Happy Monday and 300th birthday to us! (not 300 years, 300 issues 🤓)

We’ve got an exciting one today, we're getting into the numbers underneath this IPO wave (and we're not talking about SpaceX).

In deals, $521m for synthetic aperture radar satellites in Finland; $66m for compressed biogas and renewable natural gas in India; and $59m for insect-based protein and animal nutrition in France.

In other news, the Strait of Hormuz to reopen, big nuclear news from the UK, Japan, and Uzbekistan, and a massive cement-CCS deal.

If you’re in London next week for LCAW, we’re hosting an event called Building & Financing AI in the UK. Come hear the state of the market from Kim, and hear from Ofgem, Octopus, GE Vernova, and Deep Green. Space is limited, but register here.

Thanks for reading!

Not a subscriber yet?

📩 Submit deals and announcements for the newsletter at [email protected].

💼 Find or share roles on our job board here.

CTVC is powered by Sightline Climate, the tactical market intelligence platform for energy and investment decision-makers.

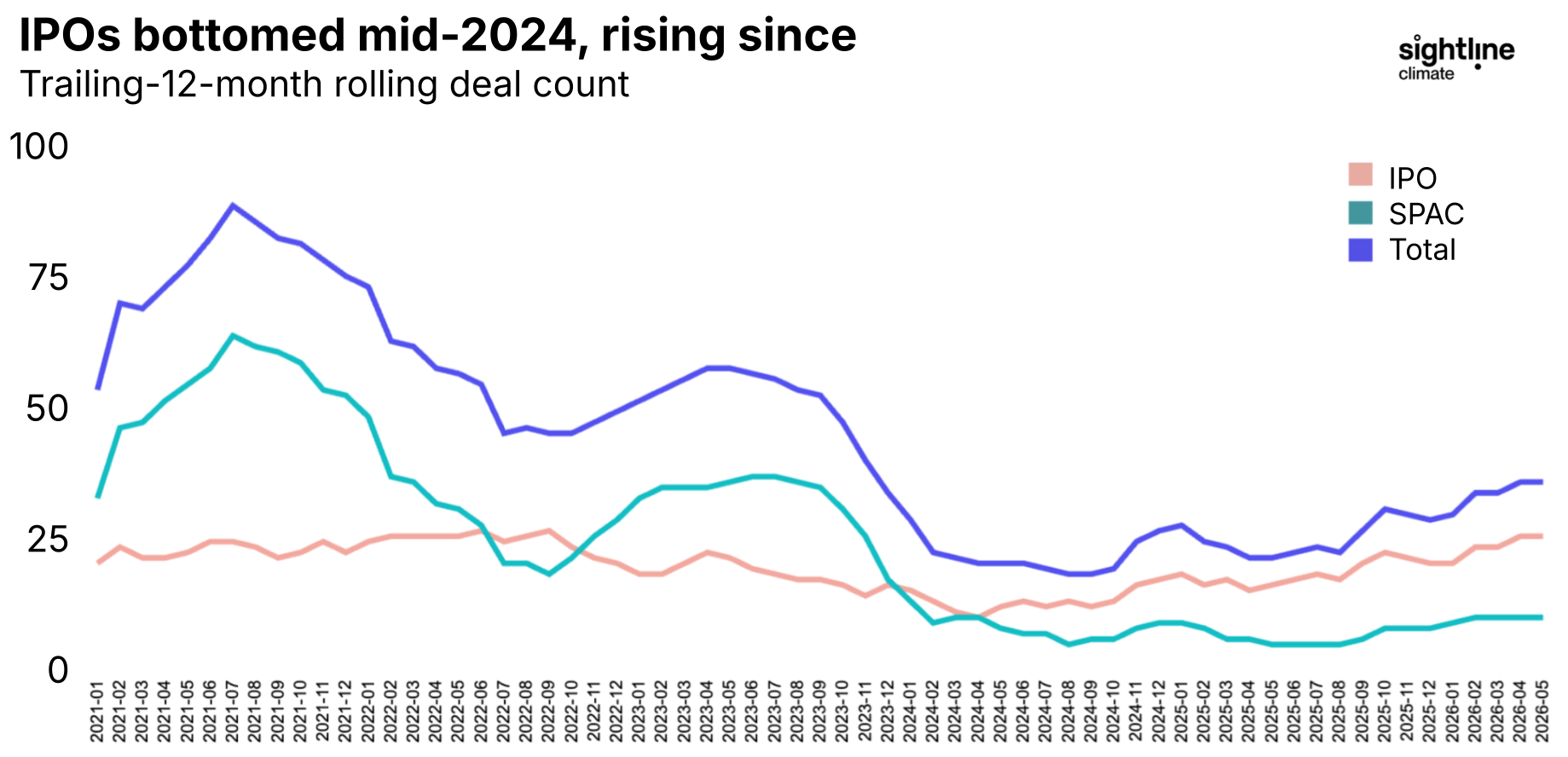

Three years after the SPAC boom busted and took EV darlings with it, public markets are welcoming climate tech companies again. Is this different, or is it déjà vu? We ran the numbers.

What happened

Twelve-month rolling climate tech public listings bottomed in mid-2024 at 18. By May 2026 they were back up to 35 -- an 83% increase off the trough, per Sightline Climate data. This time, it's almost entirely an IPO story, not just SPACs. Conventional IPOs more than doubled from their 2024 trough of around 10-11 to 25 by May 2026. SPACs have crept back too, but many of the recent announcements in fusion -- Newcleo, TAE Technologies, General Fusion -- have been announced without closing yet.

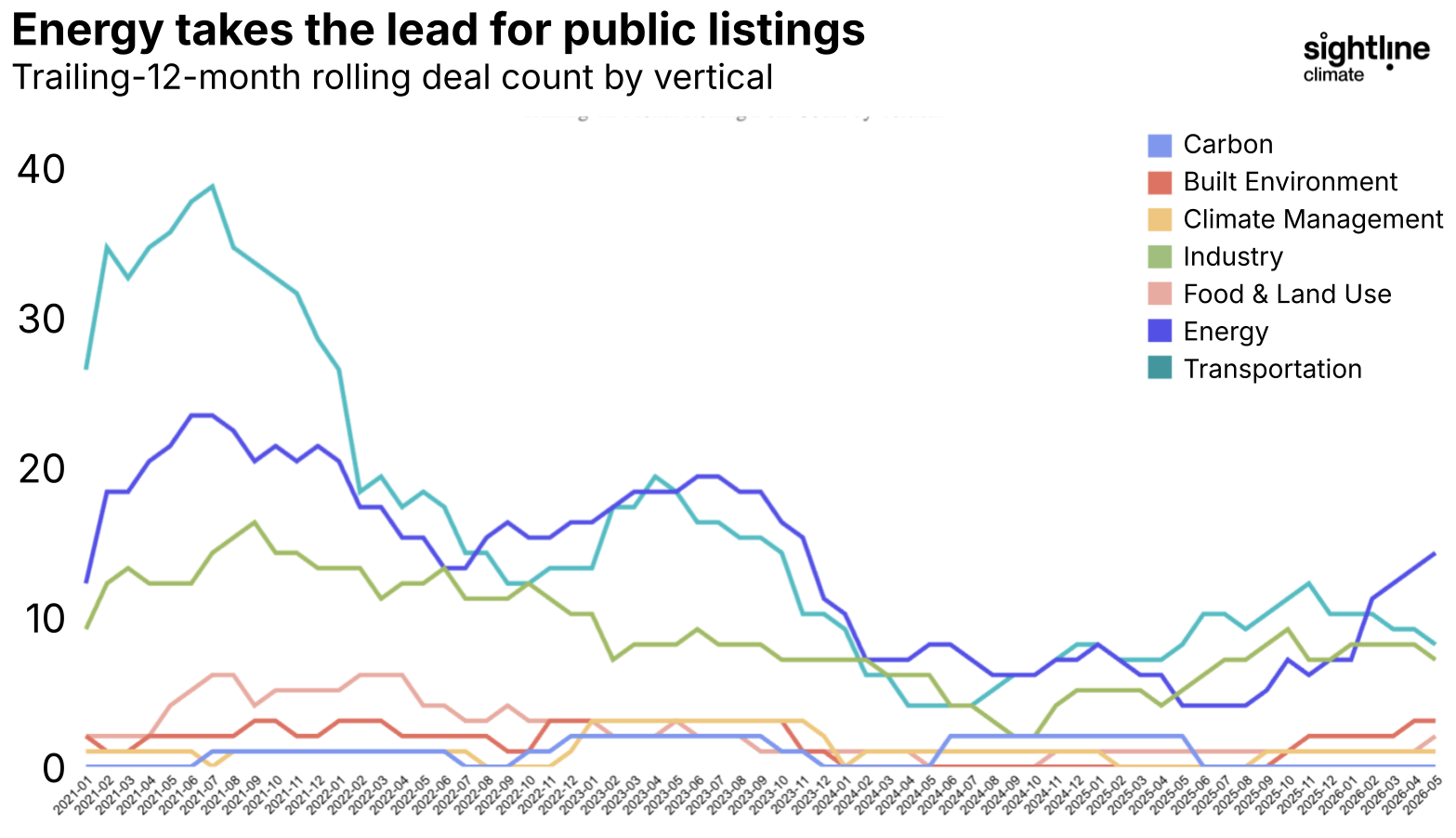

By vertical, the 2021 boom was mostly a transportation story. EV companies dominated the SPAC wave and fell hardest when it collapsed. Today, energy has run away as the leading vertical, from 8 TTM listings in mid-2024 to 14 by May 2026. Transportation is roughly flat.

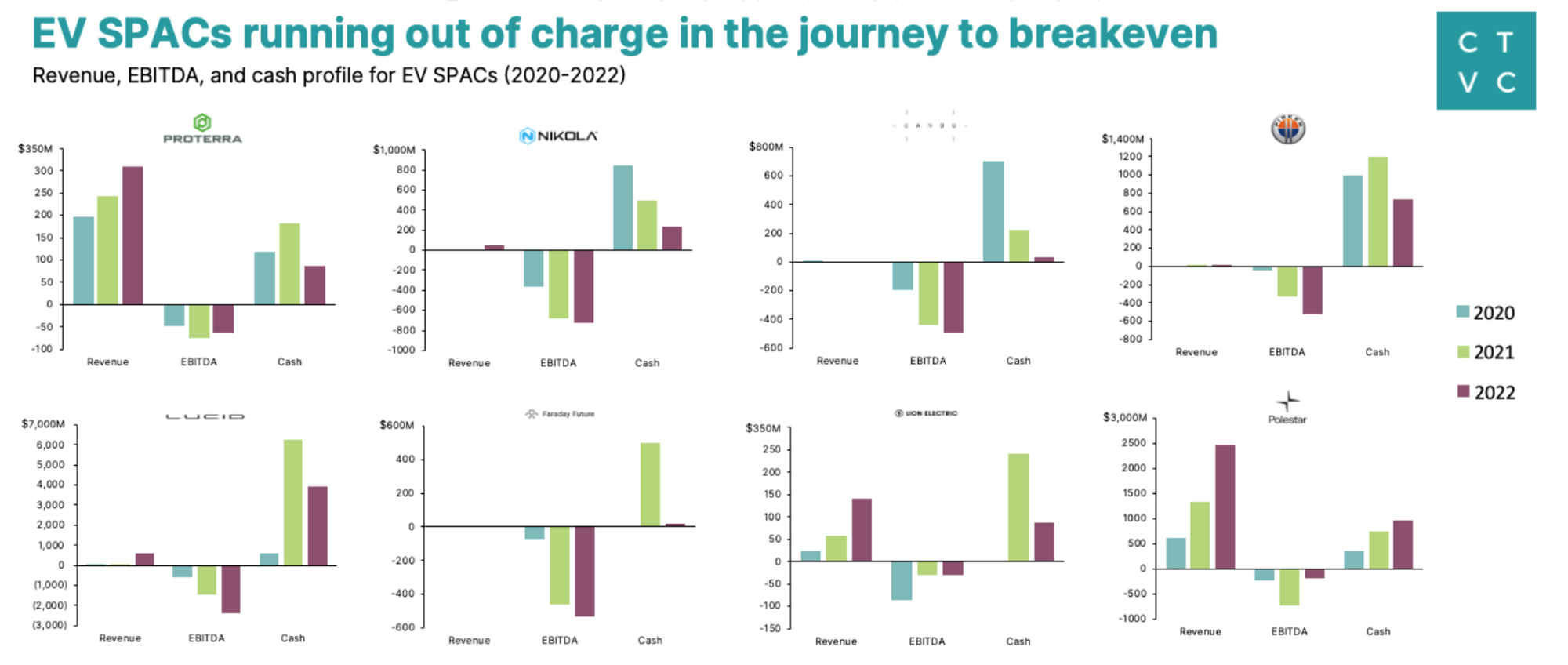

So is it 2022 all over again? Our chart from that time shows the wild west of that market. And this was before Fisker went bankrupt and Nikola's founder went to prison.

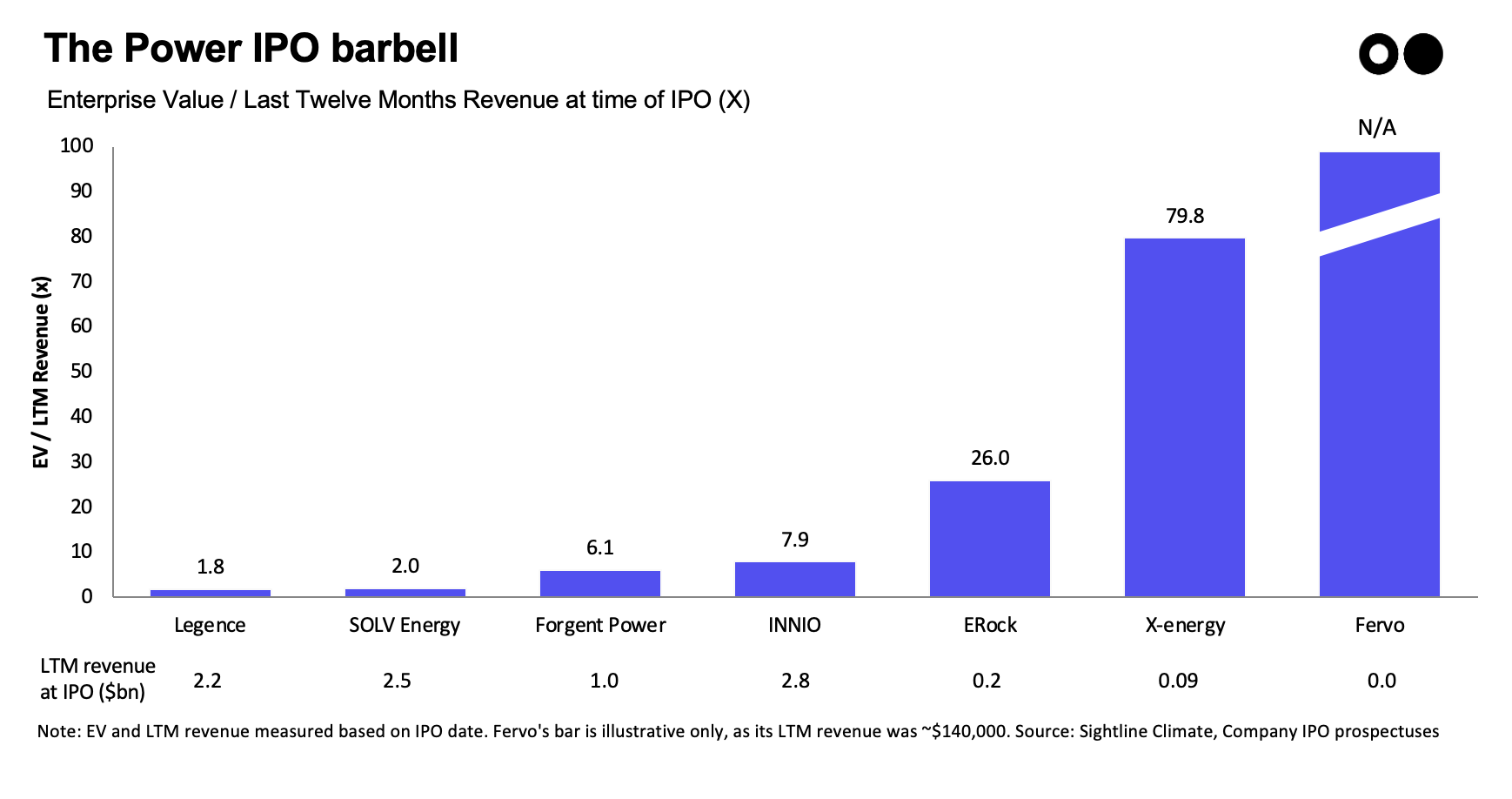

Today, the high-profile names -- X-energy ($11.5bn market cap at debut), Fervo Energy ($12.4bn) -- are getting most of the headlines, including from us (in January, last month, and just two weeks ago). Still, most of this wave of nuclear and geothermal bets will come online at scale post-2030. And the fusion companies, well, everyone knows the joke. The offtake contracts being announced are real (Fervo’s got a reported $7.2bn potential backlog of contracted revenue), but the faster the delivery, the better. Speed to power is the constraint data centers actually care about.

There’s a second bucket of quieter but arguably more commercially grounded energy or energy-adjacent companies also riding the wave: Legence, Solv Energy, Forgent Power, Innio, Enchanted Rock (now ERock). These are power services and equipment companies – they fit less neatly into the "advanced clean firm power" narrative, but they can deploy today, and they have direct exposure to the data center wave right now, not next decade.

Of seven power and energy names that have hit the public markets in the past nine months, they split into a clean barbell. On one end, the mature equipment, services providers, and developers - Legence, SOLV Energy, Forgent, INNIO, and ERock - demonstrated $1-3bn of trailing revenue (with the exception of ERock) and priced at an average 8.8x EV/revenue at IPO. On the other end, deeptech generation plays sell backlog and future growth: X-energy went public at roughly 80x revenue, and Fervo at ~41,000x, on ~$140k of revenue.

Key takeaways

🛰️ ICEYE, an Espoo, Finland-based synthetic aperture radar (SAR) satellite developer, raised $521m in Growth funding from General Atlantic, Ilmarinen Mutual Pension Insurance, Lifeline Ventures, Nokia, Qatar Investment Authority, and other investors.

⚡ GPS Renewables, a Bangalore, India-based renewable oil and gas and compressed biogas (CBG) platform, raised $66m in Series C funding from PixelSky Capital, Indian Oil Corporation, Sojitz, and Spectrum Impact.

🐛 InnovaFeed, a Paris, France-based insect protein and animal nutrition developer, raised $59m in Series D funding from abc Impact, ADM, Creadev, FFC Capital, Qatar Investment Authority, and other investors.

🚆 CameraMatics, a Dublin, Ireland-based AI-powered fleet safety and efficiency platform provider, raised $57m in Series B funding from Blume Equity, Goodbody, and Ireland Strategic Investment Fund (ISIF).

⚡ Endurance Energy, a Seattle, WA-based seafloor geothermal energy developer, raised $54m in Series A funding from Founders Fund, Ascend VC, Construct Capital, Felicis, First Round Capital, and other investors.

🚗 Evotrex, a Los Angeles, CA-based off-grid RV energy systems developer, raised $30m in Series A funding from Anker Innovations, Forebright Concerto Capital, GSR United Capital, Pegasus Capital (Japan), and TTGG Ventures.

🔋 Eclipse, a Paris,France-based battery energy storage platform provider, raised $23m in Series A funding from BNP Paribas, Noria, and Wind Capital.

⚡ Exponent Energy, a Bengaluru, India-based EV rapid-charging energy platform, raised $21m in Series B funding from 360 One Asset Management, TDK Ventures, 3one4 Capital, AdvantEdge Founders, Eight Roads Ventures, and other investors.

🌾 Leaf Agriculture, a Los Angeles, CA-based agricultural data infrastructure platform raised $13m in Series B funding from Leaps by Bayer.

🏠 GALVANY, a Berlin, Germany-based integrated smart heating systems provider, raised $12m in Seed funding from AENU and SET Ventures.

⚡ Pathway Power, a San Diego, CA-based renewable energy project developer, raised $150m in Debt funding from AB CarVal.

🔋 DRI, an Amsterdam, Netherlands-based European renewable energy developer, raised $127m in PF Debt funding from Erste Bank Polska, PKO Bank Polski, and UniCredit.

⚡ IB Vogt, a Berlin, Germany-based utility-scale solar and battery storage developer, raised $36m in PF Debt funding from Rizal Commercial Banking Corporation (RCBC).

⚡ Alinta Energy, a Sydney, Australia-based electricity and gas company, was acquired by Sembcorp Industries for $4.3bn.

🏠 ERock, a Houston, TX-based integrated resilient power infrastructure provider, announced an IPO raising $600m at an implied valuation of $4.7bn.

⚡ Brightfield AI, a New York, NY-based AI platform for battery deployment, was acquired by Voltus for an undisclosed amount.

☀️ Vanguard Energy Partners, a Somerville, NJ-based solar installation designer and builder, was acquired by QE Solar for an undisclosed amount.

This is a sample of deals available for Sightline clients. Can’t get enough deals?

🤝 The US and Iran agreed to a 60-day ceasefire extension and framework for nuclear talks, with a formal signing expected Friday in Switzerland. The Strait of Hormuz, which handled ~20% of global oil and LNG before the conflict, is set to reopen, though full shipping volumes won't return immediately given mine-clearing and infrastructure work. Nuclear enrichment, uranium disposal, and sanctions relief are all left to negotiate in the 60-day window. Meanwhile, US inflation rose to a 3-year high on the spiking energy prices. [Link, link, link]

⚡ The UK is planning to extend its nuclear reactor, Sizewell B, through 2055 at £70/MWh ($93.85). Sizewell B is the only UK reactor forecast to stay online past March 2030, with Hinkley Point C unlikely to generate before then and Sizewell C further out still. [Link]

☢️ In more nuclear news, Japan proposed replacing up to 14 nuclear reactors, and Russia began construction on its SMR project in Uzbekistan, the first commercial-scale project. [Link, link]

🏭 Danish cementmaker Aalborg Portland signed a 15-year contract with the Danish Energy Agency for ~$2.6bn to capture, transport, and store up to 1.25m tons of CO2 annually starting in 2030. At 875 crowns per captured ton, it's the largest industrial CCS subsidy deal in Europe, and it covers more than half of Denmark's national CCS pool target of 2.3m tons/year. [Link]

🔋 GM is developing its own sodium-ion battery tech, with prototype cells under development, and grid-scale storage in its sights. Worth contrasting with CATL's 60GWh HyperStrong order from a few weeks back. GM is at prototype-in-R&D-facility stage; China is at GWh-scale supply agreements. [Link, link]

💨 JPMorgan signed a carbon offtake financing deal with Charm Industrial, providing project-level debt financing for Charm's liquid biomass injection CDR. It’s a bet on diversifying the tech types behind CDR. [Link]

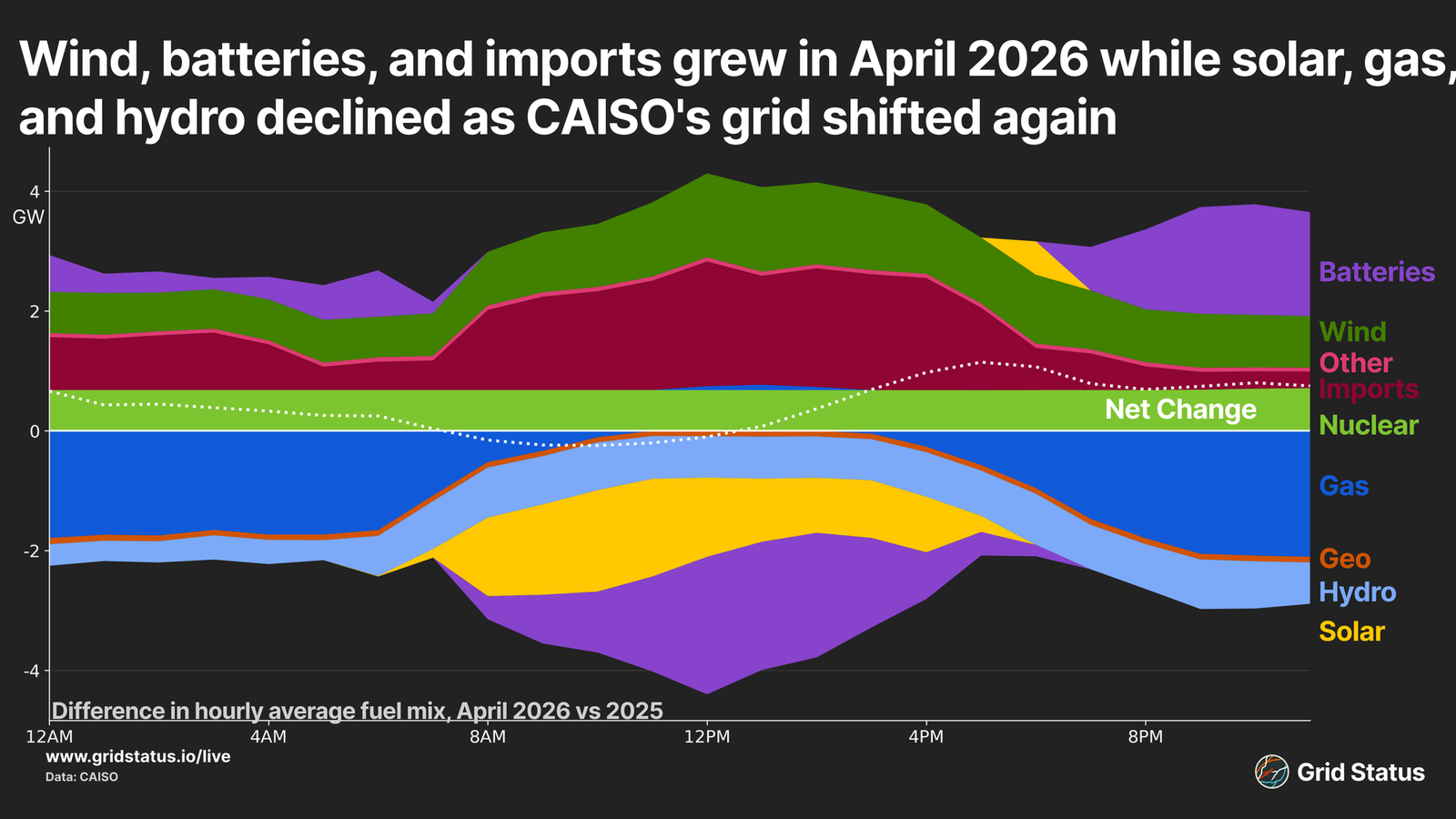

☀️ California’s energy mix in April looked very interesting. It was the first YoY solar generation decline in years driven by a ~2 GW curtailment spike at peak, SunZia coming online in stages behind the wind records, and batteries now discharging dusk-to-dawn. [Link]

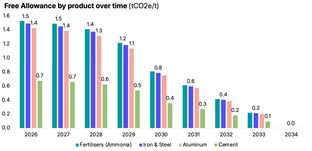

🏛 EU considers weakening its ETS to support industrial investment and competitiveness. Using ETS revenue and free allowance flexibility as an industrial subsidy, the EU is hoping to keep European manufacturing affordable and competitive against China. [Link]

🚗 Chinese EV exports to Europe up 73% year-over-year, with BYD now investing heavily in European charging and dealer infrastructure. [Link, Link]

📅 Corporate Offtake Driving Climate Innovation: On Jun 24 in London, Blue Earth and HSBC bring together corporates looking to commit to emerging climate technology projects. Hear from Sightline's Head of Research Julia Attwood and HSBC UK's Head of Climate Change Tim Lord, plus companies already putting offtake agreements into practice.

📅 Trellis Impact 26: From Jun 23-25 in San Francisco, Trellis Impact brings together 3,500+ leaders powering the future of sustainable business, from AI-enabled solutions to emerging technologies reshaping decarbonization, energy, circularity, and beyond. Get practical insights and hard-won examples of the technologies and strategies that are influencing sustainable business transformation. Get 20% off with our partner code: TI26SCP

💡 E8's Decarbon8 Fund: Apply by 18 Jun if you’re an early-stage companies building climate resilience solutions across grid, water, and food, for equity investment in mid-October 2026.

Senior Manager / Director, Communications @Carbon Removal Canada

Finance & Ops AI Lead – Associate @Keyframe

Software Engineer @Althea

📩 Feel free to send us deals, announcements, or anything else at [email protected]. Have a great week ahead!

Our new report ft. low-carbon data center megadeals, reopened public markets, and rise of adaptation

Newsletter

Newsletter