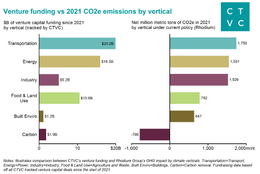

Rhodium: Taking stock of Paris targets

Late breaking ‘Inflation Reduction Act’ changes odds for the better w/ Rhodium’s Ben King

This past week we caught up with Jigar Shah, one of the most astute voices in sustainable finance, to explore whether hydrogen is really worth all its hype. A self-described “hydrogen bull”

Jigar Shah, Co-Founder of Generate Capital

This past week we caught up with Jigar Shah, one of the most astute voices in sustainable finance, to explore whether hydrogen is really worth all its hype. A self-described “hydrogen bull”, Jigar will be the first to point out the manifold ways that hydrogen is not a standalone decarbonization silver bullet.

Jigar is the Co-Founder of Generate Capital, a sustainable infrastructure investment firm, and is best known as the Founder of SunEdison, where he pioneered “no money down solar” and unlocked a multi-billion-dollar solar market. In 2009, Jigar joined Richard Branson to be the first CEO of the Carbon War Room, a global non-profit committed to supporting global entrepreneurs scale their climate solutions. Based on that experience, he authored Creating Climate Wealth: Unlocking the Impact Economy. Every week you can catch him on Greentech Media’s “Energy Gang” podcast.

Why is hydrogen seen as the “ultimate enabler of clean electricity?” What’s all the hype about?

I mean it certainly is hype. Let’s just be clear about it. Hydrogen is something that people have talked about and studied for a long time. It’s already a $130 billion business, so it’s not foreign or brand new. The question then becomes whether hydrogen is more likely to be adopted when compared to other long-term seasonal storage ideas we have for the grid.

I think that we certainly have more near-term applications for hydrogen than we have for industry-specific solutions like compressed air storage, physical gravity-based approaches, or other mechanisms that take and return power to the grid. With hydrogen, you actually have the ability to take power from the grid and to then use it in ways that are different than returning it back to the grid.

What does the market for hydrogen look like?

Plug Power uses about 27 tons a day, which is why we [at Generate Capital] know a lot about hydrogen. This specific application is focused on transport in the forklift space and is in use across the country at Walmart and Amazon distribution centers.

Today in the US, we have 150 tons of hydrogen that gets shipped via liquid mechanisms everyday. A lot of people say that’s tiny because that’s less than 0.1% of the total volume in the global market. All of that might be true but that’s exactly how you start off. You begin with these niche applications where people are willing to pay $5-20/kg of hydrogen (which varies because of transportation costs) compared to ~$1.50/kg for refinery or ammonia fertilizer applications. It is through these niche applications that you can profitably deploy next-gen electrolyzers and on-site hydrogen production technologies.

After you complete that entire set of niche projects, the cost curve for hydrogen will come down such that it can be produced at ~$1.50/kg and, 10 years from now, have use cases in ammonia production. That’s certainly not the case today, but that could be the case in the future.

Where in the hydrogen innovation versus deployment spectrum are we? How will cost curves of hydrogen production likely come down in the future?

We’re in the same exact place as the solar business when I entered in the early 2000s. When I started, the average solar panels were around 11.5% efficient. Today they’re probably 18.5% efficient. Back then, no one thought there were really any breakthroughs to get to 18.5% – there were just minor incremental improvements every year that marched up. Separately, the cost for panels when I entered the solar business was probably around $2-3/watt for modules. Today it’s $0.30/watt or less. That also came from the learning curve (e.g., larger manufacturing facilities and so on).

I think the same is true for hydrogen. The electrolyzer and other relevant technologies are fully mature. Now, with volume, they will continue to benefit from the learning curve. We’re not expecting any real critical breakthroughs to occur with hydrogen, but rather scaling from a handful of units to fully automated manufacturing will allow us to realize substantial cost reductions.

Is this a financing revolution or a hardware revolution?

If I’m working on it, it’s always the former. My brand is that I don’t invest in technology innovation. I start where the technology is mature, and it’s really now about deployment-led innovation. That’s the only place I work.

How do you approach investing in hydrogen at Generate Capital?

At the core of project finance, which is what we do at Generate, the technology can’t have any risk. You can’t take the risk that in year 5 the technology doesn’t work and that you need it to work for 10 years to pay it off. The next criteria to consider is the offtake arrangement. Who’s going to buy the product? We have that dialed in with Plug Power because we know that they’re buying 27 tons per day and using more with every new deployment of their fleet. Another consideration is where the feedstock is going to come from. In the case of an electrolyzer, it’s going to come from grid electricity — hopefully renewable energy. In the case of other processes like chlor-alkali, it might be natural gas. And then the last criteria is whether there’s a competent operator that can actually operate the plant. Lots of people can prove that they’re competent in managing fuel cells, electrolyzers, chlor-alkali plants etc.

We start with this framework. Then we try to position ourselves within the framework to make the most money and reduce the cost curves.

Who do you think is next to buy hydrogen at a larger scale?

There certainly will be pilot projects like the recent Shell Rotterdam and Ørsted announcements. The Europeans are likely going to lead the charge on the pilot side, although there are a couple of small-scale pilots that were awarded in California. But it doesn’t make any sense to scale up those solutions for large scale applications until hydrogen is within striking distance of $3/kg — because Europeans pay more for natural gas than Americans do. I also don’t see how you scale more-mature large-volume applications without some sort of feed in tariff or like-minded subsidy regime. The early markets will be the people who are currently buying 150 tons that’s liquid in nature (there is an equivalent market in Europe). There are many speciality buyers of hydrogen that pay through the nose because of shipping costs.

What do you think of hydrogen as a potential replacement for natural gas? What will a scaled hydrogen future look like?

There are a lot of people who want to turn hydrogen into natural gas. They want to combine hydrogen with a carbon molecule to make it into natural gas and put it into the pipeline. In the long term it’s unlikely that all of the natural gas pipelines are going to be converted into hydrogen ones. Transporting 10% or 20% hydrogen in natural gas pipelines safely is dependent on natural gas pressure. So if over the next 30 years, we’re effective at pursuing an electrify-everything strategy (and the work of Rewiring America comes true), then you’ll have less gas pressure. So, by definition, you’ll have less ability to accommodate hydrogen unless you spend billions of dollars upgrading all the pipelines to handle higher percentages of hydrogen.

In general, I see hydrogen production being far more localized, with the transport via electrons to the site. So if you’re a steel, cement, or some other industrial facility, instead of using natural gas, you would use hydrogen (like the new plant in Sweden that recently came online) which can be made when the electricity grid has room. When it doesn’t have room, you have enough storage onsite to take you through that 4-7 day period or you shut down the plant due to very high demands for electricity on the power grid or low hydrogen production.

Are there certain policy changes that would boost hydrogen deployment and adoption?

We’re only talking about 150 tons a day of hydrogen where people are paying prices above $5/kg. If we want to create subsidies, that’s the universe that needs to be subsidized. So it’s not a large amount of money when you think about how much we spent on solar, wind, or even electric vehicles. The question then becomes what does the deployment-led innovation curve look like? When you talk to some of these hydrogen players they say the learning curve is pretty fast. They see themselves reducing capex by 80% just by producing hundreds of units a month. If that’s the case, then my sense is that the amount of subsidy is not that large.

We have not followed the same rubric of solar and wind with all these other clean energy technologies. The Low Carbon Fuel Standards in California is one of the most difficult-to-understand markets in the world. It requires PhDs to figure out and has 460 pathways to earn credits. That’s exactly the wrong lesson people learned from solar and wind. What you want is a 20 year fixed price power purchase agreement (PPA), figure out how to operate the plant, and make sure that it’s an investment grade credit that’s signing the contract. So whether it’s anaerobic digesters, fuel cells, or even electric vehicles why we have this complex set of tax credits and incentives I’ll never know. Why would you subsidize the capital cost if the truck isn’t driven? They should instead implement the subsidy on a “per mile” basis which is directly proportional to emissions reductions. I don’t think this stuff is that difficult but people haven’t spent the time to understand how we got renewables to where it is over the last 15 years.

Where can our readers go to learn more about hydrogen?

Unfortunately there aren’t a lot of places to go for hydrogen. You’ve got a couple of hydrogen podcasts which people should go to. Separately, I try to write about hydrogen as much as I can on my Linkedin and Twitter, but frankly most of these data points are super proprietary.

I would say these some final points on hydrogen. Hydrogen for passenger vehicles is never going to happen so stop pining for it. We’re talking about hydrogen for industrial and specialty transport purposes. The second thing I would say is that people are always trying to figure out the cost per hydrogen unit, but that’s not how the world works. If there’s a 1200 MW wind farm that can’t be built because of the lack of transmission infrastructure, I can go to the wind farm and put an electrolyzer right there to make sure it is allowed to interconnect. Now a $1.2 billion asset gets unlocked. If all they have to do is subsidize a hydrogen facility to the tune of $100 million for the electrolyzer, they’ll write it off just to build their wind farm. So the notion of all these things having to pay for themselves within the box of hydrogen doesn’t make any sense. There are a lot of system-level benefits that unlock infrastructure, and that other infrastructure will pay you to unlock those projects.

Interested in more content like this? Subscribe to our weekly newsletter on Climate Tech below!

Late breaking ‘Inflation Reduction Act’ changes odds for the better w/ Rhodium’s Ben King

Out in front on carbon removal, Nan Ransohoff sets a new tier for climate leadership with Frontier

John Doerr and Ryan Panchadsaram's new book on OKRs to get to Net Zero

Experts

Experts

Investors

Investors