🌎 The investment case for water

Why dedicated water investors are building out a new asset class, with Burnt Island Ventures and Echo River Capital

Happy Monday!

Small nuclear startups are hitting milestones, but are they at critical mass? We’ve been tracking the big moves, and have a new leaderboard out now for the SMR space.

In deals, $11.4bn for AI data center across two deals, $230m for independent power production, and $200m for solid state transformers across two deals.

In other news, more tariff turbulence, the new US Farm Bill, and the new Octopus-California partnership.

Thanks for reading!

Not a subscriber yet?

📩 Submit deals and announcements for the newsletter at [email protected].

💼 Find or share roles on our job board here.

CTVC is powered by Sightline Climate, the tactical market intelligence platform for energy and investment decision-makers.

Small modular reactors (SMRs) were catapulted into the spotlight late last year by massive raises, the second coming of SPACs, and high-profile partnerships with hyperscalers. But it’s a David and Goliath story: SMRs are being deployed first by major nuclear incumbents, while startups dominate the headlines by linking their solutions to the data center power crunch.

Last week, two more developments continued the shakeup: SMR developer Nuscale reached final investment decision (FID) on its Romanian project, just the third OECD SMR project to reach FID and the largest capacity yet. Meanwhile, the NRC approved a partial construction permit for nuclear supply chain company Holtec for its project on the Palisades site in Michigan.

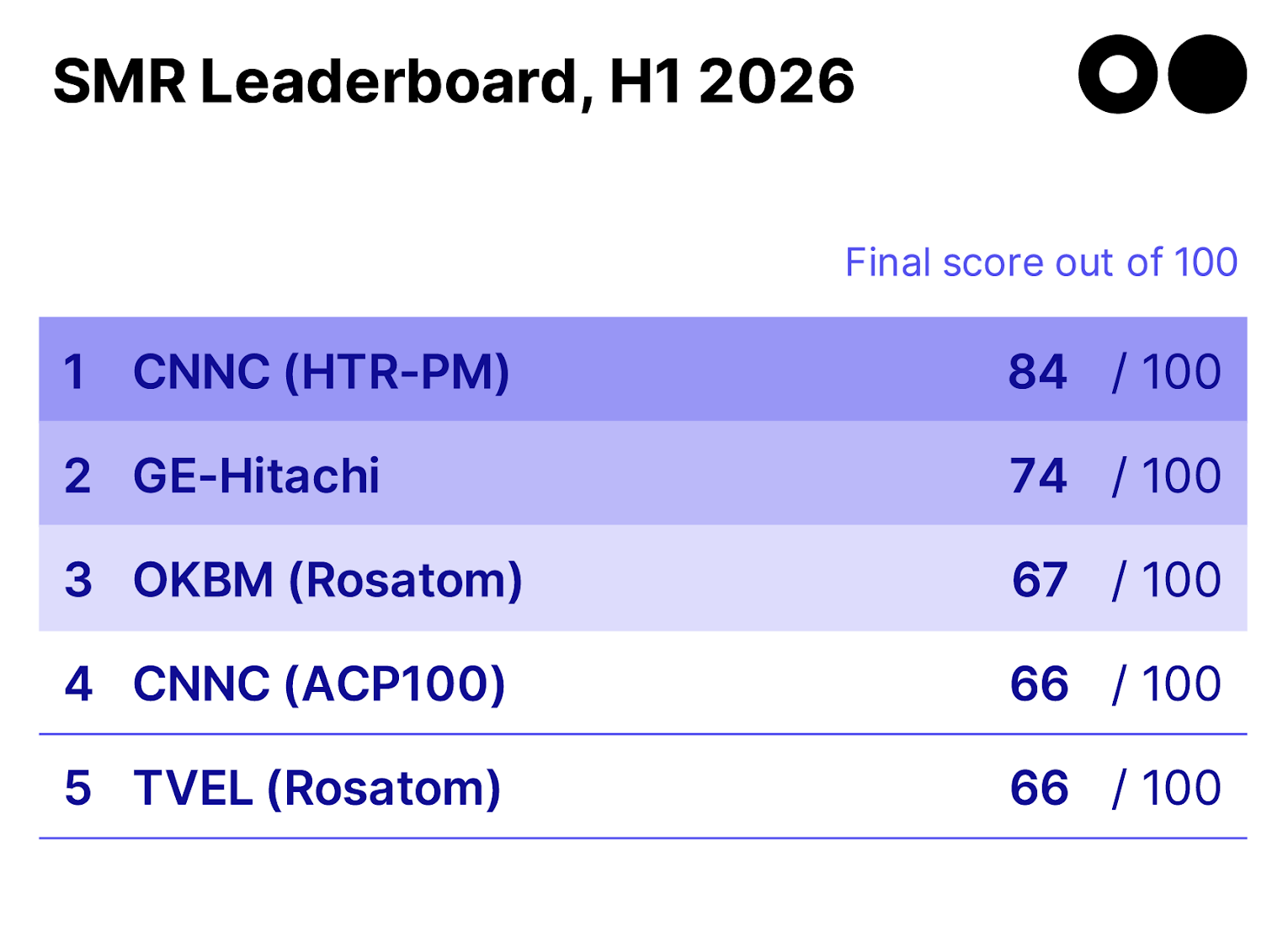

With so many milestones, tech nuance, and interest in nuclear for energy security, it’s difficult to cut through the noise and figure out who’s actually making progress. To give you a data-based, expert opinion, Sightline Climate created its SMR leaderboard, ranking the top 20 reactor vendors globally across four metrics: technology, deployment, finance, and supply chains.

Clients can see the full list on the platform here. CTVC is previewing the top 5 below, and you can read more on Sightline’s website here.

This leaderboard shows which reactor vendors are furthest along the path to bankability, and will be updated every six months to capture all the moves in the space. The ranking considers credible licensing progress, the status of their real-world projects, availability of durable financing, and an executable supply chain. (It excludes the speculative likely economics or operational performance of different reactors.)

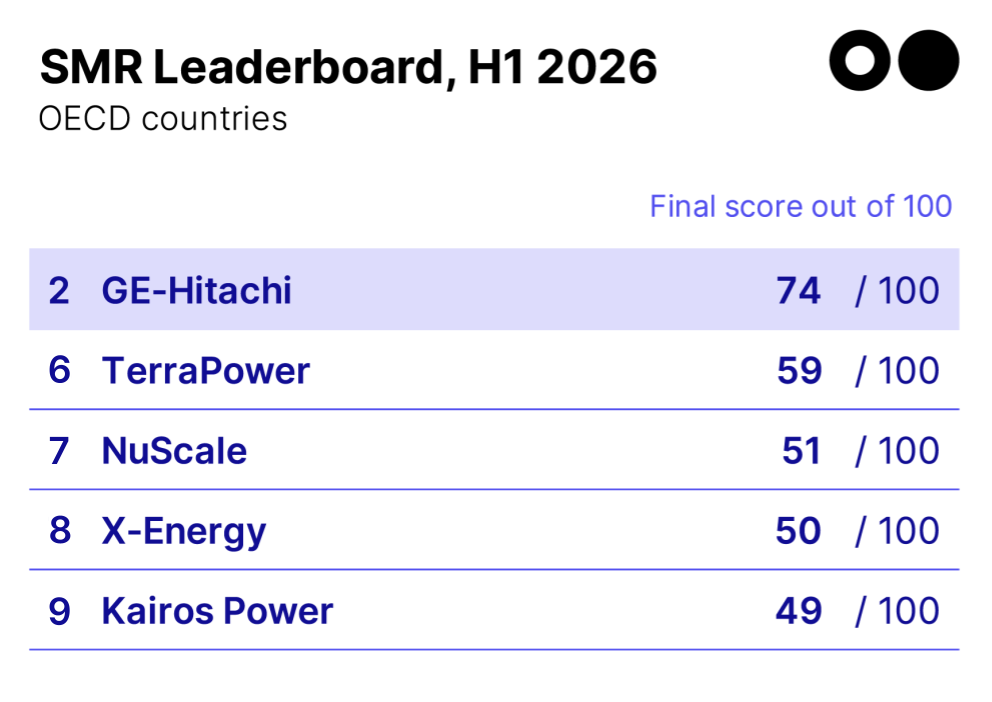

Despite last week’s milestones, OECD companies are still playing catch up. The early lead in small modular reactors belongs to Moscow and Beijing. Their state-owned nuclear bodies, CNNC and Rosatom, respectively, lead across almost every dimension Sightline tracks — technology maturity, available financing, and supply chain readiness.

China’s CNNC sits at #1, as the owner of the only SMR currently in commercial operation anywhere in the world: the HTR-PM reactor. Its ACP100 is also the only SMR expected to reach operation in 2026. No Western vendor is close on either metric.

But excluding China and Russia, US vendors like TerraPower, X-energy, Kairos Power, and Oklo are climbing as hyperscaler offtake agreements and DOE support strengthen their finance and deployment scores.

⚡ Heron Power, a Scotts Valley, CA-based solid-state transformer developer, raised $140m in Series B funding from Andreessen Horowitz, Breakthrough Energy Ventures, Capricorn Investment Group, Energy Impact Partners, Gigascale Capital, and other investors.

⚡ Utility Global, a Houston, TX-based blue hydrogen producer, raised $100m in Series D funding from APG Asset Management and Ara Partners.

⚡ DG Matrix, a Morrisville, NC-based solid-state transformer developer, raised $60m in Series A funding from Engine Ventures, ABB, Cerberus Capital Management, Chevron Technology Ventures, Clean Energy Ventures, and other investors.

💧 FYLD, a London, England-based AI-powered frontline infrastructure intelligence platform , raised $41m in Series B funding from Energy Impact Partners and Partech.

🛰 SatVu, a London, England-based high-resolution thermal data collector, raised $41m in Series A funding from NATO Innovation Fund (NIF), Adara Ventures, British Business Bank, Lockheed Martin, Molten Ventures, and other investors.

⚡ Statiq, a Gurgaon, India-based EV charging network platform, raised $18m in Series A funding from Tenacity, RCD Holdings, Shell Ventures, and Y Combinator.

🏠 Zero Homes, a Denver, CO-based digital-first home upgrade assessment software, raised $17m in Series A funding from Prelude Ventures, FJ Labs, Overture VC, SJF Ventures, VoLo Earth Ventures, and other investors.

🌾 Resurrect Bio, a London, England-based crop health technology developer, raised $8m in Series A funding from Corteva, AgFunder, Calculus Capital, Pymwymic, SynBioVen, and other investors.

🏭 Kilter, a Langhus, Norway-based autonomous weeding robot developer, raised $8m in Series A funding from Halden Pensjonskasse, Kubota Corporation, Nufarm, Pymwymic, and SBG invest.

🏠 nuuEnergy, a Munich, Germany-based heat pump installer, raised $5m in Seed funding from Amberra, Better Ventures, Bynd Venture Capital, EnjoyVenture, HTGF, and other investors.

🏠 Firmus Technologies, a Saint Leonards, Australia-based AI infrastructure developer specializing in immersion-cooled data centers, raised $10bn in PF Debt funding from Blackstone Group and Coatue.

🏠 Nscale, a London, England-based AI infrastructure platform, raised $1.4bn in Debt funding from Blue Owl, LuminArx Capital Management, and PIMCO.

⚡ European Energy, a Søborg, Denmark-based renewable energy project developer, raised $76m in PF Debt funding from Nordic Investment Bank (NIB) and Ringkjøbing Landbobank.

🏠 NewCold, a Breda, Netherlands-based automated cold chain logistics service provider, raised $37m in PF Debt funding from Banca Comercială Română and European Bank for Reconstruction and Development.

⚡ Bioo, a Porto Alegre, Brazil-based biomethane project developer, raised $29m in PF Debt funding from Brazilian Development Bank (BNDES).

🐄 Eco-Pork, a Tokyo, Japan-based sustainable pig farming technology developer, raised an undisclosed amount in Debt funding from Tokyo Star Bank.

⚡ SkyNRG, an Amsterdam, Netherlands-based sustainable aviation fuel producer, raised an undisclosed amount in PF Debt and Equity funding from ABN AMRO, BNP Paribas, Crédit Agricole Alpes Développement, Deutsche Bank, Groninger Groeifonds, and other investors.

☀️ SOLV Energy, a San Diego, CA-based renewable energy solutions provider, announced $589m in IPO funding.

⚡ Global Uranium and Enrichment Limited, a Perth, Australia-based uranium assets and enrichment technology developer, was acquired by Snow Lake Energy for $30m.

⚡ Jaguar Uranium Corp, a Thornhill, Canada-based uranium exploration assets developer, announced $25m in IPO funding.

🏠 Sobre Energie, a Boulogne-Billancourt, France-based energy management platform for buildings, was acquired by Deepki for an undisclosed amount.

☀️ Aerial PV Inspection, an Aachen, Germany-based drone-based solar inspection service provider, was acquired by Intertek for an undisclosed amount.

⚡ Smarter Power Solutions, a Melbourne, Australia-based engineering advisory for the power sector, was acquired by DNV for an undisclosed amount.

🚢 Wasaline, a Vaasa, Finland-based passenger and cargo ferry manufacturer, was acquired by Stena Line for an undisclosed amount.

🌾 Amos Power, a Cedar Falls, IA-based autonomous electric tractor manufacturer, was acquired by FarmX for an undisclosed amount.

⚡ VoltStorage, a Munich, Germany-based long-duration energy storage developer, completed an asset sale to ESS Tech for an undisclosed amount.

🧱 FORTA, a Grove City, PA-based synthetic fiber concrete reinforcement manufacturer, was acquired by The Heritage Group for an undisclosed amount.

⚡ Solstice, a Cambridge, MA-based community solar development platform, was acquired by Perch Energy for an undisclosed amount.

♻️ E-Z Recycling, a Saint Paul, MN-based food and beverage depackaging and recycling service provider, was acquired by Vanguard Renewables for an undisclosed amount.

🛰️ Insight M, a Sunnyvale, CA-based aerial methane detection and analytics platform, was acquired by Zeitview for an undisclosed amount.

🌱 ESG-X, a Düsseldorf, Germany-based ESG reporting platform, was acquired by Dcycle for an undisclosed amount.

⚡ Green4T, a São Paulo, Brazil-based data center infrastructure developer, was acquired by Legrand for an undisclosed amount.

⚡ Kratos Industries, an Arvada, CO-based low-voltage (LV) and medium-voltage (MV) power equipment manufacturer, was acquired by Legrand for an undisclosed amount.

This is a sample of deals available for Sightline clients. Can’t get enough deals?

A new Supreme Court ruling struck down Trump’s tariffs, but he’s already announced more, higher ones through a different authority. Open questions persist for developers importing various clean energy equipment and parts, especially as unrelated solar tariffs and FEOC rules continue.

The House Committee on Agriculture released its draft of the 2026 Farm Bill, an 800-page draft of the first farm bill in seven years, now waiting for Congress’ notes. It includes some expanded voluntary conservation and credit programs, but also faces criticism for not addressing SNAP and other concerns.

UK energy company Octopus plans to invest $1bn as part of a California-UK climate MOU. It includes backing two carbon removal developers with Big Tech offtakers, industrial heat batteries that replace fossil-fuel boilers with flexible electric thermal storage, and acquiring a solar-plus-storage project alongside a new California-UK climate MOU.

The EU said it is narrowing its Corporate Sustainability Reporting Directive, now only applying to companies with more than 1,000 employees and over €450m in annual revenue, as it continues to weaken environmental regulations amid corporate and Trump admin pressure.

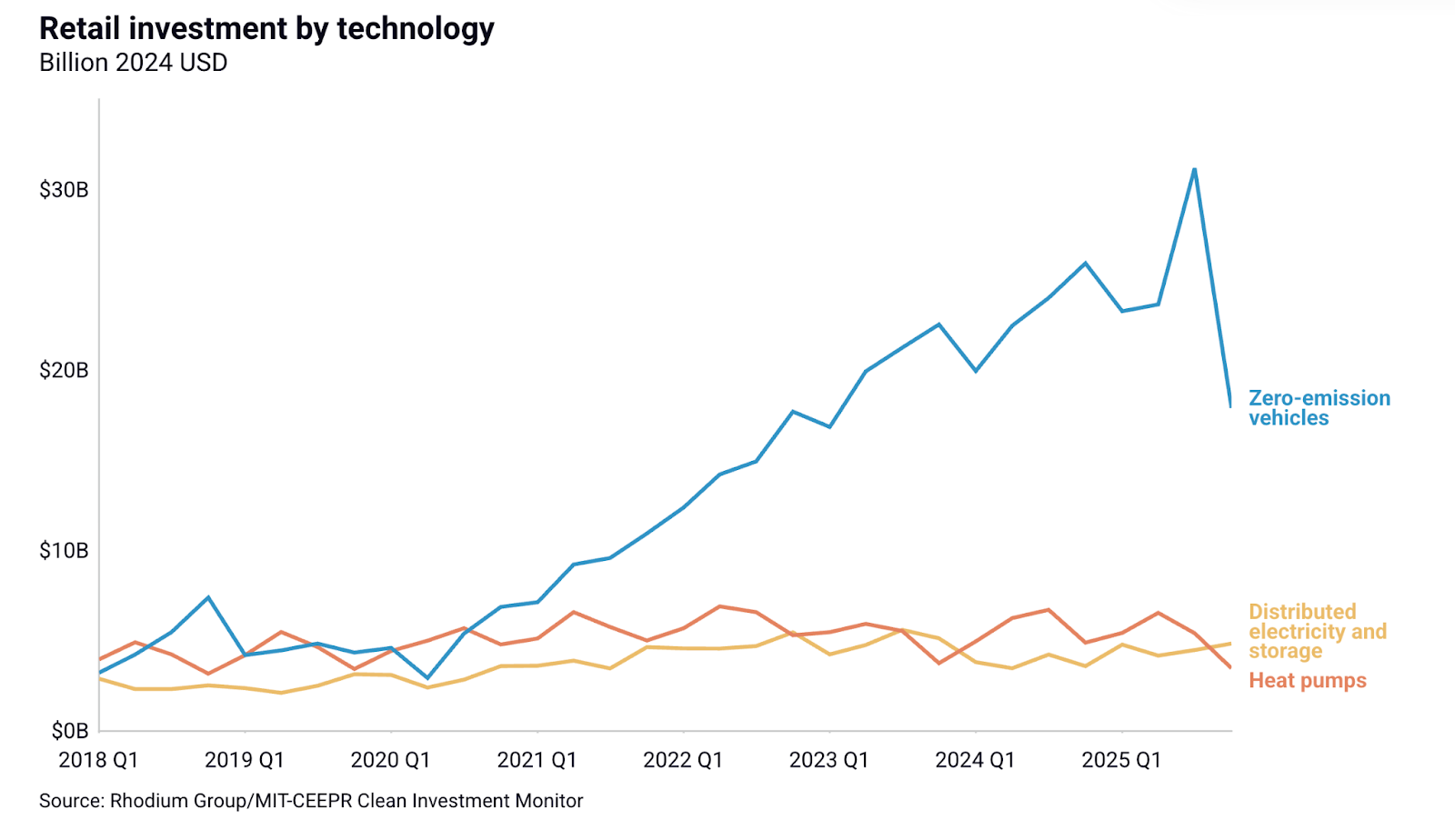

In 2025, US clean energy investment hit a record $278bn, although EV sales dropped drastically after the EV sales credits expired at the end of September. Despite being the highest annual total on record, Q4 investment fell year over year.

The White House published its "Maritime Action Plan", largely aimed at restoring shipbuilding in the US. It includes a proposed tax on all foreign-made ships entering US ports, which is almost all of them as China, Korea, and Japan make up 94% of the global market.

Apple just took the “green bonus” out of its own green strategy.

Britain looks skyward for net-zero electrons with space-based solar report.

Duke drops a new roadmap for making the grid bend without breaking.

Your new favorite interactive grid and energy model is live.

Breakthrough Energy Catalyst puts the brakes on new investment.

Endangerment finding in the crosshairs of new legal challenge, already.

Mamdani’s New York’s new climate czar.

📅 Climate Innovation Showcase Day: On February 26th, from 2-6pm, celebrate Carbon13’s cohort of venture builders in Google's Berlin headquarters to pitches, connect with the founders, and network with climate leaders, VCs, and angel investors.

📅 Q1 2026 Data Center Outlook: Register and join us at 10am EST February 27 for a webinar on all things data centers; the delays in the pipeline and how data centers are getting creative in finding energy capacity.

💡 VC-Founder Matchup – Energy: Join SOSV from March 2-6 for VC-Founder Energy Matchups. Join virtual 1:1 meetings that bring together 250+ startups and 250+ investors for all things energy: critical minerals, generation, energy storage, grid efficiency, and more.

📅 Women Entrepreneurs Boot Camp | Climate Tech 2026: A one-day climate tech accelerator program for women founders, taking place April 16, 2026 in New York.

XIG Imprint Business Development Lead - Vice President @Goldman Sachs

Junior Account Executive, @3V Infrastructure

Associate, @Foundry-Logic, Inc.

Summer Research Intern, Senior Associate – Clean Fuels, Principal Analyst – Data Centers and Power Markets, Data Analyst – Late-Stage Finance, @Sightline Climate

Associate, @Prelude Ventures

US Program Director, UK Programme Manager, Operations Manager, @Constructive

📩 Feel free to send us deals, announcements, or anything else at [email protected]. Have a great week ahead!

Why dedicated water investors are building out a new asset class, with Burnt Island Ventures and Echo River Capital

Storage, satellites, and the SaaSpocalypse

Newsletter

Newsletter