🌍 Getting current on kelp processing with Macro Oceans

The synthetic bio startup sees an upswell of seaweed applications beyond the food industry

A flood of innovation with guest column from Elle Brunsdale

What do western wildfires and the global semiconductor shortage have in common? Water...or rather the lack of it.

While Earth is the “Blue Planet,” paradoxically only 1% of its water is available for use. We’ve taken water for granted, despite it being a basic human need and critical component to our industrial, food, and energy supply chains. In the western US, reservoirs are at record low levels, caused by a dangerous combination of rising temperatures and declining runoff that might jeopardize the region’s water supply and even cause blackouts. Across the Pacific, Taiwan is experiencing its worst drought in 56 years, driving global semiconductor shortages in an industry where the largest chipmaking company relies on 80 swimming pools’ worth of water a day. Meanwhile, floods are inundating Central China and Germany, resulting in more than 200 deaths so far. Governments and companies around the world are facing severe water quantity (too little or too much), quality, and equity challenges.

Water and climate are intricately linked, with extreme weather events - droughts, floods, sea-level rise, intensifying storms - manifested through changes in the water cycle. Climate change is precipitating more variable, unpredictable, and catastrophic water outcomes. Droughts in the West aren’t merely episodic - they’re the new normal, necessitating a focus on climate resilience and adaptation. Through an emissions lens, water can be both a source of emissions as well as a pathway for mitigation.

💨⬆️ GHG source: The massive amount of energy we use to pump, convey, treat, distribute, and utilize water (heating and cooling) produces emissions, known as the “Water-Energy Nexus.” California’s water system accounts for ~10% of the state’s GHG emissions, with 20% of the state’s electricity used for pumping, treating, and heating water. Removing toxic organic pollutants from wastewater requires diesel fuel (trucking) and natural gas (incineration). More indirectly, water plays a major role in fracking, refining, and processing in the oil and gas industry. Globally, water accounts for over 1,100 TWh of energy a year - a number that will only rise with population growth and climate change.

💨⬇️ GHG mitigation: Conversely, water can be used to reduce GHG emissions through hydropower (though not always sustainably), concentrated solar power, geothermal, and bioenergy. Treating wastewater onsite for use by cooling towers and other industrial processes can also mitigate water usage emissions.

💨🤷 Water-carbon dichotomy: Low carbon doesn’t necessarily mean low water. Critical decarbonization technologies (like biofuels, CCS, and nuclear) are water-intensive and, if not properly managed, could potentially become limited by water availability or exacerbate existing water problems.

We’re still at the early stages of unraveling this “Blue Planet Paradox.” As we face the water supply and demand challenges that come with our departure from the holocene, water footprint reducing technologies will become increasingly valuable. This confluence of growing water value with business value presents a sea of opportunity for watertech innovators.

Water permeates every industry. Broadly stated, watertech is any technology solution that has water at the core of its value proposition. Anders Hallsby, Partner at water-focused Mazarine Ventures, summarizes, “We invest in technologies with applications in water and wastewater across a variety of markets like power, food, agriculture, and real estate. Water is central to each one of them, even though the end product isn’t water. Without water it wouldn’t be possible to do anything.”

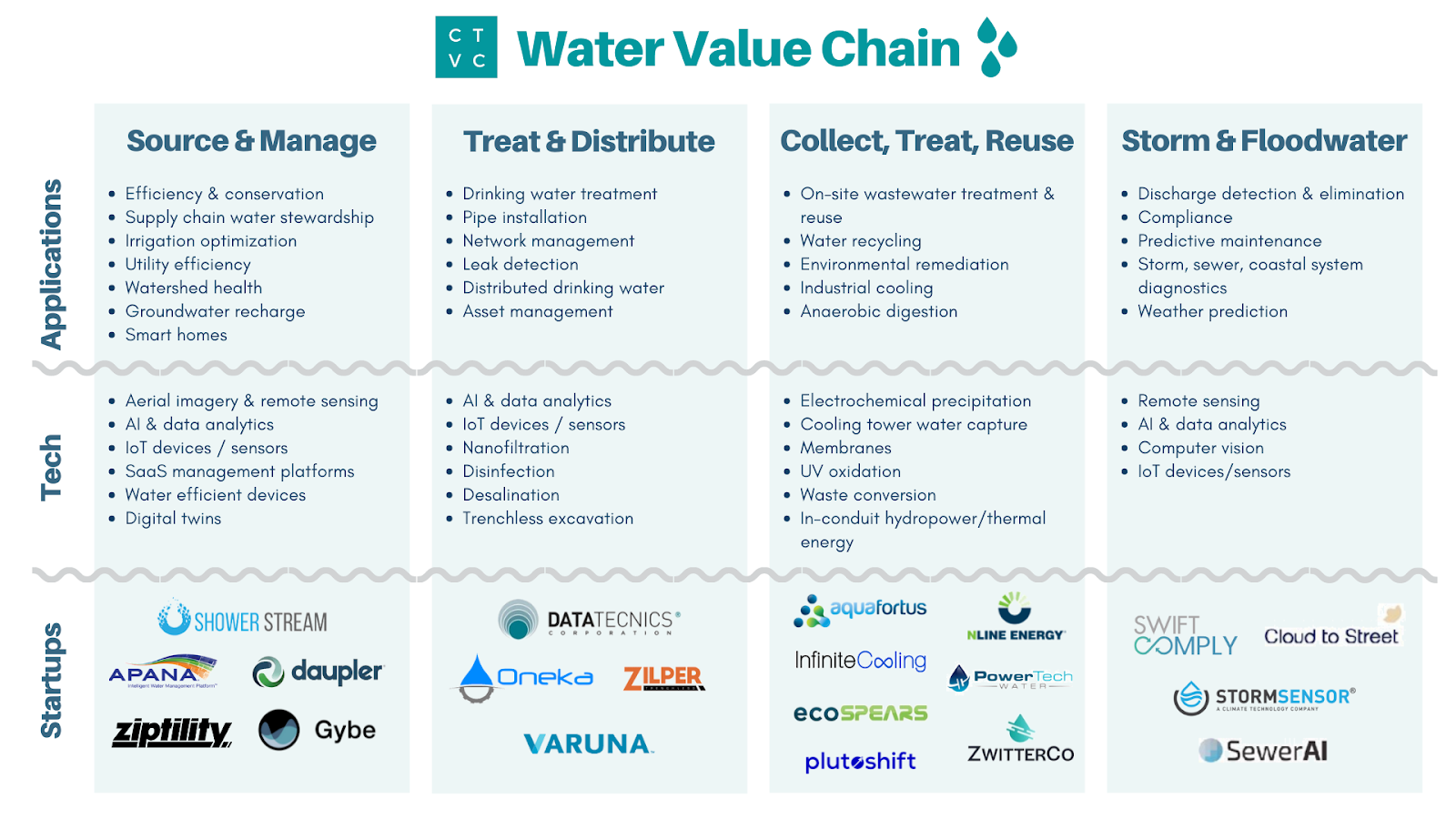

From the aquifer to your glass and back down the drain, we provide a sector agnostic framework for categorizing the value chain of water technology solutions with some example applications:

(1) Source & Manage - watershed health, groundwater recharge, efficiency and conservation, supply chain water stewardship, smart homes

(2) Treat & Distribute - water treatment, pipe installation, leak detection, distributed drinking water, asset management

(3) Collect, Treat, Reuse - processing and/or reusing wastewater, environmental remediation, industrial cooling

(4) Storm & Floodwater - storm and floodwater management, discharge detection and elimination, weather prediction

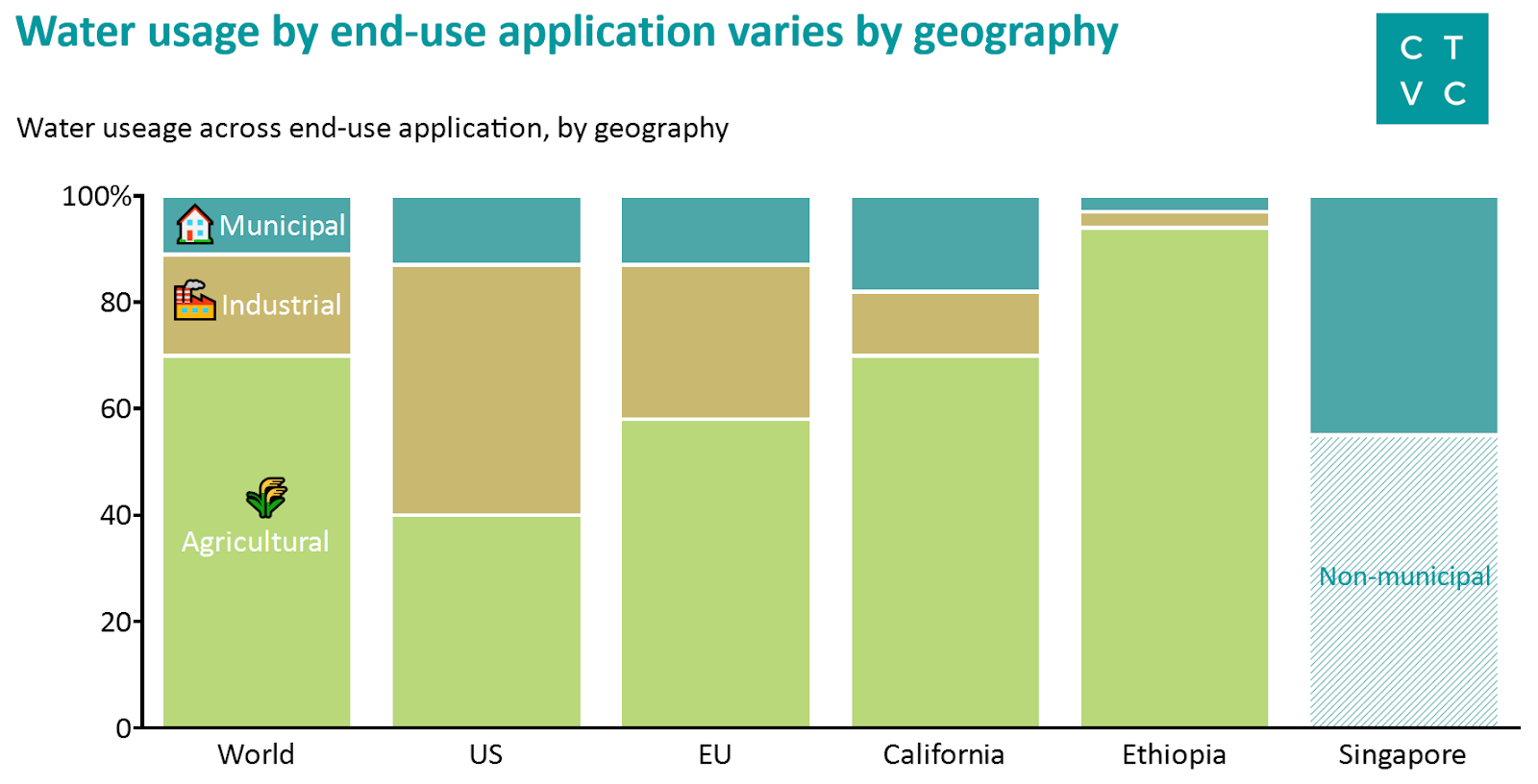

Watertech can also be categorized by its primary end-use: agricultural, industrial, and municipal. Across geographies, water use across these three categories varies widely - driven by natural resource availability, industrial makeup, and level of technology development.

🌾 Agricultural

Key customers: farmers, irrigation districts, agricultural, livestock, and aquaculture producers

Water underpins the entire food system. Globally, agricultural water use dwarfs all other applications, accounting for ~70% of water withdrawals for irrigation, livestock, and aquaculture. Agriculture is a major source of water pollution and is causing public health crises from nitrate fertilizer contamination of groundwater. Big data, sensors, and aerial imagery technologies help farmers make the most of every drop while maintaining water quality.

Representative startups:

Other startups: Sensoterra (wireless soil moisture sensors), Eco2Mix (sustainable water pH control), Swan Systems (irrigation optimization), Gybe (watershed health) Carbon Neutral Ag Sciences (crop science for irrigation efficiency), Ignitia (high accuracy tropical weather forecasting), Climate AI (supply chain weather risk), Veracet (water contamination prediction), Watergenics (aquaculture analytics)

🏭 Industrial

Key customers: heavy industrials, oil and gas, energy utilities, fashion, and other companies using water

Industry, including energy and power generation, accounts for 19% of global water use. A wide range of industries use water for fabricating, processing, washing, diluting, cooling, and transportation. Heavy industries like concrete, steel, and mining (see: the lithium triangle water-battery nexus) rely on water, as does the fashion industry, which is the second most water-intensive industry and a major polluter. Water is also used as a product - the bottled water industry is expected to reach $500b by 2028. A wide range of water treatment and recycling technologies are helping companies do more with less.

Representative startups:

Other startups: Allonia (oil sands water remediation), Aquafortus (zero liquid discharge wastewater treatment), PlutoShift AI (industrial water analytics), Aqua Membranes (3D printing for RO membranes), EcoSpears (eco-marine remediation), NLine Energy (in-conduit hydropower and thermal energy), Mimbly (laundry water recycling), Cambrian Innovation (decentralized wastewater)

🏠 Municipal

Key customers: water utilities, local governments, individual consumers

Pour a tall, cool glass of tap water? That municipal water makes up 12% of global water use and encompases everything residential indoor (showering) and outdoor (#zeroscape), as well as commercial indoor (water cooler) and outdoor (Water World). Utilities, both private and public, typically bookend the water customer experience and are responsible for sourcing, treating, distributing, and recycling water and wastewater. Utilities play a central role in managing and maintaining local water infrastructure from everything from algal blooms to PFCs/PFASs, where the stakes are increasingly high with severe consequences for failures.

Representative startups:

Other startups: Daupler (utility first response), SwiftComply (environmental compliance), Zilper (trenchless pipeline installation), DataTecnics (pipework monitoring), Flo (residential water monitoring), IoTank (septic tank monitoring), StormSensor (storm, sewer, and coastal system diagnostics), Shower Stream (water efficient hotel showerhead), Oneka Technologies (wave-powered desal)

🚣 Environmental/Recreational

Key customer: governments, NGOs, individual consumers, corporations

There is one other very important water end-use that is often not accounted for - nature! Rivers, streams, lakes, and wetlands are living ecosystems that require water for survival. They also provide invaluable ecosystem services like flood and disease control. The $650b outdoor industry also depends on water, and is often one of its largest advocates.

Representative startups:

The public sector typically funds massive water infrastructure projects, yet isn’t incentivized to take technology risk. The capital tap is running dry - by 2029, there will be a $434b water and wastewater investment gap.

The private sector has a huge role to play in driving innovation, particularly for solutions that are decentralized, localized, and distributed. While there have been relatively few watertech exits or big fundraises to date, the tides have started to turn (Infinite Cooling, Epic Cleantec, PowerTech Water). Players old and new (even a SPAC!) have wet their appetite for watertech investments. Here are a few of the water investors we’re tracking: Burnt Island Ventures (see Q&A below), Mazarine Ventures, XPV Water Partners, Sylmar Group, True North Venture Partners, Emerald Technology Ventures, PureTerra Ventures, Alpheus Water Tech Fund, Cycle Capital’s Bleu Impact, Colorado River Basin Fund.

Integrated thinking is a must. Water is a wicked problem that requires systems-level thinking, in addition to tech innovation. As Water Foundry CEO Will Sarni said on a recent webinar, “Digital transformation is not going anywhere unless there is leadership tied to a business strategy and the workforce is empowered to make it happen.” How can we ease customer implementation? How can we monetize waters’ 2nd, 3rd, & 4th use? Innovators in Israel have pioneered this approach, making the country a world leader in desalination, aquifer recharge, and water reuse (86% of wastewater is recycled!)

Get a PhD in water customers’ unique needs. Most US utilities serve <500,000 people and lack the resources, financing, and risk appetites to implement new tools at scale. Customers typically do not have a choice of water or sewerage service provider, which has atrophied utilities’ customer-first marketing and sales muscles. Selling to a fragmented market with limited appetite for innovation requires customer savvy on the part of watertech entrepreneurs. As Anders Hallsby put it, “We want our companies to have a PhD in the customer and truly understand their needs.” Maher Damak, CEO and Co-Founder of Infinite Cooling, which reduces water consumption and waste generation in cooling towers, strives to “work individually with our customers to identify and quantify the value proposition in their specific case in terms of water savings, treatment cost reduction, and plume abatement.”

Water is cheap, but that is changing. As some consider towing Arctic icebergs to California as a replacement freshwater source, we’re seeing signs that the cost of poor water management is tangible and rising. Enter the end of cheap water. Furthermore, while water is a product and input, it’s also a human right (implication: priceless). Water equity will be front and center.

The pipe is bursting on US water infrastructure. The American Society of Civil Engineers most recently scored stormwater infrastructure a D and drinking water a C-. While the INVEST in America Act promises $168 billion in funding and support, the private sector must plug the leak with basic hardware and software technology solutions that enable utilities to more efficiently and proactively manage and maintain assets (Daulper, Zilper, Ziptility).

Turnkey, comprehensive solutions may have an advantage. Given the complexity of water treatment systems, full-service solutions will often have an advantage. Axine Water Technologies is a great example. Its technology is packaged into modular, automated, turnkey treatment plants that are assembled off-site for “drop and play” installation at customer sites. It finances, designs, builds, owns, operates and maintains its systems for the customer. According to Jonathan Rhone, Axine President & CEO, the hyper-local nature of wastewater requires technology companies to “be capable of addressing a wide range of pollutant types, volumes and treatment requirements in order to achieve scale and impact.”

Plan for lead time. It’s not simple to instantly turn on the tap for watertech deployment. Scaling watertech businesses takes time due to well-entrenched incumbents and highly technical, risk averse customers that require evidence of performance. Entrepreneurs and investors should expect long sale cycles that require sustained, relentless effort by management teams and patient capital. But once the pipes are laid, these same high barriers to entry present unique opportunities for successful companies to scale.

What got you first interested in water? Walk us through how you launched Burnt Island Ventures, with the goal of “building the world’s best early stage water fund.”

My first connection to water was while I was working as a sustainability consultant for ERM. The Carbon Disclosure Project had started working on their first Water Disclosure Report and over the next 3.5 months, I became the de facto water sustainability guy. Then, after business school, I had the opportunity to help build out the Imagine H2O accelerator. So that was sort of the fork in the road for me.

At Imagine H2O in 2020, we worked with 36 entrepreneurs through our three programs. It was an amazing team of people, but no one was building the seed fund I wished existed. It was becoming obvious that it was a reasonable idea for three principal reasons 1) the caliber of entrepreneurs entering watertech 2) the accelerating speed to commercialization and 3) exit and market liquidity signaling. We had people proving out that water doesn't have to be slow and terrible, but can actually function a lot like building an enterprise software company. On the liquidity side, we’re seeing strong PE activity, from EQT selling Innovyze to Autodesk for $1bn, Mountain Capital taking Aegion private, Partners Group buying out Resilient Infrastructure Group, or XPV teaming up with KKR for a wastewater treatment platform. We also had three IPOs in June 2021 - way ahead of what I thought was possible. The liquidity avenues are there. A seed fund to shorten the timeline for the best early founders to raise money, and bring the network and expertise to help them build their solutions and companies made a lot of sense.

People put water in the “too hard” pile. Water is quite easy to get wrong and we didn’t really see an explosion of investor interest in water during the last cleantech cycle. This is a tremendously esoteric and difficult market, but absolutely enormous, vital, and doable. The history of non-water people investing in water has often been characterised by slightly silly bets and approaches. Mainstream investors sometimes ask people to change too much, or run into a brick wall of working with municipalities, and think things are going to go much faster than they are. So I'm quite grateful that people take their time before going into water, but one of the things that I hope we can do at BIV is be a catalyst.

Can you give us an example of a watertech company that you recently invested in to shore up our understanding?

We don't really have a sector focus but look for deep pain points in areas like industrial wastewater or process management for water utilities. We’ve invested in a company called StormSensor that tracks storm and flood risk in real-time. Our stormwater systems are so extensive and old that hundreds of millions of dollars go into upgrading it, but if you get it wrong you’ve got flooded basements, impassable roads, commercial damages, insurance payouts, and pissed off taxpayers. StormSensor becomes the source of truth to be able to actually track what’s going on in the system. On the hardtech side, we’re just about to expand our investment in ZwitterCo which has a fascinating membrane technology that can maintain 97% recovery when dealing with the worst wastewater like landfill leachate or dairy wastewater. They've just signed up some really fantastic companies to put their tech into the wild.

Big credit to sustainable infrastructure investor and watertech enthusiast Elle Brunsdale for her leadership with this feature. Follow more of Elle’s musings on sustainable development on Twitter and her journey in her new role at Greenbacker Capital. We’re raising a big, cool glass to Anders Hallsby, Will Sarni, and Tamar Honig who generously shared their expertise and helped raise our (water) level of understanding. And if your watertech career appetite has been wet, all 12 of Burnt Island Ventures’ portfolio companies are hiring!

The synthetic bio startup sees an upswell of seaweed applications beyond the food industry

The underappreciated role of carbon insets in decarbonizing Scope 3 supply chains

Food

Food

Carbon

Carbon