Rhodium: Taking stock of Paris targets

Late breaking ‘Inflation Reduction Act’ changes odds for the better w/ Rhodium’s Ben King

This week, we chatted with Azeem Azhar, an entrepreneur, investor, and creator bridging the gap between technology and humanities to provide a holistic thinking about our near future.

Azeem Azhar, Founder of Exponential View & Venture Partner at Kindred Capital VC

This week, we chatted with Azeem Azhar, an entrepreneur, investor, and creator bridging the gap between technology and humanities to provide a holistic thinking about our near future. Exponential View is a highly-regarded newsletter on the future, and Kindred Capital VC is a venture capital firm focused on pre-seed and seed founders.

During Climate Week, Azeem, Celine Herweijer, and a team at PwC published The State of Climate Tech 2020. In addition to breaking ground as the first market report on “climate tech,” the research included a number of interesting findings:

We asked Azeem to share more about his background and the report.

Why did you predict climate tech as the “dominant narrative” of the next decade?

Over the last five years, I’ve been writing Exponential View and focusing on artificial intelligence and other technologies. But, I’ve always included news from the climate sphere.

Fifteen years ago I invested in New Energy Finance – now Bloomberg New Energy Finance – and started to develop an understanding of the climate tech space. Since, I’ve seen more founders and investors talking about climate change related issues and I’ve started to connect the dots between climate change urgency and the news that I write about in Exponential View.

One of the amazing things about venture capital is that it’s an incredibly fast follower, in the sense that it can “vector” very rapidly into a new domain. Much like how at one point no VCs were investing in social networking platforms, and then suddenly everyone’s investing in them – VC has started to “vector” toward climate tech and has accelerated quickly.

So, I had a discussion with some colleagues and friends at PwC about this VC trend. Celine Herweijer, who leads their global sustainability practice, saw the possibility of the report having a big impact. She committed a great team to do the heavy lifting. They were pretty open minded, and we started to write “The State of Climate Tech 2020” report.

How does the story of climate tech investment’s growth parallel the AI investment boom?

For a long time, AI companies couldn’t get funded. It took a couple breakthroughs, like computer vision and speech recognition, to trigger massive interest. Within a year of that development, large companies and venture capital started to invest, which then grew to billions. The growth in AI investment took about six or seven years. We are now seeing this parallel in the climate tech space. Great entrepreneurs with venture capital backing are a leading indicator about the boom coming in this space.

What are your thoughts on applying the traditional VC model to climate tech challenges?

In the climate change battle we need as much help as we can get. Venture capital excels at identifying a technology that is just at the biting point, and, if the economics work, offers a radically better solution. VC also helps founders scale companies quickly.

But there are problems with the model. In venture firms’ timeframes, companies have just five or six years to get to an exit – which works for mobile apps or SaaS companies but of course climate tech has different constraints. Companies can’t hack together a prototype quickly, run some tests, and get out in front of 500 people. For some climate tech founders, their initial prototype involves literally moving many tons of physical material.

There are shortcomings in taking the software model of VC and blindly applying it to climate tech. However, for the great entrepreneurs in this space, there is no barrier that is too high for them.

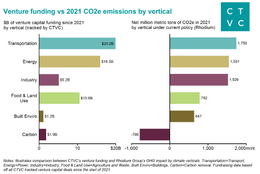

Your report found that ~63% of climate tech funding is in the mobility / transport space. How much of the surge in climate tech investing reflects EV hype?

Let’s peel that apart. 60% of EV investments are in Chinese venture capital investments. American and European investments are largely made by publicly listed companies, so Volkswagen’s investments in batteries for example won’t show up in this data.

Moreover, China’s investment in climate tech is virtually all in the mobility space – whether it’s electric vehicles or micro-mobility. So far, there hasn’t been much investment in alternative climate technologies that we’re seeing across Europe and the US, like carbon capture and storage.

I think there’s something that is really meaningful about the electrification of the car. Fossil fuels have been significant for humans over the last hundred years. One could characterize the sound of the 20th century as the hum of a petrol or diesel engine. We ended up architecting our cities and suburbs on the basis of cars and we even went to war over what we put in our cars. There’s sort of a momentous aspect to driving an electric vehicle – it creates a belief that this climate future is not just possible, it’s actually here.

We’re seeing companies and funds tout climate pledges without an approach to carbon measurement. How will we quantifiably assess their performance?

I think that’s a great observation. There’s an opportunity for startups to come in and provide that missing data piece of quantifying carbon levels.

For example, if I use Salesforce, I know exactly what my sales position is on a given day, who I owe money to, and what my inventory looks like. We don’t have that yet for carbon. We need solutions that can provide data that’s more accurate and closer to real-time than a biannual audit so that investors and companies can view their performance against all of the SDGs and their carbon footprint.

There are a few early companies trying to solve that need. If we look out three or four years, funds should have a much better real-time view of what’s going on. Maybe this will come from Equilibrium World, which is one of the companies I recently invested in, or maybe it will come from a Stripe or Shopify plugin. Then, that data might get aggregated by an existing market data player (e.g., RobecoSAM or MSCI) and support portfolio manager ESG metrics.

As a private market manager, you can ensure that you’re on track for your carbon targets by simply asking management the right questions, so that you have confidence in what they’re going to deliver. I talked to Rebecca Henderson, who is Harvard Business School professor and the author of Reimagining Capitalism in a World On Fire. I asked her why fund managers or ETFs perform better (lower volatility and higher returns) when they have an ESG mandate. Rebecca thinks that once you place an ESG mandate, managers have to ask many more questions about how businesses are being run. That additional diligence, from competent managers, results in the company being run better.

Why do you think that there is a faster “graduation time” from Seed to Series A for climate tech startups (29% in 36 mo) vs the market (19% in 36 mo)?

That’s a hard nut to crack. I think that it’s worth looking at it the other way around – specifically inspecting the corollary of the software space, which dominates a lot of venture funding.

Software companies have clear funding stage milestones that they need to hit, and clear dilutive effects if they don’t hit those milestones. To go from Seed to Series A, there is a well-articulated set of things that you have to get right. You’re incentivized to wait on graduating in the software space because of the significant valuation increment from Seed to Series A.

A faster graduation time for climate tech is positive in that there’s generally investor interest in the market. However, we’re still left with the uncertainty about milestones and associated valuations. There is no exact playbook for timing or derisking between funding stages in climate tech like in SaaS.

Interested in more content like this? Subscribe to our weekly newsletter on Climate Tech below!

Late breaking ‘Inflation Reduction Act’ changes odds for the better w/ Rhodium’s Ben King

Out in front on carbon removal, Nan Ransohoff sets a new tier for climate leadership with Frontier

John Doerr and Ryan Panchadsaram's new book on OKRs to get to Net Zero

Experts

Experts

Investors

Investors