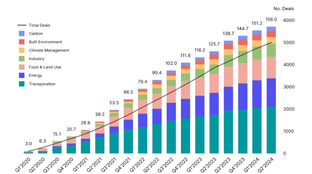

🌎 A weak $11.3bn start to 2024

Poor performance this half as investment falls to 2020 levels, but some strong plays.

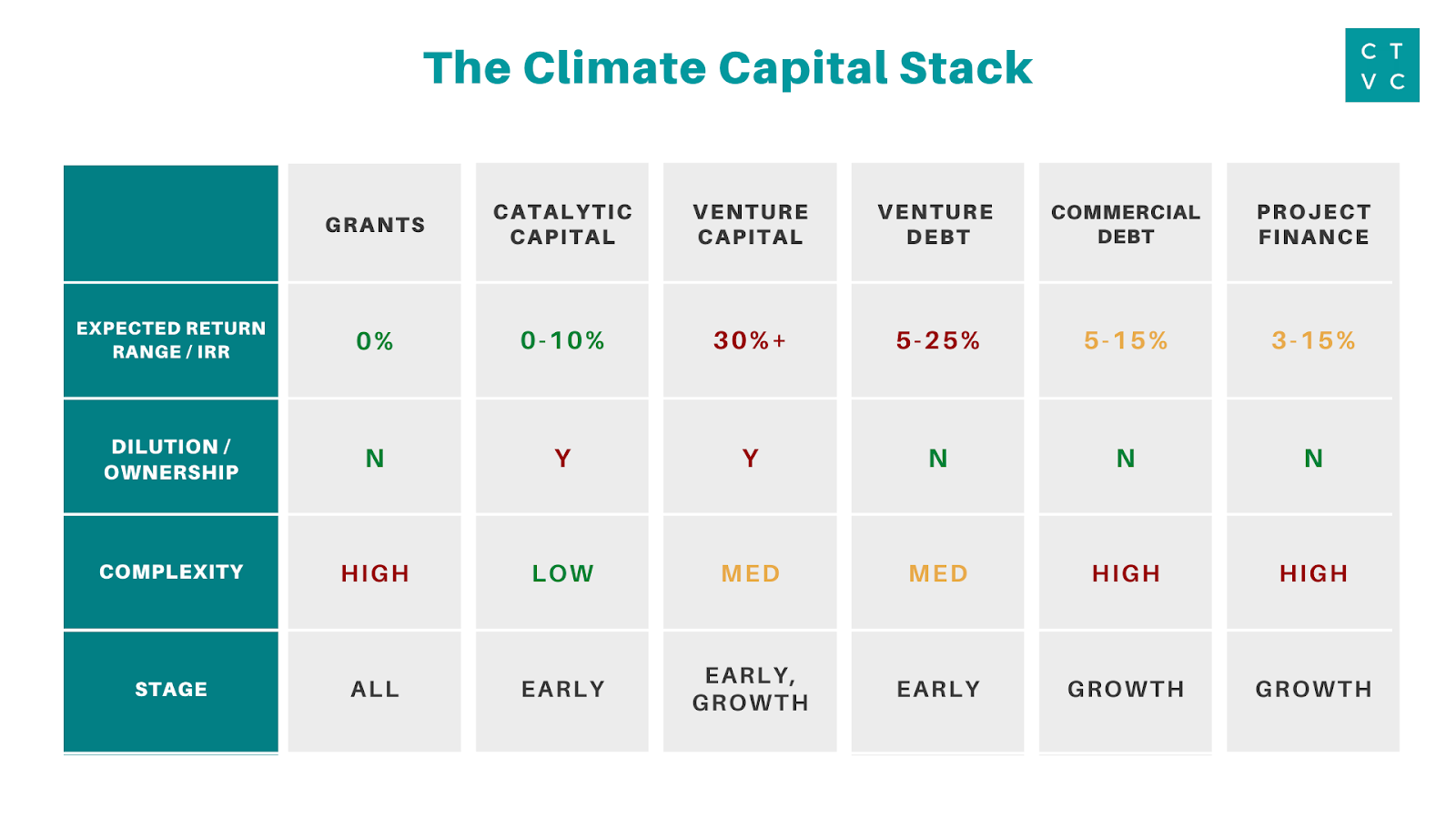

A buyer’s guide to financing your climate venture (not just with venture)

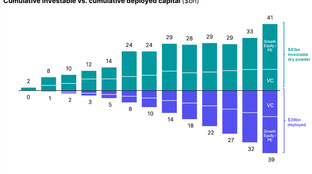

Despite the climate tech market’s accelerating pace, scientifically-speaking, it’s still nowhere near enough. To avoid a climate catastrophe, we must invest an estimated $4T annually (just in infrastructure!) into the clean energy transition globally. This year, we invested $800b - and a mere $32b in venture capital.

Science tells us that we need to scale up total climate investment at least 5x annually. Venture capital investment into climate tech is doubling YoY, but the funding gap is not closing fast enough. To cross multiple technical valleys of death, particularly in hard tech, innovators need not only more capital, but more types of financing.

The goal of this resource is to accelerate your climate tech venture’s growth by more efficiently identifying and accessing capital. Despite our name, we believe looking outside of venture towards the full stack of climate tech financing options is critical to hitting individual and collective escape velocity.

In any industry, there are different kinds of capital for different kinds of businesses and the kind of capital you take will likely inform your business strategy - if not entirely direct how you run your business. Your cost of capital will ultimately determine your ability to scale, and in climate specifically, capital tends to have an outsize influence earlier in your journey through growth. The capital you bring on board should either be a) cheap and/or b) value add —most of your challenge will be figuring out whether a) or b) are true across stages, structures and multiple possible strategic paths.

📈 Expected rate of return: What are your investors (and their investors/LPs) expecting from you? By and large, the degree of risk (early) determines the rate of return (high). If you’re early and can deliver high return, you can access smaller amounts of riskier though oftentimes more expensive capital. Quick overview (preview of thinking about rate of return) here.

⚖️ Dilution / ownership: What will your investors’ bet on you cost you in equity ownership? Ownership vs. debt prescribes different expected versions of future revenue share. Do you dilute yourself early or take on a cost to be repaid in the future? Lots of resources on this elsewhere, including here and here. Your dilution during fundraising rounds also impacts your ability to issue equity to new hires, advisors, and other key stakeholders during the early days of your startup.

⌛ Complexity: What do your investors do to, for, and with you? There’s an inherent tradeoff between complexity of operational / financial covenants, control, timing, effort spent fundraising and associated costs. Simpler, no strings capital may not add as much as really getting to know a few investors that can be significant value adds - but the converse may also apply. It’s wise to think beyond this fundraise and set up your financing structure to scale across to new markets and future fundraises.

An idea without action isn’t a business, and we need all shots on goal to solve climate change. Oftentimes, novel technologies without a clear path to revenue languish due to lack of initial funding to prove out a concept. Non-dilutive, project-based funding is typically unavailable at early stages due to lack of track record; it’s also limited in scale and often restrictive in scope, including specific details as to how funding can be used. Dilutive funding at this stage tends to be more open-ended, but at a much higher cost if the idea proves viable.

Pre-seed generally has the fewest rules and the least cookie-cutter approach to capitalization. The tradeoff is typically time (e.g. filling out grants) to dilution. Empty caveat around government funding is that the cycles can be long, particularly when revisions are involved, and the certainty expected of a proposal doesn’t always translate into the uncertainty you have to cross to get to product-market-fit. This type of funding also tends to come with reporting requirements after you’ve landed the grant. In climate specifically, philanthropists have been rushing to fill the void here over the past ~18 months, providing catalytic prizes, capital, and resources to get more fundable opportunities out there. There’s also a good amount of climate angels out there, though variance is wide in approach and growth expectations.

Philanthropic Foundations/ Private Grants/ Prizes: Non-dilutive project-based grants or competitions offering prizes to focus research on a specific area; typically tied to some timelines or demonstrations or progress. This can range from no-strings-attached cash to high signaling factor branding to primarily auxiliary benefits. To navigate the morass of climate grants, folks like Climate Finance Solutions offer help.

Carbon XPRIZE, NYSERDA, MassCEC, Emerson Collective, High Tide Foundation, Sea Change Foundation, Hewlett Foundation, Rockefeller Foundation

Government grants: Non-dilutive (public) capital to support specific technologies and research activities. Federal agencies that fund climate-related sectors include the Dept of Energy, National Science Foundation, EPA, Dept of Defense, Dept of Transportation, and Dept of Agriculture. Grant announcements for many agencies are here, but some specific places to look include:

SBIR grants: Grant funding for specific R&D projects in small businesses, awarded by many agencies across the federal government

ARPA-E funding: periodic Funding Opportunity Announcements (FOAs) focused on R&D in high-risk, high-reward technologies in energy and emissions (Check out this helpful video on how startups can work with ARPA-E)

Angel Investors / Syndicates: High net worth individuals, previous founders, etc. often pooling together into SPVs (group one-off deals) which are typically very network-based, low on diligence, and thesis / category driven

CREO Syndicate, Vectors Angel, E8, Keiretsu Capital, T-Bird Capital, AngelList syndicates like C3

Catalytic Capital: Funds bringing investment rigor and process to deals with a bias towards impact potential over financial returns

PRIME, Breakthrough Energy Ventures, Grantham Foundation, Clean Energy Trust, family offices, VertueLab

Rolling Funds: Investment vehicles structured like venture funds (LPs front capital so GPs can do multiple blind deals) but raised on a rolling quarterly basis, minimizing the hurdle to fund launch. Typically thematically or community-focused, with similar terms to VC deals albeit mostly following and unpriced (e.g. SAFE notes)

MCJ Collective, Climate Capital, Footprint Coalition

Crowdfunding: Product-focused and marketing-heavy fundraise hosted on a tech platform that enables access to greater pool of potential backers who do not need to be accredited investors

Raise Green (example BlocPower climate impact note), Kickstarter, Impact Kickstarter, Indiegogo

Accelerators/ Incubators/ Fellowships: Programs offering funding and resources such as strategic partnerships, advisors, and workshops to help founders build and iterate on their thesis. Programs run the gamut from general business accelerators like Y Combinator to climate vertical-focused ones.

Y Combinator, Techstars, Elemental Excelerator, Greentown Labs, LACI, Third Derivative, Activate Fellowship, Breakthrough Energy Fellows

For more top programs, we’ve just released an updated list of Climate Accelerators and Incubators.

New List of Climate Accelerators

Once a technology, company, or concept has some evidence of commercial viability or traction there’s a marked increase in the type of financing available to it; however, that financing boom comes with expectations of a return on investment. Capital here becomes critical for hitting product market fit, testing out go-to-market strategies, and building out the team to enable growth.

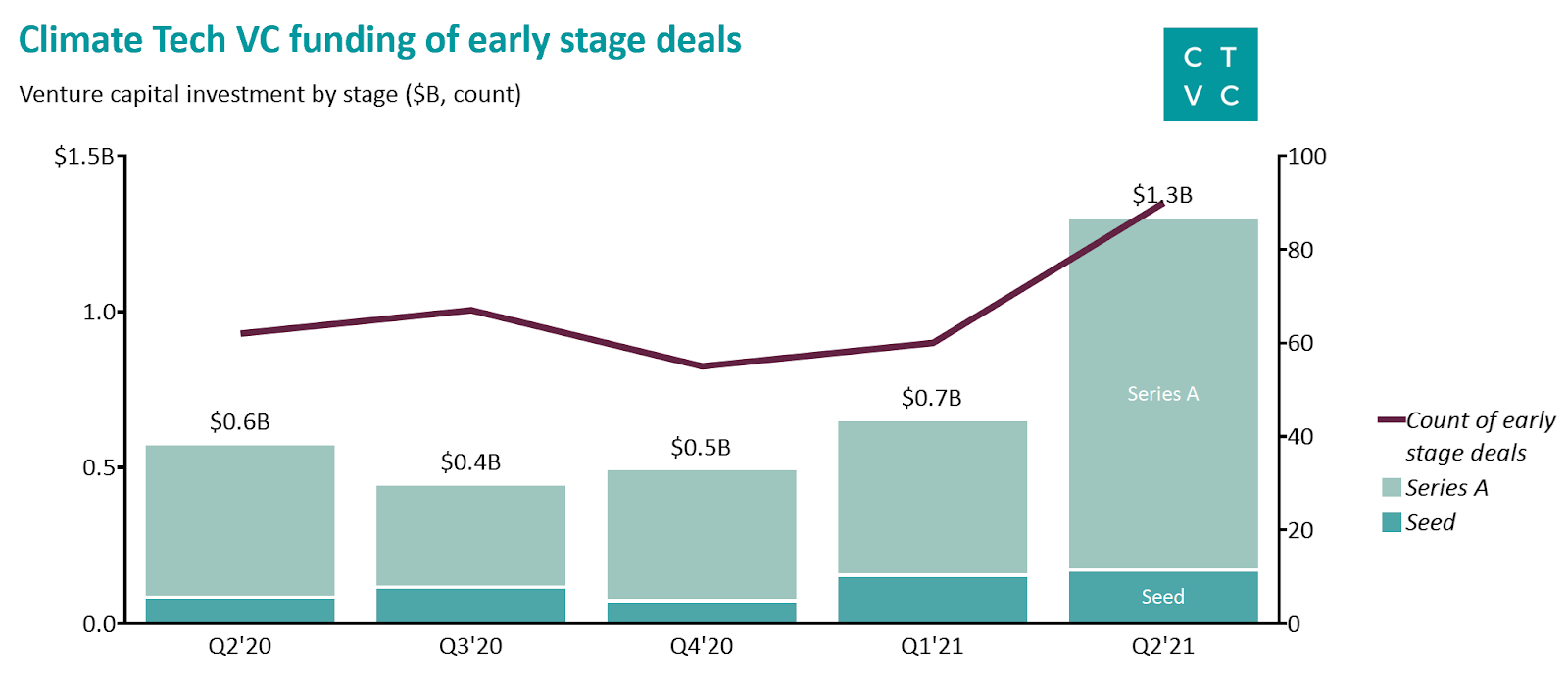

By Seed or Series A, you’ll likely have some proof of traction in the form of revenue, scale of your in-field pilot, or a prototype. Demonstrating customer demand or future potential revenue (with LOIs/MOUs) will be your main lever for preserving ownership and getting better terms. While big valuations and rounds make for great headlines, in climate businesses in particular the challenges of scale aren’t as immediately obvious even once you start getting early traction. Clarity in your expected milestones and an understanding of how much capital you’ll need to hit them, will keep current and future dilution in check. Specifically, you want to be mindful not to lock in future investment expectations from those you take money from early if you’re interested in exploring other sources of capital in the future.

Early-Stage Venture Capital: Seed to Series A capital in exchange for ownership of the company, dependent on fundraising terms of round size and valuation. If you’re reading this newsletter, odds are you’re familiar with the name of the game. Over 1,000 unique investment firms participated in a climate tech deal in the first half of 2021, though VCs vary dramatically in their value add, focus areas, and target stage.

We maintain The Running List of Climate Tech VCs to make it easier for you to source and filter the ~200 most active climate tech venture firms

Venture Debt: Loans designed for fast-growing Series A to C stage startups that allow founders to extend their capital and save dilution on the backend. Founders can pair equity with venture debt as a non-dilutive cushion to fund cash flowing assets. While commercial debt is typically underwritten to a company’s cash flows or physical assets, venture debt bets on the same adage of venture equity that valuations will continue to go up and the startup can raise more capital to repay the debt.

Venture debt’s key metric is loan to valuation, which is ~6-8% of the company’s last post-money valuation. Pricing consists of the interest rate, warrants, and an origination fee. Higher-risk of default leads to covenants and terms such as minimum cash on hand (6 months runway) and delayed draws based on hitting operational milestones. As with all debt, venture debt sits on top of the capital stack and gets paid out first before equity. Since many climate tech companies tend to lean more capex-intensive, venture debt offers a nice offset to equity for high-growth startups with a path to profitability. Companies fronting costs for EV chargers or solar installations can use debt to bridge the working capital shortfall before generating revenue from those assets.

Silicon Valley Bank is one of a few banks who offer venture debt, with the remainder comprised of a fragmented and underserved landscape of funds. Many VC firms have started venture debt funds to balance the capital stack, but there’s still a big void to fill here.

Silicon Valley Bank, Energy Impact Partners, TriplePoint Capital, Windsail Capital, Hercules Capital, Keyframe Capital

Alternative Credit: Other forms of credit that exist underwrite based off inventory, purchase orders, and revenue. Inventory and PO financing is useful for companies to pay for inventory and purchase orders before generating revenue. Revenue-based financing exchanges cash investment for a portion of revenue for a pre-agreed term or up until a cap is met. Although factoring, royalty financing, and other revenue-dependent instruments have existed in capital markets, the expansion of players like Pipe, Clear, and Decathlon have made RBF more mainstream for post-revenue high-growth startups with strong gross margins. Most RBF financiers focus exclusively on e-commerce and SaaS, but new entrants like Enduring Planet now offer RBF more broadly to climate companies.

Enduring Planet, Pipe, Clear, Decathlon, Urban Us

Pilot Funding: Non-dilutive funding options to build first of a kind (FOAK) projects. Typically companies must fund their first pilot or factory buildout off their own balance sheet with (expensive) venture capital. FOAK projects have a challenging credit profile, given the high upfront risk of being first of a kind and generating lower infrastructure returns. There’s a huge gap for alternative loan financing to bridge this valley of death of putting the first steel in the ground.

Breakthrough Energy Catalyst, LACI Market Access, Elemental Excelerator Projects

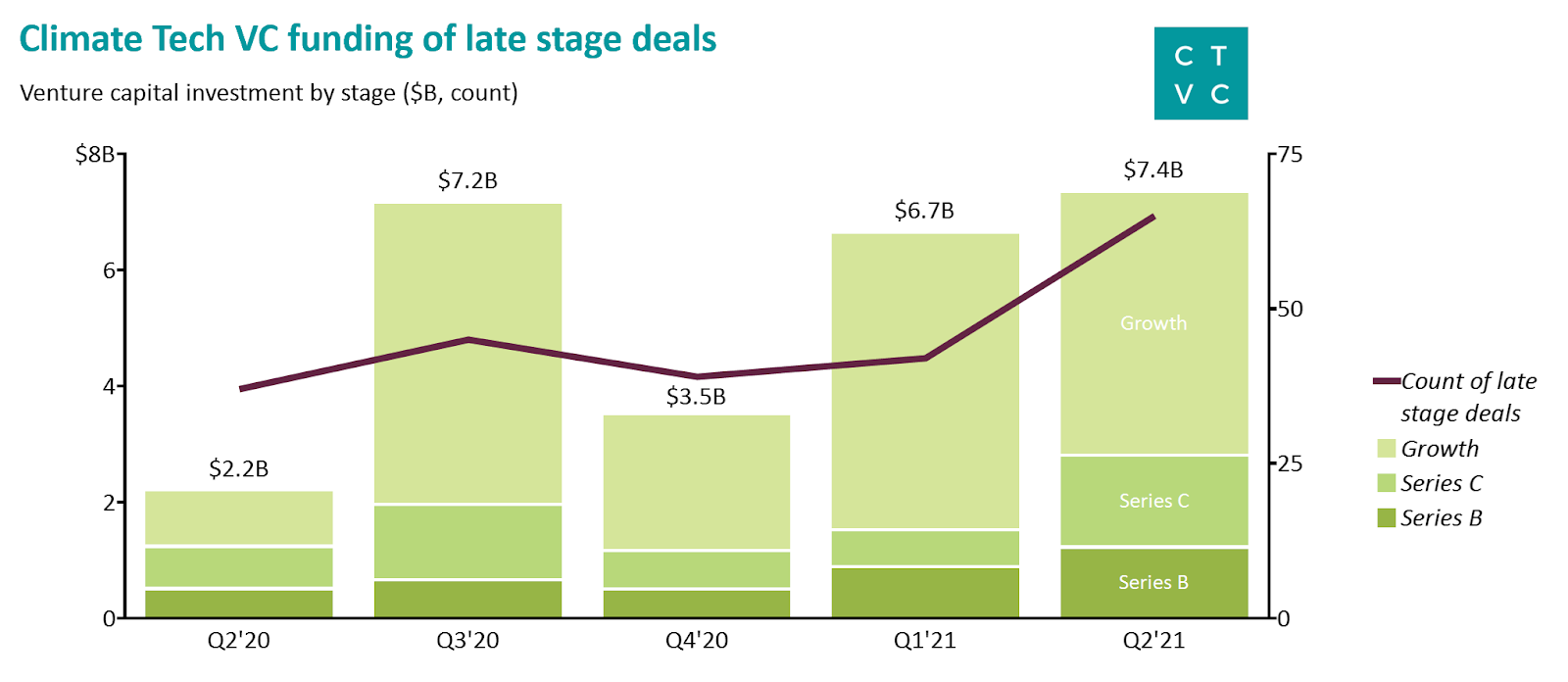

As you’re starting to hockey-stick your growth and have a viable path to scale revenue, your financing pathways open up exponentially - as do your means of spending all that cash. Be it bumping up product development, factory production, acquisition, marketing spend or org buildouts, your reasons for raising should be dollar for dollar compelling and create a path to shorter term, less dilutive capital now that you’ve reduced much of the typical execution risk. If you have real business metrics, the array of potential investors clamoring for the opportunity to invest will continue to expand - so long as your performance continues to exceed.

Growth Equity: A later breed of venture capital in the Series B+ stages, again exchanges capital for ownership of the company, dependent on fundraising terms of round size and valuation. Backers of growth stage climate tech companies run the gamut from traditional venture capital funds and corporate VCs to private equity, public-private crossover funds, and everything in between.

We created a list of the most active Climate Corporate Venture Capital funds to speed up your search, though it’s best cross referenced with growth investors from our other VC firm list.

Commercial Debt: Non-dilutive capital suited for later stage companies who have proven performance (aka EBITDA positive) and can borrow based off their cash flows or assets. Commercial debt can be sourced at earlier stages, but often comes at a hefty price tag and with personal guarantee requirements, complex and burdensome operational/ financial covenants, and lots of other strings. Depending on the credit profile of your company, cost of capital for commercial debt is likely the cheapest form of capital - ranging from single digit percentages to low teens. The structure of traditional commercial debt is more straightforward than venture debt, consisting of the interest rate, origination fee, and covenants. Here, the typical lenders will be commercial and investment banks. Later-stage debt comes in all types of colors and shapes - from lines of credit to smooth out working capital or secured debt backed by collateral.

Project Finance: Venture equity and debt fund companies, while project finance funds projects. Most mature hardware solutions get deployed commercially through infrastructure projects handled by a utility or project developer. Think of a project developer like a real estate developer - they identify a site, find a revenue stream, and organize all the project elements. Project finance is the art of funding those assets [read more about project finance from our Q&A with Scott Jacobs from Generate Capital]. At this stage, a project itself becomes a company (with its own LLC!) and has an entire capital stack including equity and debt that’s walled off from the corporate level.

Since infrastructure projects are seen as low-risk cash flow generators, project finance has a much lower cost of capital (3-9% for project and junior debt; 8-15% for infra equity). Traditionally, project finance has played well in the mature tech and large asset sectors - think: large solar and wind projects. Now some investment firms are taking this same toolkit and applying it to emerging climate technologies. While project finance is starting to take on more risks, there’s still a significant gap here in financing newer technologies like hydrogen fuel cells and anaerobic digesters to scale them faster than renewables did. Meanwhile, venture-backed businesses themselves like Perl Street and Banyan Infrastructure make it easier to execute these complex deals with technology.

Generate Capital, Springlane Capital, Vision Ridge, Sidewalk Infrastructure, Greenbacker Capital

DOE Loan Programs Office: More than $40b in loans and loan guarantees are available to help deploy large-scale US energy infrastructure projects. While the LPO is infamous for its simultaneous bets in Tesla and Solyndra back in Cleantech 1.0, new directors Jigar Shah and Vanessa Chan are reviving the Loan Office and Office of Tech Transitions, respectively, to be more accessible for climate tech entrepreneurs. They’re open for business - current available loans include ~$18b for advanced technology vehicles manufacturing, ~$11b for advanced nuclear energy, $8.5b for CCUS and other advanced fossil, $4.5b for renewable energy and efficient energy, and $2b for tribal energy development.

Purchase/ Procurement/ Partnerships: The power of the purse from corporates or governments can powerfully accelerate climate tech co’s growth through early purchases or offtake agreements, guaranteeing future revenue. By signing up early for orders pre-launch and paying some portion upfront, corporate or government purchases can fund climate startups’ buildout. For financing capital-intensive hardware or factories, it can make sense to form a JV, leveraging the corporate’s development and operational experience (and credit profile for bankability) and the startup’s technology innovation.

Amazon’s order of 100,000 Rivian electric delivery trucks; Stripe and Microsoft’s carbon removal purchases; Swiss Re’s 10 year $10m carbon removal partnership with Climeworks; joint venture between LanzaTech, Suncor, and Mitsui to establish LanzaJet

There’s a lot of ink out there already on multiple paths to exit, most of which are not unique to climate except for two key points: 1) later stage climate companies, particularly those with heavy government or project based financing, likely already have a high level of disclosure and obligatory reporting, and 2) public markets, due to various growing ESG mandates, are thirsty for companies that offset carbon or demonstrate a positive environmental benefit. These two factors make climate exits, when eventually they do come, a more attractive option to reducing your cost of capital to public market levels even if your business may be earlier by market cap or revenue than traditionally techy debuts. We’ve seen this acceleration already in the recent frenzy of EV SPACs, which while smaller by revenue, benefit substantially financially without trading off for greater scrutiny than they already were pre-public.

IPO/ SPAC: These acronyms both boil down to becoming a publicly-traded and owned entity. The climate tech SPAC frenzy has lost some of its luster since its summer heyday, though SPACs still remain a viable vehicle for capital-intensive solutions looking to go public. Good SPAC candidates should have some traction (or iron-bound offtake agreements from corporates), proven pipeline, and strong ESG story with a big TAM. It should be noted that most companies are staying private, longer.

Recent exits: Polestar went public at a $20b valuation via a SPAC; Energy Vault is also SPACing, valuing the company at $1.6b; Fluence Energy filed for an IPO

Acquisition: A good old M&A purchase from a strategic or financial buyer could provide the right platform for climate tech companies and teams to thrive.

Recent M&A: BP acquired Blueprint Power, a New York City-based startup transforming built environments into flexible power sources.

Special thanks to the named and unnamed army that supported this guide. Hat tip to Dimitry Gershenson, Mark Westfall, Caroline McGeough, Nell Gallogly, Brendan Hermalyn, et al.

This guide is meant to be directional and representative - not completely exhaustive, though we do aim to update and revise it over time as we continue to explore the evolving climate financial stack. If we’ve missed a leading organization or important category to founders trying to scale their climate innovation, we need to hear it! Please reach out to us at [email protected] with feedback or thoughts.

Poor performance this half as investment falls to 2020 levels, but some strong plays.

$82bn of new capital for climate tech in the past 6 months

A new interactive Climate Capital Stack Map

Investing

Investing