🌏 Who are the Climate Tech Investors?

A new interactive Climate Capital Stack Map

This week we chatted with Tyson Woeste of Fifth Wall about the VC firm’s approach to climate investing in the built world.

This week we chatted with Tyson Woeste of Fifth Wall about the VC firm’s approach to climate investing in the built world. Infrastructure and buildings are an enormous – and often under-cited – driver of emissions, and few traditional climate investors bridge the divide. Fifth Wall is a global venture capital firm focused specifically on the real estate industry and property technology for the Built World. Over the past few months, Fifth Wall has published their perspective on the intersection of climate and the built environment via a series of Medium posts. Their climate investments to date include Aurora Solar, Blueprint Power, Homebound, Enertiv, among others.

What is Fifth Wall and your approach to venture investing?

Fifth Wall specializes in startups and technology for the global real estate business. We think about real estate broadly – as the entire built world. This includes hotels, homes, apartments, shopping centers, data centers, warehouses, and any other kind of building.

We have over 60 LPs from 14 countries. Real estate corporates – the most significant owners and operators of real estate around the world – make up approximately half our LP base. With this global and corporate footprint, we probably have an LP associated with any sort of building anywhere in the world.

Fifth Wall was started because of the size, reach, and outdatedness of the real estate industry. Real estate is one of the largest business sectors by asset class on the planet. It’s also one of the largest operating sectors of GDP. Interestingly, before Fifth Wall was founded four years ago in 2016, real estate had not been transformed by technology – like just about every other sector of the economy had. Software is eating the world but hadn’t eaten the built world yet. The idea behind starting Fifth Wall was to build the very best venture capital manager at addressing that gap, and, of course, building a strong LP network. If you have the industry on your side and aligned on the cap table of the investments you make, it creates strong incentive on both sides – for the technology creator and user.

Today, we think of ourselves as a technology and innovation accelerant for the real estate business. The reason our LPs work with us is because they want help seeing what the next disruptor in real estate will be. Functioning at the center of tech and innovation for the global real estate business, we help our LPs see into the future.

What are some of the challenges of investing in the built world and how does Fifth Wall address them?

It goes back to the beginning of the conversation – the founding vision of Fifth Wall. We were built around the observation that real estate was a laggard in technology adoption.

On the flip side of that is that entrepreneurs starting technology, businesses generally had a difficult time accessing real estate. If you have a product or service, it’s really tough to sell into the real estate business. There are a few reasons for that: the sales cycles are long; it’s not clear who your internal buyer is; or your buyer is technology and risk averse. Our secret sauce is that once you bring the industry in, you get to know them well and they trust you. Then, you can start to create value.

How does climate change and decarbonization fit into your firm’s strategy in real estate?

It started in earnest two years ago. But, honestly, it got really loud about 12 months ago. Climate and sustainability are not brand new things to the real estate industry, it has been part of the focus on ESG that became prominent four or five years ago.

Historically sustainability has been lumped into “ESG” along with a bunch of other important but traditionally non-fiduciary responsibilities. Credit is due mostly to the northern European pensions who worked hard for a decade through GRESB to create some pressure on the real estate business to take ESG seriously. What has really shifted in the last 12-24 months is the increased focus on the “E”, on sustainability and the climate crisis. We first started to notice this shift about 12 to 18 months ago, when we began to see an increasing volume of inbound questions from our LPs and other groups who were increasingly focused on climate tech. They were looking at AI systems to manage their HVAC systems better or new IoT sensors that could help with submetering, or on-site solar, to name just a few. Three forces were driving LPs to ask these questions: regulatory pressures – ie. carbon taxes, investor pressures, and tenant demands. I’ll get into these later. But, the decarbonization efforts in real estate which started as a “trickle” a year or two ago are now full steam.

What’s your framework for thinking about climate?

Buildings are the biggest end user of energy and therefore the biggest polluters in the economy. 40% of all GHGs emitted can be attributed to buildings. People tend to focus on transportation, manufacturing, and food production as the primary sources of emissions. But, targeting real estate is one of the biggest opportunities for decarbonizing – for both the emissions it produces and its market size.

When we think about climate tech, we think about carbon as our North Star. We ask ourselves, “Does this technology we’re looking at have the potential to meaningfully decarbonize the built world?”

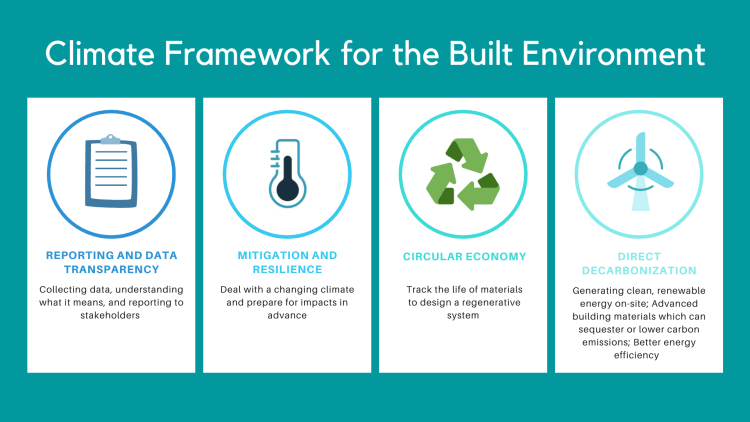

We think about the investment landscape for the built environment and climate tech in four categories:

📈 Reporting and data transparency is the first. To manage anything, you need to measure and report it. There is a whole category of startups focused on collecting data, understanding what it means, and then reporting those takeaways to stakeholders. When an owner or operator of an asset or a portfolio of assets wants to decarbonize, this is usually the first step.

🚧 Mitigation and resilience is the second category. Technologies in this space help our LPs deal with a changing climate and prepare for impacts in advance. If you’re a real estate owner in Florida dealing with flooding or in Los Angeles dealing with wildfires, you have big decisions to make today related to climate risk. As one example, software products (e.g., insurtech) have popped up to help these folks decide whether to buy or sell certain properties based on their climate risk exposure by modelling these threats.

♻️ Circular economy is the next category. This tends to be more of a European concept than an American concept. Here, we include technologies that track the life of materials. Doing so helps you measure the carbon impact of creating and operating a building through the materials that were used to make it. Water, for example, might not seem like a decarbonization problem but it is. In California, some estimates put 20% of the power in the state being used to pump water around, treat it, heat it up, and dispose of it. So, how a building uses water is a decarbonization problem. IoT sensors and ML have come in to help monitor and address this issue.

💨 Direct decarbonization is the last category, which has a few subcategories.

⚡️One is on-site power. As one example, we have an LP who is a large logistics and warehouse provider with a ton of rooftop space. One of their customers is Amazon, who wants to charge its electric trucks at this LP’s facilities when they are loading. All of a sudden our LP has become a utility company. This presents many many opportunities for various technologies to manage and deliver this service, from roof to outlet. Office building owners face a similar challenge/opportunity with workers increasingly driving their Teslas to work and wanting to plug in.

🏗Another subcategory is advanced building materials and carbon sequestering building materials – or at least lower carbon building materials. Most folks talk about how concrete or cement account for ~10% of the carbon load for buildings, but there are a lot of other pieces that go into that. There are some interesting opportunities in retrofitting as well. For example, Local Law 97 in New York – which requires most buildings 25,000 square feet or larger reduce their carbon emissions by 40% by 2030 and by 80% by 2050 – has implications on retrofitting; for example buildings built between the nineties and early aughts, as their envelope thermal performance just can’t perform to current code.

🚴Lastly, there’s efficiency. This includes better ways to run HVAC systems informed by better sensors and ML algorithms. One unexpected example I like to talk about in this space because it illustrates the breadth of opportunities here are electric motors. It may come as a surprise to learn that there is a small army of electric motors in some buildings and up to 20-30% of the electricity consumed in some buildings can be from these electric motors in garage ventilation fans, air conditioning fans, refrigeration condensers, etc.. There’s a new generation of electric motors coming up now that is 30-60% more efficient than current ones. The analogy to think about here is LED light bulbs. Ten years ago, we swapped out incandescents for LEDs, and we’re still in that process. Electric motors is a category that we think is going to go that way as well.

What are some examples of companies you’ve invested in over the course of Fifth Wall’s history that fit into this climate framework?

How do you assess the climate impact of investments? Specific metrics?

We have an in-house carbon impact underwriting approach that we use when looking at a company to forecast and underwrite the carbon impact potential of any particular company we’re looking at. This is also important to our real estate corporate LPs, but also to our non-real estate LPs that include more traditional venture investors like endowments, pensions, and sovereign wealth funds. There’s some interest on their side and actually tracking carbon impact as well.

What’s your underwriting criteria?

Our unique insight – our venture super power – is understanding the real estate business better than anyone else. We can predict things because we eat, sleep, and breathe the real estate business. If there’s something we want to know or don’t understand, we can pick up the phone and talk to folks all over the business across the world. When we’re doing diligence on a company, we uniquely understand how fast itstech or innovation can scale and be deployed.

As it pertains specifically to climate tech specifically, what this means is that we believe we have some unique insight into where the global real estate business plans to spend money, how much, and when they are going to do it. We also believe we have some ability to influence which climate tech solutions get adopted. Taken together, this is why we are very bullish on climate tech for the built world and our ability to invest well here.

How would you frame the climate tech investor landscape and Fifth Wall’s role within it?

The field is growing incredibly quickly. I would group investors into four categories:

One way to understand what we do is to view us as an outsourced, pooled corporate venture for the real estate business. Energy Impact Partners is in some ways similar with a focus on the utilities businessAnd you also see a lot of individual participation by corporates in that space. That’s one thing I would say is notably different here from other areas of venture – a higher level of corporate participation.

You’ve mentioned there’s been a tipping point in your industry. Why do you think the conversation around climate change has changed?

If you look at sustainability and the climate crisis broadly – across the economy – everybody knows there’s a problem. Everybody roughly has the idea that technology is part of the solution. But, for more than a decade, we’ve been discussing and trying to figure out how to create short-term economic incentives to get people to act differently and change their behavior. That’s always kind of been the problem with the climate crisis. You can see it coming and know its causes, but it’s hard to put economic incentives in place for people to change the way they do business.

What we think is unique about the real estate business is that it has an economic problem around their GHG footprint that a lot of other sectors don’t. I would not want to be a climate tech investor anywhere but real estate. I think it’s going to be really hard in other sectors. There are echoes of the cleantech 1.0 or greentech 1.0 bust 10-15 years ago. I’m not just talking about $200 million solar farms and hydrogen infrastructure projects only. I’m talking about how back then there was no demand. People were not willing and had no economic incentive to adopt a lot of these things. I think that’s still true with climate tech in many sectors of the economy today – despite all the rhetoric. Real estate, though, is different.

The reason for that statement is we basically think there are three things driving actual economic incentives in real estate:

⚖Number one is regulation – like Local Law 97 in New York. It’s really exciting to hear some of the things coming out of the Biden administration, but, if you go back a few months ago, the United States at the federal level was not aligned with the Paris Agreement. However when you look at a map of the US, there are these blue dots. Those blue dots tend to be cities, and cities are where the majority of the buildings are. So when mayors and city councils get elected in these cities, they are generally left learning and want to demonstrate strong climate action.

Real estate tends to be a natural target for these regulators. Buildings like the Empire State Building can’t threaten to leave New York City, so, if you’re going to put a carbon tax on anything, you put a carbon tax on buildings. To my knowledge, real estate is one of the only industries with short-term carbon taxes directed at them. Therefore, the real estate business is starting to take those economics into account.

👬Another force is the tenants of buildings. The people who’ve shown leadership here are corporates like Facebook, Google, Amazon, and Walmart. Fortune 500 companies taking decarbonization pledges, like Amazon, means they’re going to lean on all of their suppliers to decarbonize and provide low carbon versions of their current goods and services. One of the biggest suppliers to Amazon globally is real estate – for logistics, warehouses, distribution centers, data centers, office buildings, and even hotels for business travel. If you’re a landlord for an office building in New York City and Amazon is your primary tenant, you’re going to get taxed for your carbon emissions by city officials and pushed by Amazon to decarbonize more quickly. These are fast-approaching targets – for next year or even next quarter.

💸The third force that we see is not unique to the real estate business; it’s capital markets. You’re starting to see big institutional global investors like BlackRock, pension funds, endowments, and sovereign wealth funds show explicit preferences to deploy capital into lower- and no-carbon assets. With real estate being the world’s largest asset class, it feels that pressure the strongest. We talk to our real estate CEOs who come off earnings calls and say that analysts are talking all about sustainability.

These three forces come together in a way that is unique to the real estate business. This is not a five year problem. People are going to pay the price in the very short term – creating an economic incentive for climate tech and real estate.

Does the US lag behind other countries?

Definitely – mostly on the regulatory side but it’s more nuanced than stronger or weaker. The EU has been much more focused and much more unified on their views around sustainability and decarbonization. They even have a new EU-wide framework for thinking about it. It’s been socially, politically, and culturally more important in the EU – for at least a decade.

What makes the US interesting to us though is its big, climate-aligned cities. Efforts to decarbonize these cities are only going to get stronger. States and their cities are generally independent and then there’s the federal government. When you want to understand the American regulatory framework, you have to think through how things are going to impact all those levels.

While the EU and countries like Singapore have been focused on climate for quite a long time, the US will become more interesting as the political, cultural, and financial landscapes shift. This is happening extraordinarily quickly. Joe Biden’s “Build Back Better” economic recovery plan prioritizes infrastructure and clean energy as one of its four focus areas. The incoming administration’s transition website is made up of a few thousand words, and 20% of them are dedicated to this issue.

Within the Biden administration, are there any regulations you’re excited about?

We are not legislative experts. We’re looking at everything that’s happening. But, in some ways real estate is a local problem impacted by local decisions and regulation.

Federal regulations like robust carbon trading markets are exciting and interesting and will only increase the pressure on real estate to decarbonize (and thus create the Climate Tech opportunity). However, the things that matter to the real estate industry and our LPs are typically influenced by local regulations – where the devil is in the details.

Interested in more content like this? Subscribe to our weekly newsletter on Climate Tech below!

A new interactive Climate Capital Stack Map

Financing around first- or early-of-a-kind project risk

‘Government-enabled, private sector-led’ in action in Washington, DC