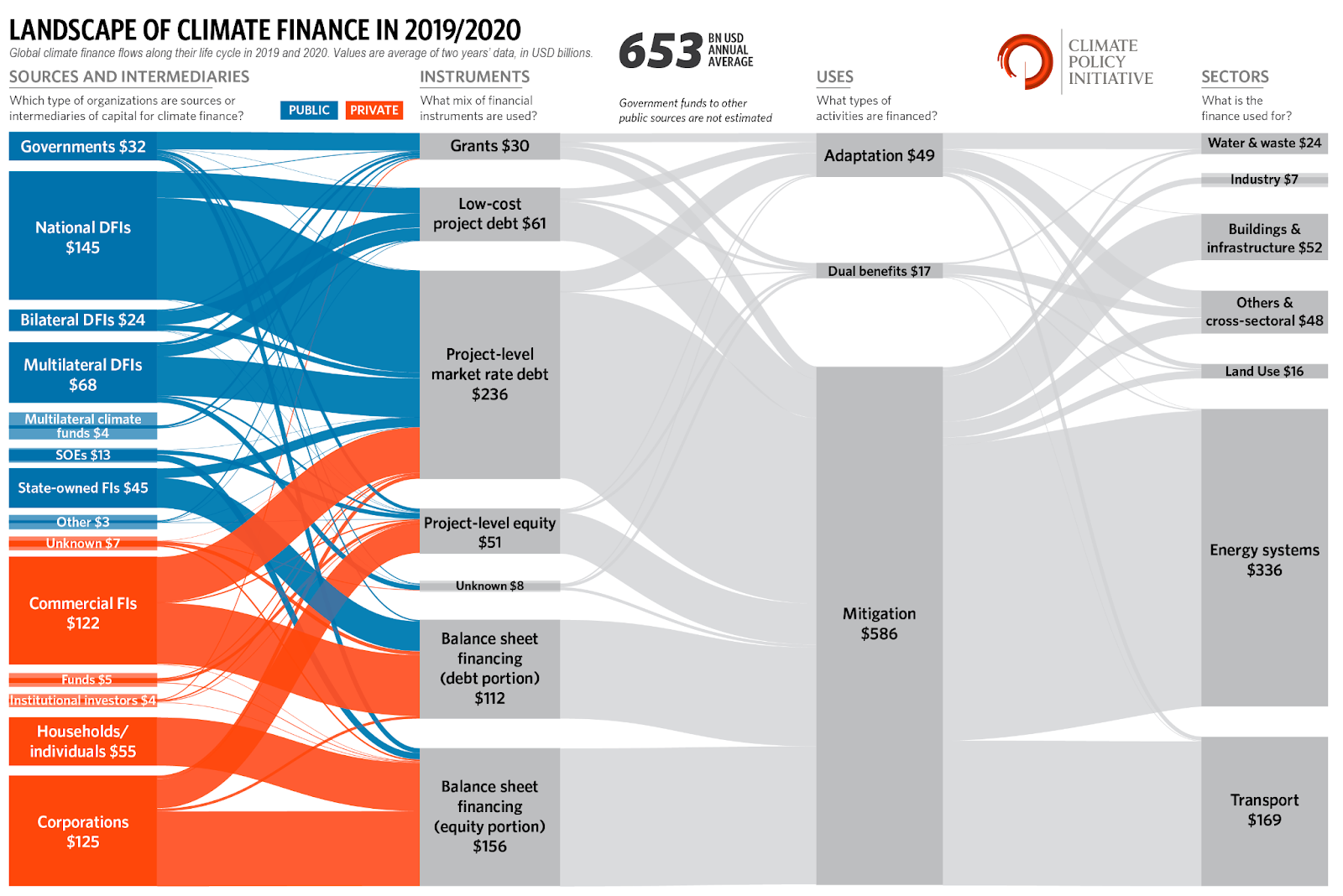

The actual term “climate finance” is most often associated with the international climate change negotiation processes, calling for developed countries to provide financial resources for developing countries to meet the costs of climate change. These financial resources originate from a wide variety of sources - both public (governments, to development finance institutions, multilateral climate funds, state-owned enterprises and financial institutions), and private (financial institutions, investment funds, institutional investors, individuals, and corporations).

Development finance (DFI, or also known as a development bank or development finance institution) is a special breed of climate finance that invests in private sector projects in developing countries to promote job creation and sustainable economic growth. DFIs may have different flavors of investment outcomes, from environmental and humanitarian to strategic for national security and global competitiveness. DFIs can be bilateral, serving to implement their government’s foreign development and cooperation policy (e.g. US IDFC), or multilateral, established by more than one country (e.g. the World Bank).

Development finance in the global climate finance stack:

The US International Development Finance Corporation (DFC) is one of the newest US federal agencies, a “startup within the government”. Established in October 2018 by the BUILD Act with the purpose of reforming and strengthening US development finance capabilities, the DFC follows in the footsteps of its older development siblings, the Overseas Private Investment Corporation (OPIC) and USAID Development Credit Authority. Unlike OPIC’s financial returns requirements to the US Treasury, the DFC’s “appropriate financial performance” responsibility under the BUILD Act widens its greater risk profile and encourages DFC to act as a key impact capital allocator - especially climate impact.

DFC is not alone. The international world of development finance is a crowded ecosystem, with a couple of leading players including British International Investment (BII), International Finance Corporation (IFC), and European Bank for Reconstruction and Development (EBRD) devoting significant amounts of capital to advance their strategic priorities across the globe. By the numbers, China has led the pack in bilateral aid, but the impact of their deployment is up for debate. With its $60B impact-driven capital mandate and Jake Levine at the helm as Chief Climate Officer, the DFC aims to provide an alternative investment source for borrowers that advances high environmental and labor standards - and they’re rapidly expanding their climate workforce.

What was your journey that led you to DFC?

I got my start in climate working in the Obama White House with the small team that set the first-ever GHG standards for cars and trucks, and laid the groundwork for the Clean Power Plan. After law school, I wanted to get experience in business, so I went to a startup called Opower, where I served as Chief of Staff and helped build our overseas presence in Latin America and China. When Opower was acquired, I returned to California, and teamed up with my state senator Fran Pavley and Assemblyman Eddie Garcia to pass state-wide climate legislation that for the first time sought to situate itself within an environmental justice framework, with two bills called California SB32 and AB197. Then when the Trump administration came into office, I helped Covington & Burling LLP set up their climate tech practice, where I led an effort to challenge the various climate rollbacks at EPA in litigations and regulatory proceedings.

When Biden won, I joined DFC to lead their climate effort, which combined my previous experiences but with an extra focus on the intersection of finance and foreign policy. DFC has opened my eyes to the enormous financing gap for climate mitigation in the places where the impacts hit hardest. I felt I could bring my experience in California and the private sector to bear on DFC’s mandate – and now we’re making a major push in climate that cuts across nearly all of our work. We’re hiring fast and expect to be posting more roles over the next couple of weeks, so please get in touch, or watch this space!

What does the DFC do?

Development finance is fundamentally about providing public finance for the purpose of advancing economic growth and mobilizing private sector resources in the places that need it most. We work in some of the most complex and challenging markets around the world, and we partner closely with the local business community - ultimately, if we’re doing our job right, we’ll set the private sector up to run us out of business.

The DFC, which is the US Government’s development bank, has also been designed to play a critical role in strategic and foreign policy engagement. We’re not just pursuing a development mandate, but a strategic mandate to advance US foreign policy that will position the US to compete and win in key regions and markets. This adds an interesting dimension to our work, in that we have to look at how our work sits against the backdrop of a global competition with other countries who take a different approach to development and foreign policy.

How does the DFC fit into the global landscape of development finance? How does this relate to the UNFCCC’s mandate for climate finance?

The DFC is not unique to the US - it’s one of several development finance institutions (“DFIs”) around the world. Within this ecosystem, we are the largest bilateral development finance institution, meaning we’re the largest, single-country shareholder institution. There are other, similar financial institutions, known as multilateral development banks (“MDBs”), like the World Bank’s International Finance Corporation, or the European Bank for Reconstruction and Development Bank, who are larger than DFIs, with many shareholders and stakeholders – including by the way the US government who plays a leadership role as a major shareholder in the MDBs. Within the DFI ecosystem, DFC has the largest mandate in terms of our ability to invest total dollars, with authority from Congress to invest up to $60 billion. If we reach that cap, Congress might decide to legislate to increase it.

With regards to the UNFCCC’s mandate, we aren’t formally associated with the UN, but we’re active in several multilateral partnerships. In places like Vietnam, Indonesia, and South Africa, for example, where the US is working alongside G7 partners toward advancing “Just Energy Transition Partnerships,” DFC figures very prominently in the US commitment to those frameworks. We’re active in those markets building pipelines, assisting in clean energy deployment, exploring coal retirement transactions, and focusing on investments that can create pathways for job creation and manufacturing infrastructure. So while we don’t have a formal relationship with these commitments, we continue to work in partnership alongside those efforts.

Where does international development finance sit within the “climate capital stack”?

DFC actually sits across the entire spectrum of the CTVC climate capital stack. We provide financial products ranging from grants to project finance, and equity, debt, guarantees and political risk insurance. Our diversity of approach is a reflection of our statutory authorities, and how we’re seeking to deploy those to meet a renewed and accelerated urgency within the Biden Administration to scale public finance across a range of climate sectors and geographies.

To date, DFC has been concentrated to the right of the capital stack – in project finance, commercial debt, and a little bit of venture debt slash growth equity. Historically, we’ve been more skewed toward commercially-viable projects, and we remain best placed to help scale proven tech and business models. But Congress has given us the mandate to think about risk differently as we approach our work, and that’s allowed us to do things like deploy equity in more forward-leaning ways. The goal is to move to the left and scale our work with our technical assistance grants, earlier-stage equity, and mobilizers like guarantees and insurance that can have an even more catalytic effect in terms of the way we’re enabling private sector players to direct capital investments toward the epicenter of the climate crisis – which is in emerging markets.

What is DFC’s investment mandate? How do you think about balancing return and impact?

We seek to balance impact and return – but whereas our predecessor agencies actually had a return requirement, DFC has a requirement to generate “an appropriate financial performance.” That gives us a tremendous amount of latitude.

Our mandate is also broad across sectors and geographies. Climate spans nearly every industry – power, transportation, buildings, and so on. Geographically, we have sought to focus in markets where there’s both a pronounced need for decarbonization, as well as a need for adaptation and resilience – places like Vietnam, Indonesia, India, Pakistan, Nigeria. But we have a global mandate to work in lower-income countries, and we’ve seen enormous opportunities – from Eastern Europe, where electrification can mitigate dependence on Russian imports of oil and gas, to Latin America, Central Africa, and Southeast Asia, where we’re exploring how a tremendous wealth of nature-based resources could be preserved and monetized through carbon credits.

There’s a lot to do – and the really exciting thing is that we’re building out our expertise by hiring investors and climate policy experts who understand and can push forward our mandate.

Walk us through some of the DFC’s recent climate investments

Trella (Pakistan): One of the really exciting investments that we did recently was in Pakistan. Through a financial intermediary, we supported a company called Trella, which is creating a digital marketplace for shippers and truckers to create efficiencies in routing, inventory, and space allocation.

Golomoti solar + storage (Malawi): In Malawi, we made a $25 million loan for a battery energy storage system to be constructed and installed in tandem with a solar power plant. The country has recently experienced a historic drought, which left something on the order of 25% of its electricity generation capacity out of commission, and this new power station has provided critical grid capacity resources.

Blue Bonds (Belize): In Belize, we committed $610 million of political risk insurance (“PRI”) in a transaction with Credit Suisse and the Nature Conservancy to help Belize retire $354 million of sovereign debt and reissue a new investment-grade bond. DFC’s PRI protected the bond from what would have been a B-minus rating. That new bond will create about $180 million of debt service payments that will go towards coastal resilience, alongside a set of policy interventions and commitments by the government.

Other notable projects:

Do you see a trend of new innovation or “fast follower” deployment in these developing countries?

We see a little bit of both. For example, in India, there’s a huge two- and three-wheeled sector of the transportation industry that’s now getting electrified. We supported an e-mobility bike company called Yulu through an $80 million raise. The innovation is not in the technology, but in the business model, where mobility-as-a-service allows new providers to come into the market. In Rwanda, we supported a company called Ampersand, which provides mobility-as-a-service through a battery swapping electric motorcycle business. We’re also looking at companies in Sierra Leone working on battery swapping innovation that you really don’t see taking root in the US.

In contrast, we’re seeing “fast follower” large-scale industrial projects taking shape, including a green hydrogen project in Egypt last year. Solar, wind, and offshore wind are also picking up in areas like Vietnam, Indonesia, and South Africa where there’s a global marketplace.

How does DFC fit into the US’s wider climate tech ambitions?

You can think of DFC almost like the international LPO (Loans Program Office). We’re different in that we can offer more financial products, but very similar in the way that we think. In fact, there are some transactions that we’re working on together.

For example, we’re both focused on increasing our investment in the critical minerals supply chain, including in the materials we need to power a clean energy and electric future. I can’t talk about it yet, but we’re working on a pioneering transaction in this space where the offtaker would be well-placed to take advantage of the financing tools LPO can offer to facilitate their construction and operations in the US. We enable each other – without the offtake, the project isn’t bankable for us, and without the supply, the project isn’t bankable for LPO.

What about relative to the current geopolitical climate tech arms race, especially bearing China in mind?

DFC has a really big role to play here. Right now, China dominates the supply chain of most of the key verticals, all the way upstream to mining and processing of materials. That is the result of many years of underinvestment by the United States, and many years of strategic investment by our competitors. We’re seeking to reverse that trend by diversifying the supply chain. For example, last year, we took a $30 million stake in a critical minerals production company called TechMet. Our initial focus is a nickel development project in Brazil, which is a key input into battery systems.

We think that DFC, alongside its partners in the G7, offers a compelling alternative to the kind of financing that borrowers see from China, which engages in a kind of debt-trap diplomacy, and doesn’t uphold key standards around environmental, social, and labor standards. We’re here to provide an alternative that’s more sustainable and that may require a few more checks and a bit more vetting on the front end, but that ultimately puts our clients and borrowers in a better financial position for the long-run. So far, we’ve seen that this has been a message that resonates with key partners around the world.

How has the IRA impacted your mandate at DFC?

The IRA has been a full-throated US endorsement for the clean energy economy of the future. It gives us tremendous credibility that we did not have before when we were sitting across the table from foreign governments or potential clients and borrowers. The IRA provides key tax credits, investments, and support on the domestic side, and in a way, DFC provides a similar kind of support for projects overseas. So although the IRA doesn’t technically relate to us, it can give us a guidepost for how we think about prioritization and industry focus. I’m also excited to see how it will create opportunities for us to work on projects with the DOE across the US and other jurisdictions.

For folks looking for financing or learning more about how to contribute, reach out to Jake or the DFC team! DFC is also looking to partner closely with the financial services sector - banks, investors, and private equity. Interested in driving climate finance? DFC is hiring for multiple positions, including 4 climate director positions in its sub $50M loans office to underwrite loans up to $50M for projects and companies in emerging markets.

Big shoutout to Claire Yun and Camille Bangug for their help developing this story!

Q&As with Sophie Purdom, who just closed first-time Planeteer Fund I, and John Tough, who recently closed Energize Capital's mega-fund Ventures Fund III

A Q&A with Precursor's David Yeh and Mark1's Julian Ryba-White, new strategic partners in the ecosystem

A Q&A with the DOE LPO director Jigar Shah and Solugen CEO Gaurab Chakrabarti